Self’s credit builder loans are a way for people with no credit record or a thin credit file to put an affordable installment loan on their credit records. They may also help people with low credit scores, though their impact will be lower. This Self credit builder loan review takes a closer look at the pros, the cons, and what Delf can (and can’t) do for you.

Self Credit Builder Loan

Self’s credit builder loans are a credit-building option for people who have no credit record or a thin credit file. However, there are free ways to build credit, so you may want to look into those options first.

Pros

Reports to all three credit bureaus.

Offers a credit card secured by your loan balance.

You can close the account easily and without penalty.

Cons

High cost relative to some credit building methods

Some users report customer service issues.

What Is a Credit Builder Loan?

A credit builder loan is a special type of loan that helps you build credit. It’s not used like a traditional loan, where you can use the loan proceeds to pay for something, then pay it back over time.

With a credit builder loan, you don’t actually get any money from the lender to start with. Instead, when you get the loan, Self will place the money into a savings account on your behalf. You’ll get loan bills like normal and have to make a payment each month.

Each payment you make will show up on your credit report and improve your credit score. However, just like any other loan, late payments or missed payments can damage your credit. It’s important to make sure you can make the monthly payments. If you don’t, your credit builder loan could wind up damaging your credit score.

How Does Self Work?

To get started with Self, you’ll first have to apply for a credit builder loan. You can customize your loan, choosing your desired monthly payment. Options start as low as $25 and go as high as $150. Your payment will affect the term of your loan, which ranges from one to two years.

Once you select the loan you’d like, Self will decide whether to approve your application. There’s no hard pull on your credit and you’re almost guaranteed to get approved since Self is holding your money and taking on almost no risk.

If you’re approved, Self will set aside your loan proceeds in a certificate of deposit and start sending you monthly bills.

Each month, you’ll make your loan payment, which includes both principal and interest. Over time, your monthly payment will show up on your credit report and increase your credit score. Your payments will also reduce your loan balance.

Once you’ve fully repaid the loan, Self will release the proceeds of your loan to you. This makes a credit builder loan into a sort of forced saving plan that also helps you build your credit.

Keep in mind that your loan payments include interest, so you’ll wind up paying more than you receive at the end of the loan. For example, at the time of writing, Self states that if you choose a $35 monthly payment for a term of 24 months, you’ll get $724 at the end of the loan. However, 24 monthly payments of $35, plus the $9 startup fee total $849.

That means you’ve paid $125 for the service.

- If you have an active Credit Builder Account in good standing, 3 on time payments, $100 or more in savings progress and satisfying income requirements you may be eligible to receive the Self Secured Visa Credit Card*, without a hard credit check. Criteria subject to change.

- Build credit and savings at the same time.

- Start with a Credit Builder Account* that reports monthly payments to all 3 major credit bureaus.

- At the end of your plan, unlock the savings you built — minus interest and fees.

- The Self Visa® Secured Credit Card* is accepted at millions of locations in the U.S.

*Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., SouthState Bank, N.A., First Century Bank, N.A., each Member FDIC. Subject to credit approval. Self Visa® Credit Card issued by Lead Bank, First Century Bank, N.A., or SouthState Bank, N.A., each Member FDIC. See Self.inc for details. Subject to ID Verification. Individual borrowers must be a U.S. citizen or permanent resident and at least 18 years old. Valid bank account and Social Security Number are required. All loans are subject to consumer report review and approval.

Features

There are a few important features of Self that are worth covering.

Reports to All Three Bureaus

There are three major credit bureaus in the United States: Equifax, Experian, and TransUnion.

Different lenders work with different bureaus to check customers’ credit scores. Different lenders also report account details to different bureaus.

Self reports your loan details to all three credit bureaus, which lets you improve your credit score with all three bureaus. That means that future lenders should see your improved score regardless of where they check it.

Close Your Account Early

A Self credit builder loan is a 12 or 24-month commitment. Like any other loan, if you miss payments or make late payments, that will hurt your credit score.

To help people avoid hurting their credit with a credit builder loan, Self offers the option to close your account early if you can’t keep up with the payments or no longer want the service. You can either pay the remaining balance of the loan or simply ask Self to close the account. This will incur a fee of $5 or less depending on your loan.

If you do this, Self will report the account as paid off early to the credit bureaus, which means you don’t have to worry about damaged credit due to a delinquent account.

Self Visa Credit Card

Once you’ve made three monthly payments toward your credit builder loan and have built up $100 or more in savings progress, Self will give you the option to apply for a secured credit card.

You can set the card’s credit limit, up to the total savings progress on your credit builder loan. Once you get the card, you use it like any other credit card, making purchases and paying them off each month.

This card gives you some access to the savings you’ve built through your loan, by letting you borrow against that balance. It also gives you another account to use to build your payment history.

