Lenders break credit scores into ranges. These may be described in several ways. Some lenders may call scores poor, fair, good, and excellent, some may use subprime, near-prime, prime, and super-prime. Either way, they are combining a group of scores into a single block with similar characteristics.

Grasping the concept of credit score ranges will give us a better idea of how lenders use credit scores and how much you’ll need to add to your score to move into a better credit score range. Let’s explore the fundamentals of credit score ranges and how they shape your financial journey.

Key Takeaways

- A range is a block of credit scores. Using score ranges makes it easier for lenders to categorize borrowers by the amount of risk they pose.

- Different lenders use different ranges. Understanding how different lenders use credit score ranges can help you get better deals.

- Ranges affect loan terms: Your credit score range directly influences the interest rates and terms you’ll receive on loans and credit cards.

- Improve your score for better terms: Moving your credit score into a higher bracket can save you money.

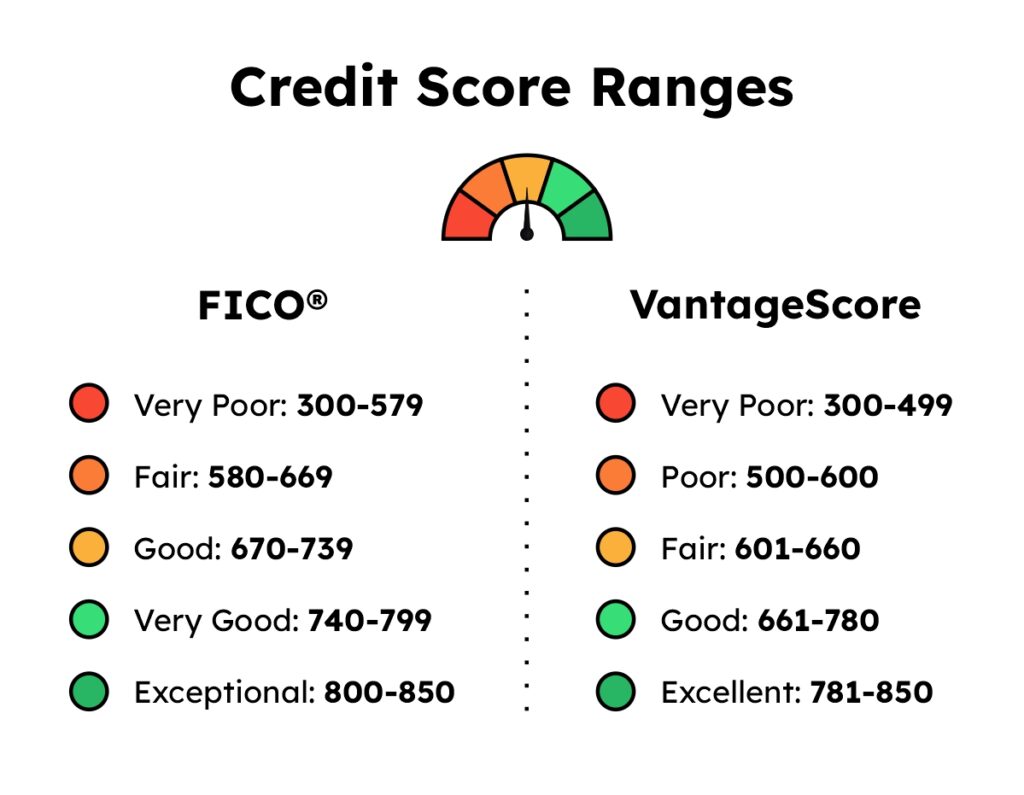

FICO® and VantageScore Credit Score Ranges

Credit scores are provided by two major companies: FICO® and VantageScore. They calculate scores using slightly different formulas and group their scores in slightly different ranges.

Both FICO® and VantageScore divide credit scores into ranges that define general risk brackets. Lenders use these ranges to help them decide what credit terms to offer.

🤔 Did you know you have more than two credit scores? In fact, you have over 30 of them. Here’s a list of all types of credit scores you should know, along with their credit score ranges.

