Some online store credit cards offer almost guaranteed approval. However, you should be careful before applying. Not all are good deals and some won’t help you grow your credit.

If you’re struggling to build credit you may be looking for any credit account you can get. Some online store accounts may be able to help, but be alert for high prices, fees, and other downsides like not reporting to the credit bureaus. You may be better off with a secured credit card.

If you do decide to pursue an online store card, here are some options.

4 Online Store Credit Card Options For Easy Approval

Finding a good store credit card when you have bad credit can be very frustrating.

If you apply for cards you can’t get approved for, you’ll be racking up hard inquiries and damaging your credit.

Getting an online store credit card with guaranteed approval is simple and there are several options to choose from.

#1

Fingerhut Credit Card Account

Fingerhut is a super easy account to obtain. An account with Fingerhut doesn’t come with an annual fee and Fingerhut reports to all three major credit bureaus. You can only use the card in the Fingerhut store and goods are overpriced. Learn more

Membership Fee

$0

Regular APR

35.99%

Credit Limit

$300+*

Credit Score

350 – 679

Poor To Average

*Fingerhut does not state the initial credit limit. According to various online forums, it can be anywhere from $300 to $3,000+ depending on your creditworthiness.

#2

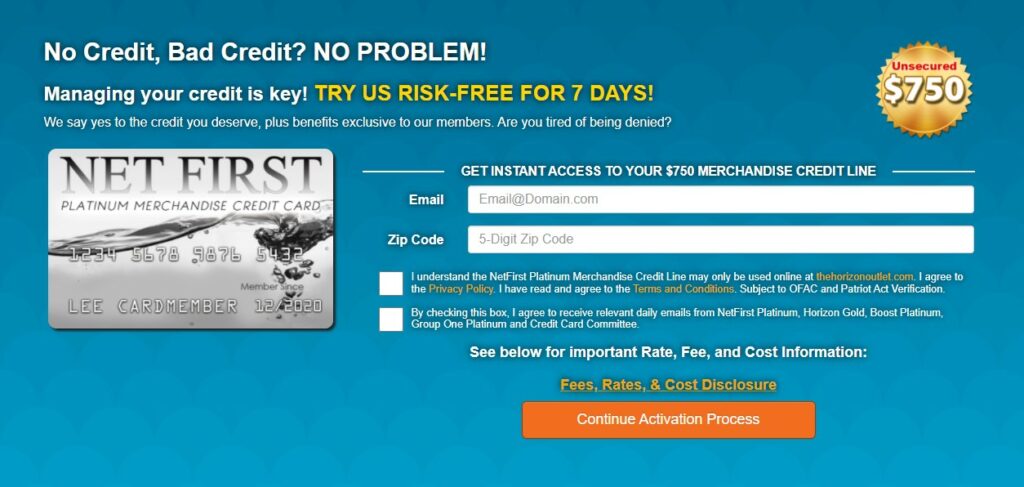

Net First Platinum

The good thing about Net First Platinum is that you are guaranteed a credit limit of $750 dollars to use on the Horizon Outlet. The bad news is that it comes with a monthly fee and does not report to the credit bureaus. Learn more

Membership Fee

$14.77 per month

Regular APR

0%

Credit Limit

$750*

Credit Score

350 – 679

Poor To Average

*Usable only at the HorizonOutlet.com

#3

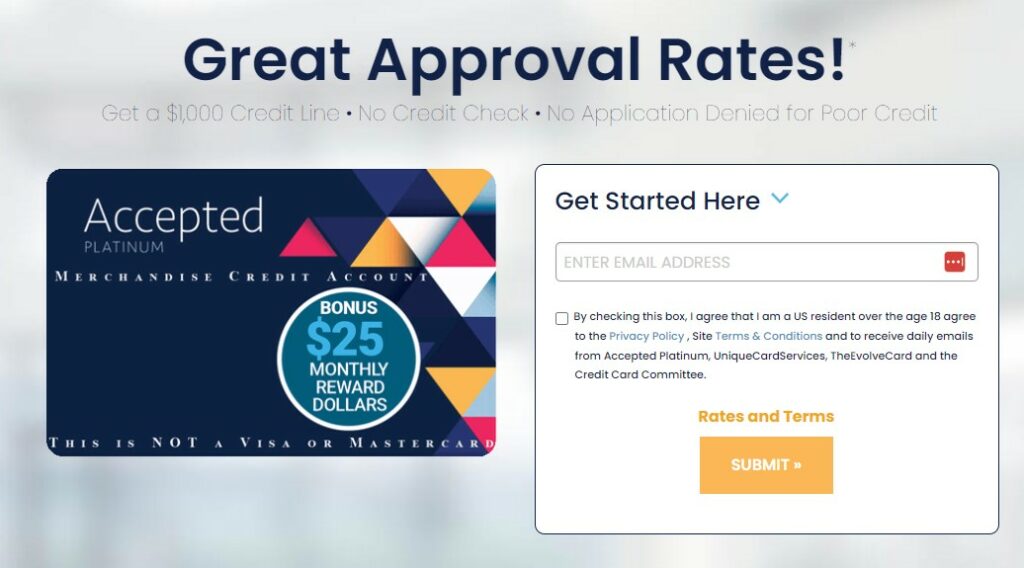

Accepted Platinum

Accepted Platinum is very easy to get approved for, but it does not report to credit bureaus, and you can only use the card at MyUniqueOutlet. The only advantage of this card is that you get a higher credit limit than with most other cards. Learn more

