A good credit score can make it easier to acquire a loan or credit card. It can also help you unlock lower interest rates, get better mortgage terms, and longer credit lines with better features and rewards. Even landlords and employers check credit scores!

With the strategies we have outlined in this article, and a little bit of patience on your end, you can increase your credit score by 100 points or even more.

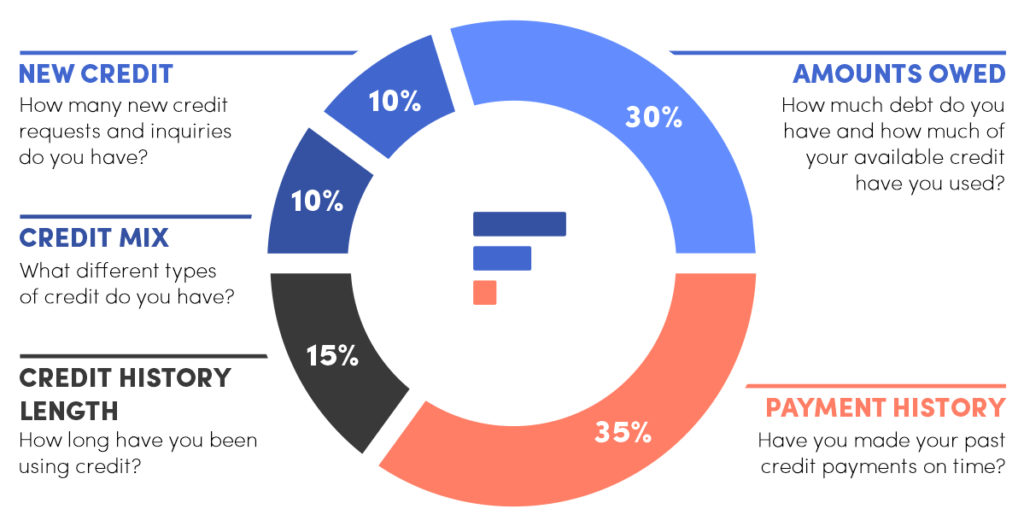

5 Ways to Improve Your Credit Score

There are 5 main factors that make up your credit score. Each of these factors can be used to improve your credit score.

- Payment History – timely payments

- Amounts Owed – your current debt and available credit

- Credit History – how long you’re using credit

- Credit Mix – how many types of credit you own

- New Credit – how many new credit requests you have made recently

1. Payment History

The single most important way to improve your credit score is by paying your credit cards, installment loans, and any other credit line on time. The key is consistency.

Since on-time payments account for 35% of your credit score, this is one of the easiest ways to improve your credit score.

In the case of credit cards, you only need to make the minimum payments for them to be counted as on-time payments and have a positive effect.

Payments that are more than 30 days late are usually reported to credit bureaus. To avoid late payments, you can set up automatic payments of the minimum payment amount on each of your credit cards, as long as you are careful not to overdraft from your bank account.

An extended history of on-time payments is one of the most effective ways to build your credit score.

2. Amounts Owed

After payment history, the amounts you owe will have the biggest impact on your credit score. The amount owed accounts for 30% of your credit score.

Lenders measure this not just as the total debt, but also by the credit utilization ratio. This is the amount of your total revolving credit limit that you are using.

Keep your credit utilization ratio below 30%. That means if you have a total credit limit of $10,000 on your credit cards, you will want to avoid carrying more than $3000 in debt.

People with credit scores of 795 and above use an average of only 7% of their available credit.

There are several ways to lower your credit utilization ratio:

- Pay off debt. The lower your balances are, the lower your credit utilization will be.

- Ask for a credit limit increase. A higher limit means lower utilization.

- Redistribute debt. Using an installment loan to consolidate your credit card debt will drop your credit utilization and could lower your interest rate.

- Open a new line of credit. A new credit card will add to your limit and reduce your credit utilization.

- Keep old cards open. Unless they carry an annual fee, it’s a good idea to keep those old cards. Their credit limits add to your total limit and lower your utilization.

💡 Remember that both your total utilization and your per-card utilization matter. Try not to bring the balance on any card above 30%. Lower is better!

