Value investing is an investment philosophy that has been embraced by some of the best-known investors of the last century, including Warren Buffett and his mentor Benjamin Graham. It’s a conservative strategy that often falls out of favor during market booms, but it has a long track record of consistent returns in all market conditions.

Value investors look for investments that offer intrinsic value that is currently greater than the share price. That sounds simple, but many of the methods for calculating intrinsic value can be quite complex.

It’s a strategy that remains relevant in 2025, with mid-cap value stocks showing improved performance, and technological tools like AI enhancing investment analysis.

Let’s take a look at the basics of value investing.

Key Takeaways

- Value investors focus on intrinsic value. This philosophy is all about identifying companies that are currently worth more than their share price.

- Calculating value can be complex. Any assessment of value starts with business fundamentals, but less tangible factors like management competence and market resilience also matter.

- It’s a long-term strategy. Value investors tend to buy and hold, and they need to resist market trends and ride through short-term volatility.

- Look for a margin of safety: Purchase securities when their market prices are significantly lower than their intrinsic value, ensuring a safety margin that can cut risk and improve long-term returns.

Speculation

Speculation is the act of purchasing an asset without regard to its actual intrinsic value, with the hope that its price will go up and that you’ll be able to sell it in the future for more than you originally paid.

Speculation is the absolute antithesis of value investing.

Speculation is the very thing that drove Benjamin Graham to formulate the concepts that would eventually become known as value investing: Graham started teaching at Columbia Business School in 1928, a year before the Wall Street Crash of 1929 that ushered in the 10-year Great Depression that we all know about it.

The Great Crash, as it’s known, was caused to a large extent by speculators, who assumed that the stock market would continue to rise at a steady breakneck pace forever. Ben Graham and his colleague David Dodd published Security Analysis in 1934 – the first financial textbook to actually teach how to calculate the intrinsic value of a business, regardless of its price.

Graham also wrote extensively about the dangers and stupidity of speculation in The Intelligent Investor.

Technical Analysis

Technical analysis is a method of evaluating securities by analyzing statistics generated by market activity, such as past prices and volume. Technical analysts do not attempt to measure a security’s intrinsic value, but instead, use charts and other tools to identify patterns that can suggest future activity.

A core teaching of value investing is that an asset’s price and its intrinsic value are two completely distinct things. Value investors employ fundamental analysis, which is the opposite of technical analysis. Fundamental analysis is a method of evaluating a security that entails attempting to measure its intrinsic value by examining related economic, financial, and other qualitative and quantitative factors.

Investing in Low P/E , Low P/B, or High Dividend Yield Stocks

This is one of the biggest myths when it comes to value investing, and it continues to be perpetuated because it’s an easy, simple, and lazy way to classify value investors.

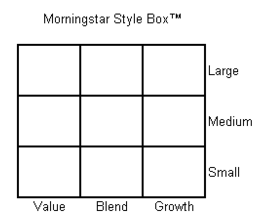

Take, for example, the style box that Morningstar has popularized. The style box helps characterize mutual funds by their focus on large-cap, medium-cap, and small-cap stocks, and by their “value” or “growth” orientation.

A value stock, according to Morningstar, has a low price/earnings ratio, low price/book ratio, low price/cash flow ratio, and a high dividend yield. A growth stock, on the other hand, has high long-term projected earnings growth, high historical earnings growth, and high sales, cash flow, and book value growth.

Or, take this explanation of value investing and growth investing by Fidelity:

Value Investing

Focus on companies with lower-than-average sales and earnings growth rates. Holdings generally feature stocks with lower price-to-earnings and price-to-book ratios. Stocks generally have higher dividend yields. Fund can potentially capitalize on turnaround situations.

Growth Investing

Focus on companies with above average rates of growth in earnings and sales. These stocks tend to have above-market price-to-earnings and price-to-sales ratios, as the rapidly growing sales and earnings justify a higher-than-average valuation.

While many value investors often do seek out stocks that fit the above criteria, the qualities of low valuation, low growth, and high dividend yields are not required for value investing.

The problem with these classifications and definitions is that they imply that a value investor cannot invest in a stock that has a high P/E ratio or in a business that has experienced higher than average sales growth.

For example, a stock’s intrinsic value could warrant a high P/E, or the company may have low or negative earnings yet positive free cash flow – which would result in a negative P/E ratio. And dividend yields should have little to do with intrinsic value, as that cash could be better used by being plowed back into the company.

As I wrote in my very first post, What’s Better: Value Investing or Growth Investing?, there should be no difference between value investing and growth investing. The difference is between fundamental analysis / intelligent investing and technical analysis/speculation.

In this sense, value investing is synonymous with intelligent investing.

Investing in Low Growth, Mature, or Unpopular Companies

This is the biggest misconception I see when it comes to value investing. and it’s very much related to the above point on value versus growth investing and low P/E, high dividend yield stocks.

The common thinking goes:

- If growth investors look for stocks that are experiencing high growth, then value investors must look for stocks with low growth.

- If value investors look for stocks with low P/E valuations, then these companies must be unpopular.

- If value investors look for companies that are paying high dividends, then these companies must be in a “mature” stage of life.

I’ve already shown why the common thinking about growth, P/E ratios, and dividends are wrong. Consequently, the conclusions about low growth, popularity, and maturity are wrong as well.

Here’s an Example

I invested heavily in Microsoft stock and Google stock at various points in 2010-2012. Microsoft’s dividend yield was a meager 2% and Google doesn’t even pay a dividend. And while Microsoft wasn’t necessarily considered a “hot” company around that time, Google certainly was.

