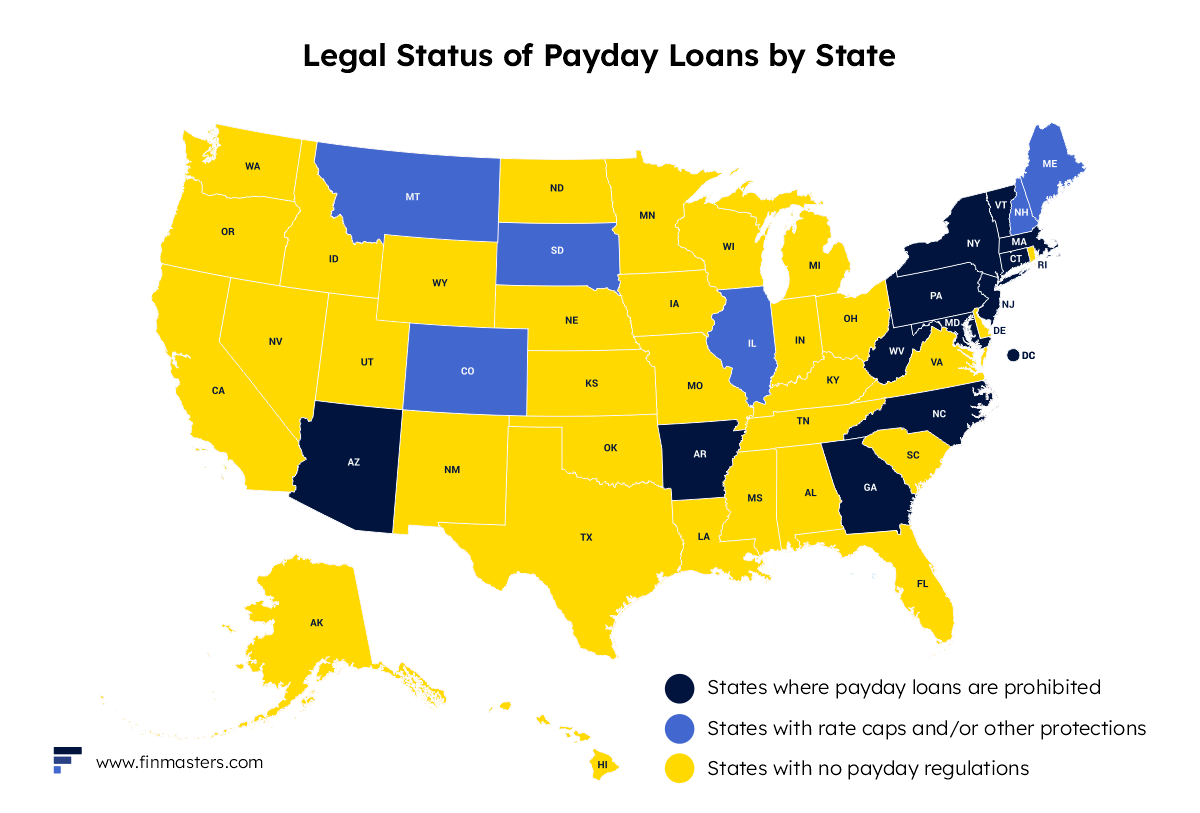

The legal status of payday loans differs significantly across the United States, with each state having its own set of laws and regulations. Some states ban payday lending altogether. Some states allow payday loans with some restrictions. Others have no restrictions at all.

