This one’s a little different. Normally these reports focus on a single company. We’ve been watching the resurgence of interest in nuclear power for some time, and the confluence of climate change, soaring fossil fuel prices, and conflict-driven supply constraints in fossil fuel markets have driven that interest to higher levels. We didn’t see a single company that stood out, so instead, we’re presenting a review of the state of the nuclear industry and three possible investment options. We hope you find it interesting!

Table of contents:

1. Executive summary

A brief discussion of the nuclear industry and its potential appeal to value investors.

2. Extended summary

A more detailed explanation of the nuclear industry and possible investments in the sector.

3. Nuclear power history

The former and future rise of nuclear power.

4. Industry overview and new technologies

Who are the main actors, and how new techs will change the industry.

5. A selection of nuclear companies

3 different stocks to invest in nuclear.

5.1. BWX Technologies (BWXT)

5.2. NuScale (SMR)

5.3. Nuclearelectrica (SNN)

6. Conclusion

Why the nuclear industry is worth a closer look.

1. Executive Summary

For a long time, discussions about energy were focused on carbon emissions and global warming. With a brutal energy crisis engulfing the world, and especially the EU, it gets more evident by the day that reliable, cheap, and low-carbon energy is more needed than ever. This gives nuclear energy a chance to grow again and make outstanding profits.

In addition to this macro environment, new technologies are being developed. A new type of reactor is promising a modular, flexible and safer design. They will also be built quicker and with much smaller upfront costs, two of the main constraints on developing new nuclear power plants.

The entire industry is turning to this new technology. The companies featured in this report are at the forefront of this revolution in a long-stagnant industry:

- One is the most trusted supplier of nuclear reactors to the US military.

- One is the startup that first moved to make this technology a reality and is likely to be the first one to deploy it.

- And the last company is at first glance a simple, “boring” utility. But it will also be the first one in Europe to deploy this new technology and have an ambitious plan to double its nuclear power production in the next decade.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

2. Extended Summary: Why Invest in Nuclear?

Nuclear Power History

Nuclear power history is one of crisis. From a boom in response to the 70s energy crisis to crashes with Chernobyl and Fukushima. A new boom is likely, with the current European energy crisis unfolding. This might make the industry the new focus on an investing community that ignored it so far in, preferring renewables and green tech like EVs.

Industry Overview and New Technologies

The industry is roughly separated between manufacturers (making the reactors), utilities (operating the reactors) and uranium miners. New types of reactors are coming to the markets. The most interesting technology is SMR (Small Modular Reactor). It promises to alleviate most of the inconveniences of traditional nuclear reactors (size, upfront costs, safety profile).

A Selection of Nuclear Companies

This report covers 3 different companies: BWXT, a military nuclear reactor producer, NuScale, an ambitious startup looking to make SMR the standard template for the nuclear industry, and Nuclearelectrica, a European utility selling at an attractive price.