3. Credit History

While you cannot retroactively open a credit card or line of credit to improve your credit history, you can become an authorized user on someone else’s card.

If you want to increase your credit history length, which makes up 15% of your credit score, the best way to do this is by being added as an authorized user by someone you know with a good credit score. You can do this for a temporary boost, such as when applying for a mortgage, or long-term for a sustained credit boost.

If you have a friend or relative with good credit history willing to add you to their oldest credit card, the additional time of good credit will give your credit score a boost.

But how do you ask your friend, parent, or family member and get them to say yes? Watch the video below to see the 5 easy steps you can take when asking your friend, mom, dad, or other relative and get them to add you as an authorized user.

You can also maintain your credit history by keeping old accounts open. Don’t close old credit cards unless they have an annual fee!

⚠️ While some people will attempt to do the same through buying tradelines, we don’t recommend it.

4. Credit Mix

Your credit mix takes into account the different lines of credit. A good credit mix includes both revolving lines of credit, like credit cards, and installment loans, like student loans, auto loans, and mortgages.

To improve your credit mix, consider what you already have.

If you only have credit cards, getting even a small installment loan, such as a credit builder loan, can improve your credit mix.

We’ve reviewed 5 of the best credit builder loans, and if you’re considering taking out a credit builder loan we recommend you check out Self or Credit Strong.

If you only have installment loans like student loans or auto loans, adding a credit card or store line of credit will improve your credit mix.

Since credit mix makes up only 10% of your credit score, this is not the most important factor to consider. But if you’ve already improved the other areas, this is a way to further boost your score. Every bit counts.

5. New Credit

Opening a new credit card is one strategy to improve your credit score, but only if you do it strategically. Too many new accounts or hard inquiries can hurt your credit score.

Avoid opening more than two to three accounts per year to avoid being penalized, and try to spread them out.

💡 Once you have an account open, try to keep it open even if you do not use the card. This will increase your total available credit and improve your credit utilization ratio.

How Long Does It Take to Improve Your Credit Score?

How long it takes to improve your credit score depends on your individual credit history and situation. Many people can see improvement in as little as a month.

The time it takes to change your credit score is heavily affected by the amount of information in your credit file. If you have a thin credit file with a small number of accounts, any change, even a small one, will have a noticeable impact. If you have many accounts and a long credit history it will take more time and effort to change your score.

Research from FICO shows that it can take 3 months for credit to return to its previous level after closing a credit card account, maxing out a credit card, or applying for a new credit card. Late mortgage payments can affect credit scores for 9 months, while missed or defaulted payments can decrease credit scores for 18 months.

If you’ve had any of these situations, you can expect your credit score to gradually increase over 3 to 18 months.

Fastest Ways to Improve Your Credit Score

If you’re looking for an immediate boost to your credit score, you have a few options:

- Pay off credit card debts

- Pay installment debt on time

- Be added as an authorized user

- Ask for a higher credit limit

- Get credit for what you pay

- Dispute inaccurate information on your credit report

1. Pay Off Credit Card Debt

Paying off any credit card balances is good for both your credit and your finances. Your credit utilization will drop and you won’t be paying interest!

2. Keep Up With Installment Debt

There’s generally no advantage to your credit in paying off installment loans early. A loan that’s paid will still be on your credit record, but active accounts have more impact than paid accounts.

You want to be sure to make every payment on time, but keeping that live installment loan on your record will help your credit more than paying it off early.

3. Become an Authorized User

If you are added as an authorized user to someone with good credit and a longer credit history, you can get an instant credit score boost.

If you have a credit history of 10 years, and a friend has a credit history of 20 years and a higher overall credit score, being added to one of their cards will double your credit history length, instantly improving your credit score.

4. Ask for a Higher Credit Limit

Asking for a higher credit limit can improve your credit score quickly. If your credit card has a limit of $5000, ask for an increase to $7000 or $8000. This can instantly reduce your credit utilization ratio and increase your credit score.

📚 Explore how to increase your credit limit, and the most important things to consider before you do.

5. Get Credit for What You Pay

Another way to build credit is to have payments you make on a regular basis added to your credit profile. You may be able to get regular expenses like your mobile phone bill, rent, and utilities included in your credit report. You have to pay them anyway, so you might as well gain from them.