Here’s a quick summary of the status of payday loans in all 50 states, followed by a closer look at the laws in each state.

| State | Payday Lending Legal Status | Max. Loan Amount |

|---|---|---|

| Alabama | Legal | $500 |

| Alaska | Legal | $500 |

| Arizona | Prohibited | – |

| Arkansas | Prohibited | – |

| California | Legal | $300 |

| Colorado | Legal with restrictions | $500 |

| Connecticut | Prohibited | – |

| Delaware | Legal | $1000 |

| District of Colombia | Prohibited | – |

| Florida | Legal | $500 |

| Georgia | Prohibited | – |

| Hawaii | Legal | $600 |

| Idaho | Legal | $1000 |

| Illinois | Legal with restrictions | $1000 |

| Indiana | Legal | $605 |

| Iowa | Legal | $500 |

| Kansas | Legal | $500 |

| Kentucky | Legal | $500 |

| Louisiana | Legal | $350 |

| Maine | Legal with restrictions | None |

| Maryland | Prohibited | – |

| Massachusetts | Prohibited | – |

| Michigan | Legal | $600 |

| Minnesota | Legal | $350 |

| Mississippi | Legal | $500 |

| Missouri | Legal | $500 |

| Montana | Legal with restrictions | $300 |

| Nebraska | Legal | $500 |

| Nevada | Legal | 25% gross monthly income |

| New Hampshire | Legal with restrictions | $500 |

| New Jersey | Prohibited | – |

| New Mexico | Legal | $5000 |

| New York | Prohibited | – |

| North Carolina | Prohibited | – |

| North Dakota | Legal | $500 |

| Ohio | Legal | $1000 |

| Oklahoma | Legal | $500 |

| Oregon | Legal | $50,000 |

| Pennsylvania | Prohibited | – |

| Rhode Island | Legal | $500 |

| South Carolina | Legal | $550 |

| South Dakota | Legal with restrictions | $500 |

| Tennessee | Legal | $500 |

| Texas | Legal | n/a |

| Utah | Legal | None |

| Vermont | Prohibited | – |

| Virginia | Legal | $2,500 |

| Washington | Legal | $700 or 30% of gross monthly income |

| West Virginia | Prohibited | – |

| Wisconsin | Legal | $1500 or 35% of income |

| Wyoming | Legal | None |

💡 Payday loans are convenient, but they cost much more than many borrowers can afford. Consider these payday loan alternatives instead.

Payday Loan Regulations by State

If you are trying to pay off a payday loan, it’s important to be familiar with the laws governing payday loans in your state. Many online payday lenders are not licensed in all of the states in which they operate. Both online and physical payday lenders may violate state laws.

☝️ If your payday loan is illegal you may not be required to pay it back.

Payday lenders who are members of the Community Financial Services Association of America are required to meet certain standards, including offering extended payment plans to borrowers who cannot pay their loans on time. These standards apply even in states that do not regulate payday loans.

Let’s dive a little deeper into what regulations apply for each state.

AL | AK | AZ | AR | CA | CO | CT | DE | DC | FL | GA | HI | ID | IL | IN | IA | KS | KY | LA | ME | MD | MA | MI | MN | MS | MO | MT | NE | NV | NH | NJ | NM | NY | NC | ND | OH | OK | OR | PA | RI | SC | SD | TN | TX | UT | VT | VA | WA | WV | WI | WY

Alabama

Payday loans are legal in the state of Alabama.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 10 days (minimum) – 31 days (maximum)

- Finance Charges for $100 (14-day loan): $17.50

- APR for 14-day $100 Loan: 456%

- Number of outstanding loans permitted: Any as long as the total amount advanced doesn’t exceed $500

- Rollovers allowed: 2

- Repayment Plan: If the customer can’t repay the outstanding balance in full, he can receive an extended repayment option of four equal monthly installments of the remaining balance.

- Criminal Action: Prohibited unless the check is returned due to a closed account.

Complaints & Information

To get more information about lending regulations you can visit the Alabama State Banking Department website.

To check if your payday lender is licensed in the state of Alabama you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Alabama here: https://banking.alabama.gov/con_affairs/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Alaska

Payday loans are legal in the state of Alaska.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 14 days (minimum)

- Finance Charges for $100 (14-day loan): $20

- APR for 14-day $100 Loan: 521%

- Number of outstanding loans permitted: Unknown

- Rollovers allowed: 2

- Repayment Plan: Unknown

- Criminal Action: The licensee cannot threaten an advance recipient with criminal action because of the recipient’s default.

