We all know it’s important to know your credit score. But you have several credit scores, and which do you need to know? Let’s look at VantageScore 3 vs FICO 8 and the difference between them.

Understanding one credit score is hard enough. That’s not all you have, though. You may have heard of credit scores from VantageScore and FICO, but what’s really the difference?

I have been tracking my credit scores with all three of the major credit bureaus – Equifax, Experian, and TransUnion – for my journey from a poor credit to a 700 credit score. That’s why I have been tracking my credit score with all three of the major credit bureaus; Equifax, Experian, and TransUnion.

There are many documented differences between the two scores.

Free vs Paid: The Big Difference Between FICO and Vantage Score

It typically costs money to get your FICO scores. Some credit card companies or banks will give you a free score but it’s usually from ONE credit bureau only. For all three scores, sign up for the myFICO service.

You can typically get your Vantage Scores for free using services like Credit Karma or Credit Sesame.

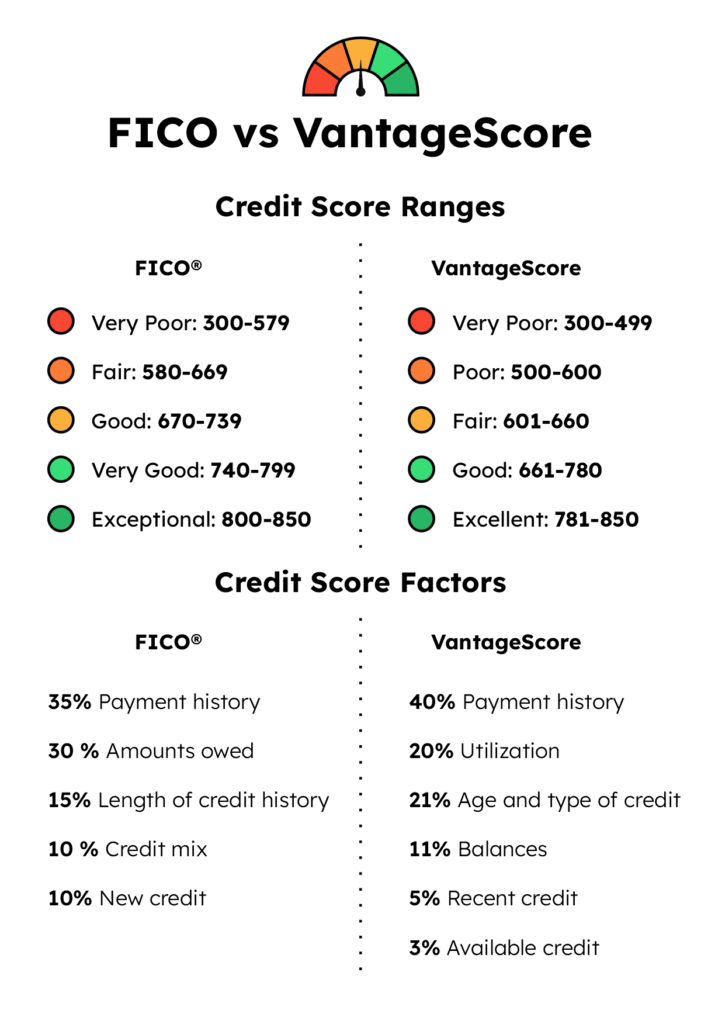

FICO and VantageScore use the same information – your credit reports – to generate your credit score. They may process this information in different ways.

If you’d like to know more about the factors that influence your credit score, read our article on how credit scores are calculated.

Below are three VantageScore 3.0 vs FICO 8 credit score comparison charts for TransUnion, Experian, and Equifax with my credit scores.

I will update these charts on a monthly basis and make notes of any movements and speculate the cause or reason for the difference.

EQUIFAX – FICO VS VantageScore Comparison Chart

I have been tracking my Equifax VantageScore with Credit Karma’s free credit monitoring services.

In addition, I have purchased MyFICO’s credit monitoring service, which provides me with FICO scores for all three of the major credit bureaus; Equifax, Experian, and TransUnion.

In the FICO vs Vantage comparison chart above, you can see that Vantage in the blue line reacts much more extremely to credit report changes than the FICO credit score, represented by the orange line.

Generally, the lines go up and down around the same time, reacting to the same information, it is just that the VantageScore 3.0 is more volatile.

Interestingly, the early large dip in March was due to me disputing my Equifax credit reports.

You can read more about how my Equifax Dispute lowered my credit score by almost 70 points around March 12, 2019!

EXPERIAN – FICO VS VantageScore Comparison Chart

The more you look at these charts and compare Experian Vantage Score vs FICO, the more you realize how different these two credit scores can be.

Keep in mind that the majority of lenders are using your FICO score to determine loan eligibility.

By looking at the huge swings and differences between the two scores, it is no wonder why.

Understand that my Vantage Score is provided by my Credit One Secured Visa card for free.

They provide me with a snapshot credit score one time a month for Experian.

This is a great example of why you should purchase a credit monitoring service instead of relying on a once-a-month free snapshot of your credit score.

I don’t understand how in February, my VantageScore was around 500 but my FICO credit score was over 575 and nearly 600.

However, a month later, my credit score with Vantage went up over 150 points in 30 days to a 650.

I understand that March was a huge month for me with all the tools I implemented to build my credit score but I think that this is a great example of the difference between the two scores.

VantageScore reacts extremely positively to every credit building move you make, whereas, FICO’s reaction is more tempered, like the older and more mature brother who doesn’t quite react as immaturely as his younger sibling, Vantage Score 3.0.

TRANSUNION – FICO VS VantageScore Comparison Chart

I feel like the TransUnion VantageScore 3.0 vs Fico credit score 8 comparison chart is the most accurate reflection of my credit history the past couple of months…

With one MAJOR exception!

Take a look at the blue Vantage line and how it pretty much tracks right along with FICO orange credit score line.

Until it doesn’t…

In early April, we had a major disagreement between Vantage and FICO to the tune of over 50 points.

What happened?

Well, do you remember when I disputed all of my credit reports in March?

For some reason, TransUnion 3.0 score pretty much dropped every delinquent account on my credit history, in fact, my on-time payment history with TransUnion Vantage is 99%, whereas it is around 70% with Experian and Equifax.

I know, you are wondering why that would increasing my payment history hurt my credit?

Well, to get my on-time payment history to 99%, TransUnion pretty much deleted my entire credit history and now it looks like I have only had credit for the last couple of years.

This is a weird situation that currently has my Vantage score nearly 75 points lower than my FICO TransUnion score.

We’ll keep monitoring it and let you know!

Informative. Thank you. Two questions:

– If you are declined financing based on FICO can you request the lender utilize your Vantage ?

– What type of lender is more likely to run your Vantage?

Thanks!

Very informative! Goes to show how useless the bureau models are.