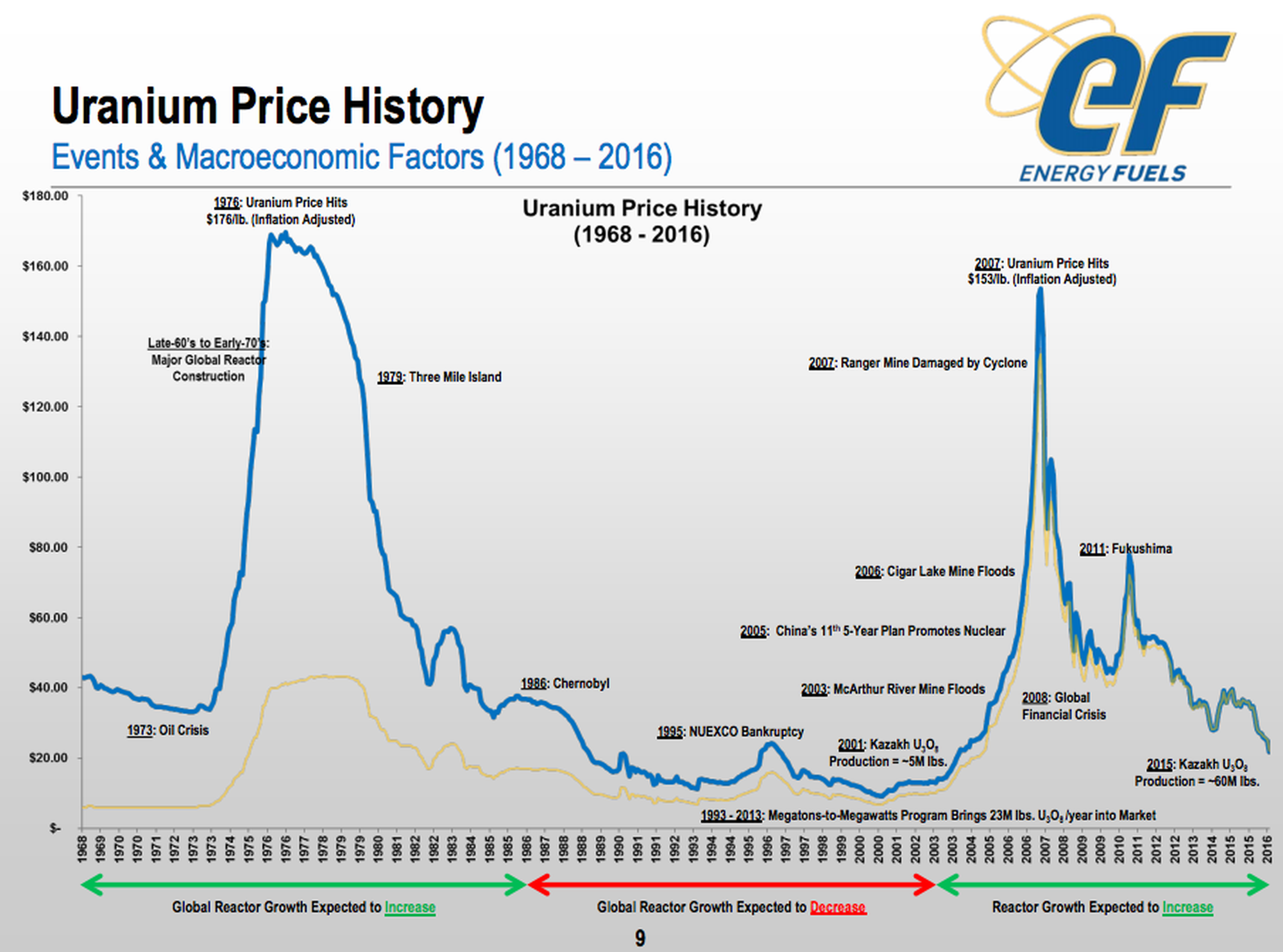

3. Nuclear Power History

A Controversial Past

Nuclear energy is a complicated topic. It triggers a lot of passions, fears, and hope. It is a very technical industry, with technology truly understood only by experts. It also carries a heavy emotional load, from its association with doomsday nuclear weapons to the trauma of the Chernobyl incident and its nuclear fallout all over Europe.

The idea of nuclear power was initially welcomed with overwhelming enthusiasm. You can read almost any novel by Isaac Asimov for an idea of the hopes put on nuclear energy as soon as the 30s. Literally, every vehicle or gizmo is nuclear-powered in the novels of the grandfather of science fiction.

When engineering caught up with science fiction, it triggered a massive build-up of nuclear power plants in the 60s and 70s, most notably in the USA, Russia, and France, but other developed economies as well. The 70s inflation and oil crisis (through the OPEC embargo) seemed to confirm the advantages of nuclear over geopolitically vulnerable fossil fuels.

The gradual realization of the dangers of radioactivity soon created a small, but very vocal opposition to nuclear power. Initially welcoming the alternative to coal mining and oil, ecologist activists and Green parties turned against nuclear and are still to this day massively opposed to the technology. The incident at Three Mile Island increased the fear of a serious nuclear incident one day.

But for the wider public, the turn of opinion was in 1986 when the Soviet Chernobyl nuclear reactor exploded. This dispersed highly radioactive compounds all over Europe. Suddenly, from cheap and safe, nuclear power plants acquired the image of a ticking time bomb. Four decades of fearing a post-apocalypse nuclear wasteland did not help either.

This led to essentially freezing of new projects, except in small parts of the world where local politics justified continued investment in nuclear, notably in France. During that period from 1986-2011, nuclear power was very slowly coming back in favor as fossil fuels became accused of putting the entire planet and its climate at risk. Wind and solar might one day be enough, but nuclear was perceived by many as a possible “transition” solution. And Chernobyl was now getting blamed on antiquated technology and Soviet corruption more than nuclear power as a whole.

In 2011, a historic earthquake and tsunami devastated Japan, notably the power plant of Fukushima. This immediately reawakened the fear of the Chernobyl incidents and led Japan to stop all nuclear power plants in the country. It put in motion a plan by Germany to phase out all nuclear power as well.

The Growing Energy Crisis

The world is currently short of fossil fuels. The crisis had been brewing for a while, due to a combination of factors :

- No discovery of mega oil & gas fields to replace aging resources like Saudi oil.

- Low oil prices in the 2010s due to short-lived, but abundant overproduction by US shale oil.

- ESG pressure to switch to renewables, cutting funding to oil & gas exploration.

- Political pressure to reduce carbon emissions as soon as possible.

- ESG and political pressure and low prices led to historically low capex in the energy industry.

This report will not try to pit renewables versus fossil fuels. We have covered before companies working in energy, from Brazilian hydropower Copel/ELP, fossil fuel Argentinian Pampa Energia and American Enterprise Partners, to American renewable Brookfield.

The fact is, for now, the sun and wind cannot fully replace fossil fuels. This is due to the intermittency of renewables, and simply the sheer gigantic and growing demand for energy in the world. But keeping fossil fuels is barely an alternative when global warming is judged an imminent and existential crisis. Alternatives like nuclear fusion of commercial geothermal are still decades away.

On top of this, geopolitics made a bad situation worse. The war in Ukraine is echoing the 70s oil embargo by Opec countries. Europe is now desperate to try to find enough energy for next winter. It is preparing for anything between blackouts to complete economic collapse.

I singled out Germany in the above headline because this is the EU country that has both the largest energy-intensive industries (heavy manufacturing, chemicals, etc…) and have been the most aggressively turning toward renewable.

This is also the country in Europe the most opposed to nuclear power. Look again at the recent headlines above. Despite this gloomy outlook, Germany shut down 3 of its 6 nuclear power plants in January 2022. And insist on stopping the last 3 by the end of the year.

Germany has maintained it will switch off its last three nuclear reactors by the end of the year despite a senior EU official urging the bloc’s biggest economy to rethink.

Source: MSN.com

Turning Tides for Nuclear

Even just 1 or 2 years ago, Germany’s plan to phase out nuclear was eventually criticized for being too quick, but that was it. But since the largest energy crisis in the history of the EU, the discussion has changed. The neighbors of Germany are trying their best to make them keep nuclear production.

The EU is not an organization known for its quick-acting or pragmatism. It is however able to realize when a problem is getting really too massive to ignore. As a clear sign of growing desperation, the EU has reclassified nuclear energy (and even gas) as “green” energy.

So far I mostly spoke of the EU because this is where the change is the most dramatic and the need the direst. For example, Poland is looking to acquire 4 to 6 last-generation reactors (EPR) from France. The same France that will build 14 additional reactors for itself, instead of mostly closing them like planned 1 year ago. The UK is now planning one new nuclear plant per year.

The rest of the world is doing the same, signaling a global turn of events not limited to Europe.

South Korea has restarted the construction of 2 new reactors. It is also South Korea that is producing the UAE’s first nuclear reactors.