Complaints & Information

To get more information about lending regulations you can visit the Alaska Division of Banking and Securities website.

To check if your payday lender is licensed in the state of Alaska you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Alaska here: https://www.commerce.alaska.gov/web/consumerservices.aspx

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Arizona

Payday loans are prohibited in the state of Arizona.

Arkansas

Payday loans are prohibited in the state of Arkansas.

California

Payday loans are legal in the state of California.

- Payday lending status: Legal

- Maximum Loan Amount: $300

- Loan Term: 31 days (maximum)

- Finance Charges for $100 (14-day loan): $17.65

- APR for 14-day $100 Loan: 460%

- Number of outstanding loans permitted: None

- Rollovers allowed: One

- Repayment Plan: The customer may receive an extension of time to repay an existing deferred deposit transaction without being charged any additional fee or charged of any kind in addition to the extension or payment plan.

- Criminal Action: The licensee cannot prosecute a customer in a criminal action in conjunction with a deferred deposit transaction for a returned check or to threaten with prosecution.

Complaints & Information

To get more information about lending regulations you can visit the California Department of Financial Protection and Innovation website.

To check if your payday lender is licensed in the state of California you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in California here: https://dfpi.ca.gov/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Colorado

Payday loans are legal in the state of Colorado.

- Payday lending status: Legal but effectively outlawed

- Maximum Loan Amount: $500

- Loan Term: 6 months (minimum)

- Finance Charges: 20% of the first 300$, 7.5% of any amounts higher than $300

- APR: 36%

- Number of outstanding loans permitted: Unlimited, as long as the total balance is less than $500

- Rollovers allowed: One

- Repayment Plan: Not Specified.

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Colorado Office of the Attorney General website.

To check if your payday lender is licensed in the state of Colorado you can perform a License Search online.

The licenses can be found in PDF under the “Active Supervised Lenders” link in the sidebar.

You can find all the information on how to submit a complaint about a payday lender in Colorado here: https://coag.gov/file-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Connecticut

Payday loans are prohibited in the state of Connecticut.

Delaware

Payday loans are legal in the state of Delaware.

- Payday lending status: Legal

- Maximum Loan Amount: $1000

- Loan Term: 60 days (maximum)

- Finance Charges for 14-day $100 Loan: No limit

- APR for 14-day $100 Loan: No limit

- Number of outstanding loans permitted: No more than 5 short-term consumer loans from all licensees in a 12-month period.

- Rollovers allowed: 4

- Repayment Plan: Payments in equal installments over a period of at least 90 days.

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Delaware Office of the State Bank Commissioner website.

To check if your payday lender is licensed in the state of Delaware, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Delaware here: https://banking.delaware.gov/consumer-complaints/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

District of Colombia

Payday loans are prohibited in the District of Colombia.

Florida

Payday loans are legal in the state of Florida.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 7 days (minimum) – 31 days (maximum)

- Finance Charges for $100 (14-day loan): $15

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: 1

- Rollovers allowed: None

- Repayment Plan: 60 days after the original termination date, without any additional fee.

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Florida Office of Financial Regulation website.

To check if your payday lender is licensed in the state of Florida, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Florida here: https://www.flofr.gov/sitePages/FileAComplaint.htm

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Georgia

Payday loans are prohibited in the state of Georgia.

Hawaii

Payday loans are legal in the state of Hawaii.

- Payday lending status: Legal

- Maximum Loan Amount: $600

- Loan Term: 32 days (maximum)

- Finance Charges for $100 (14-day loan): $17.65

- APR for 14-day $100 Loan: 460%

- Number of outstanding loans permitted: 1

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints and Information

To get more information about lending regulations you can visit the Hawaii Department of Commerce and Consumer Affairs website.

