May 26th, 2021

Pampa Energia (PAM) & Companhia Paranaense de Energia (ELP)

Common background for both PAM and ELP

For the prudent investor, utilities have long been a safe haven from the volatility of the stock market. This is especially true for electric companies.

A Sector Full of Moats

Irrespective of the individual companies’ decisions and situations, utilities tends to benefit from a series of moats due to the structure of their business sector.

The first one is economy of scale. Electricity production is a very capital-intensive sector, and new dams, power plants or electric grid networks require billions to be build. They are also very durable assets, lasting decades. This means that any company able to gather a critical mass of assets will be able to save on maintenance, corporate overhead, regulatory costs, etc.… thus reducing the cost per kW produced.

The second one is operational capacities. Being extremely technical and sensitive operations, utilities need specialized personnel who are experts in their trade, and very familiar with the infrastructures in place. Running the electric supply of a whole region or country smoothly and efficiently is no small feat, one which would be hard to replicate for a newcomer in the industry.

Lastly, utilities, due to their vital importance to the country, are heavily regulated. Prices are often decided jointly in negations between the company, the government, and other stakeholders, to guarantee that sufficient investment can be made to maintain a stable and safe supply. Employees will need specific certifications. The company’s assets will regularly be audited and controlled by the regulatory agencies.

Regularly, a company will be granted a monopoly over an entire region, or even sometimes the whole country, reducing vastly the sales & marketing costs.

All together, these moats mean that utilities tend to work as monopolies or oligopolies, with very limited competition.

Pricing power is somewhat limited by political constraints to not completely gauge the consumer, but profits per kW produced are almost guaranteed to stay above a certain threshold. Otherwise, under-investment and corner cutting could endanger the country’s electric supply.

A Value Investing Approach to Utilities

For a value investor, utilities can seem like a perfect company to own.

- It has large and almost indestructible moats.

- Its business is highly predictable, and it is not uncommon to be able to be reasonably sure of the company’s prospects 20 or 30 years in the future.

- It is asset-rich and usually can borrow at low cost (instead of needing to constantly raise capital and dilute existing shareholders).

- It is always able to price its production to guarantee a profit and a healthy margin. Actually, the government itself has an interest in making sure that the company has enough cash flow and profit to reinvest into its assets.

- It is likely to keep growing at the speed of the broader economy.

So, in terms of company quality, utilities have a lot to go for them. But of course, one last important question is the matter of price. Due to their safer nature, utilities tend to often be pricey. Cautious investors like utilities, and sometimes buy them at any price as an alternative to bonds. In an era where safe bonds have often zero or even negative interest rates, this makes sense.

But this is a big problem for any other type of investor, as these companies are unlikely to grow quickly, improve dramatically their margins, or launch a new bestseller product like other companies. If bought at an expensive price, they are unlikely to lose you much money, but will also not bring much in the form of returns.

In a nutshell, utilities are great stocks to invest into, as they have very strong intrinsic margin of safety built-in their business model. But low growth and stability means these returns will only be good if the stock is bought at a discount.

The Hunt for Utility Value

A lot of investors are looking for a safe place instead of cash and bonds have been putting money in US electric utilities. The growth of passive investing and ETF indexation might also have something to do with it.

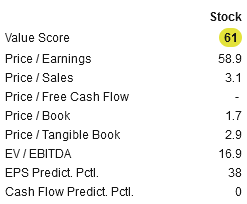

This has brought their price up, way above fair value, in my opinion. For example, you can look at Duke Energy. This is just an example, I have no special grudge against this company, but its ratios seems out of place for something as stable and “boring” as an electric utility.

Source: www.stockrover.com

With a P/E of 59 and no free cash flow, why would anybody want to buy this stock at this price? I might be missing something here, but at first glance, this looks really expensive, especially since we remember that the company is unlikely to be able to increase price or expand massively without expensive mergers or acquisitions. A lot of other utilities in the US seem to be similarly expensive compared to earnings, cash flow, return on capital, or really any metric. But why limit the search to the USA?

The Hidden Gems Overseas

Even in countries with unstable politics and struggling economies, electric utilities can be a good investment. This is because, like food and water, electricity is very much a basic in life. In a crisis, people might forego dinner in town, house renovation, vacations, and other luxuries. But they are likely to keep the lights and the freezer on as much as possible.

At the same time, dramatic economic instability has a strong tendency to spook investors away from ANY company in a country, depressing stock prices, no matter what the fundamentals of an individual company are. And in such market mispricings lie the opportunities for the astute value investor.

Two countries in particular have caught my attention: Brazil and Argentina.

Brazil’s economy has been struggling for a while. In 2017 it went through the “worst recession on record”. And in 2020, suffering from an out of control COVID outbreak, its GDP dropped 4% and the country went from the 9th to the 12th world economy.

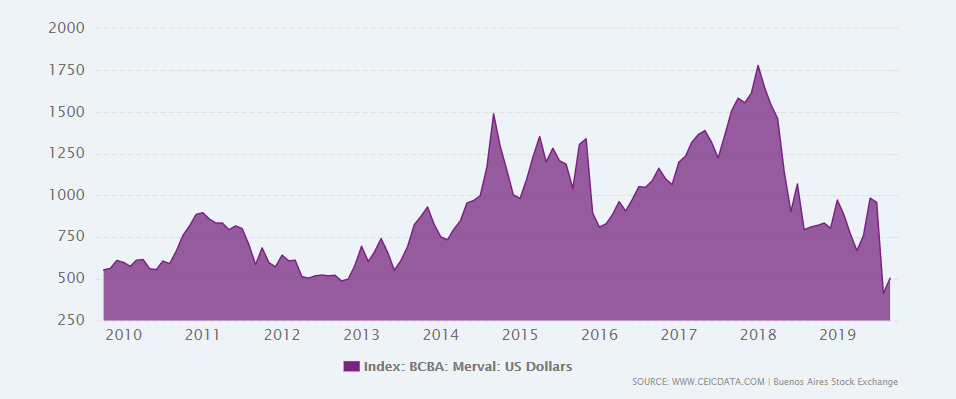

If Brazil the economic outlook does not look great at the moment, its neighbor Argentina is way worse. A first look at the main Argentinian index, the MERVAL, might indicate there is no problem. But with the regular collapse of the local currency, the stock market performance actually look as if measured in US dollars.

Source: www.ceicdata.com

A recent 70-80% decline and virtually no progress in a full decade of booming stock market worldwide. No surprise, this means that ALL Argentinian equities are quite out of favor at the moment. To keep the report reasonably short, I will go into detail about Argentina’s history, but you see more about it in this video.

In each of these countries, I found an undervalued electric utility company worth a look. I decided to exceptionally publish this as a double report, as the profile of both companies was somewhat similar. Both are in the business of power generation, established in an out-of-favor South American country, and seemingly undervalued.

One has higher risks and higher rewards, while the other is safer but also less likely to provide extremely high returns.

So, I thought that publishing them side by side would give quite a good example of crisis investing strategy, of how to manage country and currency risks and how to search for high returns overseas.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Quick Stock Overview

Ticker: ELP

Source: www.stockrover.com

Key Data

- Sector: Utilities

- Sales ($M): 3,360

- Industry: Utilities – Diversified

- Net Cash per share: $-2.03

- Market Capitalization ($M): 2,985

- Equity per share: $6.70

- Employees: 6,832

- Debt / Equity: 0.5

- Interest coverage: 408.9

Summary

Companhia Paranaense de Energia (which will be referred to as Copel) is an electric company operating in Brazil, mostly in the state Parana. The state is one of the most developed in the country, ranking 4th in domestic gross product. It is also the 6th most populous state, with an urbanization rate of 83.5%, with a relatively low crime rate. I mostly bring these statistics to give a fairer picture of the place than the developing nation conditions that many might imagine.