Monthly Fee

$19.95/mo

Regular APR

0%

Credit Limit

$1,000*

Credit Score

Any Credit Welcome

*Usable only at the MyUniqueOutlet.com

#4

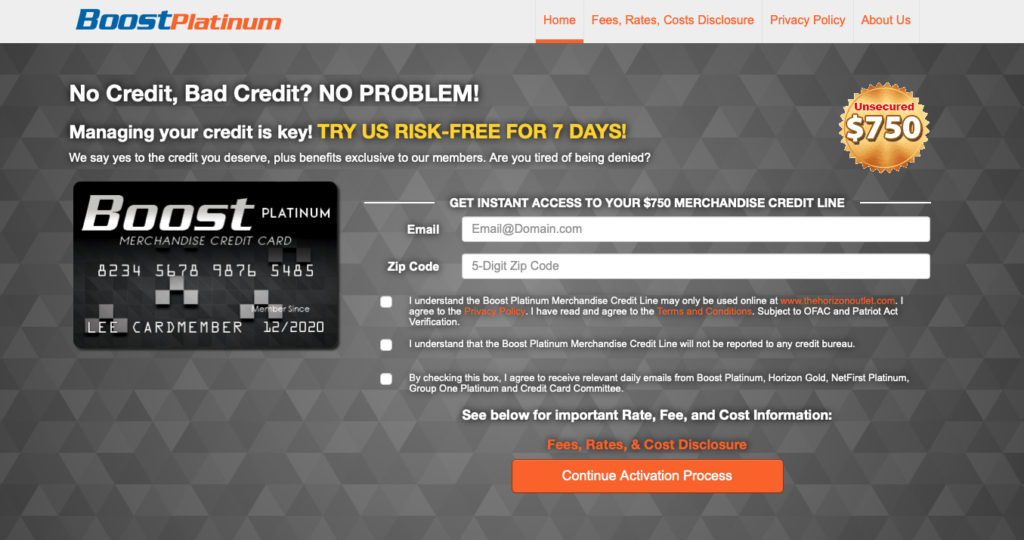

BOOST Platinum Card

BOOST Platinum Card is another card that can be used on Horizon Outlet. It comes with the same terms as Net First Platinum and does not report to the credit bureaus. Learn more

Monthly Fee

See website for details

Regular APR

0%

Credit Limit

$750*

Credit Score

Damaged credit to Fair credit

*Usable only at the HorizonOutlet.com

Fingerhut Credit Card Account

Fingerhut is a super easy account to obtain. An account with Fingerhut doesn’t come with an annual fee and Fingerhut reports to all three major credit bureaus.

To make things better, pretty much no one will be declined. You will either be approved for a Fingerhut Fetti account or a Fresh Start account.

If you are trying to rebuild or establish credit and want a nearly certain approval, then the Fingerhut credit card account is worth a look.

Pros & Cons

While this account is an excellent option for re-building your credit or getting your credit started, there are still some things you must consider when making a choice. Here are the pros and cons of the card:

➕ Pros

- Build Your Credit. Your on-time payments will be reported to Equifax, Experian, and Transunion.

- No Annual Fee. You don’t need to worry about huge annual fees eating into your credit limit.

- Guaranteed Approval. Seriously, you will get approved for at least one of their accounts.

- 400,000 Items To Choose From. Thousands of everyday Items to purchase.

➖ Cons

- Can Only Use At Fingerhut. You can only use your credit limit at Fingerhut.com.

- 35.99% Interest Rate. The interest rate is really high; however, it’s a really small price to pay to get your credit back in shape. Just keep your balance low!

- Hard Credit Pull. While your approval is pretty much guaranteed, you will still receive a hard credit pull.

- High prices. Products sold in the Fingerhut store are substantially more expensive than the same products in other stores.

📞 Customer Service

Fingerhut has 24/7 customer service and they are easy to reach. Just call 800-208-2500.

Verdict

You won’t be using Fingerhut to furnish your home. However, you can use it to purchase a few things you need and establish your credit.

If you pay your bill on time after a few months you will start to receive credit limit increases. These can help you lower your credit utilization.

This is a low-cost way to start building credit. Just keep your purchases limited to inexpensive items that you would have bought anyway, and keep your eye on the prices.

Net First Platinum Card

Net First Platinum is a third-party card to the Horizon Network and it functions exactly like the rest of Horizon cards.

You are guaranteed a credit limit of $750 dollars to use inside the Horizon Network.

As mentioned earlier, this network doesn’t have as many buying options as Fingerhut.

You will still get the same Zero percent APR for the items you purchase. You will still also get that $14.77 monthly fee.

Pros & Cons

This is another account where there are more things we don’t like than we do like.