To check if your payday lender is licensed in the state of Hawaii, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Hawaii here: http://cca.hawaii.gov/consumer-complaints/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Idaho

Payday loans are legal in the state of Idaho.

- Payday lending status: Legal

- Maximum Loan Amount: $1000 / 25% of gross monthly income

- Loan Term: 32 days (maximum)

- Finance Charges for $100 (14-day loan): $17.65

- APR for 14-day $100 Loan: 521%

- Number of outstanding loans permitted: Not Specified

- Rollovers allowed: 3

- Repayment Plan: 60-day extended payment plan with at least 4 equal payment installments

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Idaho Department of Finance website.

To check if your payday lender is licensed in the state of Idaho, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Idaho here: https://www.finance.idaho.gov/complaint-guidance/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Illinois

Payday loans are legal (but with strict restrictions) in the state of Illinois.

- Payday lending status: Legal but with restrictions

- Maximum Loan Amount: $1000 / 25% of gross monthly income

- APR: 36%

- Number of outstanding loans permitted: No loan made to a customer with an outstanding balance on 2 payday loans.

- Rollovers allowed: Prohibited

- Repayment Plan: 55-day extended payment plan to repay in installments

- Criminal Action: Prohibited

The Predatory Loan Prevention Act signed in 2021 by Governor J.B. Pritzker, caps the interests rates on payday loans to 36% APR, thus allowing lenders to offer small loans similar to payday loans, but the annual percentage rate cannot exceed 36%.

Complaints & Information

To get more information about lending regulations you can visit the Illinois Department of Financial and Professional Regulation website.

To check if your payday lender is licensed in the state of Illinois, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Illinois here: https://www.idfpr.com/Admin/Complaints.asp

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Indiana

Payday loans are legal in the state of Indiana.

- Payday lending status: Legal

- Maximum Loan Amount: $605 / 20% of gross monthly income

- Loan Term: 14 days (minimum)

- Finance Charges for 14-day $100 Loan: 15% (first $250), 13% (on next $150), $10 (final $150)

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: 1

- Rollovers allowed: None

- Repayment Plan: at least 60-day extended payment plan with at least 4 equal payment installments

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Indiana Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Indiana, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Indiana here: https://www.in.gov/dfi/file-a-complaint/where-do-i-file-my-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Iowa

Payday loans are legal in the state of Iowa.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 31 days (maximum)

- Finance Charges for 14-day $100 Loan: $15 (first $100), $10 (next $100)

- APR for 14-day $100 Loan: 337%

- Number of outstanding loans permitted: 2

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Iowa Division of Banking website.

To check if your payday lender is licensed in the state of Iowa, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Iowa here: https://www.idob.state.ia.us/bank/docs/comscomp.aspx

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Kansas

Payday loans are legal in the state of Kansas.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 7 days (minimum) – 30 days (maximum)

- Finance Charges 7-day Loan: 15% of the balance of the loan

- APR for 7-day Loan: 782%

- Number of outstanding loans permitted: 2/lender

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Kansas Office of the State Bank Commissioner website.

To check if your payday lender is licensed in the state of Kansas, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Kansas here: https://www.osbckansas.org/consumers/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Kentucky

Payday loans are legal in the state of Kentucky.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 14 days (minimum) – 60 days (maximum)

- Finance Charges for $100 (14-day loan): $16

- APR for 14-day $100 Loan: 417%

- Number of outstanding loans permitted: Two, as long as all of the deferred deposit transactions do not exceed $500

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Kentucky Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Kentucky, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Kentucky here: https://kfi.ky.gov/newstatic_Info.aspx?static_ID=347

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Louisiana

Payday loans are legal in the state of Louisiana.

- Payday lending status: Legal

- Maximum Loan Amount: $350

- Loan Term: 60 days (maximum)

- Finance Charges for $100 (14-day loan): $30

- APR for 14-day $100 Loan: 782%

- Number of outstanding loans permitted: Not Specified

- Rollovers allowed: The customer has to pay 25% of the amount advanced plus fees charged, in order to enter into a new deferred presentment transaction or to renew the small loan for the remaining balance owed.