The secured credit card provides a revolving credit line, which in combination with your credit builder loan will improve your credit mix and may help your credit. As with any credit card, you will need to make on-time payments and keep your credit utilization low to build credit.

👉 Read our full review of the Self Visa Credit Card for more information about how this card works.

Pricing

A credit builder loan from Self isn’t free. Even though you get some of your money back at the end of the loan, some of your payments go toward fees and interest, which means you’ll pay more than you receive in the end.

The cost of a credit builder loan depends on the interest rate and fees of the loan. Rates can change regularly, but at the time of writing, the price breakdown looks like this.

| Monthly Payment | Term | Administrative Fee | APR | Total of Monthly Payments and Fee | Money Received at End of Loan | Net Cost |

|---|---|---|---|---|---|---|

| $25 | 24 months | $9 | 15.92% | $609 | $520 | $89 |

| $35 | 24 months | $9 | 15.97% | $849 | $724 | $125 |

| $48 | 24 months | $9 | 15.72% | $1,152 | $992 | $169 |

| $150 | 24 months | $9 | 15.88% | $3,600 | $3,076 | $533 |

If you want the cheapest option, the $48 monthly payment will cost just a bit more than half as much as the next cheapest credit builder loan. However, you should also consider the affordability of the monthly payment.

A longer term will help you build credit, You will accumulate credit history and the account will remain active longer.

Customer Reviews

Customer reviews for Self are mixed. Some customers have had great experiences while others have had significant issues. Many reviews say the service works, but costs too much.

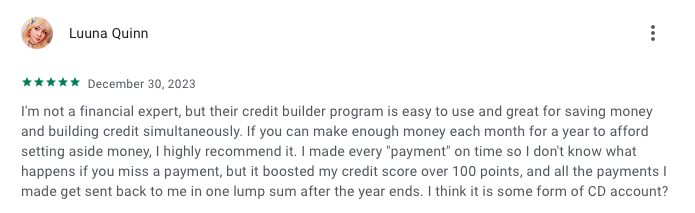

One positive review from Google Play discusses the positive results.

This negative review from Trustpilot mentions that you might see a drop in your credit score. It also claims that the company has added inaccurate data to its credit report.

A middle-of-the-road review mentions that the product works, but is overly expensive.

Self Alternatives

Self is just one of many services available for people who want to improve their credit score. If you’re in the market for a credit builder loan, consider these alternatives.

| Features | Cost | Pros | Cons | |

|---|---|---|---|---|

| Credit Strong | Loan terms up to 120 months. Customize your monthly payment. Cancel your loan any time. | $28 – $25 one-time fee; 5.85% – 15.73% APR. | Various plans to choose from. No credit check required. Available in 48 states. | Loans with low payments have very long terms. Higher net costs than some other loans. |

| MoneyLion | Combine credit building and banking services. Debit card with 55+ in-network ATMs. | $19.99 monthly fee. 5.99% – 29.99% APR. | Immediate access to some of the loan funds. Keep your loan and banking in one place. Early direct deposit of your paycheck. | Most expensive option on our list. |

| Digital Federal Credit Union | Full-service credit union combines credit building with other banking services. Loans up to $3,000. | 5% APR | No fees and low APR. Available in all 50 states. | You need to join DCU and open a deposit account to be eligible. |

Is a Self Credit Builder Loan Worth It?

A Self credit builder loan may be worth it to some people.

If your only goal is to build your credit, there are many other ways to do that without having to pay. For example, a student credit card is a good option for younger people. There are many ways to build credit for free.

Even people with damaged credit or who may not qualify for a student card can apply for a secured credit card. With a deposit of a few hundred dollars, you can get a fee-free secured card that you can use to build credit.

However, if you like the idea of having something that forces you to save money while you build credit, a Self credit builder loan may appeal to you. You’ll have to decide whether you’re willing to pay the fees. If you are, then Self can help you build a small amount of savings and improve your credit.

Verdict

A Self credit builder loan is one way that you can build your credit and set some money aside at the same time. While there are free alternatives that will help you build credit, the overall cost is low enough that you might be willing to pay it for the service.

All Credit Builder Accounts made by Lead Bank, Member FDIC, Equal Housing Lender, Sunrise Banks, N.A. Member FDIC, Equal Housing Lender or Atlantic Capital Bank, N.A. Member FDIC, Equal Housing Lender. Subject to ID Verification. Individual borrowers must be a U.S. Citizen or permanent resident and at least 18 years old. Valid bank account and Social Security Number are required. All loans are subject to ID verification and consumer report review and approval. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans subject to approval. All Certificates of Deposit (CD) are deposited in Lead Banks, Member FDIC, Sunrise Banks, N.A., Member FDIC or Atlantic Capital Bank, N.A., Member FDIC.

The Self Visa® Credit Card is issued by Lead Bank, Member FDIC, Equal Housing Lender.