Source: en.wikipedia.org

Strategic Analysis

A Concentrated Activity

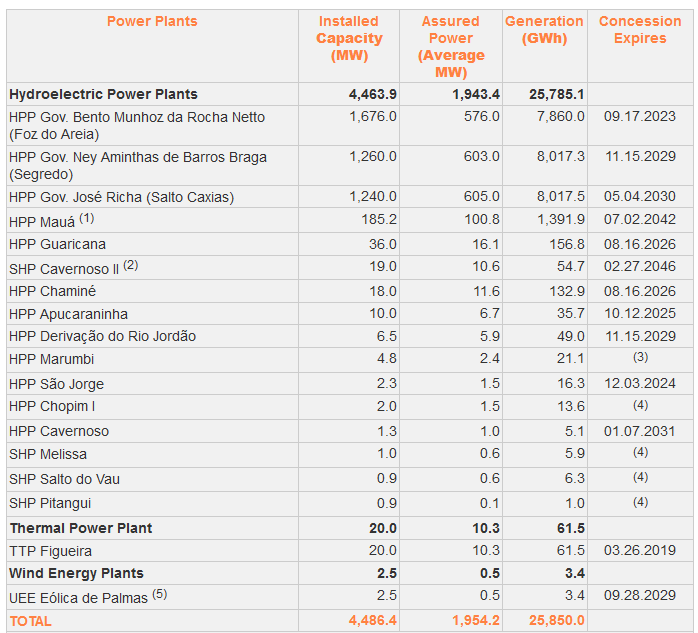

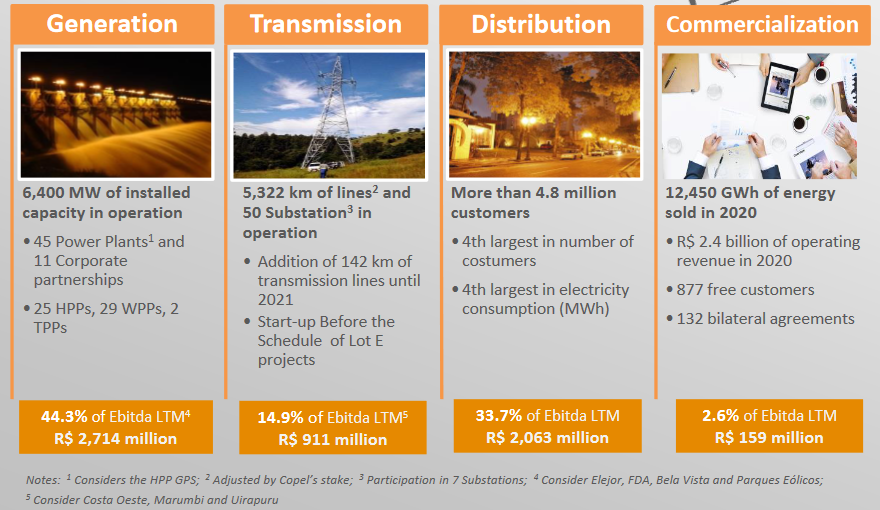

The company is operating a large number of hydro-power plants (dams), but most of its output actually comes from just 3 facilities as you can see in the table below. I imagine the secondary smaller dams are useful for managing peak consumption and water flow, but are not directly very important to the company’s financial results. The same can be said for one thermal power plant and a small wind energy plant.

Source: www.copel.com

The company is also handling transmission and distribution of the power it generates, vertically integrating the whole value chain.

It also used to own a telecom operation, but it has very recently sold it, to re-focus on its core business of power generation and sale.

Source: api.mziq.com

Total capacity in production and distribution has been increasing over the last 2 years.

Source: api.mziq.com

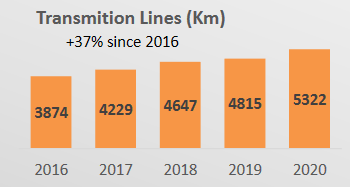

An extra 120 MW of production and 142 km of transmission is already in construction.

Source: api.mziq.com

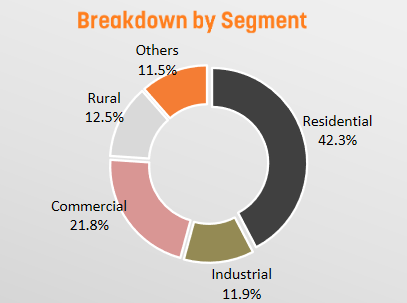

The main clients of Copel are residential consumers, with the rest (rural, industrial, and commercial) making up for the other half of the consumption. As I discussed before, this implies that the business of Copel is highly stable and predictable.