- Repayment Plan: Once a year (four substantially equal installments)

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Louisiana Office of Financial Institutions website.

To check if your payday lender is licensed in the state of Louisiana, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Louisiana here: http://www.ofi.state.la.us/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Maine

Payday loans are legal (but with restrictions) in the state of Maine.

- Payday lending status: Legal with restrictions

- Finance Charges: $5 for $75, $15 for amounts between $75 and $250, $25 amounts that exceed $250

- APR for 14-day $100 Loan: 196%

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Maine Department of Professional and Financial Regulations website.

To check if your payday lender is licensed in the state of Maine, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Maine here: https://www.maine.gov/pfr/consumercredit/complaint.htm

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Maryland

Payday loans are prohibited in the state of Maryland.

Massachusetts

Payday loans are prohibited in the state of Massachusetts.

Michigan

Payday loans are legal in the state of Michigan.

- Payday lending status: Legal

- Maximum Loan Amount: $600

- Loan Term: 31 days (maximum)

- Finance Charges for $100 (14-day loan): $15.61

- APR for 14-day $100 Loan: 407%

- Number of outstanding loans permitted: 2

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Michigan Department of Insurance and Financial Services website.

To check if your payday lender is licensed in the state of Michigan, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Michigan here: https://www.michigan.gov/difs/0,5269,7-303-12902_12907—,00.html

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Minnesota

Payday loans are legal in the state of Minnesota.

- Payday lending status: Legal

- Maximum Loan Amount: $350

- Loan Term: 30 days (maximum)

- Finance Charges for $100 (14-day loan): $15

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: None

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Civil penalties, repaying borrower up to $1000 fine, attorney’s fees, and injunctive relief.

Complaints & Information

To get more information about lending regulations you can visit the Minnesota Commerce Department website.

To check if your payday lender is licensed in the state of Minnesota, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Minnesota here: https://mn.gov/commerce/consumer/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Mississippi

Payday loans are legal in the state of Mississippi.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 28 days (minimum) – 30 days (maximum)

- Finance Charges: $20

- APR: 521%

- Number of outstanding loans permitted: Maximum $500 in all checks

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Mississippi Department of Banking and Consumer Finance website.

To check if your payday lender is licensed in the state of Mississippi, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Mississippi here: https://dbcf.ms.gov/complaint-form/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Missouri

Payday loans are legal in the state of Missouri.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 14 days (minimum) – 31 days (maximum)

- Finance Charges for $100 (14-day loan): max. 75% of the principal balance

- APR for 14-day $100 Loan: 1955%

- Number of outstanding loans permitted: One

- Rollovers allowed: 6

- Repayment Plan: Not Specified

- Criminal Action: It is not considered a crime the passing of a bad check if the payee accepts a check with the understanding that he will not present it for payment until later and the payee knows that there are insufficient funds on deposit at the time of acceptance.

Complaints & Information

To get more information about lending regulations you can visit the Missouri Division of Finance website.

To check if your payday lender is licensed in the state of Missouri, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Missouri here: https://finance.mo.gov/consumers/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Montana

Payday loans are legal in the state of Montana.

- Payday lending status: Legal with restrictions

- Maximum Loan Amount: $300

- Loan Term: 31 days (maximum)

- Finance Charges for $100 (14-day loan): $1.38

- APR for 14-day $100 Loan: 36%

- Number of outstanding loans permitted: Not Specified

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Montana Division of Banking and Financial Institutions website.

To check if your payday lender is licensed in the state of Montana, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Montana here: https://banking.mt.gov/Consumer_Info/Complaints

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Nebraska

Payday loans are legal in the state of Nebraska.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 34 days (maximum)

- Finance Charges for $100 (14-day loan): $15

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: Two

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Not in case of a returned check

Complaints & Information

To get more information about lending regulations you can visit the Nebraska Department of Banking and Finance website.

