Grain is an app that can help you access cash quickly and build credit at the same time. It is a much cheaper alternative to a cash advance or payday loan.

With its unique features for accessing funds and building credit, Grain is an excellent tool, or at least it could be. While there are some promising features to this service, many of the customer reviews indicate that the product has serious customer service problems and could actually harm your credit.

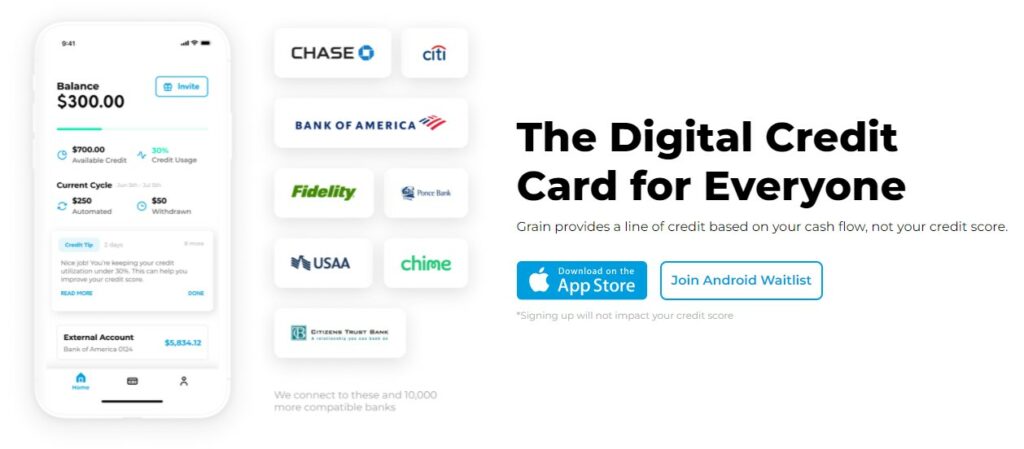

Grain Virtual Credit Card

Grain lets you build credit using a virtual credit line that allows you to transfer cash directly into your checking account. There is no credit check, and the account reports like a credit card to the credit bureaus. However, frequent bugs and related technical issues mean that users often go days, weeks, or even months without access to their accounts/funds.

Pros

Access to cash

No credit check

Builds credit like a credit card

Cons

Fee to transfer funds

Sometimes requires a security deposit

Poor customer support

May charge fees

What is Grain?

Grain is a virtual credit card that helps consumers build credit using the debit card they already have in their wallet.

There is no extra card to carry around. The Grain credit line that you receive can be directly deposited into your checking account.

Applying for Grain is quick and easy; you usually have your approval within minutes. They don’t base their decisions on your credit score. Instead, they focus on your bank account balance and spending history.

Many of the credit lines offered are unsecured, but some individuals could receive an offer for a secured credit line that will require a security deposit.

You have the option of using as much or as little of your credit limit as you want. Each month Grain will report your key account information to all 3 credit bureaus to help you improve your credit score.

How Does Grain Work?

Grain is considered a virtual credit card.

But the account operates more like a cash advance that reports to the credit bureaus as a revolving credit account, like a credit card.

Let’s take a more detailed look at setting up a Grain account and using it to build credit.

How To Setup A Grain Account

You must first download the app (currently only available for Apple devices).

⏳ If you have an Android device, there is an option to join the waitlist for the Android app.

Once the app is installed, you can begin the application process. As part of the application, you’ll need to enter your bank account details to link the account to your Grain account.

Grain will review your bank account history, looking at your income versus your spending to determine if you qualify for a credit line. They do not perform a credit check.

