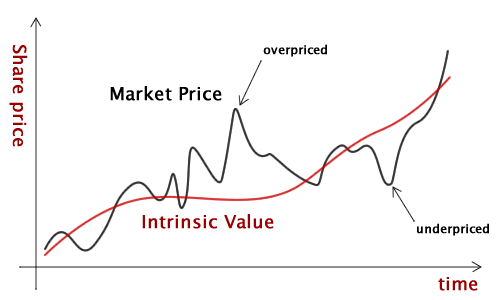

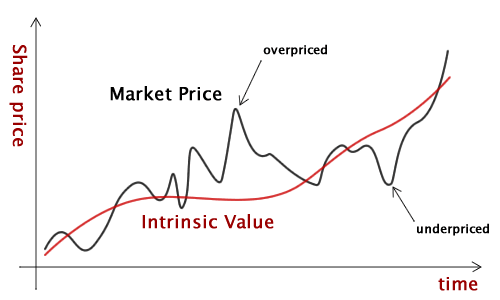

If you’ve read any of the articles on this website – or if you’re familiar with value investing concepts – then you may know that an Intelligent Investor will only buy a stock when its market value (that is, its stock price) is less than its intrinsic value.

In other words, a smart investment is one where you are buying a stock for less than its intrinsic value.

But what exactly is intrinsic value and how do you calculate it?

What is Intrinsic Value?

In the Berkshire Hathaway Owner’s Manual, Warren Buffett writes this about intrinsic value:

Intrinsic value is an all-important concept that offers the only logical approach to evaluating the relative attractiveness of investments and businesses. Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.

Viewing a Business as a Bond

What does Buffett mean by this? Imagine a bond, for instance, which pays the bondholder interest every year and principal back at maturity. From The Time Value of Money, we know that a dollar today is worth more than a dollar tomorrow, and vice versa that a dollar tomorrow is worth less than a dollar today. Therefore, the interest and principal payments we receive in the future must be discounted to a lower value in order to determine their value today.

So, the present value of a bond = the discounted value of the bond’s future interest and principal payments. Now picture a company.

What is the purpose of a company? Answer: To generate dividends for the company’s shareholders.

This is a lot like a bond isn’t it? Except instead of being paid interest every quarter, a shareholder is paid dividends every quarter. This means you can discount the value of future dividends just the same way that you can calculate a bond’s future interest and principal payments.

Remember that the present value of a future payment = the future value of the payments, discounted at a certain rate?

In math form, this equation is the following (where i = the discount rate):

If the future payments will growth at a constant rate, then the equation can be simplified as:

The above equation is called the Dividend Discount Model (or the Gordon Growth Model) and its output is the intrinsic value of a stock.

Example

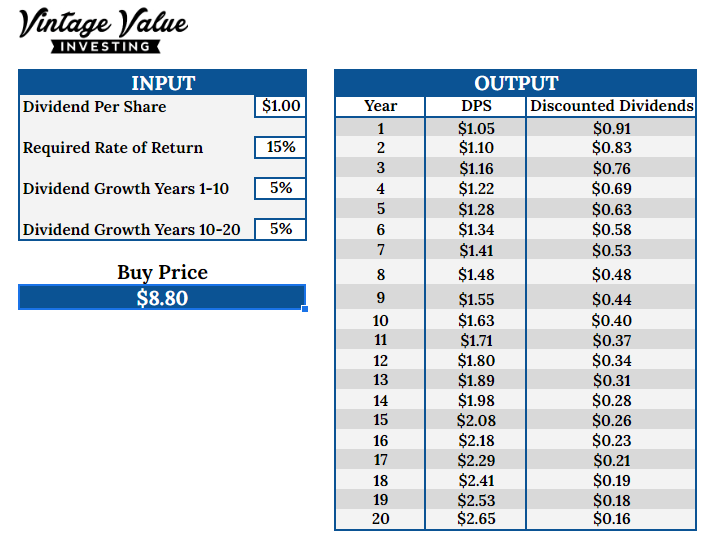

Let’s try the DDM model just for fun. Let’s say a company is producing a dividend of $1.00 per share and plans to grow that dividend by 5% per year for the next 20 years. Let’s also assume that you want no less than a 15% return per year on your investment. Here is the calculation:

As the years go on, the margin between the DPS and discounted dividends grows significantly. According to our calculations, in order to achieve a 15% return, we would have to purchase the stock at $8.80 per share.

Limitations of the Dividend Discount Model

You might argue, “but not all stocks pay dividends, and even the ones that do pay dividends don’t have a consistent dividend growth rate.”

You’re right, of course. Unlike with a bond, a company doesn’t have any contractual obligations to pay a dividend to its shareholders.