To check if your payday lender is licensed in the state of Nebraska, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Nebraska here: http://www.ndbf.org/consumers/complaint.html

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Nevada

Payday loans are legal in the state of Nevada.

- Payday lending status: Legal

- Maximum Loan Amount: 25% gross monthly income

- Loan Term: 35 days (maximum)

- Finance Charges for $100 (14-day loan): No limit

- APR for 14-day $100 Loan: No Limit

- Number of outstanding loans permitted: One

- Rollovers allowed: Yes, as long as the initial payoff term is not exceeded by 60 days

- Repayment Plan: Must be offered before civil action commences

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Nevada Financial Institutions Division website.

To check if your payday lender is licensed in the state of Nevada, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Nevada here: https://fid.nv.gov/Resources/Resources/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

New Hampshire

Payday loans are legal in the state of New Hampshire.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 7 days (minimum) – 30 days (maximum)

- Finance Charges for $100 (14-day loan): $1.38

- APR for 14-day $100 Loan: 36%

- Number of outstanding loans permitted: One

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the New Hampshire Banking Department website.

To check if your payday lender is licensed in the state of New Hampshire, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in New Hampshire here: https://www.nh.gov/banking/consumer-assistance/complaint.htm

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

New Jersey

Payday loans are prohibited in the state of New Jersey.

New Mexico

Payday loans are legal in the state of New Mexico.

- Payday lending status: Legal

- Maximum Loan Amount: $5000

- Loan Term: 120 days (maximum)

- Finance Charges for $100 (14-day loan): Not Specified

- APR for 14-day $100 Loan: 175%

- Number of outstanding loans permitted: None

- Rollovers allowed: Yes, but it must become a new loan

- Repayment Plan: Four equal installments

- Criminal Action: Civil action permitted

Complaints & Information

To get more information about lending regulations you can visit the New Mexico Financial Institutions Division website.

To check if your payday lender is licensed in the state of New Mexico, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in New Mexico here: https://www.rld.nm.gov/financial-institutions/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

New York

Payday loans are prohibited in the state of New York.

North Carolina

Payday loans are prohibited in the state of North Carolina.

North Dakota

Payday loans are legal in the state of North Dakota.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 60 days (maximum)

- Finance Charges for $100 (14-day loan): 20%

- APR for 14-day $100 Loan: 521%

- Number of outstanding loans permitted: Max. $600 outstanding for all lenders

- Rollovers allowed: Only once on the same loan

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the North Dakota Department of Financial Institutions website.

To check if your payday lender is licensed in the state of North Dakota, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in North Dakota here: https://www.nd.gov/dfi/file-complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Ohio

Payday loans are legal in the state of Ohio.

- Payday lending status: Legal

- Maximum Loan Amount: $1000

- Loan Term: 91 days (minimum) – 1 year (maximum)

- Finance Charges: 10% of the amount financed or $30

- APR: 28%

- Number of outstanding loans permitted: One

- Rollovers allowed: None

- Repayment Plan: Equal installments across all months

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Ohio Department of Commerce website.

To check if your payday lender is licensed in the state of Ohio, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Ohio here: https://com.ohio.gov/divisions-and-programs/financial-institutions/file-a-complaint-fi/file-a-consumer-financial-complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Oklahoma

Payday loans are legal in the state of Oklahoma.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 12 days (minimum) – 45 days (maximum)

- Finance Charges for $100 (14-day loan): $15 and database fee

- APR for 14-day $100 Loan: 204%

- Number of outstanding loans permitted: One for all lenders.

- Rollovers allowed: No deferments or renewals

- Repayment Plan: $15 fee to enter into an installment plan with 4 equal payments (after the third consecutive loan)

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Oklahoma Department of Consumer Credit website.

To check if your payday lender is licensed in the state of Oklahoma, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Oklahoma here: https://www.ok.gov/okdocc/Complaints/index.html

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Oregon

Payday loans are legal in the state of Oregon.