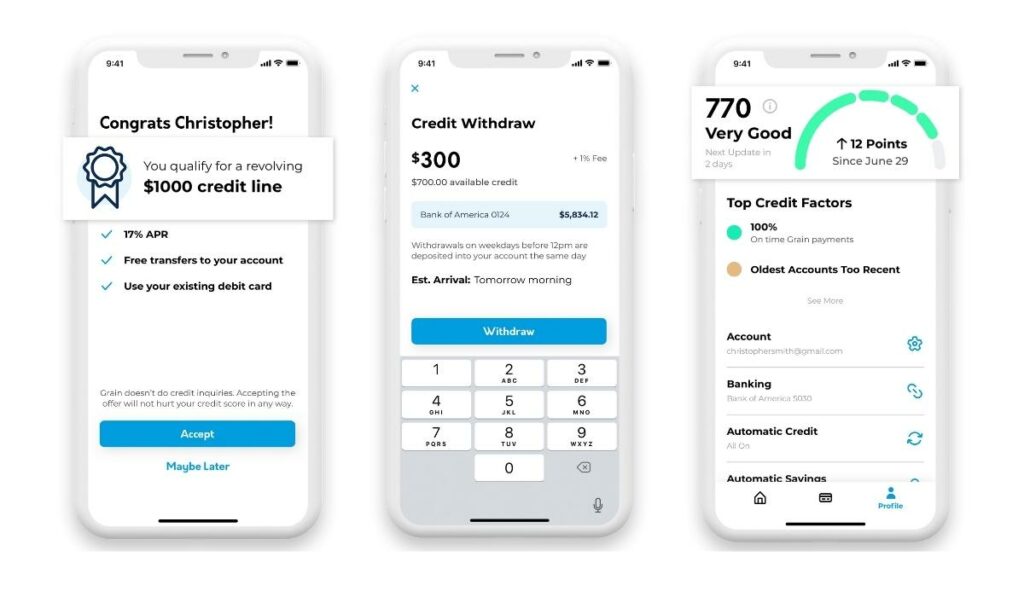

If eligible, Grain will approve you with up to a $1000 initial unsecured credit limit. And that’s it: you’re ready to go.

If you don’t meet the qualifications you will be offered a secured credit line. You’ll need to put up a security deposit before you can begin using your Grain account.

How to Use A Grain Account

First, you’ll need to transfer a portion of your credit limit to your linked bank account. You can transfer as little or as much as you want (up to your credit limit). Just be aware that the amount you transfer will determine your credit utilization rate.

For example, transferring $200 when your credit limit is $1000 will give you a credit utilization of 20%.

☝️ If your credit utilization rate is over 30% your credit could suffer. Avoid using over 30% of your credit limit.

You can then use this money as you wish. You can pay bills online, make online purchases, swipe your debit card, or draw cash out of the ATM.

Each month you’ll receive a statement, and your key account information (balance, credit limit, and payment history) will be sent to all 3 credit bureaus. On-time payments will help your credit. Late payments will hurt your credit

☝️ You’ll need to pay off your entire balance each month to avoid interest charges.

Additional Grain Features

The Grain account is designed to work with your cash flow situation to help you build credit. Here are a few unique features that Grain offers to support its customers’ financial/credit needs.

- Instant Transfer – transfer your credit line to your bank account immediately for a small fee. Not all banks support this feature.

- Custom Auto-Pay – when enabled, this feature will pay your minimum balance on a date where your cash flow is optimal. So instead of having a set payment date, this date will change each month as your expenses change.

- Credit Tips – Grain will display your credit score on your profile and offer you tips on improving it.

- Credit Line Increases – After 6 months of on-time payments and low utilization, your account can be reevaluated for a credit limit increase.

👏 These unique features could help you cover emergency expenses immediately, avoid overdraft fees, and help build credit quickly.

How to Close A Grain Account

First, you’ll need to wait until your account balance is zero. This means paying your account in full and waiting until that is reflected in the Grain app.

If you received a secured credit line (requiring a security deposit), your next step would be to withdraw your deposit.

Once that is done, or if you have an unsecured account, you will need to visit Grain’s Submit A Request page and select the “I need to close my account/application” option. Once the request is filled out and submitted, Grain will contact you to confirm account closure.

How Much Does Grain Cost?

The Grain website doesn’t mention fees, but their terms of service state that they “may” charge an annual service fee of 8% of your credit limit and a sign-up fee of $56.25 to $75.

If you are offered a secured line of credit, you must pay a security deposit.

There are two important fees to be aware of.

The first is the transfer fee. Each time you want to transfer some of your credit line to your bank account, you’ll need to pay a 1% transfer fee. If you’re going to do an instant transfer, the fee is 1.5%.