Furthermore, dividends alone don’t capture all of a company’s earnings. Besides paying a dividend, a business can also use the cash it generates to acquire new equipment or machines, to improve its factories or buildings, for research & development, to acquire another company, or to make other investments.

Any of these can be a better allocation of capital than if the company had paid a dividend. So while the dividend growth model (DDM) provides a good framework to understand intrinsic value, it doesn’t actually generate a realistic result.

The Ultimate Guide to Value Investing

Do you want to know how to invest like the value investing legend Warren Buffett? All you need is money to invest, a little patience—and this book. Learn more

How To Calculate Intrinsic Value

According to Warren Buffett:

Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.

So how do you discount the value of the cash that can be taken out of a business during its remaining life? You run a DCF analysis, projecting out the company’s cash flows for a number of years and then discounting those cash flows back to the present value using some discount rate.

You could then use the intrinsic value you calculate and decide to buy the stock only if the company’s market price is less than its intrinsic value.

But what do we mean when we talk about a company’s “cash flow” anyway, and how can we project it?

Free Cash Flow

When we say cash flow, what we’re really talking about is Free Cash Flow.

Free cash flow is the amount of cash that a business generates that is available for distribution to all of the security holders of that company, including both debt holders and equity holders.

There are multiple formulas to calculate Free Cash Flow (“FCF”). Here are the most common ones:

FCF = EBIT x (1 – Tax Rate) + Depreciation & Amortization – Change in Net Working Capital – Capital Expenditures

FCF = Operating Cash Flow – Capital Expenditures

FCF = EBITDA – Change in Net Working Capital – Capital Expenditures

No matter which formula you use, FCF incorporates three major items.

First, FCF starts with the “profits” of the company (whether that is EBIT, Net Income, or EBITDA) and adjusts for all non-cash items (like depreciation and amortization) to determine the “cash profits” of the business.

Then FCF adjusts for changes in net working capital. Net working capital is Current Assets (not including cash) minus Current Liabilities. Current Assets includes things like accounts receivable and inventory, and Current Liabilities includes things like accounts payable. If working capital increases (e.g., the company invests in inventory, accounts receivable increases, or accounts payable decreases), then this is a use of cash; if Working Capital decreases, then this is a source of cash.

Finally, FCF must account for the company’s investments in its long-term assets, including its Property, Plant, and Equipment. This is called the company’s Capital Expenditures.

Warren Buffett’s Owner Earnings

Warren Buffett essentially runs a DCF to determine a company’s intrinsic value, but he uses what he calls “Owner Earnings”, which is a slight variation on Free Cash Flow.

Warren says this about Owner Earnings in his 1986 Berkshire Hathaway Shareholder Letter:

If we think through these questions, we can gain some insights about what we may call “owner earnings.” These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges… less (c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume.

(If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in (c). However, businesses following the LIFO inventory method rarely require additional working capital if unit volume does not change.)

Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since (c) must be a guess – and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes – both for investors in buying stocks and for managers in buying entire businesses.

We agree with Keynes’s observation: “I would rather be vaguely right than precisely wrong.”

Okay. So Buffett’s Owner Earnings is basically the same exact calculation as Free Cash Flow, except he determines intrinsic value by looking at the company in a “no growth” situation.

Warren essentially views a company as a bond with an annual interest payment and says:

If I owned this company today, and if revenue never grows and margins stay flat, and if the company only invests as much as it needs in marketing and PP&E to keep its current position, then how much Free Cash Flow could the business consistently generate on an annual basis?

In other words, Warren Buffett’s Owner Earnings is just Free Cash Flow in a 0% growth scenario.

In a 0% growth scenario, changes in net working capital would be 0, because sales aren’t growing so accounts receivable, inventory, accounts payable, and other current items remain flat. And capital expenditures would be equal to just “maintenance capital expenditures” (an item that we would have to estimate), because “growth capital expenditures” would be equal to 0. So:

Owner Earnings = EBIT x (1 – Tax Rate) + Depreciation & Amortization – Maintenance Capital Expenditures

After all this talk about Owners Earnings, Capital Expenditures, Inventories, here’s what you really need to know for simple DCF calculations: use the company’s most recent Free Cash Flow to run your calculations.

You can complicate your calculations by adding and subtracting things like everything we just discussed, but FCF will work just fine for most applications. You can easily find FCF and other metrics for free on most financial reporting websites, but I find Quick FS to be the most comprehensive.

Discounted Cash Flow Analysis

The Present Value Equation

Do you remember the Present Value formula? If not, here it is again:

In the PV equation we take a future cash flow and divide it by 1 plus the discount rate, taken to the power of n (where n is the number of periods).