- Payday lending status: Legal

- Maximum Loan Amount: $50,000

- Loan Term: 31 days (minimum) – 60 days (maximum)

- Finance Charges: One-time origination fee of $10 up to $30 per $100 advanced.

- APR: 36%

- Number of outstanding loans permitted: Not Specified

- Rollovers allowed: Two

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Oregon Division of Financial Regulation website.

To check if your payday lender is licensed in the state of Oregon, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Oregon here: https://dfr.oregon.gov/help/complaints-licenses/Pages/index.aspx

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Pennsylvania

Payday loans are prohibited in the state of Pennsylvania.

Rhode Island

Payday loans are legal in the state of Rhode Island.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 13 days (maximum)

- Finance Charges: Not Specified

- APR: No Limit

- Number of outstanding loans permitted: $500/ lender, max of 3 different loans

- Rollovers allowed: Only one per loan

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Rhode Island Department of Business Regulation website.

To check if your payday lender is licensed in the state of Rhode Island, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Rhode Island here: https://dbr.ri.gov/divisions/banking/complaint.php

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

South Carolina

Payday loans are legal in the state of South Carolina.

- Payday lending status: Legal

- Maximum Loan Amount: $550

- Loan Term: 31 days (maximum)

- Finance Charges for $100 (14-day loan): max. 15% of the face amount of the check

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: One

- Rollovers allowed: None

- Repayment Plan: Once a year with 4 equal installments

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the South Carolina State Board of Financial Institutions website.

To check if your payday lender is licensed in the state of South Carolina, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in South Carolina here: https://consumer.sc.gov/consumer-resources/consumer-complaints

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

South Dakota

Payday loans are legal in the state of South Dakota.

- Payday lending status: Legal with restrictions

- Maximum Loan Amount: $500

- Loan Term: 6 months (maximum)

- Finance Charges for $100: $1.39

- APR: 36%

- Number of outstanding loans permitted: $500 out at a time

- Rollovers allowed: Four

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the South Dakota Division of Banking website.

To check if your payday lender is licensed in the state of South Dakota, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in South Dakota here: https://dlr.sd.gov/banking/consumers/filing_complaint.aspx

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Tennessee

Payday loans are legal in the state of Tennessee.

- Payday lending status: Legal

- Maximum Loan Amount: $500

- Loan Term: 31 days (maximum)

- Finance Charges for $100 (14-day loan): $17.65

- APR for 14-day $100 Loan: 460%

- Number of outstanding loans permitted: Three

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

If you want to get more info, you can visit the Tennessee Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Tennessee, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Tennessee here: https://www.tn.gov/tdfi/tdfi-how-do-i/file-a-complaint.html

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Texas

Payday loans are legal in the state of Texas.

- Payday lending status: Legal

- Maximum Loan Amount: Not Specified

- Loan Term: 7 days (minimum) – 180 days (maximum)

- Finance Charges for $100 (14-day loan): Not Specified

- APR for 14-day $100 Loan: 400%

- Number of outstanding loans permitted: No limit

- Rollovers allowed: No limit (as long as it doesn’t put the customer over the statutory limit)

- Repayment Plan: Not Specified

- Criminal Action: Prohibited, except for, theft, forgery, fraud

Texas has one of the least restrictive regulations regarding payday loans in America. Because of this, there is no maximum loan amount that one can borrow, and payday lenders can charge any fee they want without restrictions.

Complaints & Information

To get more information about lending regulations you can visit the Texas Office of Consumer Credit Commissioner website.

To check if your payday lender is licensed in the state of Texas, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Texas here: https://occc.texas.gov/consumers/file-a-complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Utah

Payday loans are legal in the state of Utah.