👉 So, if you wanted to transfer $200 of your credit line to your bank account, it would cost you either $2 for the standard transfer or $3 for the instant transfer.

The second type of fee to consider is interest charge.

If you don’t pay your entire statement balance by the due date, you will begin to accrue interest charges. The APR on the Grain account is 17.99%. If you enable auto-pay to cover your minimum payments, the APR will drop to 15%.

Grain Customer Reviews

While I would like to say the customer reviews for Grain are all great, they are not. They are mixed at best.

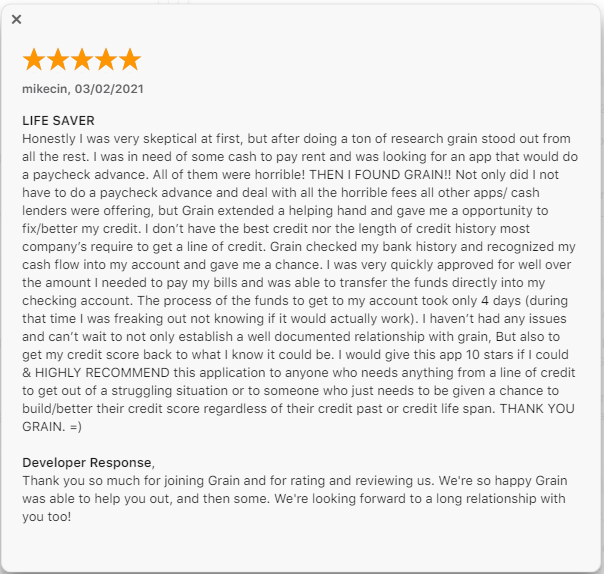

A handful of customers have seen a positive experience using the Grain account to solve their cash flow problems and boost their credit. Here’s an example from the Apple app store.

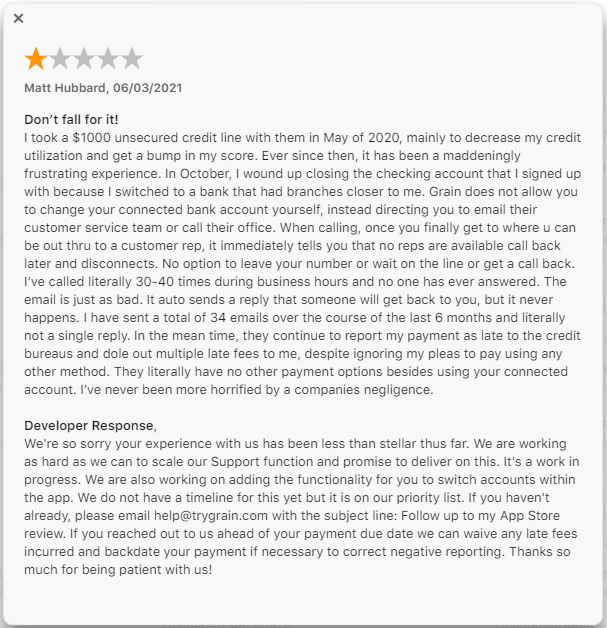

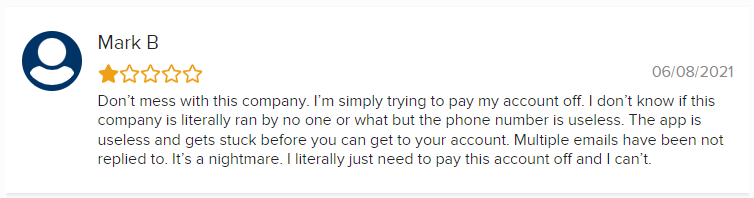

But many of the other reviews of the app or Grain’s service, in general, are very negative and critical of Grain’s absentee customer service. Here is an example from the Apple app store.

Here is another example from the BBB website where Grain Technology currently has an F rating and an abysmal 1 out of 5 stars review score.

