Payday loans are a fast road to financial devastation. The interest rates are crippling and the loans are designed to force you into a cycle of never-ending debt. People still use these loans, mainly because they are desperate for cash and don’t see any other way to get it. There are payday loan alternatives, and these are some of the best.

Best Payday Loan Alternatives

People with bad credit scores need to borrow money just as much as, if not more than everyone else. Unfortunately, their credit options are limited, as traditional lenders are generally reluctant to work with them.

Payday loans are a convenient solution to that problem. Regardless of your credit score, you can walk into a payday lender’s store with a post-dated check and walk out an hour later with cash to pay your bills.

The only problem is that the finance charges are so excessive that you’ll likely struggle to pay off the debt. In other words, payday loans would be a perfect solution to your problems if they weren’t so expensive. Instead of looking for the cheapest payday loan, it’s better to look for an alternative.

From that, we can deduce that the ideal payday loan alternatives would meet the following requirements:

- Available to people with bad credit

- Fund quickly in an emergency

- Affordable enough to be manageable

Of course, they also have to be realistic. I’m always a little annoyed when I see articles recommending that you dip into your emergency savings or ask your family and friends for money in an emergency.

If you had cash in a savings account or a family member who wanted to pay your bills, you wouldn’t be considering a payday loan in the first place. Instead, we’ll focus on more practical payday loan alternatives.

1. Credit Union Payday Alternative Loan

There’s really such a thing as a payday alternative loan (PAL). Payday loans are so bad for consumers that the National Credit Union Administration (NCUA) created the PAL program in 2019 to replace them.

PALs are what payday loans should be. They’re short to medium-term accounts for people with bad credit that need relatively small amounts of money at an affordable rate. PALs range from $200 to $1000, but the amount you can borrow will be based on your income.

PAL repayment terms are between one and 12 months, their finance charges are capped at 28% APR, and there are absolutely no rollovers allowed. This makes them a much cheaper and safer alternative to traditional payday loans.

In 2019 the NCUA created PAL II, a second PAL option, which allows loans up to $2000 with payment terms of up to 12 months. Your loan amount and term may be lower at the discretion of your credit union, and you can only have one PAL at a time.

The only catch is you must be a member of a federal credit union that offers PALs to be eligible for one. You won’t need good credit, but you do have to demonstrate that you have enough income to pay your debt. There are now national credit unions that anyone can join, which can be a great alternative to traditional banks.

2. Cash Advance Apps

One product of the fintech industry that’s become popular in recent years is the cash advance app. These apps are viable payday loan alternatives. Essentially, they let you tap into the earnings you accrue at your place of employment before you would otherwise receive a paycheck. Usually, they let you take out a few hundred dollars or so, similar to the size of a payday loan.

👉 For example

Say you make $4,000 per month after taxes and receive a $2,000 paycheck every two weeks. After the first week of the month expires, you’d have earned $1,000, but you wouldn’t get paid for another week.

With a cash advance app like Earnin’, you’d be able to borrow a few hundred dollars of those funds regardless of your credit score, then pay off the balance the following week when you receive your wages.

Some other apps, like Dave and Brigit, allow you to take out small short-term loans, paid with your next paycheck. In some cases, these are interest-free, though you will pay a small monthly fee to use the app.

There generally isn’t a credit check to sign up for these apps, and many offer their services for free. If they do charge something, it’s often just a small monthly membership fee.

☝️ You need to have an active account to draw cash from these apps, so they aren’t a solution if you need money right now.

3. Bad Credit Personal Loans

Generally speaking, traditional lenders don’t want to give money to someone with bad credit. That’s what pushes so many people to take out payday loans, thinking that they could never qualify for any other form of financing.

While it’s true that a bad credit score prevents you from accessing the best credit accounts, it doesn’t mean payday lenders are your only option. You may be able to qualify for a personal loan for bad credit through an online lender that’s somewhat more affordable. Online lenders are generally less strict than traditional financial institutions like banks.

For example, personal loans through Upgrade have APRs from 8.49% to 35.99%. Your loan won’t be cheap if you end up at the high end of that range, but you would avoid paying triple-digit interest rates.

4. Debt Relief Options

In general, the only way to end up with a low credit score is by misusing debt accounts. For example, you might’ve borrowed more than you could afford, missed some of your monthly payments, and defaulted on one of your loans.

As a result, many people considering payday loans are feeling hard-pressed partially because they’re struggling with the monthly payments on other outstanding debts.

If you’re in that situation, seeking debt relief to free up some extra cash flow is a viable alternative to taking out a payday loan. For example, you could sign up for credit counseling. They’ll often try to negotiate better terms with your creditor or establish a more affordable payment plan for you.