Source: api.mziq.com

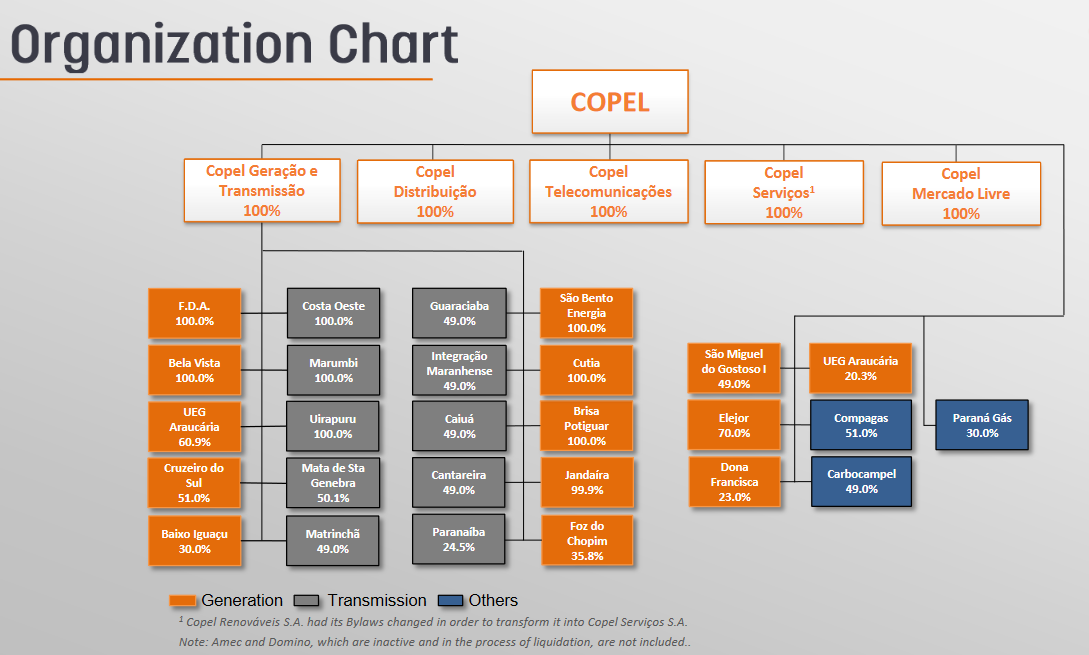

The Corporate Structure

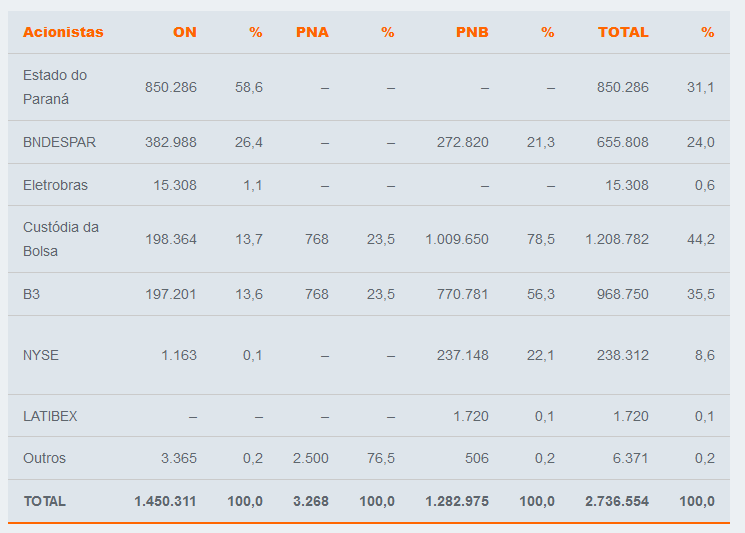

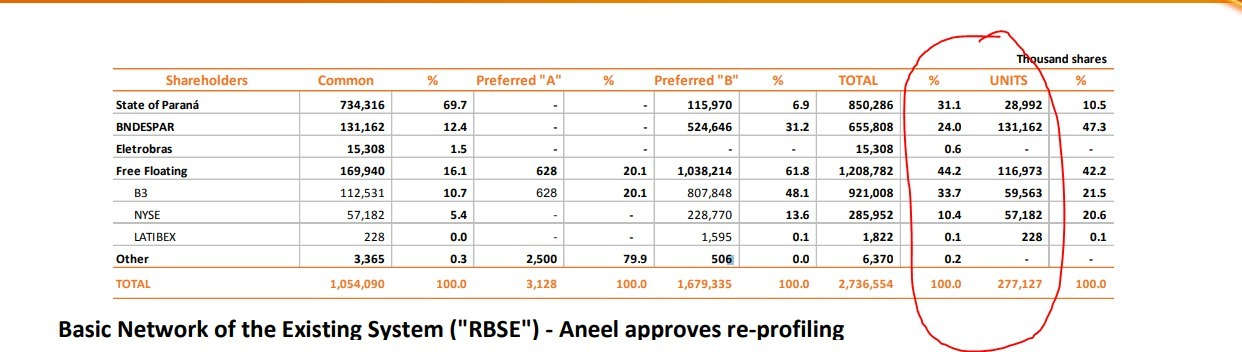

The company ownership is worth a special mention, with the Parana state owning a controlling part (58.6%), together with the Brazilian Economic Development Bank (BNDESPAR, 26.4%). Other significant owners are Electrobras (the largest Brazilian utility), B3, the Sao Paolo stock exchange.

The float present in the NYSE is only 0.1% of the total ownership.

Source: ri.copel.com

Its corporate structure is quite complicated. And this is quite a euphemism from me here. After hesitating for a while, I decided to keep this report readable by not exploring in detail each of the subsidies of Copel. In practice, the annual report and the consolidated financial data give us the bigger picture we need to evaluate the company performances.

Qualitative Analysis

Business Analysis

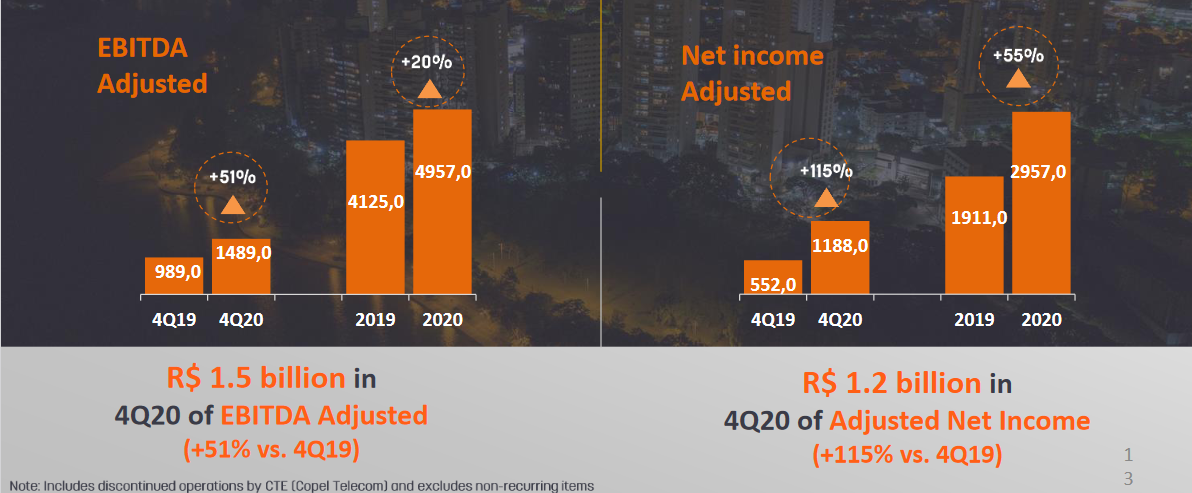

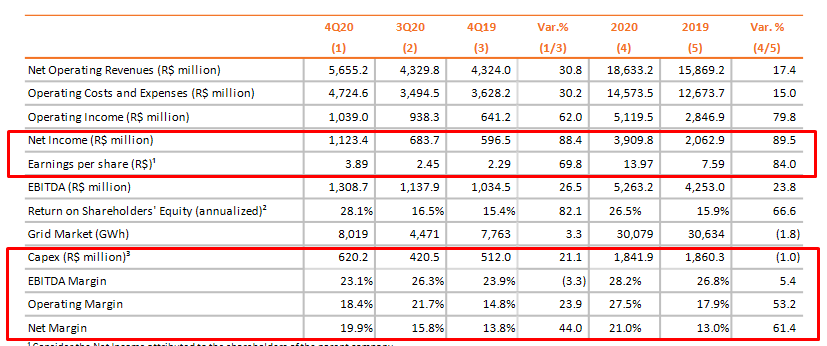

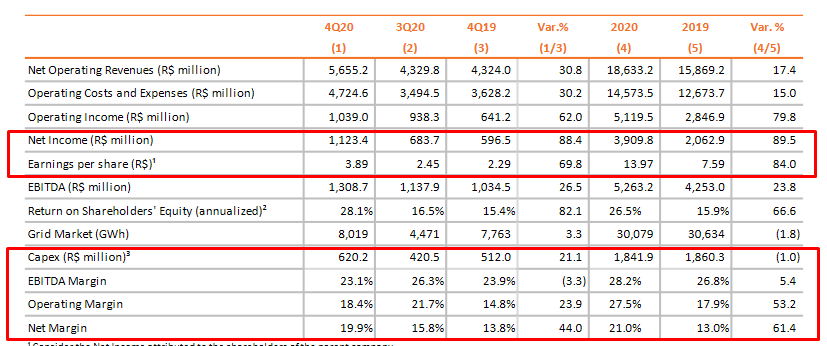

Despite an un-reactive stock price, the company has performed really well in 2020 with increasing income and overall good financial results.