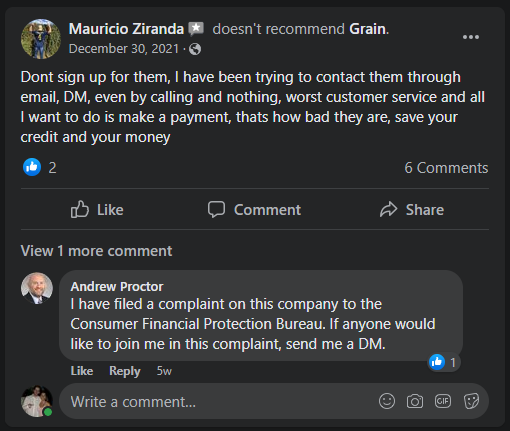

And the reviews on Facebook aren’t any prettier.

People are very angry with Grain. There are repeated complaints about a complete lack of customer service. In addition, the app seems to be buggy, and there appear to be problems with the 3rd party company they use to link to your bank account.

👉 Unfortunately, this means many customers are reporting that Grain is hurting their credit instead of helping it.

Grain Alternatives

The Grain app is one of several credit-building debit card services on the market. Though Grain is unique with its model of transferring cash directly into your checking account, there are other products out there that can build your credit in the same way.

Below are 3 of these products, along with a summary of their features, fees, and eligibility requirements.

| Chime Credit Builder | Sesame Cash | Extra | |

|---|---|---|---|

| Requirements | Requires Chime checking account | Create Sesame Cash banking account | Linked bank account |

| Unique Features | Doesn’t report credit utilization | Preset your utilization rate | Earn rewards |

| Fees | None | None | $8 – $12 a month |

| Security Deposit | $200 + | Depends on the credit limit you want | None |

| Ease of Approval | No credit check | No credit check | No credit check |

| Reports to | Experian, Equifax, TransUnion | Experian, Equifax, TransUnion | Equifax, Experian |

| Read Our Review | Read Our Review | Read Our Review |

Be aware that not all of these products build credit in the same way and not all of them report to all three credit bureaus.

There are other products still in development that are on their way to market soon. The Sequin card, for example, is a credit-building debit card geared towards women, while the Zoro Card is a subscription-based virtual credit card.

👉 The Grain account, with its unique type of credit line, will undoubtedly be appealing to many customers, but its fees, lack of rewards, and customer service issues make it far less appealing compared to its competitors.

Is Grain Worth It?

Grain seems like a worthwhile tool. It is a much cheaper alternative to a cash advance or payday loan. Account approval is income-based; they don’t even check your credit.

And, unlike other types of short-term loans (payday, title, etc.), a Grain account offers you the option to build credit if you make your payments promptly.

This should make Grain a good credit-building tool for those with little or no credit, especially those who prefer to pay for purchases using their debit card or cash. Unfortunately, the poor reviews and apparent customer service issues raise questions about whether the app can actually deliver on its potential.

☝️ Reports of the inability to change the linked bank account and irregular scheduling of automatic withdrawals are of particular concern. These issues can create late payments, which can do serious damage to your credit.

The Grain app is limited to Apple device users, which cuts out a significant number of potential consumers.

If you are an Android user, Grain will not be an option for you. Other individuals who might struggle to get good use out of the Grain account include:

- Those with low (or negative) cash flow in their bank accounts

- Someone who already has good or better credit

- Anyone who wants to earn rewards on their purchases

When it comes to the features offered, Grain is lagging a bit behind its competition. Their only worthwhile feature is the ability to transfer cash directly into your checking account.

Verdict

At first glance, Grain seems like it would be a useful tool that offers quick access to cash while also helping you build credit.

Unfortunately, the current reviews on Grain indicate the opposite.

Frequent bugs and related technical issues mean that users often go days, weeks, or even months without access to their accounts/funds.

⚠️ Problems with their bank-linking feature and the lack of an option to manually make a payment with a different account have left many users with unwanted interest charges and late payments on their credit reports.

And then there is the lack of timely customer service, with many customers going weeks or even months without hearing back from Grain. All the while, their credit scores tank because Grain is reporting them for late payments.

While the service Grain offers is an interesting concept that holds some promise, we recommend skipping this service in favor of one of the alternatives until they can get their technical issues resolved and improve their customer service.