Experian BOOST™ and TransUnion’s eCredable Lift can help you improve your credit score by giving you credit for paying utilities and other bills on time.

Grow Credit places streaming service bills on your credit report.

If you rent your house or apartment you can get a big credit score boost by reporting your rent. Companies like Boom and Rent Reporters will report your rent to the credit bureaus.

We’ve reviewed 12 of the best rent reporting services, and if you’re considering rent reporting the review is a great place to start.

6. Dispute Inaccurate Information on Your Credit Report

Be alert to get your free credit reports from Experian, Transunion, and Equifax. Learn how to read a credit report. If you spot any incorrect or inaccurate information, use the dispute process to have them removed.

Knowing your credit reports will help you know how much work you have to do to improve your credit.

If you have legitimate late payments, chargeoffs, or collection accounts on your record you can help by paying the accounts off, but they will remain on your record for seven years from the date of the first delinquency. That sounds like a long time, but older accounts affect your credit score less than newer ones, so the impact of those old black marks will fade as time goes by.

What Not to Do

Many people who are eager to improve their credit embrace methods that are risky or ineffective. Some even fall victim to credit repair or debt relief scams.

⚠️ If anyone promises that they can improve your score instantly or remove legitimate items from your credit report, be careful. It’s easy to make promises but hard to deliver on them, and you may end up spending money for nothing.

There are legitimate credit repair companies but also many that are less legitimate. do your research carefully before hiring someone to improve your credit, purchasing tradelines from someone else, or using other shortcuts.

In general, it’s not a good idea to spend money to improve your credit score. If you open a new credit line, only use it to buy things that you need and would have bought anyway. If you get a new credit card or keep an old one just to help your credit, be sure you’re not paying annual fees for those cards. Getting a credit line at an online store that sells overpriced goods is a poor way to build credit.

You want your spending to work for you, not against you!

How To Improve Your Credit Score In 30 to 60 Days

The best way to improve your credit score in 30 days is to use the strategies to instantly improve your credit score. Your 30 to 60-day credit score boosting checklist:

- Debt: Pay off as much credit card debt as possible. If not all, try to get the credit utilization ratio below 30%, lower if possible. Make installment loan payments on time.

- Credit Limit: Ask for a higher credit limit with each of your credit card companies.

- Credit History: If you know someone, like an older relative, with good credit history, ask to be added as an authorized user.

- Get Credit For What You Pay For: You can boost your credit by reporting your utility, rent, and even streaming service bills.

- New Credit: If you haven’t opened a new line of credit in at least 3 months, opening a new line of credit will increase your total credit limit and can increase your credit score.

Be sure to make all payments on time and focus on paying off as much debt as possible. These strategies together will show a boost in your credit score in 30 to 60 days.

How to Improve Your Credit Score in a Year

If you have a year to improve your credit score, first follow all the strategies we recommended for increasing your credit score in 30 to 60 days.

Here’s what else you can do to increase your credit score in a year:

- With a year to plan, you can open two new credit cards in the first 6 months of the year to increase your total available credit.

- Diversify your credit mix. Try to have at least one revolving line of credit, like a credit card, and one installment loan, like an auto loan, student loan, or credit builder loan.

- Finally, near the end of the year, after paying on time and decreasing debt throughout the year, you can request an increased credit limit again.

Be sure to make all payments on time!

FAQ

Active accounts have more impact on your credit score than past accounts. While you are paying off a loan, it is active. If you make the payments on time, they boost your score and raise the average age of your active accounts.

Once the debt is paid, it is no longer active. The payment history of the debt has less impact, and the average age of your active accounts may fall. This may cause a small, usually temporary, drop in your credit score.

When you apply for new credit, a hard inquiry is registered on your credit report. This can cause a small, temporary drop in your credit score. If you make all payments on time and keep your credit utilization low, your credit score should improve.

When you close a refinancing deal, you will likely see a drop in your credit score. That’s partly because of the hard inquiry made by your lender and partly because you’ve taken on a new loan and haven’t proven that you can pay it.

Make your payments on time, and your score will recover quickly.

Check out the email I got from my new rent reporting company BOOM