Source: s23.q4cdn.com

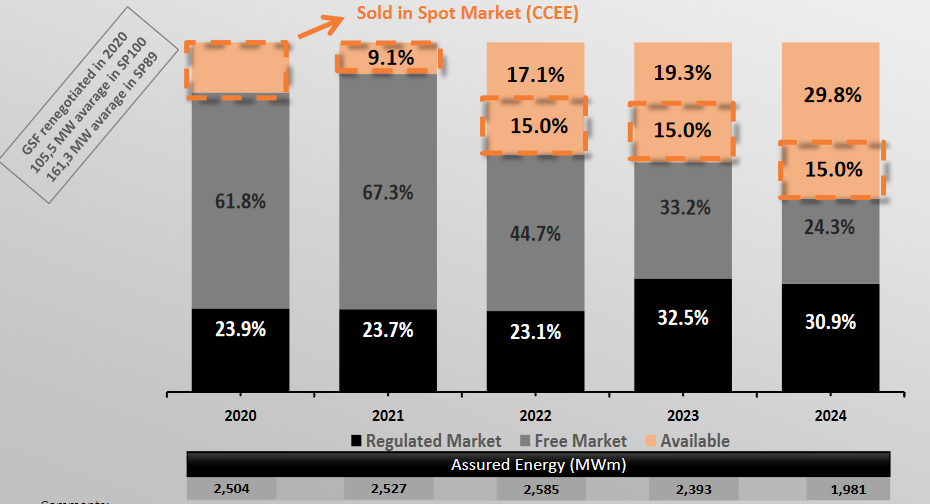

In the next years, Copel is going to increasingly sell its electricity on the spot market, thanks to reform in the electricity market. Spot price means that every hour, the price of electricity is re-calculated according to supply and demands, instead of a fixed rate. Usually this give an advantage to the producers with the lowest costs. This should help grow its margin, especially considering that hydropower is very reactive and can take advantage of temporary high prices, for example if renewable sources are too low at one point. Over time, this should ensure a durable increase in Copel margins.

Source: api.mziq.com

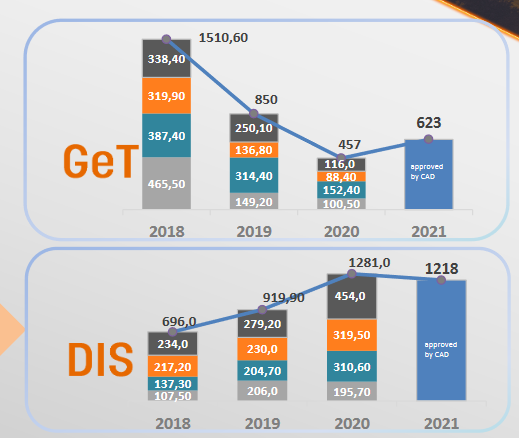

CAPEX

The total capex has decreased over the last 2 years, following the jump in electricity production in 2018. The Capex in now focused on distribution (DIS) instead of Generation and Transmission (GeT), which is logical as the new capacity needs extra distribution network.

Source: api.mziq.com

Economic Moats

Copel is very rich in economic moats, as any good utility company should be.

Long Duration Assets and Low Costs

Being mostly a hydropower producer, Copel has power plants that have low maintenance cost, and no fuel cost. These assets are difficult or impossible to replicate by a competitor, as only a few spots are suitable for the building of dams.

Regulatory and Regional Monopoly

The presence of the Parana state as the main shareholder ensures that Copel is likely to maintain its dominance on the electricity generation in the region for decades to come. Its close contact with the local government is also an advantage when it comes to regulatory agencies and compliance with environmental rules.

Switching Cost

Even if it is possible, people rarely change their electric operator. We just receive the electric bill and pay what got asked. This is partly due to the fact that electric companies operate as monopoly or oligopoly, and also due to regulation of electricity price. Copel consumers are unlikely to leave for a competitor, and switching would be a tedious process.

Management

I was expecting a very local management with maybe some political nepotism, and instead found a very international team. Let’s look at some key people in Copel.

Daniel Pimentel Slaviero, CEO

A Harvard graduate, Mr Salviero was before in various management positions in leading TV and media groups in Brazil. This is a bit of a surprising profile for a utility company. But as the sale of the telecom business was under his supervision, it seems this background has actually helped the company to refocus on its core competency, instead of being a distraction.

Adriano Rudek de Moura, CFO

Another Harvard graduate, Mr de Moura was from 2003-2017 CFO of Electrolux Latin America, a large international group. Again, a surprisingly good and international profile for a local utility company.

Eduardo Vieira de Souza Barbosa, Compliance Director

A native of Parana and involved for years with the local chamber of commerce and business association, Mr. Barbosa seems the perfect profile to navigate local politics and regulations to ensure that Copel operations run smoothly. If there was one job title where I wanted to see an insider of Parana local economic elite, it was this one.

Competition

As a quasi-monopoly, Copel has little competition and is expected to stay this way. The only other major electricity producer in the region is the Itapúa Dam, the second largest in the world after the 3 Gorges dam in China.

Itapúa is at the border with Paraguay and producing 15% of Brazil’s electricity and 90% of Paraguay’s. But as a one single location, international project managed by 2 different countries, Itapúa is not a competitor to Copel that could grow to steal market shares. Hence, Copel’s competitive risk is very low.

Quantitative Analysis

Financials

Revenues

Revenue and income have been growing strongly in 2020. This partly includes the sale of the telecom business, appearing in 2020 as a large 867 million BRL (Brazilian Reals), part of a jump from 2 billion BRL to 3.9 billion BRL in net income.

So, the 1.9 billion BRL increase in earnings is not just a reflection of the telecom sale, but also of growing and more efficient operations. Actually, they could even be higher if the company had not also kept reducing its debt. Earnings per share and margins have also increased.

Source: api.mziq.com

Dividends

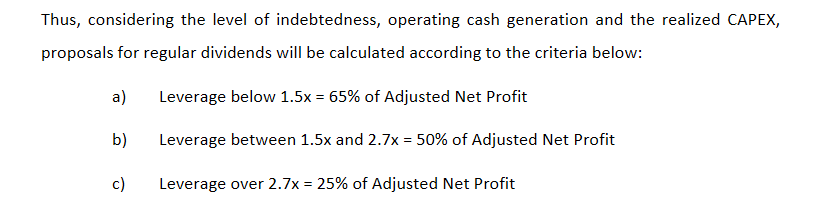

Financial data aggregators like Stock Rover seems to be unreliable for some foreign companies like Copel. Luckily, Copel publishes a clear guideline to forecast its future dividends.

Source: api.mziq.com

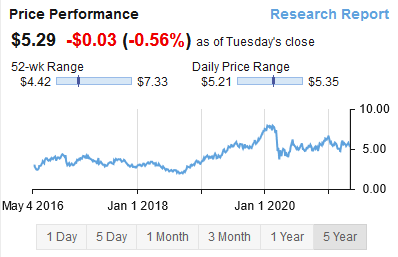

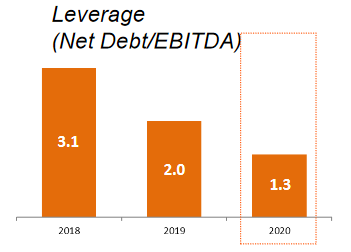

With leverage now solidly below 1.5, we can expect the 65% dividend payout ratio to be the new normal for Copel. With a net income of 3.9 billion BRL in 2020, this represents a total of 2.5 billion BRL in 2020, or 470 million USD.

This makes a total of 0.82$ per share. At the current price of 5.29 USD, this gives a very impressive yield of 15%.

Debt and Balance Sheet

Copel has been steadily deleveraging the company over the last few years, dividing by almost 3 the net debt/ EBITDA ratio.