Excellent

The credit score range for “exceptional” borrowers is 800 to 850 for FICO®.

For VantageScore, a score of 781 to 850 will put you in the “excellent” credit score range.

Borrowers in this range will have no problem getting approved for loans or credit. You’ll receive the best lending terms offered, including the lowest interest rates and fees. If your credit score is exceptional, lenders roll out the red carpet!

💡 Only 1.5% of Americans have an exceptional credit score of 850.

Very Good

If your FICO® score is between 740 and 799, you fall into the “very good” category.

VantageScore does not have a range with a “very good” designation.

Individuals who fall in this range often qualify for better interest rates on loans and credit cards, and will generally have an easier time with the lending process.

Good

A score from 670 to 739 falls into FICO’s “good” category.

The VantageScore “good” range is 661 to 780.

If your score is within this range, you are close to the national average (the current FICO® average for Americans is 715). Lenders see a score in this range as an indication of an acceptable borrower and it will qualify you for most loans and credit cards. You may not receive the best available terms, and you’re likely to pay a higher interest rate than borrowers with very good or exceptional credit scores. You may not qualify for highly selective premium credit products.

Fair

FICO® scores that range from 580 to 669 fall into the “fair” range.

The VantageScore “fair” range is 601 to 660.

This range may disqualify borrowers from some loans. Some lenders may class borrowers in this range as subprime. Some lenders may not approve your application at all. If they do approve your application they may offer a higher interest rate than borrowers with better credit would get.

Poor

FICO® doesn’t have a “poor” classification, but VantageScore does. VantageScore rates a credit score between 500 and 600 as poor.

It will be difficult to get credit with a poor credit score. Lenders who do approve you will charge very high interest rates.

Very Poor

A FICO® score between 300 and 579 is considered “very poor”.

This is often caused by bankruptcy or other major credit problems. Most lenders will not extend credit to applicants with scores in this range. If you’re applying for a credit card, your only option may be a secured credit card where you put down a deposit equal to the amount of the spending limit. Utilities will probably require a deposit.

No Credit

As many as 26 million Americans have no credit score and another 19.4 million have thin credit files.

Having no credit can be even more frustrating than having a low score, especially if you have no debts and your finances are in good order. If you don’t have a credit score, it’s probably because you have a “thin credit file,” which means you don’t have much credit history or activity. If you have no credit information on file or there is not enough information on your credit report to generate a score – you will have no credit score.

Percent of Americans In Each Credit Score Range

FICO®

VantageScore

Some Lenders Use Their Own Ranges

Many lenders adopt the ranges used by FICO® and VantageScore. Others may develop their own classifications. Major lenders may use different ranges to classify potential borrowers by risk level. Many lenders publish their credit score ranges or provide them on request.

If you’re considering applying for a credit card or a significant loan, find out what score ranges the lenders you’re considering use. Check your score and see where you fit. Don’t just consider the minimum standard for approval. Check the ranges that the lender uses to determine interest rates.

Fitting into a higher range can get you significantly lower interest rates, and that can save you money.

Know Your Credit Score Range

The concept of credit score ranges may seem unfair at first glance.

If your FICO® score is 660 you may wonder why you get offered the same loan terms as a borrower with a score of 590 but less attractive terms than a borrower with a score of 670. Some lenders will adjust terms according to your position within a range, but in many cases, the range defines the terms you are offered, fair or not.

💡 If your score falls at the upper end of a lender’s range, ask whether they will give you a break and put you in the higher range.

They may agree, especially if your financial record is generally good. If they won’t, look into other comparable lenders. You may find one that breaks up their score ranges in a way that’s more favorable to you.

If you don’t find a lender that will fit you in a higher range, consider waiting and trying to improve your credit score. A little time and effort could save you real money, and once you start working on building your score you can keep on building it and move into an even higher range.

It is possible to build better credit. If you understand how credit scores are calculated and take a few simple steps, you can improve your credit score. You can rebuild a damaged credit score or start one if you haven’t got one. You may have to wait a bit for that loan or credit card, but you may be doing yourself a big favor!