So why would I, a value investor, invest in Microsoft and Google? Because their stock prices were well below my calculations of their intrinsic value. As it turns out (and without much surprise) these two stocks are among the best performers in my portfolio.

Value investors can absolutely invest in growing companies while adhering to Graham’s original principles.

Value investing definition

In Value Investing: From Graham to Buffett and Beyond, Bruce Greenwald points out that value investing in the manner initially defined by Benjamin Graham and David Dodd rests on three key characteristics of financial markets:

1. Stock Prices Will Be Volatile

The prices of financial securities are subject to significant and capricious movements. Mr. Market, Graham’s famous personification of the impersonal forces that determine the price of securities at any moment, shows up every day to buy or sell any financial asset. He is a strange fellow, subject to all sorts of unpredictable mood swings that affect the price at which he is willing to do business.

2. Focus on the Business Fundamentals

Despite these gyrations in the market prices of financial assets, many of them do have underlying or fundamental economic values that are relatively stable and that can be measured with reasonable accuracy by a diligent and disciplined investor. In other words, the intrinsic value of the security is one thing; the current price at which it is trading is something else. Though value and price may, on any given day, be identical, they often diverge.

3. Buy on the Cheap

A strategy of buying securities only when their market prices are significantly below the calculated intrinsic value will produce superior returns in the long run. Graham referred to this gap between value and price as “the margin of safety”… he wanted to buy a dollar for 50 cents.

These 3 points are core to Graham’s teachings and are part of the definition of value investing.

But I think value investing can be defined even more succinctly than that. In summary:

Value Investing Is Nothing More Than This:

1. Knowing the difference between price and intrinsic value

2. Paying less than the value you receive in return.

That’s it. Everything else is simply a corollary of these two rules. For example:

In order to know the intrinsic value of a stock, you must perform bottoms-up fundamental analysis.

By paying less than the value you receive in return, you automatically have a margin of safety. Sometimes the margin of safety is large (if there is great risk or a great opportunity). Sometimes the margin of safety is relatively small.

By knowing the difference between price and intrinsic value, then you must know about the unpredictable mood swings of Mr. Market and you should be able to control your own emotions.

As long as he or she is paying less than the value received in return, a value investor is free to invest in any stock (or financial asset) imaginable, regardless of whether it is a low P/E stock, high P/E stock, mature business, growing business, unpopular company, etc.

Summary

Of course, there are many similarities among value investors that lead to common themes that often reappear in the subject of value investing (how to calculate intrinsic value, finding a margin of safety, contrarianism, behavioral finance). But in the simplest, rawest form, every value investor knows the difference between price and intrinsic value and seeks to pay less than the value they receive in return.

When looking at it this way, can good investing really be anything other than value investing?

The Ultimate Guide to Value Investing

Do you want to know how to invest like the value investing legend Warren Buffett? All you need is money to invest, a little patience—and this book. Learn more

The Intelligent Investor: The Classic Text on Value Investing

BY BENJAMIN GRAHAM

The greatest investment advisor of the twentieth century, Benjamin Graham taught and inspired people worldwide. Graham’s philosophy of “value investing” — which shields investors from substantial error and teaches them to develop long-term strategies — has made The Intelligent Investor the stock market bible ever since its original publication in 1949.

Security Analysis

BY BENJAMIN GRAHAM AND DAVID DODD

“A road map for investing that I have now been following for 57 years.” – From the Foreword by Warren E. Buffett

First published in 1934, Security Analysis is one of the most influential financial books ever written. Selling more than one million copies through five editions, it has provided generations of investors with the timeless value investing philosophy and techniques of Benjamin Graham and David L. Dodd.

Hi John,

Thank you for your detailed reply, it’ll help me get started. I’d like to learn how to calculate the intrinsic value of a company (stock). Will I find the knowledge required on your blog? (I just found it yesterday, when I left my comment.)

I assume my input for the calculation will be found in annual (and perhaps quarterly) reports of companies, so I assume I’ll have to go deeper than the info I can find on Marketwatch 🙂 (Would be great though if I wouldn’t have to.)

A few other things:

1) Are you able to calculate the intrinsic value of a company?

2) Do you invest exclusively based on that?

3) Do you plan to share/comment your investing results like many other bloggers do?

Best,

Dom

Hi John,

What metrics would you be looking at doing your bottoms-up fundamental analysis, to eventually come up with the “value” that you can compare to the stock price?

Can you describe it using General Electric (high P/E, but still something I own) as an example?

(If you already have a post on this topic a link is perfect)

Thank you,

Dom

Hi Dom! Good question! You have to calculate the “intrinsic value” of the stock and then compare it to the share price. What is intrinsic value? Intrinsic value is the present value of all the cash that the business will generate for its owners, from now into the future. You can think of GE – or any company – as a machine. You put some cash into the machine today (e.g. buying equipment, machines, hiring people) and it spits out more cash back to you tomorrow (hopefully). It does this year after year – forever. All you have to do is figure out how much cash this machine will spit out for you each year and then add all of it up (discounting cash received in the future to a “present value” using time value of money). Easier said than done of course. Also hard to explain fully in this comment box. If you’re unfamiliar with Time Value of Money, here’s a post I did a while back: https://www.vintagevalueinvesting.com/vintage-value-101-the-time-value-of-money-or-the-genius-of-wimpy/ And this series of posts explains how to calculate intrinsic value: https://www.vintagevalueinvesting.com/value-investing-101-intrinsic-value-part-1/ The P/E ratio is a good rough metric that you can look at, but it doesn’t tell us the… Read more »