Japan is also turning back to nuclear since Fukushima. 9 of the 39 reactors have already been restarted, and the rest is now expected to be restarted as soon as possible, notably because LNG prices are at a record high.

India is aiming to triple its nuclear capacity in the next 10 years.

But the elephant in the room is, like often, China. The latest energy plan of the country is to build no less than 150 nuclear reactors in the next 10 years. The decision was announced last November, and one can wonder if news of the incoming Ukrainian war did not precipitate this outsized renewed enthusiasm for nuclear power.

4. Industry Overview and New Technologies

Investing in the Nuclear Industry

The sector can be separated along the nuclear value chain, from fuel production to electricity generation.

Manufacturers

When it comes to nuclear technology, investors are offered a somewhat limited set of options. Many major actors are state-owned companies without public listing. Nuclear power plants use a lot of components supplied by major engineering companies, like Siemens for example, but often the nuclear segment is just a fraction of the company’s activities. Still, some companies are available, and one of the companies in this report is a manufacturer of nuclear reactors.

Utilities

Another way to invest in nuclear power is to invest in utilities producing power through nuclear plants. This will be especially true if the utility company is focused solely on nuclear power plants. One of the companies analyzed in this report fit this mold.

Uranium

The last option is to bet on the fuel used by the power plants to rise in price. #Uranium has been a trendy topic on FinTwit (financial Twitter) these last months, but I stay relatively unconvinced. The argument is based on the rising popularity of nuclear. With uranium fuel just 1-3% of total costs, utility companies are not really price-sensitive when it comes to uranium.

Of course, if a lot more reactors are built, demand will grow. But supply is also likely to catch up. And as a reactor can take 10 years or more to be built, the demand will rise at a steady, but slow pace, possibly several years in the future. In addition, uranium is barely traded on the spot market like other commodities. Instead, long-term contracts and stockpiles mean this is a very hard-to-trade market.

The sector is dominated by 2 companies, Kazatoprom and Cameco.

The first one operates in central Asia and carries a very significant geopolitical risk. It is cheap, but it ties to Russia and arguably justifies it.

The second one is in Canada but has historically struggled with profitability and with delivering good returns for its shareholders. Other miners are much smaller, with plenty of junior exploration companies hoping to join the boat of the nuclear renaissance.

The last option for uranium investing in the Sprott Physical Uranium Trust. It is a trust holding its asset in the form of uranium fuel. The idea of the Trust is to stockpile uranium until the price is right, then sell and distribute the profit to its investors. It might work, but this is mostly for speculation more than investment purposes.

For all these reasons, this is why this report does NOT include uranium itself as a possible way to invest in the comeback of nuclear energy.

Nuclear Innovation

Another possible investing strategy is to bet on innovation. Already, the new EPR (Pressurized water technology) and other Generation III+ reactors are miles ahead in terms of efficiency and safety compared to older designs like the one at Fukushima.

Out of the public gaze, a new generation of engineers have looked at “classic” nuclear power plant designs and have found them lacking. Flaws of classical nuclear power plants are:

- Every new reactor is designed from scratch.

- Large construction projects are plagued by delays and over costs.

- Uranium is not the ideal fuel and other materials could be used as fuel.

- Smaller designs are inherently safer.

Thorium Reactors and Other Designs

I will no go into the technical detail, but the short version is that uranium is not really the optimal fuel for nuclear power generation. The reason it came to dominate the industry is that it was useful to the military nuclear industry. While in the Cold War, this was viewed as a pro, this is very much a downside nowadays.

An alternative is thorium, another radioactive element. You can check here a more detailed discussion about thorium advantages, which include less nuclear waste, inherently safer reactors (no meltdown possible, as the reactor, cool down spontaneously), abundant resources, and no risk of using its byproduct for nuclear weapons.

Early design goes back to the 1960s. China is the current leader in the field, notably building waterless thorium designs that can be used in deserts with a high safety profile.

Other Designs

Over the decades-long history of nuclear power, many other designs have been tested. One with a lot of potential is fast breeder reactors. Their main advantage is the much more complete use of nuclear fuels. This means it could use the nuclear waste of traditional plants.

Unfortunately, most of those are decommissioned old designs, prototypes, or done by public companies that cannot be invested in. This design nevertheless solves in large part the problem of nuclear waste, so I thought it was worth mentioning it.

Small Modular Reactors (SMR)

This is the most interesting innovation in the nuclear industry in decades. The idea of SMR is to miniaturize a reactor down to the size where it can be transported by a truck in a freighting container.

This gives SMRs multiple advantages:

- Modularity: if you need more energy, just add more reactors.

- Higher safety: due to size and design choice, SMRs are almost always self-cooling. An accident like Fukushima or Chernobyl is impossible with SMRs.

- Production at scale: Thanks to their size and standardization, SMRs can be produced in the same way we make a truck or a car: in an assembly line, with mass-produced components assembled hundreds of times in a row. No more engineering headaches from reinventing the wheel at every new reactor building site with its own design.

- Decentralization: a few SMRs can be used to power operations in remote areas or energy-hungry industries. This might power charge (pun intended) the electrification of mining operations and heavy industry.

While thorium or fast breeder might have a space in the industry, SMRs are widely viewed as the future of the industry.

Poland, eager to get a safer energy supply and independence from Russia, is leading the charge, notably with KGHM (a copper producer) and Orlen (an energy and fuel producer).

5. A Selection of Nuclear Companies

Now that we are done with the explanations, let’s start with the actual investing.

I hope this was not too lengthy, but at the same time, I felt it was needed to give enough context to explain:

- Why nuclear power is attractive again, now that the political and macro-economics winds have turned.

- What sectors in the industry are the best opportunities.

We will look at 3 companies I feel offer a wide enough pannel of opportunity and investment profiles:

The first company is BWX Technology, a nuclear reactor producer. The company is deeply intertwined with the military reactors industry in the USA. In addition to its military and civilian activities, it is also developing its own SMR.