📕 Learn More: For more insight into the various types of debt relief out there, take a look at our comprehensive guide: Debt Relief Options: Which One Should You Use?

5. Medical Bill Assistance

The overwhelming cost of healthcare in America is another reason people struggle financially and consider resorting to payday loans. Much like debt relief, medical bill assistance is a great way to free up some cash and avoid having to do so.

Fortunately, there’s a significant number of governmental programs and private organizations dedicated to helping people afford healthcare. If medical bills are part of your financial difficulties, consider seeking help instead of taking on more debt.

📕 Learn More: For a detailed guide to getting assistance with your medical debt, take a look at our dedicated resource: 17 Ways to Get Help Paying Medical Bills in 2024

5. Nonprofits and Charities

People who consider payday loans often do so because they’re in dire straits through no fault of their own. For example, single mothers, veterans, the elderly, and the disabled are often especially financially vulnerable, and it’s not fair that they should have to take out payday loans to stay afloat.

Fortunately, there are plenty of nonprofit organizations and charities out there ready to help such people in need. It’s okay to ask for help sometimes, especially if you’re struggling financially due to unfortunate circumstances. Consider reaching out to a group that can help you put food on the table and keep a roof over your head.

💡 In many areas, especially low-income neighborhoods, local churches have active programs designed to help residents avoid or escape the payday loan trap.

6. Long-Term Solutions

The payday loan alternatives above are significantly better short-term solutions to sudden cash shortages than payday loans. However, they’re still a bit like slapping a bandaid on the bruises you used to get from the bully on the way home from school.

In other words, they don’t really fix the heart of the issue. They’re only a short-term solution. So once you get past your latest cash crunch, keep going. Take action to address the imbalance in your finances and stop living paycheck to paycheck.

Find ways to increase your income or reduce your expenses until you have some cash left over each month, then put that money to work. Use it to pay down your debts, build an emergency fund, and start investing. Otherwise, the next time you have an unexpected emergency, you’ll end up right back in the same situation.

Why You Should Avoid Payday Loans

A recent study found that a whopping 78% of Americans live paycheck to paycheck.[1] If you’re among them, you are operating on such a thin margin that even a single surprise expense could send you scrambling to take out a loan.

If you have good credit, that’s not such a bad thing. You’ll qualify for loans at reasonable interest rates. People with no credit score or bad credit often resort to payday loans. Unfortunately, those often trap their borrowers in a cycle of debt.

Payday loans are short-term, high-interest loans allegedly designed to help people with bad credit get fast cash in an emergency. Their quick funding timelines and virtually non-existent qualification requirements make them incredibly convenient.