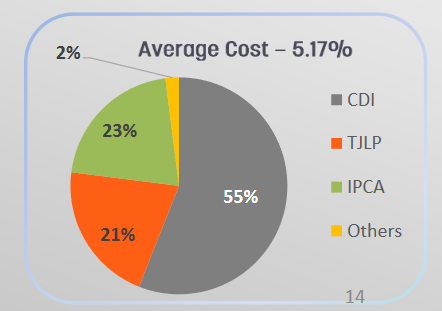

The duration of the debt is a little short and could be improved to take advantage of currently low-rate environment. The average cost is also not so low, but this is not really a surprise considering the premium usually asked from Latin American companies, even one as stable as Copel. Again, refinancing with longer duration would make sense and be an improvement, but debt is not a problem anyway.

Source: api.mziq.com

Cash Flow

I cannot again rely on Finbox or Stock Rover to calculate the free cash flow, so I will do it manually. The simplest way to calculate free cash is to use the formula:

Free cash flow = Operating cash flow – Capex

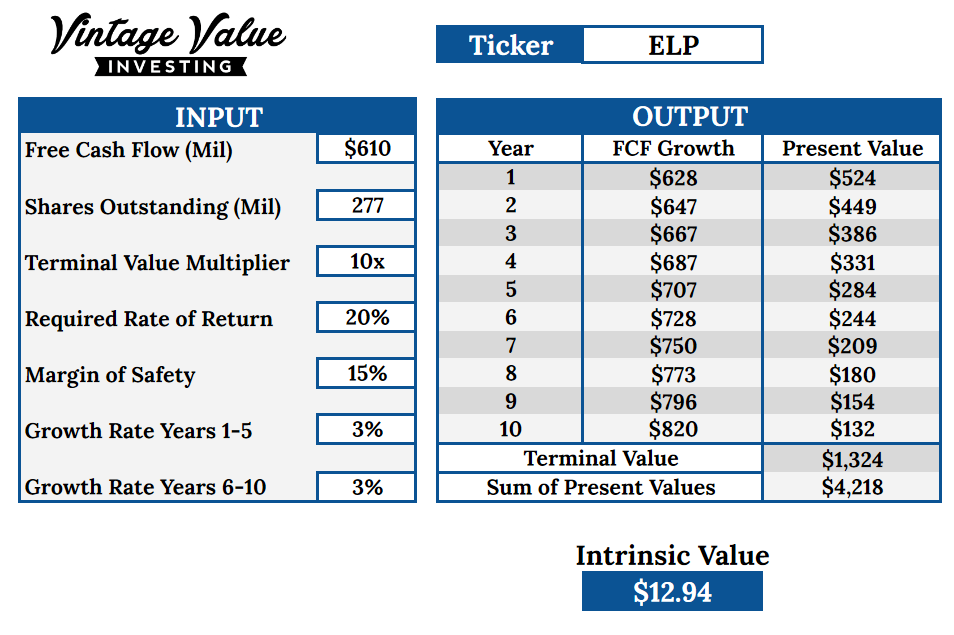

Operating cash flow in 2020 was 3.2 billion BRL and Capex was 1.9 billion BRL, which gives a free cash flow of 1.3 billion BRL, or 610 million USD. This is approximately 1/10 of the total debt, meaning that Copel could, if it chose to, be debt free in 10 years. This is remarkably low for a company with assets lasting decades and very predictable and durable business.

Categorization and Valuation

Investment Category

Copel is the typical utilities company, with large moats, stable durable business, quasi monopoly in its region. Its debt load seems rather low for the sector and does not threaten its future. Now, as Copel is not a steady compounder or a growth company, it is important to determine if it is cheap enough now, as there is little explosive growth that could justify high multipliers.

Discounted Cash Flow

Another way to calculate Copel’s valuation is by using the discounted cashflow model. You can see what it means and how it works here.

Disclaimer: In the last 2 months, Copel has done a 1-10 stock split, followed by a 5-1 reverse stock split just a month after. This was really confusing, and I after hours of reading and re-reading Copel reports, I am still only 50% sure I got the total share number right.

In the end, I decided to go with the new UNITS calculation, which seems to be 277M shares. So, this valuation might be off or completely wrong depending on this factor! I could easily have missed something here, so (as always) do your own due diligence!

For terminal value multiplier I will use a conservative 10 terminal value multiplier. Consider the size of the moats and its business model, I do not need to incorporate a margin of safety, as this is already included in the company operations themselves.

I also used a low growth rate of 3%, mostly in line with Brazil’s growing population and economy, and also to incorporate possible margin growth from selling a larger volume of its power at spot price in the incoming years.

This would give us an intrinsic value of $13 USD, way above the current $5.29 USD.

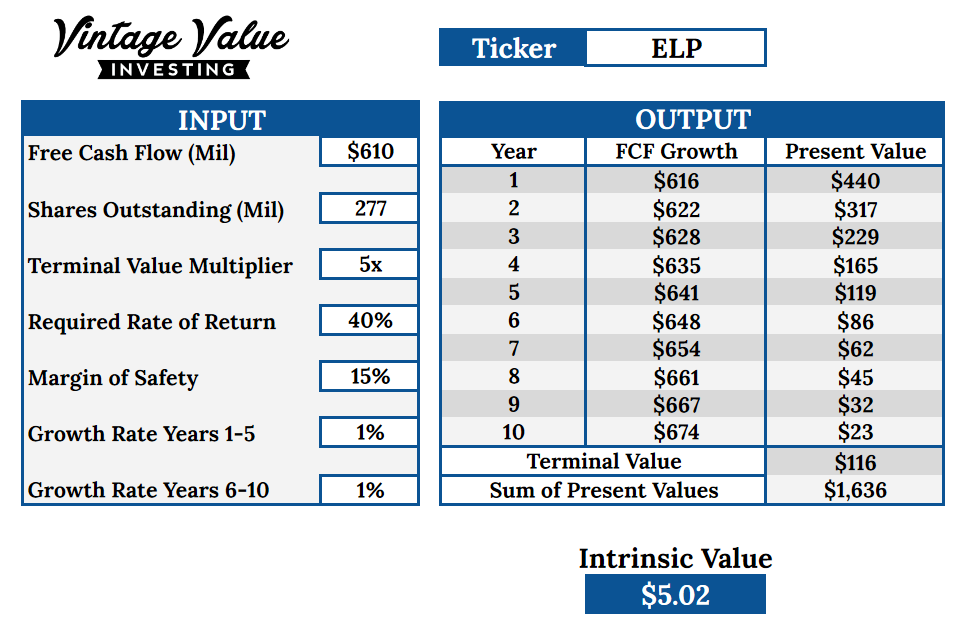

I tried to see what could justify the current price, and even with almost no growth in cash flow, low terminal value multiplier, the rate of return would be at an almost absurd 40%.

So Copel seems at the moment a serious bargain, at least according to discounted cash flow.