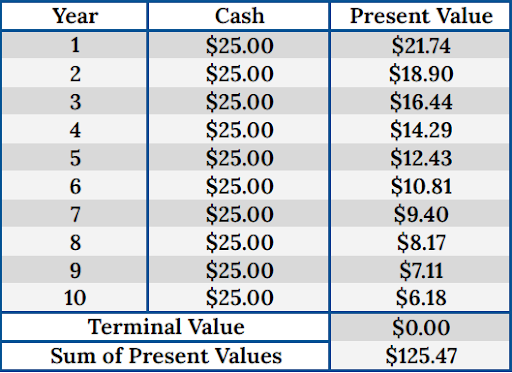

For example, let’s say we are going to receive $25 next year and our discount rate is 15%. How much is that future $25 worth to us today? Answer: $22.75.

| Year | Cash | Present Value |

| 1 | $25.00 | $21.74 |

Now what if we receive the $25 in two years instead of next year? Answer: $18.90.

| Year | Cash | Present Value |

| 1 | $25.00 | $21.74 |

| 2 | $25.00 | $18.90 |

As you can see, the $25 received in two years is worth less to us today than the $25 received next year.

Now let’s say we’re going to receive $25 for the next 10 years (and let’s keep the same 15% discount rate). What is the total value to us today? Answer: $125.47.

So, in order to get a 15% return on a cash flow of $25 per year, you would need to pay $125.47 today.

Discounted Cash Flow

Now that you’re an expert on calculating present values, we can easily run a DCF analysis to value a stock.

First, we must project the company’s future cash flows. If you need a refresher on Free Cash Flow and Owner’s earnings.

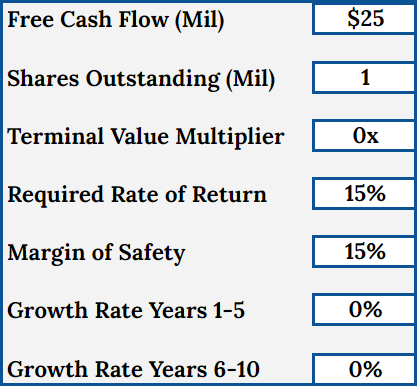

These are the inputs you need to calculate the intrinsic value of a stock using:

- Free Cash Flow (found in the cash flow statement)

- Shares Outstanding (found in the income statement)

- Terminal Value (multiplier determined by the investor)

- Discount Rate (rate of return)

- Margin of Safety (a percentage subtracted from the calculated value)

- Growth Rate (value determined by the investor)

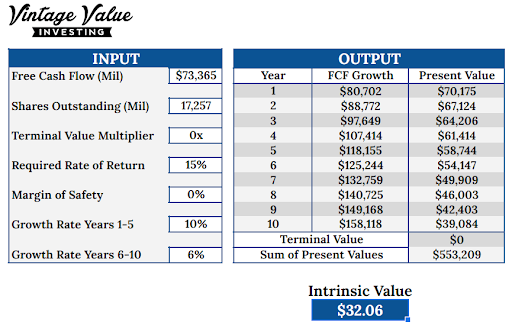

Example: AAPL

Now, lets use Apple (AAPL) as an example. All you need to do is fill in the appropriate fields. You can find most of this information for free at sites like Quick FS.

So, according to our research, AAPL currently has $73,365 million in Free Cash Flow and has 17,257 million in shares outstanding (we’ll get to terminal value later).

The Discount Rate is essentially your rate of return, since you are discounting the cash flows to the return you desire. This input is up to the investor of course, but I normally default to 15%.

The Margin of Safety is simply a percentage off of the intrinsic value calculation. You can set this to whatever you desire, but a greater margin of safety lowers your risk. This input is also up to the investor, but I generally go with 10% to 15%. We will discuss this later on as well.

Lastly, we have the Growth Rates. This is simply the calculation that you think the Free Cash Flow will compound per year. Since companies rarely grow at an exact rate year after year, it is best to break it down into years 1-5 and 6-10 with different rates for each period.

But how do you determine a growth rate? This is a very subjective number, as each investor will probably come up with different growth rates depending on their individual analysis. To keep things simple for this example, let’s assume that AAPL will continue to grow its cash flow at a rate of 10% per year for the next five years, then slow down to 6% per year for the following five years.

After we come up with all the numbers, we plug them into our calculation. Here’s the result:

As you can see, the calculator discounted the present values of all the future cash flows. You’ll notice that with each passing year the values get smaller and smaller. This is due to the time value of money. I have written an entire article about it, so go check it out if you are not familiar with this concept. In a nutshell, money is more valuable today than it is tomorrow. Therefore, an investor can pay a lesser amount today to receive more tomorrow.

Now, all we have to do is add up all of our present values and divide them by the number of shares outstanding.