➕ Pros

- No Employment Required. No proof of income or employment is needed to obtain this account.

- No Credit Check. You will not harm your credit if you apply for this card.

➖ Cons

- $14.77 Monthly Fee. A $177 annual fee is charged to your balance throughout the year making this a very costly card.

- Doesn’t report to credit bureaus. The card won’t help you build credit.

- Can Only Use At Horizon. You can only use your credit limit at the Horizon Outlet and no other store or location.

📞 Customer Service

Net First Platinum is a third-party card of the Horizon network and also has some of the worst customer service reviews on the BBB.

Verdict

This product sounds great on the surface with a 0% APR, guaranteed approval, and a starting credit limit of $750.00*.

The annual fee is simply too high for this to be a good idea.

*usable only at the HorizonOutlet.com

Accepted Platinum

Accepted Platinum is the latest merchandise card that pretty much anybody can get approved for. The card is specifically marketed to people with bad credit, so getting approved is guaranteed.

The card’s unique offerings are the extra features it comes with:

- Discounts at 62,000 pharmacies

- Free and discounted legal care

- Roadside assistance

- $25 in reward dollars every month

Pros & Cons

As with most of these cards, there are more drawbacks than benefits.

➕ Pros

- No Employment is Required. No proof of income or employment is needed to obtain this account.

- No Credit Check. You will not harm your credit if you apply for this card.

- High Credit Limit. A credit limit of $1,000 is high for this type of card.

- $25 in Reward Dollars each month.

➖ Cons

- $19.95 Monthly Fee. This means you’ll pay $239 each year just to own this card.

- Doesn’t report to credit bureaus. The card won’t help you build credit.

- Can Only Use it at MyUniqueOutlet.

Verdict

Even though Accepted Platinum offers better features and a higher credit limit than most other similar cards, the annual fee is simply too high.

BOOST Platinum Card

The best thing about BOOST Platinum Card is that you are guaranteed a credit limit of $750* dollars to use inside the Horizon Network.

This network doesn’t have as many product choices as Fingerhut. It also doesn’t have an APR for the items you purchase.

Don’t be fooled by the 0% APR: this is not a low-cost option. This card comes with about $177 in annual fees. It also won’t help you build credit, because it does not report to the credit bureaus.

Pros & Cons

This is one where there are more things we don’t like than we do like.

➕ Pros

- No Employment Required. No proof of income or employment is needed to obtain this account.

- No Credit Check. You will not harm your credit if you apply for this card.

➖ Cons

- $177 Annual Fee. Say no more.

- Doesn’t report to credit bureaus. The card won’t help you build credit.

- Can Only Use At Horizon. You can only use your credit limit at Horizon Network stores.

📞 Customer Service

BOOST Platinum Card has very bad customer service reviews on BBB and is a third-party card of the Horizon network.

Verdict

This product sounds great on the surface with a 0% APR, guaranteed approval, and a starting credit limit of $750.00*.

However, your annual fee is going to be over 20% of your actual credit limit. This is a prohibitive fee and we don’t recommend this unless it is your only option.

*Usable only at the HorizonOutlet.com

Are Online Store Credit Cards Worth It?

If you plan to improve your credit score or build credit for the first time then an online store card with guaranteed approval may be a valid option if the card issuer reports to the credit bureaus. It will provide you with a credit account and that can help you build credit.

While they do give you access to some everyday items you can purchase, shopping in these networks on a regular basis is not how these accounts should be used.

Your primary focus should be using them to establish a good payment history, get as many credit limit increases as possible, and help with your mix of credit. That means keeping your spending low, buying only items you need, and making all payments on time.

Remember that the providers offering these cards still need to make money. They often do this by overpricing the items they sell.

If online store cards don’t sound like a great deal – and they often aren’t – look into a secured credit card instead.

Eventually, you want to get to a point where you can have a strong enough credit score to get an unsecured credit card even if you still have bad credit.

💡 Once this account has served its purpose you should keep it active but not use it at all. If anything, use it once every 6 months to just keep it active.

Retail Store Credit Cards To Avoid

Have you ever been shopping at your favorite retail store and as you check out the cashier asks you if you’d like to apply for their retail store credit card?

It seems like every retail store has its very own credit card but should you get one?

The simple answer is, ‘No.’

Retail store credit cards can only be used to make purchases at company-owned stores or their online website. They usually charge extremely high interest rates and the rewards they offer to entice you to sign up have little to no value.

Most of the rewards programs offer automatic discount rewards when you hit certain points thresholds that expire within 30 to 45 days.

The largest issuer of retail store cards and administrator of valueless rewards programs is Comenity Bank.

This bank has horrible BBB reviews and ranks as one of the worst customer support services of all banks that we have reviewed. In fact, they are known for closing accounts in good standing that pay off their balance each month because they do not make enough interest off of them.

Taking Action

Building credit is a multi-step process. You’ll want to have revolving credit, like a credit card or an online store card, and also installment credit, like a credit-builder loan. An online store card can help you, but it might not be the best option.

If you’re trying to build credit, look into these strategies for rebuilding damaged credit and starting to build credit, and consider all of your options before making a choice.