The second company is NuScale, a widely ambitious startup solely focused on SMRs. There are actually many other such startups, but few are as advanced as NuScale or publicly traded.

The last company is Nuclearelectrica. This is the utility in charge of nuclear power generation in Romania, trading at an attractive valuation and with a generous dividend yield.

Together, these companies offer the possibility of investing in nuclear for any portfolio and investment strategy. BWXT is a more established and “safe” company, NuScale a bet on growth and innovation with large potential, and Nuclearelectrica a steady, “boring” dividend/income stock.

5.1. BWX Technologies (BWXT)

Quick Stock Overview

Ticker: BWXT

Source: Yahoo Finance

Key Data

| Industry | Nuclear/Defense |

| Market Capitalization ($M) | 1,041 |

| Price to sales | 3.4 |

| Price to Free Cash Flow | 100 |

| Dividend yield | 1.6% |

| Sales ($M) | 2,127 |

| Free cash flow/share | $4.23 |

| Equity per share | $7.24 |

| P/E | 17.5 |

BWTX is a well-established actor in the nuclear industry, with 6,700 employees and 14 sites in North America.

The company is largely focused on nuclear power for the government. This includes military nuclear reactors to power ships like submarines and aircraft carriers. So this is as much a defense stock as a nuclear one. Notably, BWXT is the only actor besides the government with authorization to manipulate highly enriched uranium (20%+, potentially usable for nuclear weapons).

The main attraction of the company is the quality of its investing moat. The firm is fully aware of it and has even a neat diagram synthesizing all of their advantage making the company a very “moaty” high-quality business:

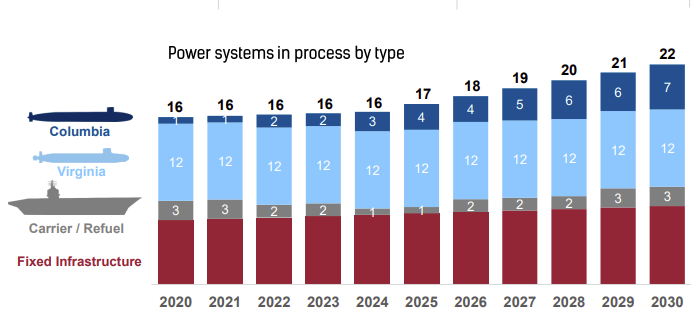

The Military Opportunity

Jobs for the military offer extraordinarily high visibility to BMXT on future cash flow. This is the first time I see a company offering in its presentation the upcoming maintenance and upgrade contracts up to 2052; notably for Ford-class aircraft carriers and Virginia and Columbia class submarines. This is a steady source of business, as the US navy is planning to grow from 293 ships to 335.

BWXT is developing its own range of SMR and micronuclear (even smaller scale than SMRs) technology. Its connection with the US government gives it a unique position to land contracts with NASA or the military (Including the Space Force).

Off-grid supply of energy to military facilities has been a long-time logistical headache for the military. BWXT will be offering solutions to alleviate the costly and military vulnerable supply chain of fuel and gas to military bases. This is also in line with the goal to slowly go fully electric for military vehicles in the next decade.

Considering the high reputation of BWXT and its connexion to the Pentagon, I think it likely will be one of the big winners of the army electrification program. In a time of renewed geopolitical tensions and military spending, this is a good business to be in.

Civilian Activities

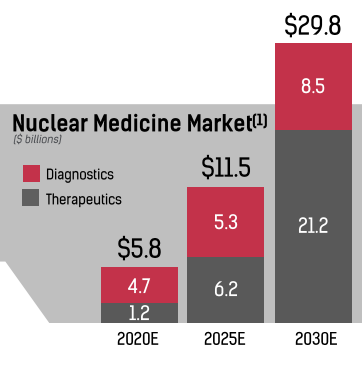

The company is also active in nuclear medicine (radiotherapy). They have stricken deals with some of the industry-leading actors, like Bayer, to provide them with the nuclear component and reactors for treatments. This market is expected to grow quickly, and BWXT is aiming to grow its current revenues from $50M to $200M+ by 2025. This would turn the current $5-10M losses of this segment to $75M EBITDA.

It is also providing services and fuel to nuclear power plants, for example in the last year contracts worth CA$130M with Bruce Power and $50M for Ontario Power.

SMR Technology & Space Tech

The company’s SMR effort will rely on the BWXT Advanced Nuclear Reactor (BANR) design. It provides everything an SMR should: modularity, higher safety, etc… What seems unique to BWXT design is a unique high-density fuel, allowing for refueling only every 5 years versus 2 years on average in the industry. Such low maintenance design seems already geared up toward military needs. An initial test of a microreactor will already be delivered by 2024, in a $300M project called Project Pele.

I also think that the possibility to build the SMRs in pre-existing and accredited facilities (with both defense and nuclear accreditation at the same time) will be a huge industrial advantage over its competitors. The existing base of expertise and manpower is also great to have in an industry that chronically trains too few people.

In addition to terrestrial SMR, BWXT is also developing space-based reactors. One application can be the local power supply for future Moon and Mars missions. Another one is space propulsion.

These technologies will probably be needed to reach reliably Mars, and with a new space race between the US and Russia+China heating up, this might be as well a growth sector for BWXT in the long term.

Financials & Valuation

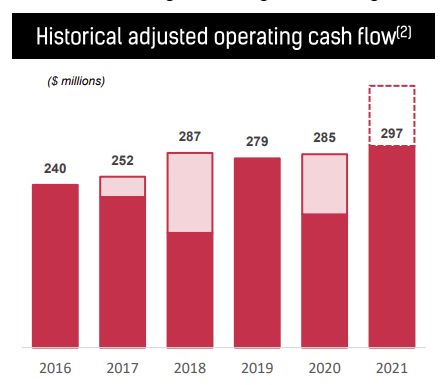

At a P/E of 17, BWXT does not seems overvalued at the moment. Operating cash flow is steady and rising over time.

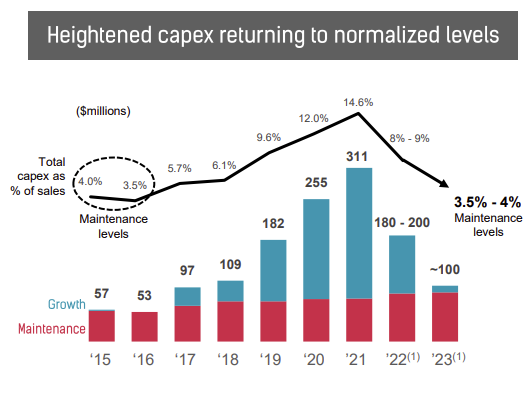

The company also has a policy of returning at least 50% of Free Cash Flow to shareholders through dividends and buybacks. FCF should improve in the years going forward, with capex spending going back down after a period of massive investment in growth in the last years.

Conclusion

BWXT is a way to play the nuclear comeback safely. It might not experience the most explosive growth or be at the cheapest valuation. But it has one of the best moats I have seen, with regulation, strong connection to the military, highly complex technology, unique intellectual property, certified production facilities, and human resources.

The company is not just relying on its moat, but aggressively using it to expand in new markets, like space-based energy, nuclear medicine, and last but not least, SMRs.

This makes for a buy-and-hold type of stock, where the company will slowly (over the next 2 decades) expand its activity from providing nuclear power to capital ships to the entirety of the $773 Billion annual budget US military machine.

5.2. NuScale (SMR)

A Careful, Slow Strategy for Outsized Ambitions

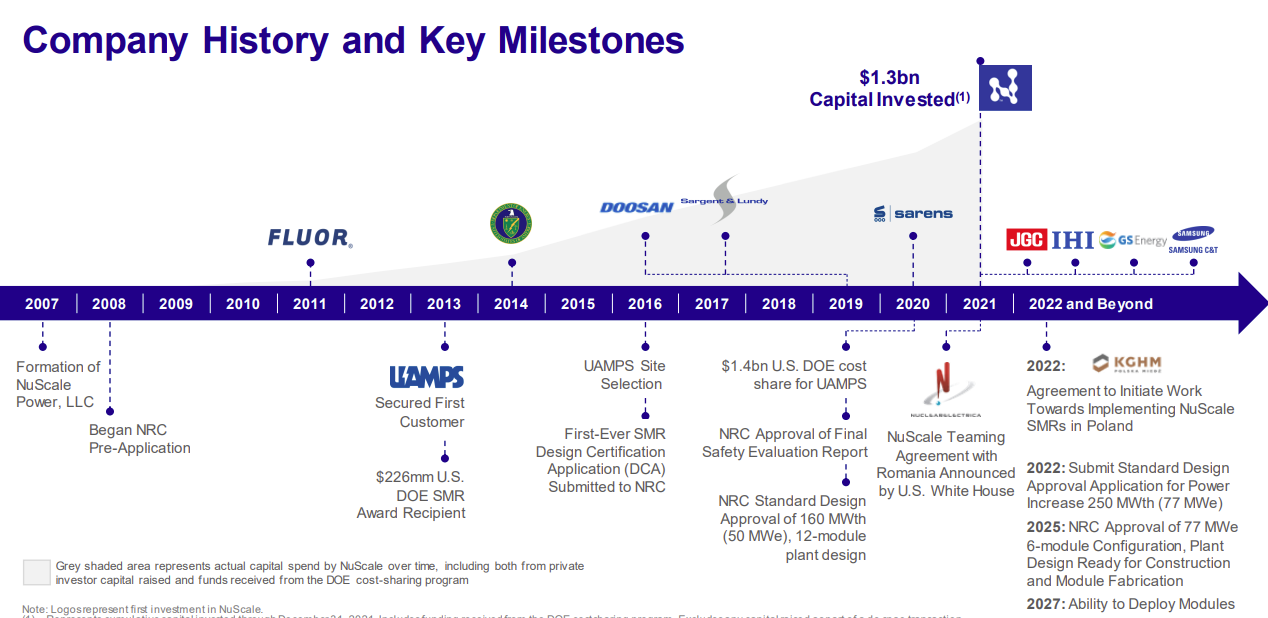

Where BWXT is the established, well-connected giant, NuScale is the ambitious upstart looking to take over the world. This ambition goes way back to 2008 when NuScale started its design and application with the US Nuclear Regulatory Commission (NRC).

The company is the only one to have received NRC standard design approval, a big deal for a newcomer in a very tightly regulated industry. It is also providing extra protection for the company and reassurance for its clients:

We started off as a new company in 2007. We started our engagement with the NRC in what was called a pre-application in 2008. We submitted an application that required 800 people working on it, 12,000 pages long, $500 million to put together. The NRC spent 200,000 hours reviewing it, asking a bunch of questions. We spent $200 million answering those questions.

(…) You still need to do all that engineering and things, because ultimately, the compact we’ve made is that we have liability protection because we’re regulated.

Chris Colbert, Chief Strategy Officer at Nuscale, Energy Power and Renewable Conference

So while NuScale is making headlines now, this was built over 14 years of preparations. A slightly amusing proof of this first mover advantage is in the ticker of the company’s stock, SMR.

Quick Stock Overview

Ticker: SMR

Source: Yahoo Finance

Key Data

| Industry | Nuclear |

| Market Capitalization ($M) | 1,041 |

| Price to sales | 3.4 |

| Price to Free Cash Flow | 100 |

| Dividend yield | 1.6% |

| Sales ($M) | 2,127 |

| Free cash flow/share | $4.23 |

| Equity per share | $7.24 |

| P/E | 17.5 |

The Backers

When judging ultra-technical projects like nuclear reactors, I think it is pointless to try to judge the technology except if you are an expert yourself with 20 years of experience. Instead, I prefer to rely on the actions of actual experts in the field.

Over its history, NuScale has been backed by reputable firms, like the engineering giant Fluor, Korean conglomerates Doosan and Samsung, as well the Department of Energy (DOE) which awarded $1.4B to NuScale for testing a 12 SMRs power plant in Idaho.

At this point, I think it fair to describe NuScale as firmly backed by the US government, and that was true through both Republican and Democrat administrations. So political risk seems rather low. If anything, NuScale is now a valuable US government asset and will be supported as such.

The Technology

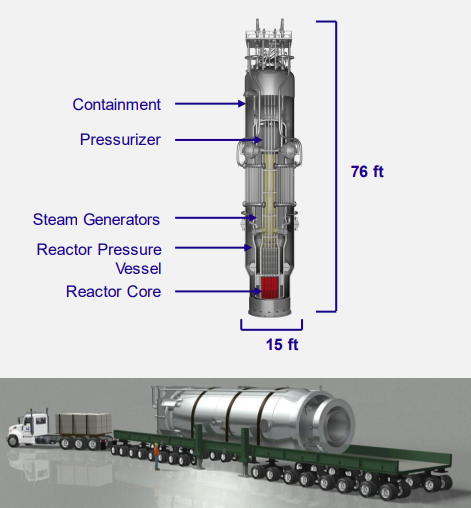

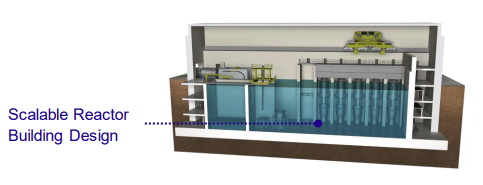

NuScale basic unit reactor is large, but still small enough to be assembled in a factory and transported by truck. The reactors (in batches of 4, 6, or 12 reactors) are then assembled together into a full power plant.

One of the key advantages of the design is that the reactors can restart even if the grid is down, something traditional nuclear power plants are unable to do. So having NuScale reactors plugged into the grid actually makes it a lot more resilient.

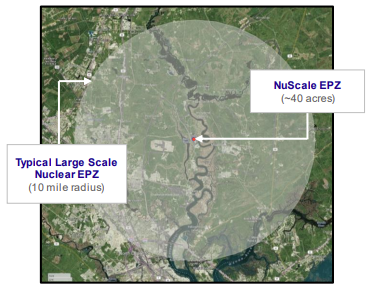

Another strong advantage is the Emergency Planning Zone. SMR technology’s inherently higher safety allows for a very small exclusion zone compared to traditional nuclear. This means NuScale reactors can be installed on site of existing or decommissioned coal-powered plants or other industrial facilities, reducing drastically the regulatory burden. It also then reuses existing power transmission, which can often be harder to get approved than a power plant.

Besides power generation, SMRs like Nuscale’s can be used for direct heat generation. As a rule of thumb, only 20-30% of the heat generated can be converted to electricity. So when heat is directly needed, it is better to not use electricity from it but directly from the power plant heat itself. For example, a 4-reactors NuScale power plant can provide enough heat for the desalinization of water to supply the entire city of Cape Town in South Africa.

NuScale is also developing and integrating a lot of technology besides the reactors themselves, from cyber-resistant control systems to a dedicated delivery system.

One even more interesting idea is a “marine-deployed” (aka: on a ship) power plant, together with Prodigy Clean Energy. Such sea-based power plants have already been proven viable by Russian Rosatom, but this is something that could be deployed to provide clean and carbon-free power to arctic regions, island nations, and coastlines all over the world (coastline harbor 80% of the world population). The combination of a ship-based nuclear power plant and SMR modular design seems a great match to me.

A Growing Pipeline of Projects

As a sign of official support, The US government has been supportive all the way for NuScale to land a first contract with the Romanian utility company Nuclearelectrica (the third company analyzed below in this report). Starting from a USTDA grant for finding a site, followed by paying for a simulator to train Romanian operators.

This culminated in the agreement for a 462MW power plant, to be fully operating by 2028. While this might seems far in the future, this is actually lightning speed in an industry usually needing 10-20 years from signing a project and having it running.

With its technology validated by the US government and a major national nuclear utility, NuScale is going at full speed to secure as many new projects as possible. Here are a few selected projects:

- Polish KGHM copper producer for its factories, smelters, and mines.

- Polish Unimot energy company to replace coal power plants.

- Carbon Free Power Project in Idaho Falls, Idaho, USA.

- Associated Electric Cooperative Inc., Missouri, USA.

- Ontario Power Generation Inc., Canada

- Bruce Power L.P, Canada.

- Ukrainian Energoatom is looking into SMR in its plans to rebuild once the war is over.

- Kazakhstan’s KNPP is interested in deploying SMRs.

- Bulgaria’s KNPP-NB (same acronym, different company) to add to its existing nuclear power plants.

- Jordan’s JAEC, looking to reach 30% nuclear for its electricity by 2030.

Financials & Valuation

NuScale is still essentially a pre-revenue startup, so usual metrics like cash flow or earnings are pretty irrelevant. While I dislike Total Addressable Market (TAM) as a metric, this is maybe one case where it makes sense. The strong interest by not only utilities but industrial companies like KGHM seems to make the TAM of SMRs a lot larger than for traditional large nuclear power plants.

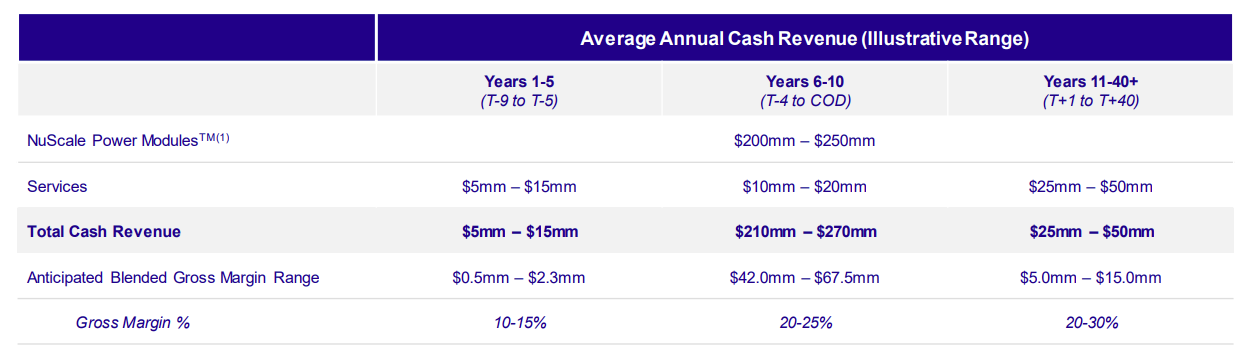

NuScale gives us the per plant economics of the business. The bulk of the money is made in years 6-10, with the sale of the module themselves, at $200M-$250M of average yearly revenue. The gross margin should be for the lifetime of a project around $250M million by year 10, and then a regular $5M-$15M/ year for the next 30+ years.

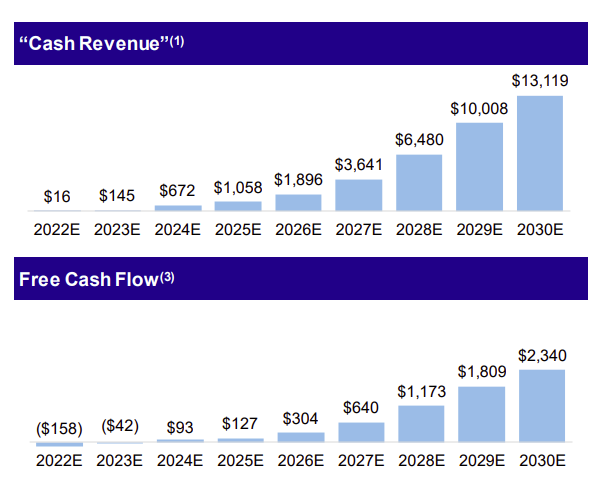

The company is projecting to become cash flow positive by 2024, with real significant cash flow by 2027. Considering the Romanian and Idaho projects already signed, with Polish projects well ahead, and many others in the pipeline, I do not think this is unrealistic.

The good news is that through its listing via a SPAC, NuScale has a stash of $425M in cash. The company management estimate this should be enough to reach the point where it will generate free cash flow. NuScale has very little capex needs, design costs are already done and it will be paid for its reactors before they are built. So this seems reasonable to me as well.

I think more projects or existing negotiations speeding up is also a real possibility. We are just at the beginning of the current energy crisis, and it is not accidental that Romanian and Polish clients are the first ones looking to get SMRs as soon as possible. I fully expect the rest of Europe to realize the need to switch away from unreliable Russian gas or very expensive LNG.

At this time last year, they were looking for a 2034 plant. In November, they said they wanted it in KGHM, we started working with in September last year, and then in February, they announced that, “We’re going to early works agreement to start selecting sites and looking at what this looks like in the Poland context.”

Chris Colbert, Chief Strategy Officer at Nuscale, Energy Power and Renewable Conference

Competition

This is maybe the most difficult part to assess. The sector of SMR is booming, but so is competitive pressure. At the moment, NuScale seems to have a first mover advantage. But many industrial giants are in its footsteps and might ultimately win through economy of scale and connections with governments, industrial clients, and utilities. This makes NuScale an inherently speculative investment, with the typical high-risk, high-reward profile of a growth startup.

Among competitors for NuScale are:

Large corporations

- BWXT (see above)

- Roll Royce (UK)

- GE-Hitachi (Japan – USA)

- EDF (France)

- CNCC (China)

- Westinghouse (USA)

Startups

- TerraPower (USA)

- X-Energy (Canada)

- Fermi Energia (Estonia)

This should not be an issue for NuScale in the sense that it will likely be able to grab a quite large section of the market anyway. In addition, its water-pressurized reactors are a proven technology. More innovative but untested molten salt or other methods might manage to succeed as well in due time but will face the very conservative streak of a nuclear industry always dreading a new Fukushima.

Conclusion

Now a 15-year-old “startup”, NuScale is ready to scale up and really enter the market. The energy crisis and the renewed interest in nuclear will only speed up its growth.

Its focus and spending to get the highest level of validation by US nuclear authorities will give it an edge in staying ahead of its competition, including large corporations. It will also be promoted by the US government as a way to support its allies in Europe and the Middle East. The partial ownership from Japanese banks and Korean conglomerates will help open doors in the Asian markets as well.

At the current valuation of $446M, NuScale is still a micro-cap yet to rise. IF the free cash flow projection from NuScale management is accurate, this is a bargain. But of course, any success investing in the company will need it to turn profitable, something still to be done.

This whole report is based on the assumption that nuclear energy will become a new focal point of the investing world in the next year when energy prices and shortages are becoming a major concern.

If this turns out to be true, NuScale stock could rise quickly.

If not, it will be a much slower potential, depending on continued progress until the 2027-2028 mark when the company turns on its first power stations in Romania.

The involved Romanian company, Nuclearelectrica, is the next and last one we will look at.

5.3. Nuclearelectrica (SNN)

This report is already quite long, but luckily, the last company is also the simplest to analyze.

In its current form, Nucleaelectrica is a classic utility company. It produces power, sells it in its home market, and makes a profit from the difference between its costs and its selling price.

As discussed in previous reports, utilities are very predictable companies. So the main points should be:

- A history of good maintenance and management of the assets.

- An ability to control input costs.

- A good market price for the stock.

- A policy friendly to shareholders with large dividends distributions.

