September 30th, 2021

Quick Stock Overview

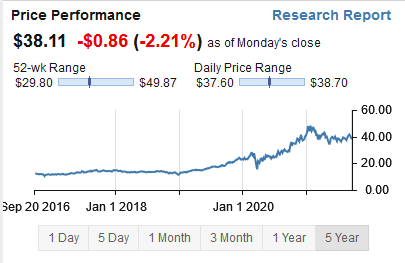

Ticker: BEP

Source: www.tikr.com

Key Data

- Sector: Utility

- Sales ($M): 3,888

- Industry: Independent power producer

- Net Cash per share: $-66.86

- Market Capitalization ($M): 11,138

- Equity per share: $16.28

- Price to sales: 2.9

- P/E: –44.6

Investment Thesis

Long Term Energy Future

In my previous report, I explained how I think that fossil fuels, especially gas, will still play a large role in the energy mix for the 1-2 decades to come. But this does not mean I am opposed to renewable energies, quite to the contrary.

I think that a realistic scenario for the energy transition is something like this:

- Removal of coal power plants in the next 5-10 years, replaced by a mix of gas and renewables.

- In the years that follow, an increase in renewable and gas power generation, to handle the increased consumption for electric transportation.

- Phasing out of fossil fuels in the 2040s and 2050s.

I would love for it to happen quicker. I really do. But considering how long-lasting are assets like power plants, cargo boats, trucks, and so on, I doubt we will see the electrification of everything before the late 2030s, or even later.

For more insights on the topic, I will refer you again to Lyn Alden’s great report.

You will notice that in the forecast above, all time periods imply growth in renewable production. First to replace part of the coal power, and then to help with the electrification process, and finally to remove fossil fuels from the mix. So, while there will be space for gas and petrochemical focus companies like Enterprise Product Partners, there will also be plenty of opportunities for renewable energy companies.

The topic has become so political that it has become hard to discuss it rationally. But ultimately, it is likely the story for investors will not be a gas versus renewables, but a gas and renewables. And I imagine also carbon capture technology like in Iceland to mitigate the slower than hoped-for pace of electrification.

The Right Kind of Renewable

Renewables is a blanket term covering a lot of different technologies and companies. So, when I started to look deeper on the topic, I realized what should be the profile of a “good” renewable company for value investors:

- A large part of the current production is from hydropower, as it is often the cheapest production with also a large moat. It is also more reliable power generation than the other renewables and can be used for energy storage.

- Demonstrated capabilities in solar and wind to be able to benefit from this technology becoming cheaper every year. And presence in both solar and wind to not be dependent on which of the two technologies dominate the field.

- A clear path for growth to respond to the need for more electricity production.

- Good access to capital and solid financial backers is possible.

- A large enough company to spread out the costs of regulatory compliance and overhead, as all renewable production needs a lot of land (or disruption of waterways for hydropower).

It took a while, but I found a company that fit the bill for all the points above, Brookfield Renewable Partners.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A Company Hard to Analyze

Part of a Giant

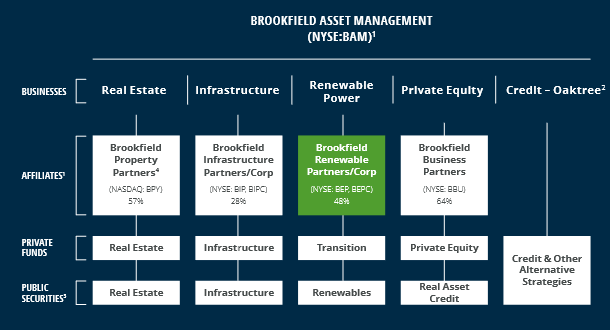

At first, I almost gave up on analyzing Brookfield Renewable Partners (I will refer to it as BEP from now on). This is because the company is a part of the larger Brookfield Asset Management company.

The company is a corporate monster, a conglomerate managing no less than $625B worth of assets. Typically, the kind of company is so complex that you would need to devote a few months of work to understand it. And it would have made this report some hundreds of pages long.

You have all kinds of things into this conglomerate:

- BEP, the renewable energy segment, also listed as BEPC in Canada.

- BIP, managing infrastructure like fossil fuel midstream, water, data cables, etc.

- Wealth management in the form of Howard Marks’ enormous Oaktree company.

- But also, insurance, corporate services, public funds, private funds, real estate funds, etc.

Source: https://www.brookfield.com/

Luckily, some individual parts of Brookfield can be invested separately. This is the case for BEP, and this is what we will be dealing with in the rest of the report. So, if you are looking for information on BEP, stick to the dedicated websitehttps://bep.brookfield.com/, and do not panic or get lost in the larger Brookfield entity that owns a large part of BEP.

So why did I mention it at all? Because it shows us two things.

First, BEP’s assets are held by one of the largest and best-established wealth management firms in the USA. If they are not selling BEP, they must have their reasons. A firm like BAM does not reach $625B in assets by being bad at capital allocation.

Secondly, it means that BEP has access to a lot of capital and connections from the larger Brookfield entity. It does not matter if it is in the form of getting access to capital, human resources, or connection to the right person in government, BEP is not just an energy company. Same thing when BEP needs to market its shares or bonds to investment funds, the rest of the group already has the perfect ESG funds ready for it.

This is a moat almost impossible to replicate but by a handful of similar conglomerates.

Financials All Over the Place

The second time I almost got discouraged in digging deeper about BEP was with its financials. On one side you have a profile of a steady compounder: growing revenue, market cap, and free cash flow.