According to our calculations, our intrinsic value of AAPL is $32.06 per share. If you were to look up the share price today, you would see that AAPL is currently trading at $120.89! What’s wrong with our calculation? Did we mess up?

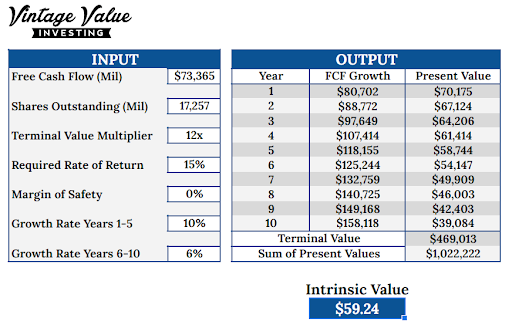

Terminal Value

Here’s where we can get into Terminal Value, and why it is so important. Projecting the cash flows of a business for 10 years is hard enough, but most businesses last much longer than that. So how do we account for those years?

Think of terminal value as the entire rest of the business’s future cash flows. There are multiple ways to calculate this, but I find the terminal multiple to be the easiest method. Basically, we are multiplying the year 10’s cash flows and discounting by our discount rate. My default multiplier is usually 10x.

Another way to think of the terminal value is if the business was sold at year 10 for a multiple of its cash flows. To do this, you could determine the multiplier based on the company’s historical Price to Free Cash Flow. This number is easy to calculate on your own, but in order to quickly view a historical perspective, a platform like Stock Rover makes it really easy to do. Here is AAPL’s historical P/FCF ratio:

Source: Stock Rover

AAPL’s current P/FCF is currently over 28, which is a 10-year high. This is a relatively high multiple for any company, not just AAPL. However, when the company was trading at more reasonable valuations, the P/FCF ratio hovered between 10 – 15. For our example, let’s split the difference and go with a terminal multiple of 12. Plug it into our DCF calculation, and let’s see what AAPL’s intrinsic value is now:

By plugging in the terminal value, we can now see that the sum of the present values ballooned, as did the intrinsic value price, which is now $59.24 per share. That was almost double the intrinsic value of our previous calculation!

This is why terminal value is so important. Too large of a number can really inflate the intrinsic value of your calculations. The same goes for growth rates as well. In order to combat over calculating and inflating your intrinsic values, be sure to use conservative growth rates and terminal multiples.

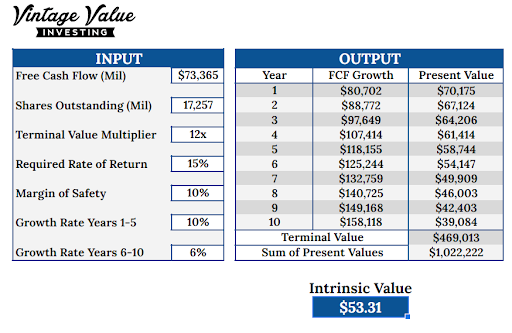

Margin of Safety

Lastly, we come to the Margin of Safety. I also have written more about this topic, but to summarize, in order for an investor to reduce their risk, they should buy a stock at a price that trades below its intrinsic value. That means we should still look to buy AAPL at an even lower price than we have calculated.

So what should that amount be? Again, this is another personal decision by each investor. Sometimes a margin of safety for a stock may not be price, but the strength in its business operations. In this example, AAPL is the largest company in the world by market capitalization and therefore is highly unlikely to go bankrupt anytime soon.

Taking this into account, let’s assume a modest margin of safety discount of 10%. This 10% is simply a percentage knocked off of the intrinsic value calculator that we already made. Think of this as a sale at a store that has reduced the price of your favorite T-shirt by 10%. Now here is our final buy price:

And there you have it, we have finally calculated our buy price for AAPL for a total of $53.31! Now, AAPL is currently trading far above this value and would therefore be considered to be quite overvalued. However, now you know what this business is really worth to you as an investor. You can simply set this value on your watch list and wait for a buying opportunity.

Summary

There you have it! Now you know how to run a Discounted Cash Flow analysis to determine the intrinsic value of a stock. There are many other ways that investors use to calculate intrinsic value, but this is the most basic method. Just because it may be the most basic, does not mean that is not valid. Quite the contrary; I am a firm believer that in investing, simpler methods are better that over complicated ones.

The DCF valuation method is a great way to help an investor establish a baseline intrinsic value for a stock. By using this method, you can know whether or not you a stock is overvalued or undervalued.

Hi John,

Dividend per share can he found.

Dividend growth rate can be calculated by eg. looking at the past 10 years avg dividend growth rate.

But where do you get the discount (interest) rate from?

Could you give an example?

Thank you,

Dom

Try this article: https://www.vintagevalueinvesting.com/how-to-determine-a-discount-rate/

good explanation!