Quick Stock Overview

Ticker: SNN

(quotation in Romanian Lei / RON)

Source: NuclearElectrica

Key Data

| Industry | Nuclear |

| Market Capitalization ($M) | 2,704 |

| Price to sales | 2.12 |

| Price to Free Cash Flow | 10.6 |

| Dividend yield | 10.7% |

| Sales ($M) | 1,273 |

| Free cash flow/share | $0.84 |

| P/E | 5.14 |

| Share price in $ | $8.96 |

SNN is a public company, owned at 82.5% by the Romanian state, and with 17.5% trading publicly on the Bucharest Stock Exchange.

It operates 2 reactors, Unit 1 and Unit 2. They are each producing 650 MW and are responsible for producing 19% of total Romanian electricity.

It is also investing in the construction of Units 3 and 4 to expand production, both rated at 720 MW. These new units would bring nuclear to 36% of the country’s electricity production. They should be connected to the grid in 2030 and 2031 respectively.

As discussed in the NuScale chapter, it is also working on adding SMRs to its mix, making it the first European site for SMRs. The project is for 462 MW of power. SNN’s CEO is aiming for the company to become “a regional trendsetter in nuclear energy”.

Company Quality

Since its launch, SNN reactors have operated with a 91.6% capacity factor, making them the number 1 in the world by that metric. The company never had a nuclear accident and has a good safety record.

Between 2026 and 2028, Unit 1 will be refurbished, giving it another 20-30 years of operational life. This should cost around 40% of the costs of a new reactor. Unit 2 will need to be refurbished in 2037.

Contrary to fossil fuel power plants, nuclear station costs are all upfront. So the company has very good control over its input costs.

Overall, SNN seems like a quality utility with a large potential to benefit from rising power prices as its costs should stay relatively stable. It is also going to quickly grow its production from the current 1.3 GW to up to 3.2 GW by 2031.

Valuation

Besides its relative quality and stability, the main attraction of SNN is its price.

The company’s shares are trading at a low P/E of 5.25 and have a dividend yield of 10.5%. Price to Free Cash Flow is 11.5

The company’s policy is to distribute between 50% and 100% of net income. Once taken into account skyrocketing electricity prices in Europe, and future production growth, SNN valuation seems rather attractive. The fact that the company produces carbon-free power is also an advantage in the EU, which taxes carbon heavily.

Conclusion

SNN’s current valuation is relatively low, despite having gone up 10x since its listing 10 years ago. This is most likely due to its listing exclusively in Romania, far from the attention of most investors.

This makes SNN a company similar to Copel, a Brazilian utility we covered in a previous report. Both have low costs and stable “fuel” input (uranium for SNN, water from the Amazon rivers for Copel) in a rising price environment. Both have a friendly policy for shareholders and generous dividends. And both are ignored as they operate in smaller, oversea stock markets. For reference, Copel was trading at $5.29 when we published the report and is now trading at $6.23 while distributing a generous 15% dividend yield in the meantime.

SNN has a shareholder-friendly policy and an excellent safety record (considering prejudice against Eastern Europe nuclear power plants, it might come as a surprise).

Its assets are ultra-durable and will produce power far in the 2030s. With reduced capex spending, they can keep producing up to the 2060s. Combined with stable input costs this makes SNN a very conservative, buy-and-hold type of asset.

On top of this “safe” profile, the company will grow its income significantly in the next decade, more than doubling its production. In the case power price do not revert fully to the pre-war levels, earnings are likely to stay quite high as well.

If you liked this report, there’s more where this came from! We publish reports like this one every month over at Stock Spotlight.

Subscribe for free and join over 9,000 rational investors!

6. Conclusion

The energy transition is usually framed as fossil fuel versus renewables. Nuclear energy is the alternative to both that have long been ignored in this discussion. Its importance in the energy mix has been brought back to the front light by the stubborn decision of Germany to phase out nuclear no matter what. This made an already bad European energy crisis more acute, and reduce the continent’s ability to reduce its dependency on Russia.

The industry might never fully recover in terms of public image from the Chernobyl and Fukushima disasters. Nevertheless, new innovations like SMRs, and maybe thorium and other fuels, are radically changing the real risk profile of nuclear. By moving away from massive uranium plants to smaller, more flexible designs, SMRs also increase dramatically the range of applications nuclear energy can be used for.

To properly invest in and profit from this nuclear renaissance, we need to focus on companies for which nuclear is the core business and not just one small division in a large corporation.

If you think public acceptance of nuclear is still too low, or SMR an unsure bet, BWTX is probably a better choice. Its bread and butter still come from producing and servicing nuclear reactors for the US navy. With rising geopolitical tensions with China, this seems like a safe enough sector to put money in.

Any profit from BWTX’s SMR design and its deployment in the US military would just be the cherry on the cake. It is however likely to happen in some capacity. The push for electrification in the US military is there to stay, and will not be dependent on public opinion.

If you think civilian utilities are in dire need of more low-carbon, reliable power supplies, NuScale is where you want to invest. The startup has a higher risk profile but should be cash flow positive in a few years. Its first-mover advantage, certifications, and proven technology make it a likely winner in the race to SMRs widespread commercialization.

If you think the energy crisis in Europe is a golden opportunity for low-carbon, high-volume producers of power, you will prefer Nuclearelectrica/SNN. The company is trading at an attractive price and gives generous dividends. Contrary to other European nuclear producers, it is safe from political interference and has strong support to double its production in the next decade.

As the first one to implement NuScale’s reactor and the first utility to use an SMR in Europe, it will also be on top of nuclear news, which might prove a catalyst for repricing.

Together, these 3 companies can be combined to make an interesting mix to hedge risks in a portfolio when it comes to investing in nuclear. SNN provides dividend income with some slow growth, NuScale explosive growth potential, and BWXT the steady safety of a major supplier to the US military.

Of course, all of these are exposed to another nuclear crisis like Fukushima striking out of the blue. This would destroy confidence in nuclear once again, and trigger a crisis for the entire sector. So while a company risk profile might seem low, the overall sector risk should not be ignored.

Overall, nuclear investments should be part of a balanced portfolio and play the role of a bet on growth and an inflation edge at the same time.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in BWXT, SMR or SNN or plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation from, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.