On the other side, net income is barely staying positive, and the P/E ratio is so absurdly all over the place from, -285 to 149 that it is meaningless. You might even have noticed the negative P/E in the key data at the beginning of the report, or that I only showed price to sales, not to earning or cash flow.

So, is the company growing steadily, or tethering at the edge of collapse?

I looked for a bit longer, and I found that for a company like BEP, earnings, net income, cash flow or P/E are indeed meaningless. And this for two reasons.

The first reason is that the company is spending a lot of capex for growth, but in bursts through acquisitions or the launch of large infrastructure projects, like large offshore windmill power plants, for example. This strategy creates a very irregular cash flow and earnings.

The second reason is that all BEP’s assets are very long-lasting. Hydropower dams last more than a century and renewable power plants last decades. It allows the company to essentially hand-pick the depreciation rate that will allow it to report no net income and optimize its taxes that way.

You might approve or not the practice, but this needs to be understood when looking at the financials. The almost non-existing earnings are not a measure of profitability, but clever accounting and a good CFO.

I will come back to the depreciation charges in the financial section, but this needed to be explained first.

Is It Even Worth Looking at Then?

I think it is. In the end, the only number that matters, in the long run, is free cash flow. Cash flows that need to be re-injected constantly in the business will never make it to the pocket of the shareholders. Free cash flow does.

And when it comes to free cash flow, BEP has been able to steadily grow it at the rhythm of 13% annually. A remarkable number for a utility, usually considered as boring non- or slow-growing companies.

But before I bore you with even more numbers, let’s look at BEP’s business.

Chapter 2: A Leader in The Energy Transition

The Hydropower Base

In my initial checklist, I mentioned I wanted a utility that had a large part of its business in hydropower. Why? Because hydropower dams are one of the most durable and lasting assets a company can own, with the exception maybe of the land itself. Once built, a dam will last almost forever, at least if it is properly managed.

Thanks to the energy being provided by rainfall, it is the only major electricity source this day that is truly carbon neutral. Some might argue that the building of the dam is emitting some carbon, but the quantity is negligible compared to other energy sources and on par with the carbon emissions to produce windmills and solar panels.

Therefore, I fully expect hydropower to be increasingly profitable in the future, thanks to carbon credits/carbon taxes.

Finally, the best part of hydropower for me is that it is a perfect inflation hedge. The production costs are in the past, often decades ago. Operating costs are limited, and it requires no input fuel.

Electricity prices tend to be linked in a way or another to inflation. This is not true for all utilities, but 90% of BEP power generation is contracted with an “average power purchase agreement” or PPA, that protected it against inflation risks.

This PPA is akin to a quasi-perpetual bond, and a perpetual inflation-linked bond at that.

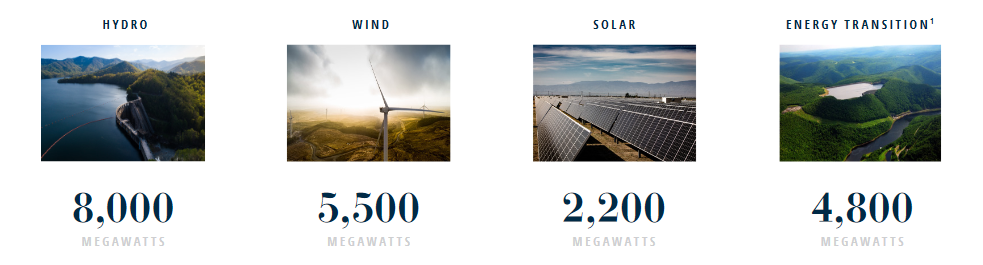

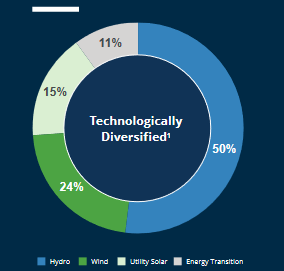

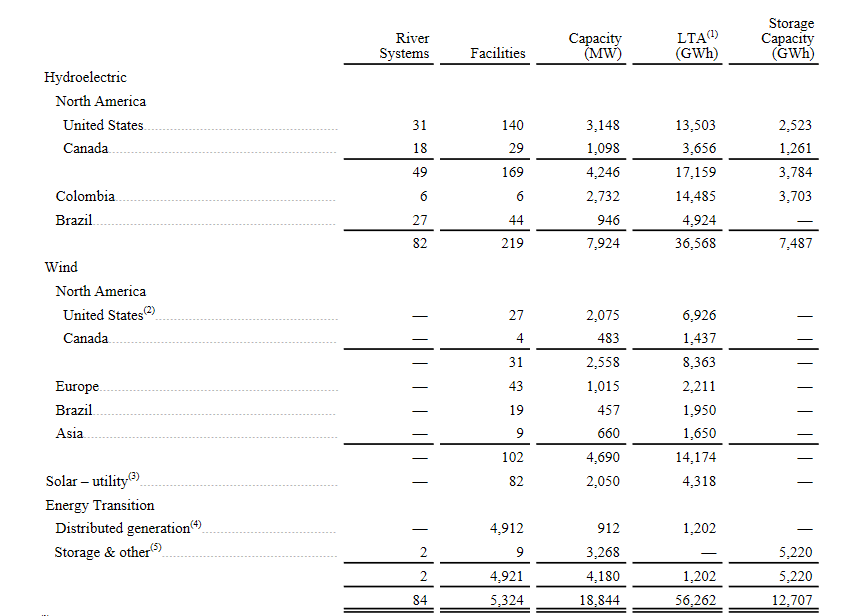

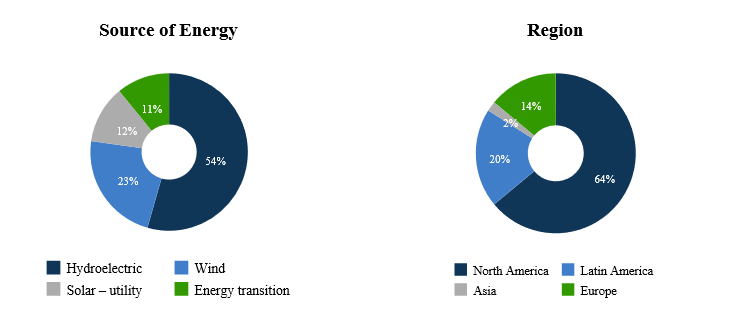

Currently, half of BEP revenues and more than half of its capacity are provided by hydropower (energy transition is largely composed of pumped hydropower, using the dams like giant batteries).

BEP power distribution, Source: https://bep.brookfield.com/

BEP cash flows, Source: https://bep.brookfield.com/

Source: https://bep.brookfield.com/

The Growing Wind and Solar

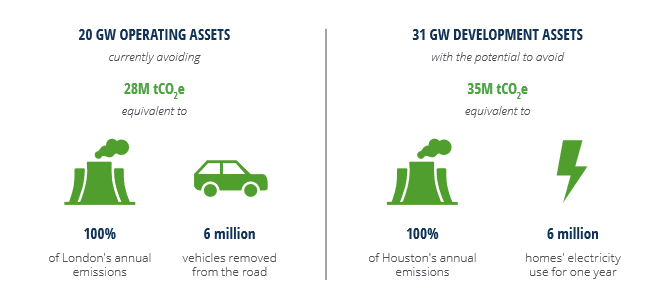

BEP has very ambitious growth plans, planning to increase its power generation by over half by 2030.

Source: https://bep.brookfield.com/

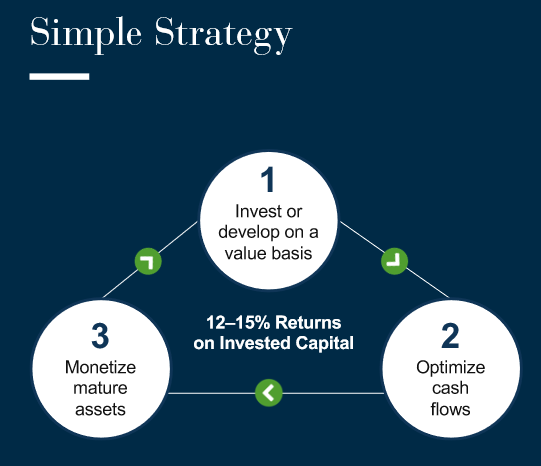

I really appreciate how casual is the company management about the strategy, calling it simple. And it is. They use mature assets like hydropower to generate free cash flow (the dams need little capex) to invest in profitable new ventures.

This will generate new cash flow, and the new assets turn into mature assets themselves. The whole ensures a steady 12-15% ROIC that can permanently reinvest in itself.

Source: https://bep.brookfield.com/

Jeff Bezos is famous to have built Amazon’s success on what does not change. People liked, still like, and will forever prefer more choice, quicker delivery, and cheaper prices.

Similarly, as long as the world will be hungry for energy, and global warming is a concern, BEP will be able to keep this flywheel running and compound at 12-15%. This seems a pretty safe bet.

What does this growth look like?

It is things like the building of one of the world’s largest new solar fields in Brazil. Or the merging with Terraform Power to consolidate activities in Europe and North America (total of 4GW of production or 20% of BEP). Or acquire Exelon Generation company (360MW) and Shepherd wind farm (845 MW).

The total amount is 23 GW of the development pipeline, or more than double of BEP’s current production. BEP has been for now exclusively present in the Americas and Europe, but this is about to change.

Source: https://bep.brookfield.com/

In a 2019 call, BEP management explained that they had focused on US wind farms. It was simple: because they had generally better returns. But with the market quickly evolving in India, they bought 210MW of wind farms, and plan to buy more. Additionally, BEP bought 200 MW of wind farms in China.

I would not be surprised that with such acquisitions, the actual growth of BEP will be even quicker than expected, with Asia becoming quickly one of their top markets, maybe even ahead of Europe and Latin America.

Just India and China could do the trick, but also Japan, Korea, Indonesia, and the rest of South-East Asia as well, a region rich in both solar and offshore wind potential.

Chapter 3: BEP’s Future

The Coming Instability

Once again, I think the energy transition will happen. And I certainly hope it will. But I doubt it will happen in a perfectly straight line.

So, we will likely see a short period where green energy gets in trouble, either because of poorly designed unprofitable projects or because the effect of intermittent production on the electric grid has been underestimated.

The recent explosion in energy prices in Europe highlight such a moment.

This reminds me greatly of some of the few best oil majors compared to the majority of the shale oil companies. In every boom, you always have a few smart companies, generally the larger and experienced players, carefully looking at profitability, and swarms of new companies looking at growth at any cost.

Generally speaking, the experienced giants tend to buy back the assets of the failed growth-focused company when the time is right.

I fully expect BEP to come out stronger from any temporary setback for renewables. It also demonstrated a strong capital discipline, for example entering the Indian market only once the local prices, rules, and regulations allowed for renewables to be profitable. And like a fearsome ambush predator, it has plenty of cash to grab any distressed assets from overextended companies with too much debt.

So overall, I will focus this analysis on the long-term past performance and long-term opportunities, instead of trying to predict the company’s short-term perspective, which is almost always futile anyway.

BEP Financials

Revenues and Depreciation

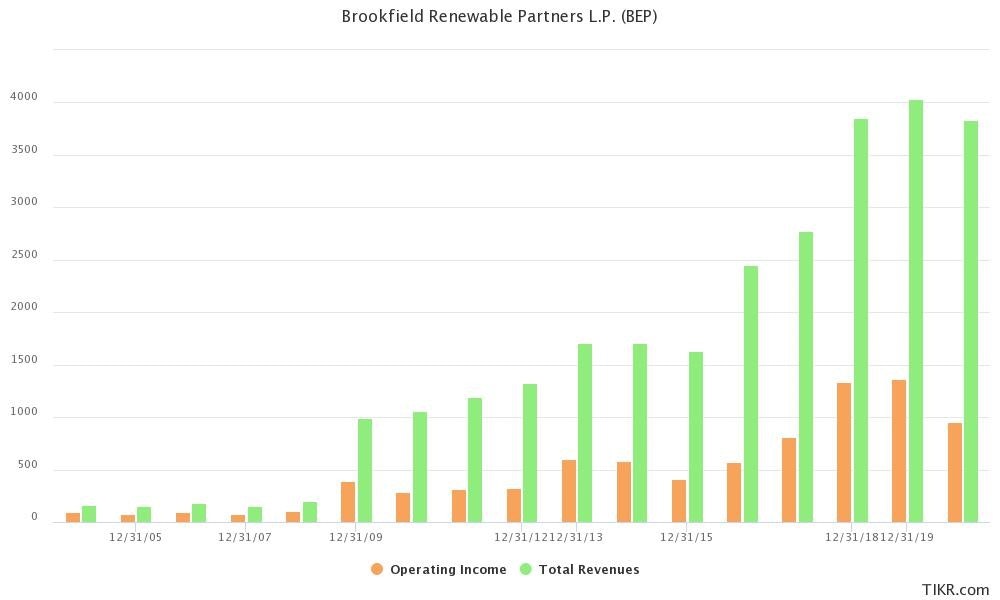

For a utility company, BEP has the most unusual revenue profile. Revenues are growing stronger over time, even if it is more by stride than a perfectly steady pace. This is mostly since the building of large solar or wind farms, or the acquisition of a smaller company creates a sudden surge in revenues, instead of a steady growth every quarter. Anyway, from revenues alone, we can validate the profile of BEP as a steady compounder.

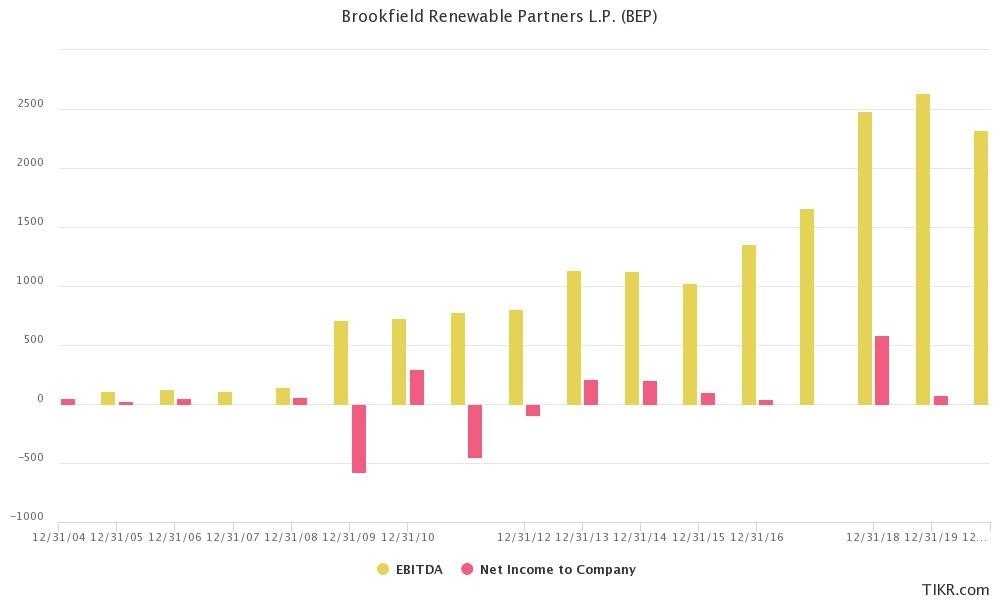

As said before, the picture is a lot less clear with net income, as depreciation is designed to cancel the net income. This can be shown by the rising EBITDA for the same period.

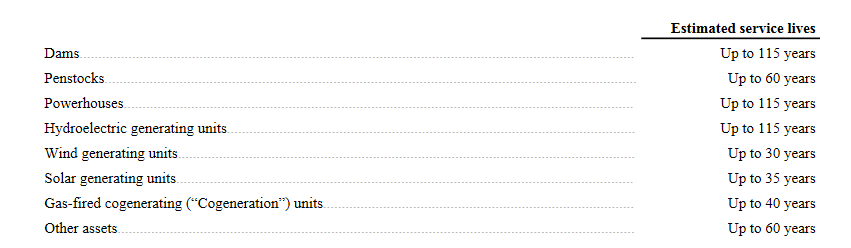

As the topic of depreciation is so important to BEP finances, I looked deeper into the annual report to find the details about it. The company uses a “straight line” depreciation method, with asset life durations varying depending on the energy source.

For dams, by far the most expensive asset to build, duration is 115 years, which is, in fact, conservative, as “the civil engineering infrastructure should last almost indefinitely provided it is maintained”.

Therefore, I would consider that the hydropower division is depreciated at a fair speed, and if anything quicker than needed, helping to reduce net income and therefore income tax.

Source: https://bep.brookfield.com/

As newer technologies, some doubts exist regarding wind and solar farms’ lifespan. Solar panels seem to lose approximately 0.5% of their output per year. Most solar panel manufacturers guarantee at least 80% of initial production after 25 years.

It also seems that proper maintenance helps increase solar panel duration. A very technically able company like BEP should easily be able to still have some production and residual value from its solar farms in 35 years (maybe even still 50-60% of initial production capacity), when they consider them fully amortized.

Again, a conservative estimate that depresses artificially earnings.

For wind farms, windmills’ lifespan is between 20 and 30 years. Windmill lifespans seems to have improved in the last decade, with 30 years lifespan becoming the norm. BEP’s estimate is not really conservative but seems fine.

Overall, this tells me that earnings are indeed artificially suppressed by the depreciation policy.

Free Cash Flow

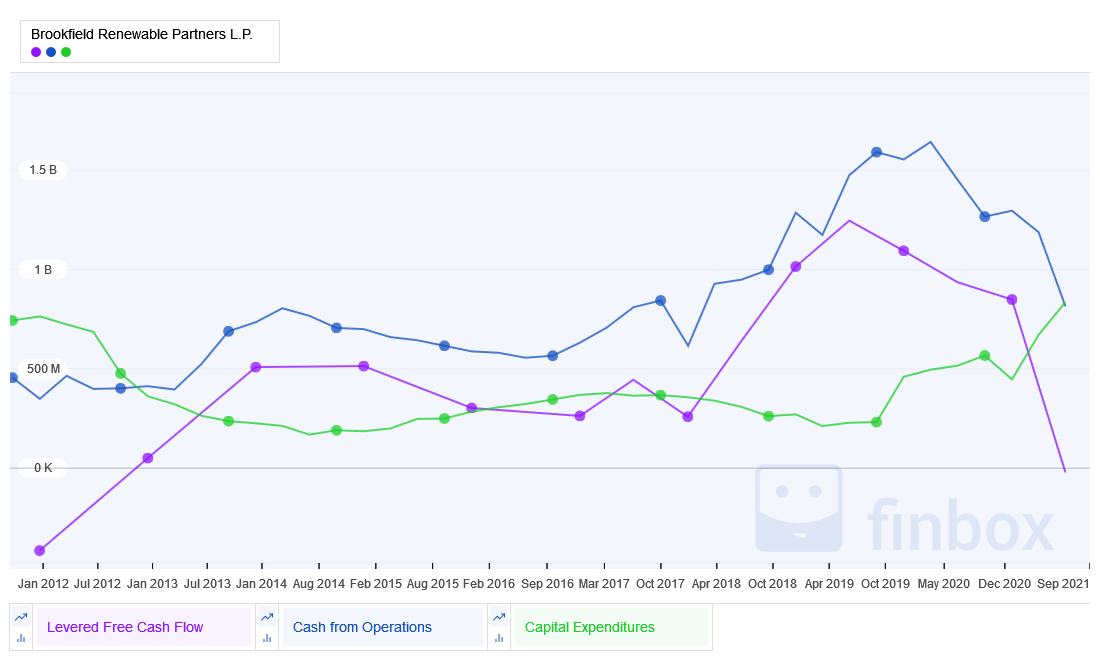

In order to have a better view of the real profitability of BEP, we need to look at cash flows. Simply looking at cash flow will not be enough, as we need to distinguish the cash used in operation maintenance and financing from the one used for growth.

So free cash flow is a better measure, but still underestimates current profitability, as some of the current capex is going to growth projects and not just maintaining the business operations.

But anyway, a growing free cash flow gives us again a compounder profile. And the recent surge in capex should bring growing income and free cash flow in 2-3 years down the road.

Source: www.finbox.com

Debt And Balance Sheet

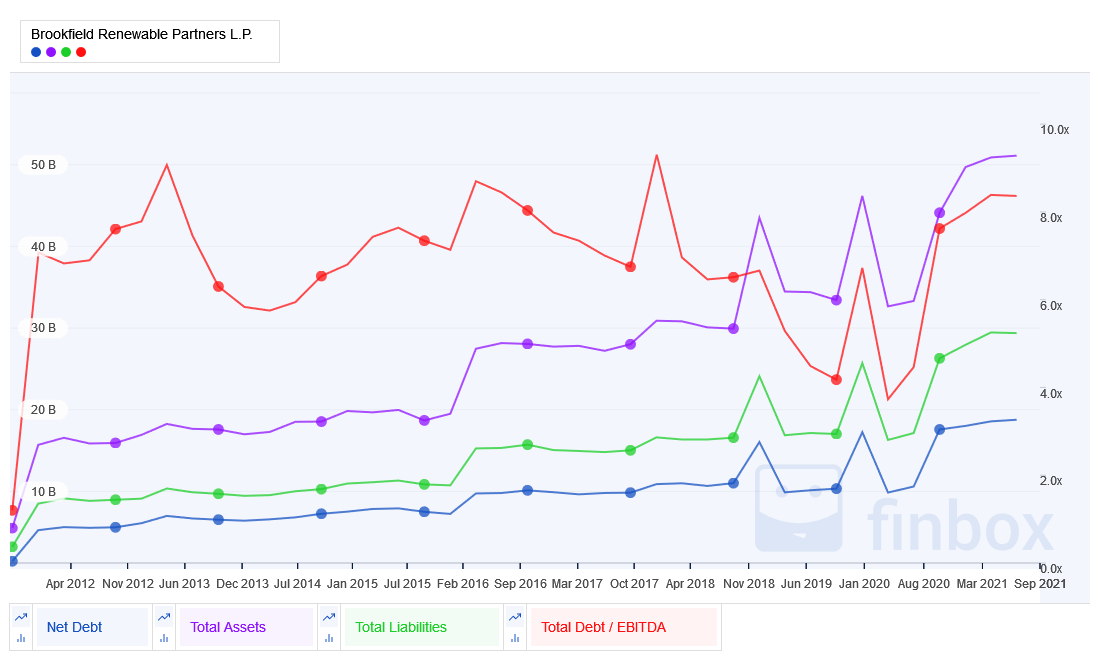

With utilities, considering the stability of the business, the moat, and the duration of the assets, the only thing that can bring it down is poor management of finances and the debt load. Debt has increased a lot in the last 10 years, and so have total assets.

Net debt has increased over time, but not dramatically. By following the total debt to EBITDA, it seems that while quite high (between 6x-8x), it is not out of control or out of the ordinary for a utility company. As BEP has no fuel input cost like coal or gas, its cost structure is fairly predictable, and profitability should stay strong.

The company seems at no risk of a liquidity crisis, with $3.3B of available liquidity. And as mentioned before, it can easily access some of the gigantic $625B pool of capital managed by BAM, the parent company. The debt has an average maturity of 13 years, with 97% of it at a fixed rate.

Together, this means that the company has a very stable debt outlook. And if inflation becomes a larger problem in the decade to come, BEP will be perfectly positioned to register huge profits from it (it should be able to raise the price of its products and use the extra cash to pay a debt shrinking in real terms).

Dividends and Returns to Shareholders

BEP has a strong focus on offering stable and growing returns to its shareholders, well aware that this is what investors expect from utilities. The company communication is clearly geared in that direction, with a strong insistence on BEP having consistently beaten the main indexes in the long run.

This is true both since inception and for the last 5 years, an impressive performance with the S&P 500 doing very well in that period.

Source: https://bep.brookfield.com/

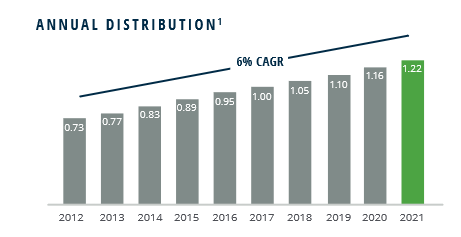

Returns to shareholders are made through dividends, which have increased by 6% yearly on average.

This again seems to fit the profile of BEP as a stable growing compounder. The only weak point on this topic is the dividend yield, which has strongly declined in the last two years, reflecting the quickly growing share price compared to the slower growth of dividends.

This leads me to expect a slowdown in the share price, at least until growing free cash flows and dividends can catch up, and dividends yield get back to a more respectable 4-5%.

As such, I do not expect BEP returns in the next 3-5 years to be above 12-16%, as some of the company quality is already priced in.

Chapter 4: Valuation

When it comes to the valuation method, as earnings are artificially depressed and unstable, calculating earnings growth is obviously out of the question. The equity bond valuation method also uses earnings per share, so it is not applicable here.

So, I will first defer to my discounted cash flow method (DCF). Considering the stability of the business and its dividend growth, I will also look at another valuation method, yield on cost.

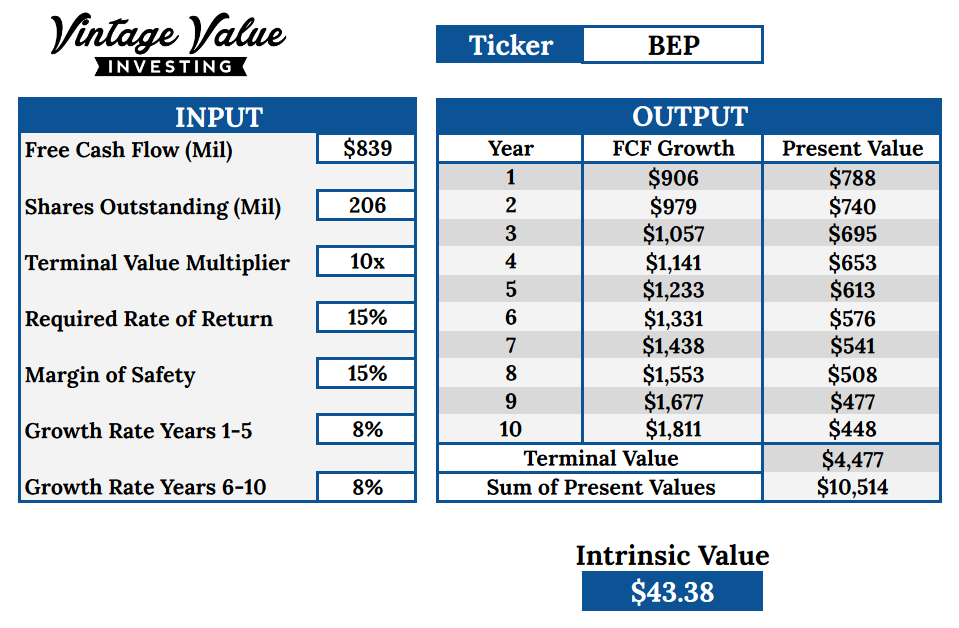

Discounted Cash Flow

BEP’s price to free cash flow multiple has historically been between 12-18x. I took a more conservative 10x to stay safe. Similarly, the historical growth rate of free cash flow has been an average of 13% the last year. I took a conservative 8% instead.

Even with such very conservative assumptions and a solid margin of safety, I end up with an intrinsic value of $43, to compare to the 38$ share price.

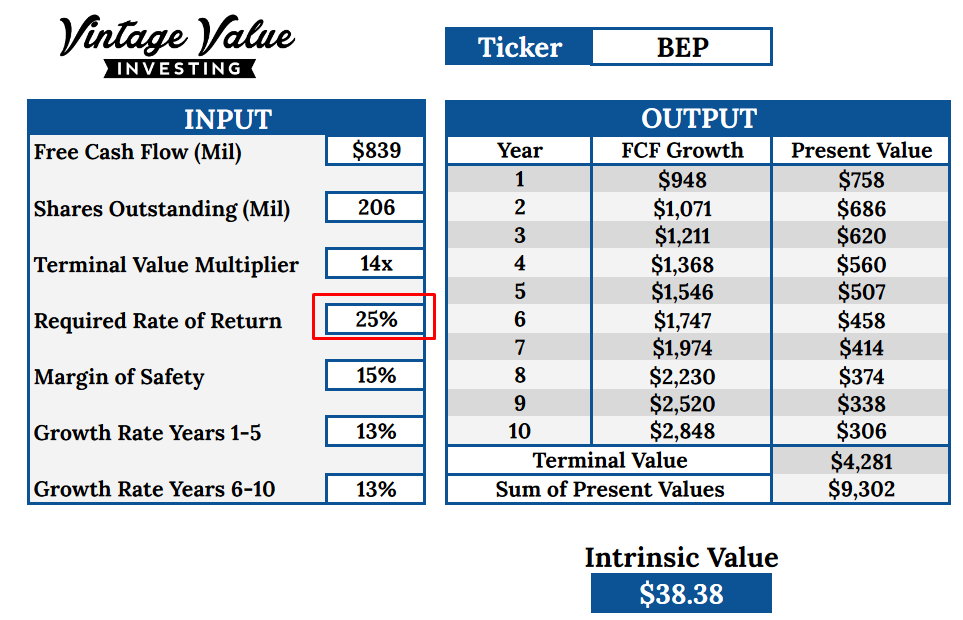

Curious to see what a best-case scenario would look like, I used numbers if business as usual persist, instead of conservative assumption. At the current share price, this would mean a 25% rate of return. Really impressive!

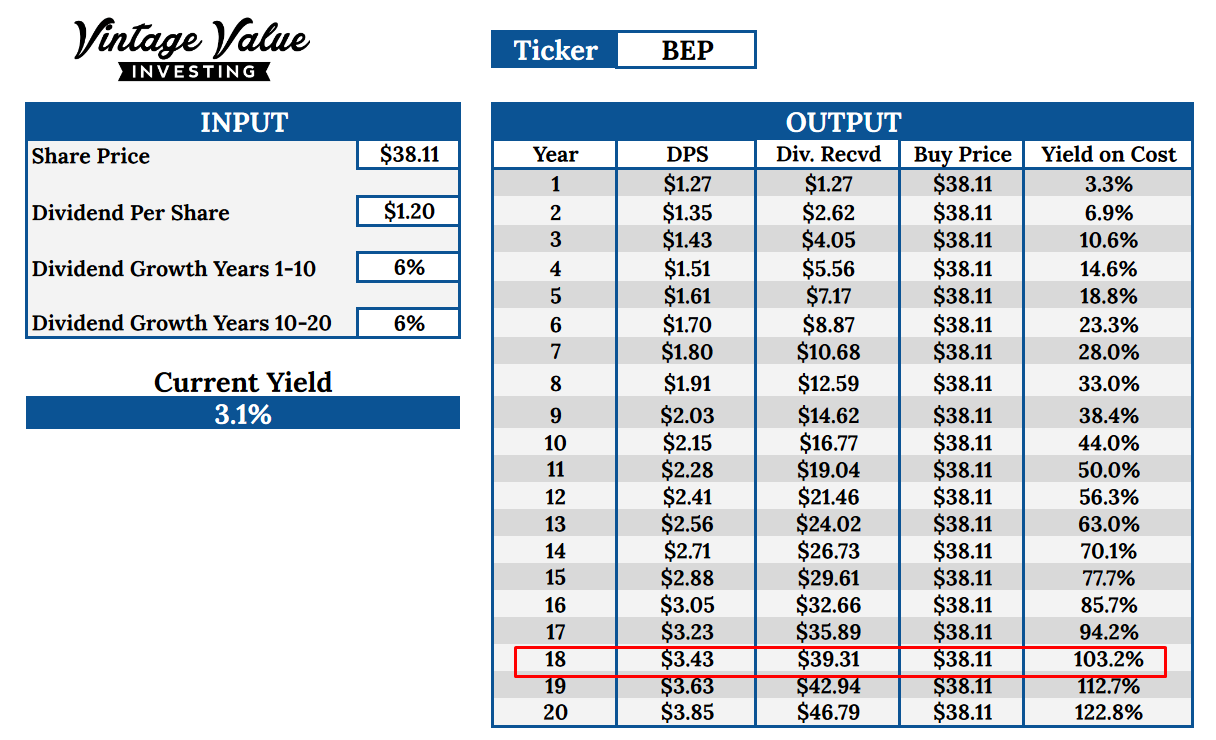

Yield On Cost

Due to the currently rather low dividend yield, the yield on cost calculation shows a less rosy picture. It would take 18 years to cover the current buy price with dividends alone.

The 6% dividend growth I used is in line with historical growth, but not with free cash flow growth. If dividend growth would follow free cash flow growth, this brings it to 14 years to cover the purchase price. Not terrible, but not great either.

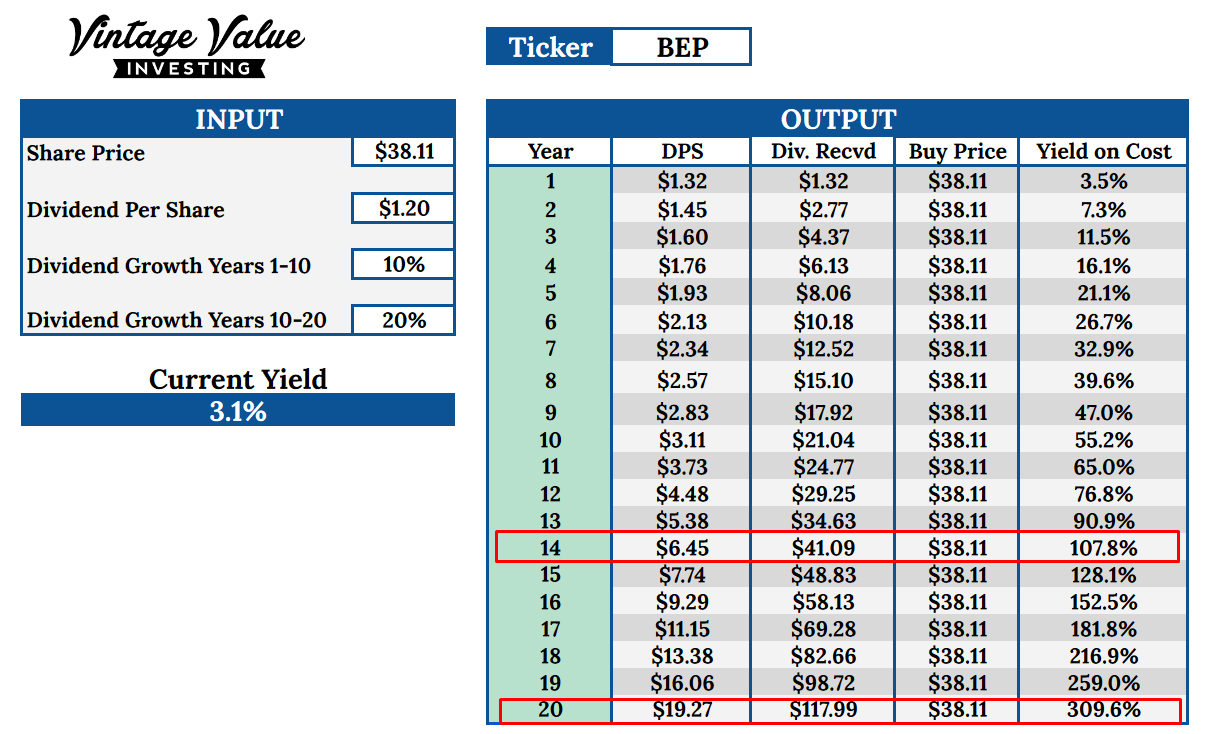

It is however interesting to notice that with BEP planning to steadily grow its income and free cash flow, a 10% growth followed by quicker 20% “catch-up” growth would have a dramatic effect in the long run.

Getting back the initial investment would happen 4 years earlier, not a spectacular difference. But by year 20, the difference would be between 122% and a much juicier 310%. This is the magic of compounding at work!

Conclusion

With this report, I wanted to analyze a company that would be a true buy and hold forever. A utility company that had fully embraced the energy transition and would be able to smoothly ride with growing cash flow and dividends.

I would then say this is quite a success. The very nature of BEP business is very capital intensive and long-term focused. We have here a company with assets lifespan measured in decades or even centuries.

How many companies can you do that with? Not many.

The historical heritage of hydropower is being leveraged to finance the future wind and solar farms and guarantee strong production growth. BEP is perfectly positioned to grab the tailwinds of ESG investing, electrification, and the fight against global warming.

The company has debt, but with a very long duration and at a fixed rate, making a surprisingly strong inflation hedge, almost as much as would an energy company or a gold miner.

BEP seems to me like a slow-moving, but almost unstoppable force. Returns might be for a few years be limited to the 3-5% dividend yield when the company is focusing all the available cash on growth projects.

The share price might even fall if electricity rises too much and a backlash against renewables builds up. But in 5-10 years, I expect more of the cash flow to be distributed and go in line with the 13% free cash flow compounding.

This might not seem spectacular, but this would create exponential growth, with most of the returns happening in the years 20-30.

With that in mind, I think the position of BEP in a portfolio is pure as an investment for a retirement account (with untaxed profits). Returns can be expected to be great, but mostly far in the future. The fluctuation of the share price on the way should not impact this strategy, except maybe on when to buy some more after a temporary weakness.

Right at the time I am writing this report, financial markets are worrying about a possible Chinese crash with Evergrande, supply chain woes, and inflation getting out of control.

But here is the magic surrounding BEP: None of these concerns will matter to BEP’s long-term success!

Even if BEP is a “boring” investment, it is likely to prove to be the proverbial winning turtle over the more aggressive, but less steady hare. And provides peace of mind to its shareholders that few other companies can rival.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in BEP and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.