- Payday lending status: Legal

- Maximum Loan Amount: Not Specified

- Loan Term: 10 weeks (maximum)

- Finance Charges for $100 (14-day loan): Not Specified

- APR for 14-day $100 Loan: 652%

- Number of outstanding loans permitted: No limit

- Rollovers allowed: As long as they don’t exceed 10 weeks

- Repayment Plan: 60-day extended payment plan with 4 equal payment installments

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Utah Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Utah, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Utah here: https://dfi.utah.gov/resources/helpful-links/file-a-complaint/

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Vermont

Payday loans are prohibited in the state of Vermont.

Virginia

Payday loans are legal in the state of Virginia.

- Payday lending status: Legal

- Maximum Loan Amount: $2,500

- Loan Term: 4 to 24 months

- Finance Charges: Monthly maintenance fee of $25 / 8% of the principal balance

- APR for 14-day $100 Loan: 36%

- Number of outstanding loans permitted: One

- Rollovers allowed: None

- Repayment Plan: 60-day extended payment plan with 4 equal payment installments

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Virginia State Corporation Commission website.

To check if your payday lender is licensed in the state of Virginia, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Virginia here: https://www.scc.virginia.gov/pages/File-a-Financial-Complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Washington

Payday loans are legal in the state of Washington.

- Payday lending status: Legal

- Maximum Loan Amount: $700 or 30% of gross monthly income

- Loan Term: 7 days (minimum) – 45 days (maximum)

- Finance Charges for $100 (14-day loan): $15 per $100 for amounts up to $500, $10 per $100 for amounts between $500 and $700

- APR for 14-day $100 Loan: 391%

- Number of outstanding loans permitted: Any, as long as it doesn’t exceed $700

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Washington Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Washington, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Washington here: https://dfi.wa.gov/file-complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

West Virginia

Payday loans are prohibited in the state of West Virginia.

Wisconsin

Payday loans are legal in the state of Wisconsin.

- Payday lending status: Legal

- Maximum Loan Amount: (Less of) $1500 or 35% of income

- Loan Term: 90 days (maximum)

- Finance Charges for $100 (14-day loan): No limit

- APR for 14-day $100 Loan: Not Specified

- Number of outstanding loans permitted: Cannot exceed the total loan amount

- Rollovers allowed: One

- Repayment Plan: Once per 12 months in four equal installments with same dates as the lendee’s pay period schedule

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Wisconsin Department of Financial Institutions website.

To check if your payday lender is licensed in the state of Wisconsin, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Wisconsin here: https://www.wdfi.org/wca/consumer_credit/complaints_and_questions.htm

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

Wyoming

Payday loans are legal in the state of Wyoming.

- Payday lending status: Legal

- Maximum Loan Amount: Not Specified

- Loan Term: 1 month (maximum)

- Finance Charges for $100 (14-day loan): $30

- APR for 14-day $100 Loan: 782%

- Number of outstanding loans permitted: Not Specified

- Rollovers allowed: None

- Repayment Plan: Not Specified

- Criminal Action: Prohibited

Complaints & Information

To get more information about lending regulations you can visit the Wyoming Division of Banking website.

To check if your payday lender is licensed in the state of Wyoming, you can perform a License Search online.

You can find all the information on how to submit a complaint about a payday lender in Wyoming here: https://wyomingbankingdivision.wyo.gov/how-to-file-a-complaint

You can also submit a complaint to the Consumer Financial Protection Bureau, a federal agency in charge of protecting consumers from predatory lenders.

To wrap it all up, payday loans are legal in the following states:

Alabama, Alaska, California, Colorado, Delaware, Florida, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Mexico, North Dakota, Ohio, Oklahoma, Oregon, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Washington, Wisconsin, Wyoming.

And they’re prohibited in the following:

Arizona, Arkansas, Connecticut, District of Colombia, Georgia, Maryland, Massachusetts, New Jersey, New York, North Carolina, Pennsylvania, Vermont, West Virginia.

👉 For more info regarding payday loans and other similar loans, feel free the check out our articles regarding courtesy loans and tribal loans.