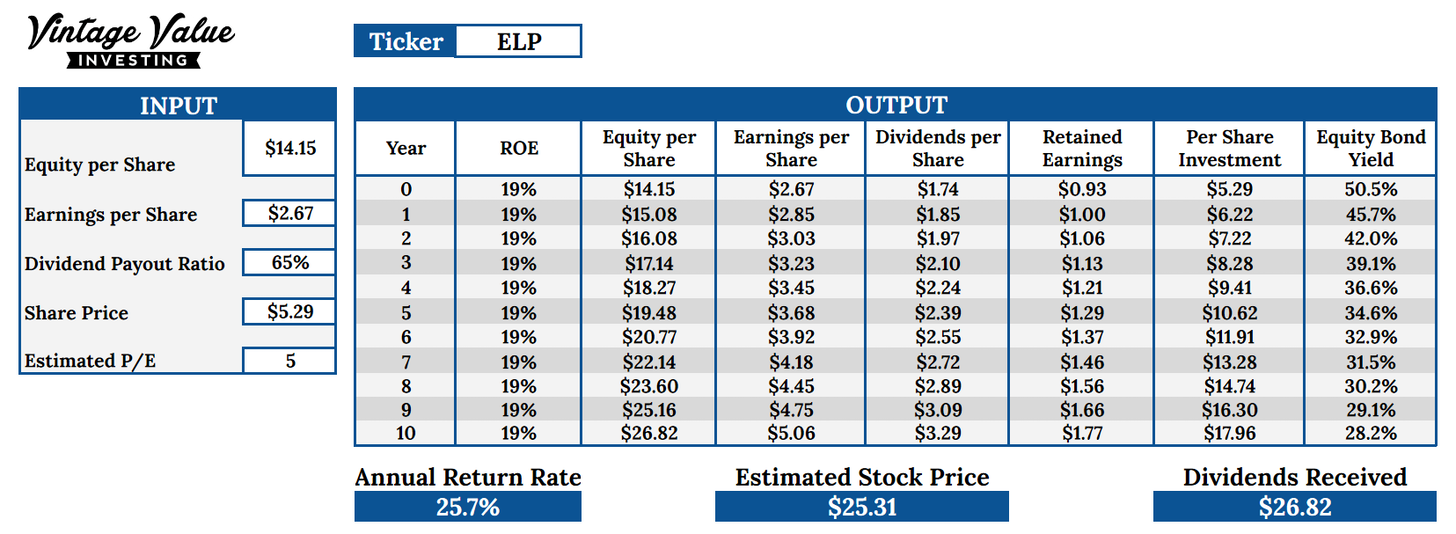

Equity Bond

Thanks to the very high dividend yield and the stability of the business, I think the best way to value Copel shares is to treat them as a bond, instead of a riskier security. Also, dividends are actually something paid and measurable, so I am more confident of the reliability of the data used here, compared to the discounted cash flow method.

Earnings per share were 13.97 BRL in 2020 or $2.67 USD.

I used a very low P/E of 5 in case the company never gets back in the market favor in terms of share price, and shareholders need to rely exclusively on dividends for their returns.

Thanks to the very high current dividend yield, annual returns could be as high as 26%.

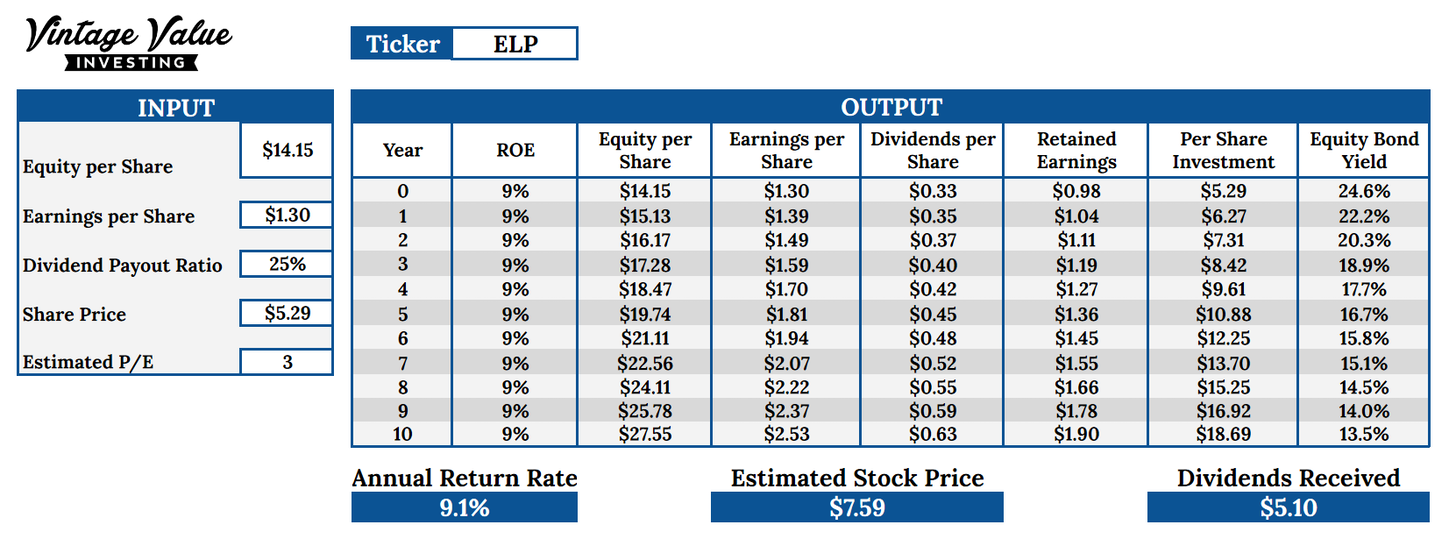

I decided to see if the earnings and payout ratio became less good in the future, what return we could expect in a pessimistic scenario. With extremely low P/E, earnings divided by 2 and payout ratio decreased to 25%, the returns would still be a not so bad 9%, confirming the intrinsic margin of safety present at current prices.

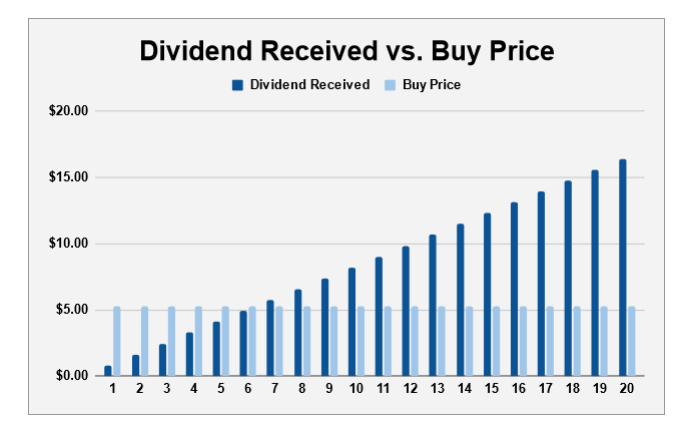

Yield on Cost

Yield on cost just look at the return from dividends only. I also consider that the dividends would never increase in 20 years, something very likely too pessimistic.

Considering the extremely high yield of 15% the company is offering now, this would make Copel a buy just on dividends, even if the company stock price never recover.

In fact, the dividends, even if never growing, would be enough to cover the purchase price after just 6 years and a half.

Other Calculation Methods

Earnings are expected to stay mostly stable, growing only slowly, so I do not think this method is the most relevant for Copel.

Partial Conclusion

With a low price compared to its dividend payout, cashflow, and earning, Copel seems significantly undervalued. A return of 20-30% is not impossible. This is mostly due to the extremely low valuation of Copel at the moment.

The company management seems to agree, and even openly say so in the company’s presentation. It shows how the dividend yield was already abnormally high compared to comparable companies when the stock was trading at the much higher level than today. Management seems to think that Copel stock could go to the 14 to 45 range when the market re-rate fairly the company.

Overall, the very high 19-39% ROE seems to mostly come from a temporarily depressed price and the now achieved debt deleveraging, so I think it might be able to stay stable overtime.