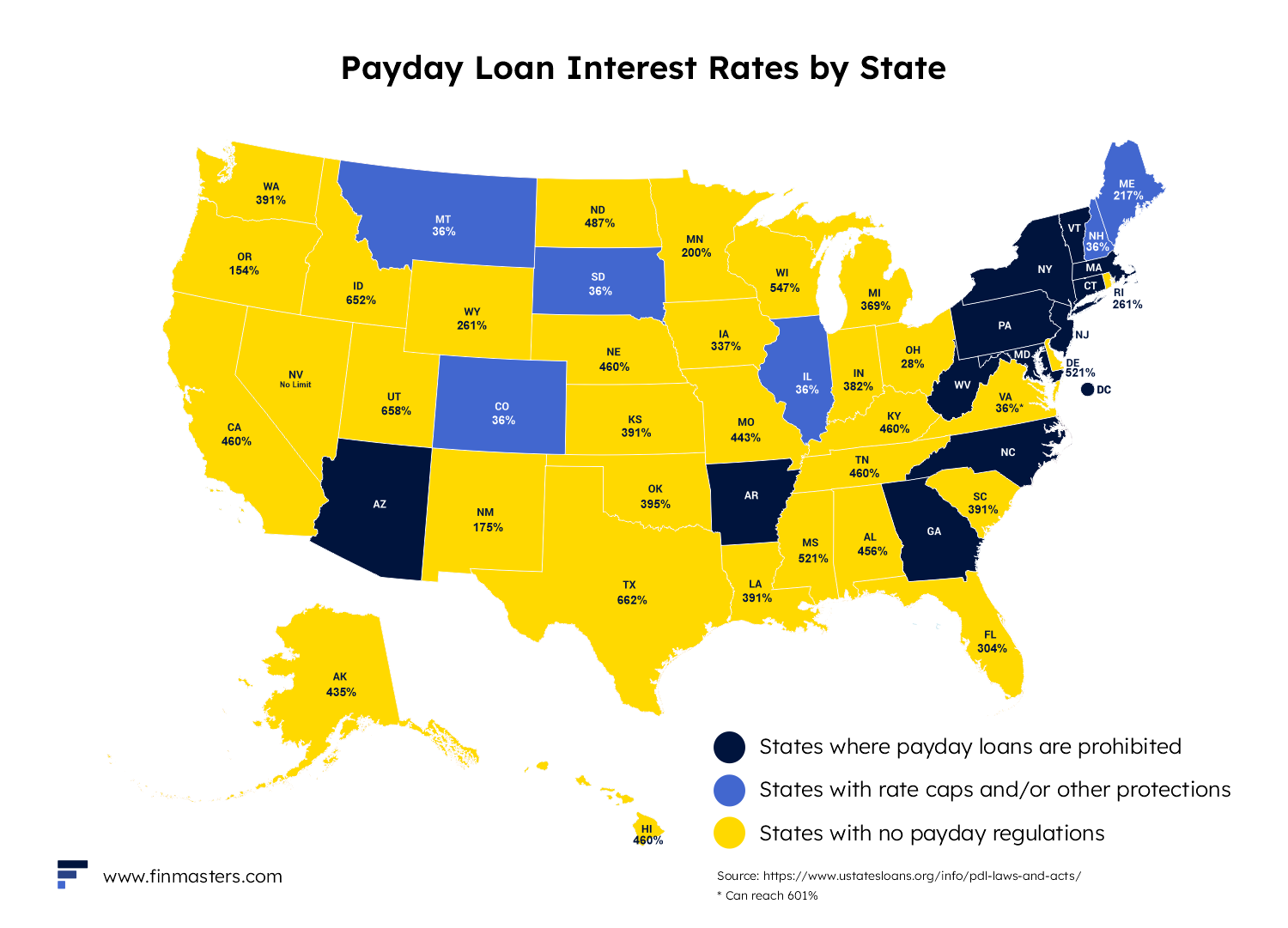

However, they’re so expensive that they often cause more problems for their users than they solve. Payday loan rates can range from uncomfortably high to downright outrageous, depending on the laws in your state.

👉 For example

Legislators in Oregon have significantly restricted payday lenders, but they haven’t forbidden them altogether. As a result, a $300 payday loan from Check Into Cash in Oregon costs $39.17, which works out to a 153.73% annual percentage rate (APR) over their standard 31-day repayment term.

Meanwhile, there are almost no consumer protections in Utah, and a $300 payday loan from Check Into Cash in the state costs $75. That works out to a ridiculous 912.5% APR over the shortest local repayment term, which is just ten days.

👉 For context, personal loan interest rates typically range from 3% to 36%, with the average currently around 11.91%[2].

As you can see, even the cheapest payday loan rates dwarf that, and the most expensive ones are worse by multiple orders of magnitude.

The Cycle of Debt

A single payday loan can be frustratingly expensive, but it’s unlikely to ruin your life if you manage to pay it off on time. The real danger of the industry begins when you can’t because the costs are so high.

If you inform your payday lender that you can’t afford your loan payment, they’ll often let you extend the due date for another two weeks. In exchange, you pay a “rollover” fee that’s comparable to the original finance charge.

Of course, when the due date comes around again, it’s just as unlikely that you’ll be able to pay as it was the last time. If you can’t, the payday lender will charge you once more and extend the due date again. In some states, that can continue indefinitely.

Though the data is several years old now, the Consumer Financial Protection Bureau (CFPB) once found that 80% of payday loans get rolled over[3]. In addition, 60% of payday loan borrowers do so a whopping seven or more times in a row.

👉 For example

Say John takes out that $300 payday loan from Check Into Cash in Utah and owes a $75 finance charge. A week and a half later, he realizes he can’t pay $375 by the due date, so he eats a $75 rollover fee and gets another two weeks of breathing room.

If he were to repeat the process six more times, he’d end up paying $600 in rollover fees and finance charges to borrow that initial $300.

Conclusion

As we’ve journeyed through the seven payday loan alternatives, it’s clear that there are viable options out there to manage financial challenges without falling into the pitfalls of high-cost payday loans. From the structured, lower-interest opportunities of credit union alternatives and cash advance apps, to the support offered by nonprofits and long-term strategies, these solutions are designed to provide relief and foster financial stability.

Remember, the key is to choose the option that aligns best with your specific financial situation. Whether it’s a short-term fix you need or a strategy to overhaul your financial health, these alternatives offer a safer and often more affordable path than traditional payday loans. Take the time to evaluate each option carefully, considering your current needs and future financial goals.

Learn More: If you need help figuring out how to earn more or spend less so you can start saving money, take a look at the resources below: