A credit score in the range of 580-669 is labeled “fair” by American standards. Having this fair credit score qualifies you for many credit cards, but you have to make your choice wisely. In this post, we’ll show you how to navigate all the different rates, offers, rewards, and fees in order to pick the best credit card for fair credit.

How We Picked These Credit Cards

When looking for the best credit cards for fair credit, we took the following things into account: Is there an annual fee? Is there a fee for international spending? What other fees does the card have? What is the APR (Annual Percentage Rate)? Does the card offer rewards? Does the card have a signup bonus? Does the card have any other perks?

Based on all this research, here’s our top six for customers with fair credit:

| Why This Card | Annual Fee | Regular APR | Rewards | Credit Score | |

|---|---|---|---|---|---|

| Capital One Platinum Credit Card | Best No-Fee Card | $0 | 30.74% (Variable) | No | 580+ |

| Petal® 2 “Cash Back, No Fees” Visa® Credit Card | No Fee Plus Rewards | $0 | 18.24% – 32.24% (Variable) | Yes | 630+ |

| Avant Credit Card | No Penalty APR | $0-$75 | 29.24% – 35.99% (Variable) | No | 580+ |

| Capital One Walmart Rewards® Mastercard® | Best for Walmart Shoppers | $0 | 18.99% – 29.99% (Variable) | Yes | 580+ |

| Discover it® Student chrome | Best for Students | $0 | 18.24% – 27.24% (Variable) | Yes | 640+ |

| Upgrade Cash Rewards Visa® | The Most Innovative Deal | $0 | 14.99% – 29.99% (Variable) | Yes | 580+ |

BEST NO-FEE CARD

Capital One Platinum Credit Card

Annual Fee

$0

Regular APR

30.74% (Variable)

Rewards

No

Credit Score

580+

The Capital One Platinum Card is a simple, basic credit card with no annual fee and no international transaction fee. The minimum credit score is 580, so it’s accessible with fair credit. That figure was not provided by Capital One and is not a preapproval offer. You can check for pre-approval with no hard credit inquiry on the website.

You’ll have fraud coverage and unlimited access to your credit score. You may be considered for a higher credit limit in as little as 6 months. There are no rewards: this is a basic card.

👎 The downside: There’s a high 30.74% variable APR. Only use this card if you are sure that you’ll be paying off the balance in full every month.

NO FEE PLUS REWARDS

Petal® 2 “Cash Back, No Fees” Visa® Credit Card

Annual Fee

$0

Regular APR

18.24% – 32.24% (Variable)

Rewards

Yes

Credit Score

630+

The Petal® 2 “Cash Back, No Fees” Visa® Credit Card (issued WebBank) has no annual fee and a variable APR of 18.24% – 32.24%. There are no international fees, making this a great travel card. You’ll also get free access to an app that helps with budgeting and with financial decisions.

🎁 Rewards: You get 1% cash back on purchases and 2% to 10% cash back at selected merchants. You also get 1.5% cash back on eligible purchases after 12 on-time monthly payments.

👎 The downside: The minimum credit score is 630, so you’ll need to be in the upper half of the “fair” range to qualify. Petal will qualify applicants with no credit score on the basis of bank account information.

NO PENALTY APR

Avant Credit Card

Annual Fee

$0-$75

Regular APR

29.24% – 35.99% (Variable)

Rewards

No

Credit Score

580+

The Avant Credit Card has a minimum credit score of 580, placing it squarely in the fair credit score bracket. You can miss a payment without triggering a penalty APR, a plus for the absent-minded or those on a shoestring budget. You may pay a late fee. The regular APR is 29.24%–35.99%, depending on your credit.

👎 The downside: You may pay an annual fee, varying with where you applied. See the issuer’s website for details.

BEST FOR WALMART SHOPPERS

Capital One Walmart Rewards® Mastercard®

Annual Fee

$0

Regular APR

18.99% – 29.99% (Variable)

Rewards

Yes

Credit Score

580+

The Capital One Walmart Rewards Mastercard is a great deal if you shop at Walmart regularly and a decent deal even if you don’t. The minimum credit score is 580. There is no annual fee or international transaction fee, and the APR is 18.99% or 29.99%.

🎁 Rewards: The real story here is the rewards.

- 5% cash back for online purchases at Walmart.com.

- 2% cash back at Walmart stores, restaurants, and on travel.

- 1% cash back on other purchases.

- Earn 5% cash back in Walmart stores for the first 12 months after approval when you use your Capital One Walmart Rewards® Card with Walmart Pay.

The rewards do not expire.

👎 The downside: The APR is on the steep side. Pay your balance in full on or before the due date!

BEST FOR STUDENTS

Discover it® Student chrome

Annual Fee

$0

Regular APR

18.24% – 27.24% (Variable)

Rewards

Yes

Credit Score

640+

The Discover It Student Chrome card is a solid offer for college students. There’s no annual fee or international transaction fee. There’s a 0% intro APR on purchases for 6 months. The regular APR is from 18.24% to 27.24%. Even applicants without a credit score may qualify.

🎁 Rewards: You get 2% cash back on gas and restaurant spending, up to $1000 per quarter. There’s 1% unlimited cash back on other purchases. Discover will automatically match all the cash back you’ve earned at the end of your first year!

👎 The downside: The 2% cashback reward comes with a low spending limit, only $1000 per quarter.

THE MOST INNOVATIVE DEAL

Upgrade Cash Rewards Visa®

Annual Fee

$0

Regular APR

14.99% – 29.99% (Variable)

Rewards

Yes

Credit Score

580+

The Upgrade Visa Card with Cash Rewards is a different kind of credit card. The basics are not unusual. There’s no annual fee, activation fee, or maintenance fee. The APR ranges from 14.99% to 29.99%.

The feature that makes this card different is that any balance carried beyond the due date is converted to a fixed-rate installment loan. You’ll pay in equal monthly installments, which makes budgeting easier. You can also request a personal loan through your card, with funds sent straight to your bank.

🎁 Rewards: You’ll get 1.5% unlimited cash back when you make a payment.

$200 bonus after opening a Rewards Checking account and making 3 debit card transactions.

👎 The downside: The minimum credit score is 580, so if you’re at the lower end of “fair” you may not qualify. Interest rates may be high.

What You Need to Know Before Picking a Card

There are some factors you need to consider and keep in mind when picking your next credit card – any card, not just the ones for fair credit.

Watch Those APRs

If we look at the details of these cards, one thing becomes clear: interest rates are high. They are the highest of all if you’re at the lower end of the credit score range for that card.

☝️ When a card issuer cites a range of APRs you can be sure that people at or near the minimum score for that card will be paying the rate at the high end of the range.

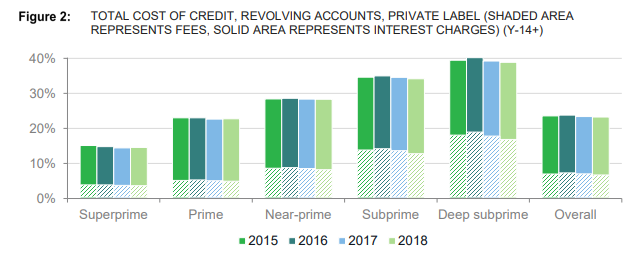

Revolving credit – predominantly credit cards – gets very expensive with a low credit score. Look at the data:

Source: Consumer Financial Protection Bureau

Fortunately, you don’t have to pay those high-interest rates. If you pay each bill in full on or before the due date, you will pay no interest at all. When your card carries an APR over 20%, compounded daily, that’s a very good thing.

Use Your Credit Card Wisely

A credit card can be a convenience or a catastrophe. It can help you build credit or help you destroy it. To keep your outcomes positive, remember these points.

Your credit card for fair credit will affect your score in two main ways.

- Payment history makes up 35% of your FICO score. Making payments on time is the single most important thing you can do to boost your credit.

- Credit utilization makes up around 30% of your score. Your credit utilization rate is the percentage of your credit limit that you actually use. If your credit limit is $1000 and your balance is $300 your credit utilization rate is 30%. Keeping your balance below 30% of your limit will help your credit and keeping it lower will help your credit more.

Here’s what you need to do to make your card an asset instead of a liability.

- Use your card. An active card does more for your credit than a dormant one.

- Pay every bill on time. Late or missed payments kill credit. On-time payments build credit.

- Pay every bill in full. If you pay in full before the due date, you won’t pay interest. That’s a free loan from the card company! If you carry a balance you will pay high interest, compounded daily.

- Never make the minimum payment. Minimum payments are a one-way street into the credit card debt trap. Even if you can’t pay the whole balance, pay as much above the minimum as you can.

- Keep your balance low. Remember your credit utilization and keep track of it.

Using a credit card wisely takes discipline, but that discipline will build your credit and prevent you from accumulating high-interest debt.

Build on That Start

Once you’ve established good habits with your credit card, consider an installment loan. Many banks and credit unions offer credit-builder loans, or you can apply with an online lender like Self. These loans are designed for people with poor credit. They put an installment loan on your record, which improves your credit mix, and if you make your payments on time you’ll be boosting your score.

Knowledge is the key to building better credit. Start by learning how your credit score is calculated. Get your credit reports: they will give you better awareness of your own financial situation. If you have trouble understanding them, look at this guide to how to read a credit report. Many credit reports contain errors. You’ll want to watch out for them and dispute any problems that you find.

There’s no need to hire a person or company to improve your credit. You can do anything they can do. If anyone tells you that they can remove legitimate items from your credit report, give you a new credit identity, or fix your credit issues, you may be looking at one of many debt relief or credit repair scams.

It takes time and effort to rebuild damaged credit. It’s worth it to make the effort. You won’t just be raising your credit score, you’ll also be taking control of your financial life!

Conclusion

Here are our top picks for the best credit cards for fair credit again, plus their most standout features:

| Why This Card | Annual Fee | Regular APR | Rewards | Credit Score | |

|---|---|---|---|---|---|

| Capital One Platinum Credit Card | Best No-Fee Card | $0 | 30.74% (Variable) | No | 580+ |

| Petal® 2 “Cash Back, No Fees” Visa® Credit Card | No Fee Plus Rewards | $0 | 18.24% – 32.24% (Variable) | Yes | 630+ |

| Avant Credit Card | No Penalty APR | $0-$75 | 29.24% – 35.99% (Variable) | No | 580+ |

| Capital One Walmart Rewards® Mastercard® | Best for Walmart Shoppers | $0 | 18.99% – 29.99% (Variable) | Yes | 580+ |

| Discover it® Student chrome | Best for Students | $0 | 18.24% – 27.24% (Variable) | Yes | 640+ |

| Upgrade Cash Rewards Visa® | The Most Innovative Deal | $0 | 14.99% – 29.99% (Variable) | Yes | 580+ |