However, a strong risk needs to not be ignored, which is currency risk. Copel is a Brazilian company, with assets and earnings denominated in Brazilian Reals. If Brazil currency would crash against the US dollar, the BRL profit could be entirely lost to the conversation rate changes.

In the conclusion for both Copel and Pampa Energia, I will address how to manage this risk.

Quick Stock Overview

Ticker: PAM

Key Data

- Sector: Utilities

- Sales ($M): 1,928

- Industry: Utilities – Regulated electric

- Net Cash per share: $-8.75

- Market Capitalization ($M): 1,269

- Equity per share: $22.51

- Employees: 1,944

- Debt / Equity: 0.9

- Interest coverage: 2.0

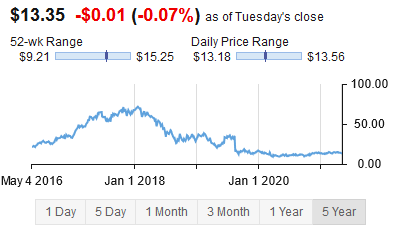

Summary

Pampa Energia, or PAM, is an Argentinian company exclusively focused on the country’s energy sector. Its activities are split between electricity production and distribution (through mostly thermal plants) and natural gas production. The company stock price and activities have suffered from the recent economic trouble in Argentina.

Suffered is probably too weak of a description for a stock that went nowhere since 2014, erasing all its gain since 2017, and collapsing from $70 USD per share to around $10 USD. But I would argue that for the investor brave enough, this is actually an opportunity. The company has not really changed much since 2017, but it is now 7-fold cheaper.

As you will see, PAM is in many ways a more volatile, riskier version of Copel in the neighboring country and I will discuss possible ways to handle the risk associated to Argentina in the conclusion of this report.

Strategic Analysis

The Argentina Issue

Argentina is somewhat of a basket case when it comes to economic performance. It is the only country that has been bankrupt 9 times in 200 years. In a century, it replaced its currency 5 times. And the troubles are not only in the past, with no less than 2 defaults in the last few decades. And it is still the top creditor to the IMF … Worldwide… So why would anyone even remotely consider investing in the country?

One part is that crisis also means opportunity. Depressed prices and assets a dime on the dollar are a basic of deep value investing strategies. While some investors would be permanently sacred off by such a crisis-ridden country, others might want to time their entry after the last crisis is passed.

The other reason is that Argentina’s crises are essentially fiscal and monetary. It is not natural catastrophes or civil wars that are striking the country, but poor management of the currency, inflation, balance of payment, etc.… Just in 2020, the official cost of living in Argentina increased by 36.1%.

But this means that even in the heart of the latest crisis, real assets are still there, perfectly intact. Fertile lands keep growing grass and trees, buildings are still standing, and power plants are still running.

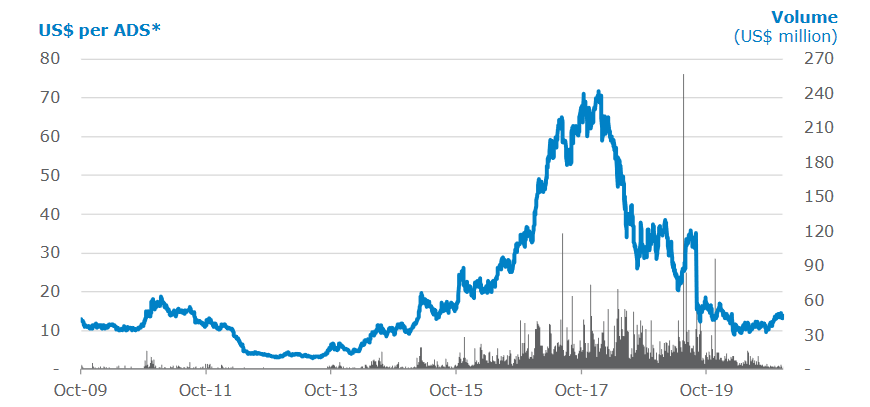

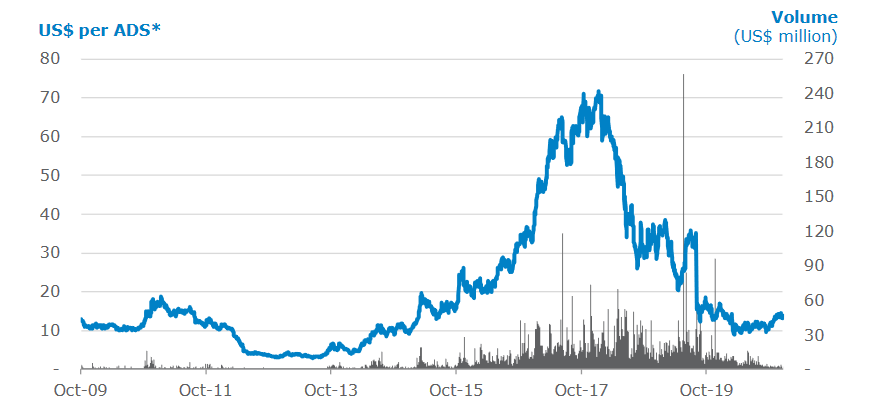

But if you looked at the valuation of Argentinian publicly traded companies, you are more likely to image a devastation similar to Syria than just a poorly managed country. I put down here the graph of the MERVAL, the Argentinian equivalent of the Dow Jones, in USD. I priced it in USD, as in local currency, the stock market seems to go up nominally, only because the real value of the currency is going down the drain.

It spiked at $1700 USD in 2018 and stands in the $300 USD range today. This is one hell of a brutal crash.

Source: estadisticasbcra.com

But does this mean the Argentinian stock market will never recover? I highly doubt it. In fact, you can see in all the previous crashes, the recovery of the MERVAL has been rather spectacular, while crashes are 70-80% down, upsides after the crash are often 70-150%.

So, investing in Argentina is not for the faint of heart, and probably not something you want to buy and hold forever. But that does not mean opportunities are not around, especially for quality assets hammered just because they are Argentinian.

As you can see below, PAM stock has mostly followed the broader stock market direction, but are the recent low levels really justified? I will discuss that further in the valuation section, but first, let’s look at what kind of business Pampa is.

Two Complementary Activities

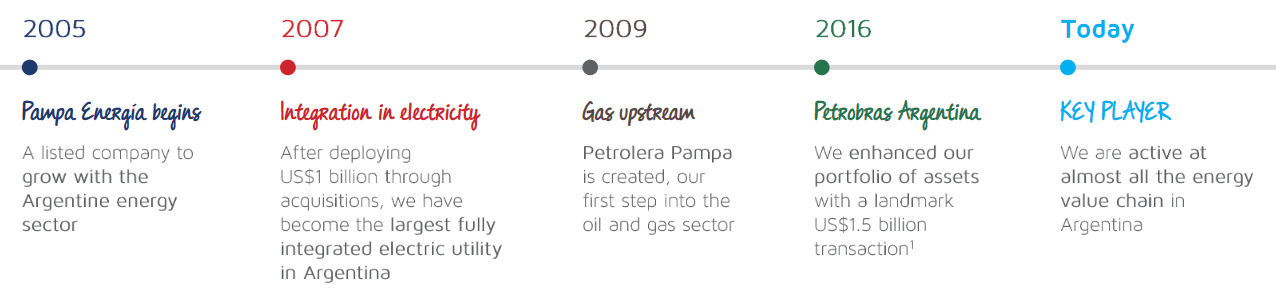

Pampa was founded in 2005 to be an investment vehicle to gather assets in the Argentinian energy sector. It progressively expanded to the gas & oil sector and expended further with the acquisition of Petrobras Argentina assets in 2016.

The company is involved at multiple levels of Argentina’s energy backbone through complex multi-layered ownership, so I will detail the exact percentage of each part in the corporate section below. But first, let’s have a general overview of the assets owned or co-owned by PAM.

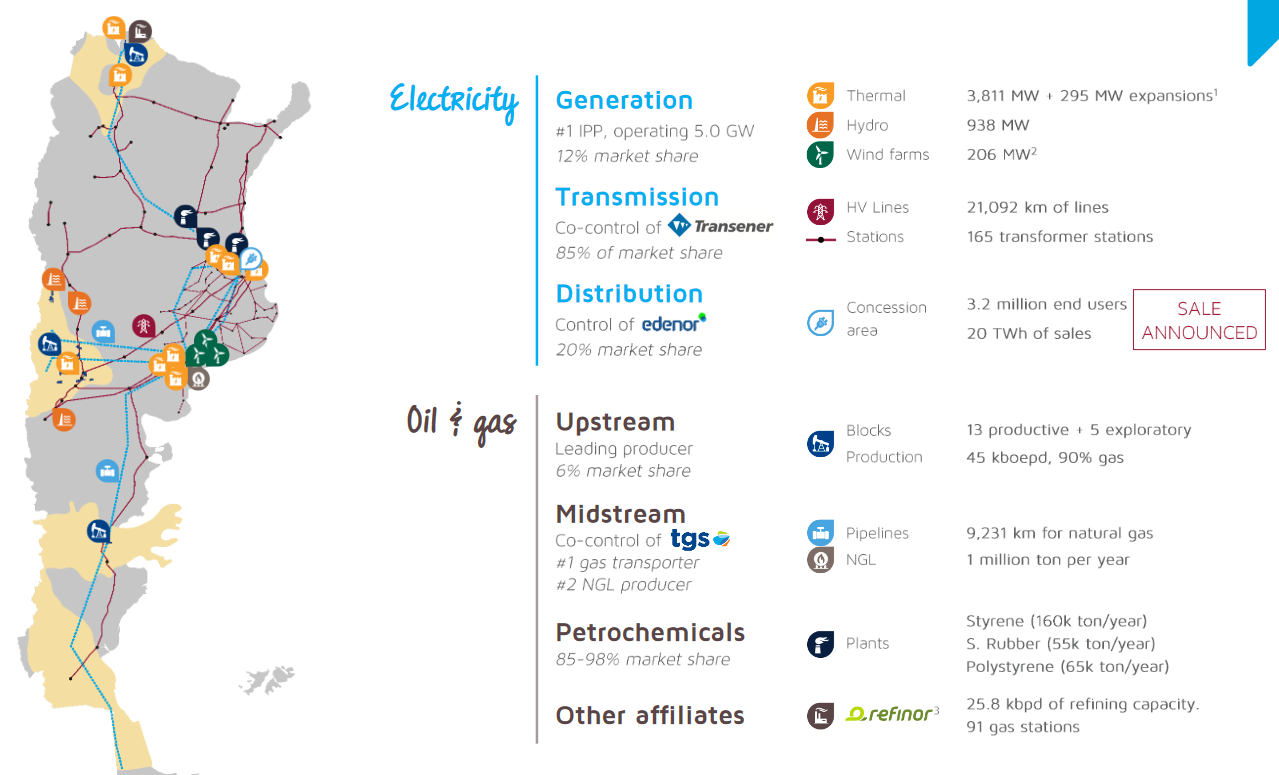

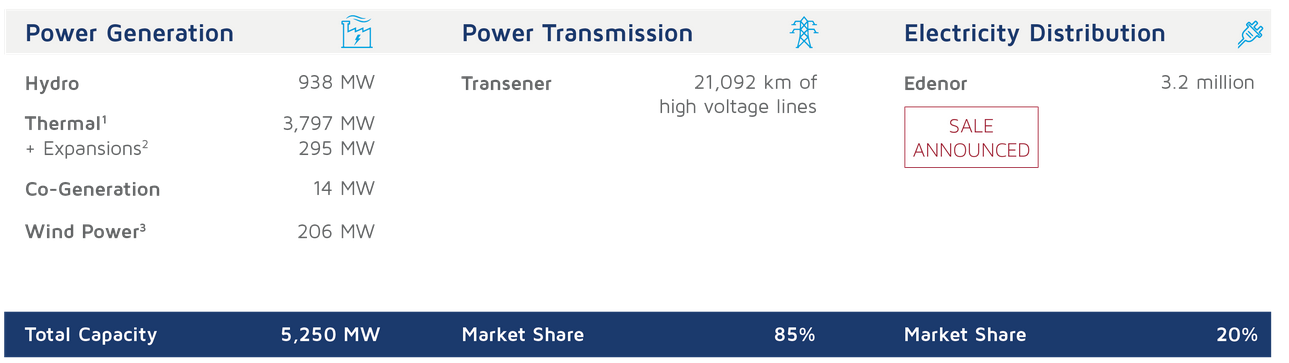

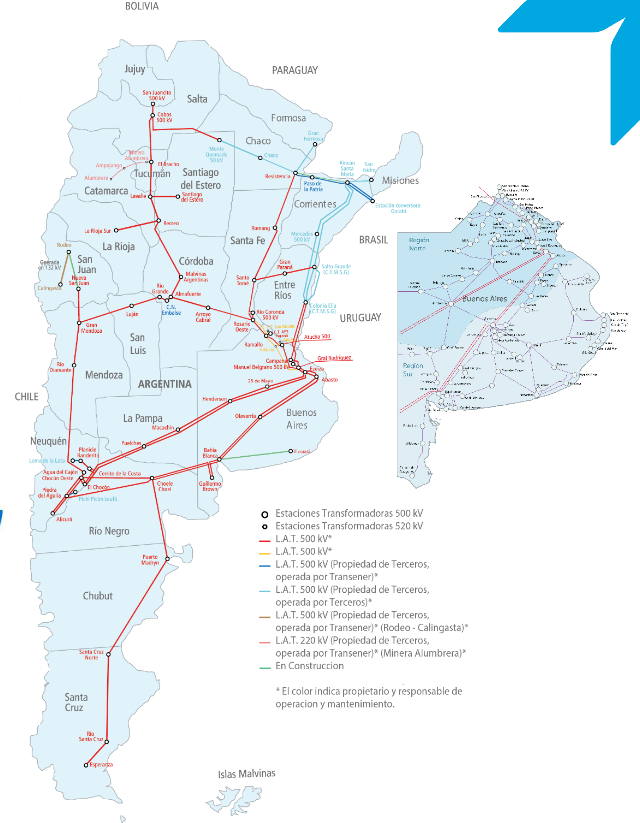

The Electric Division

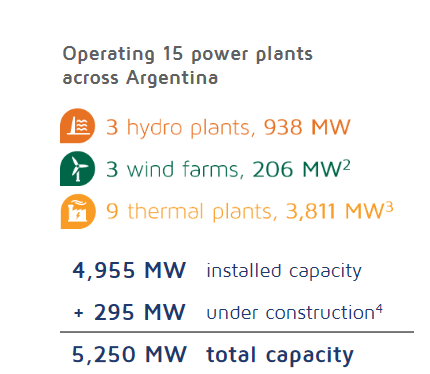

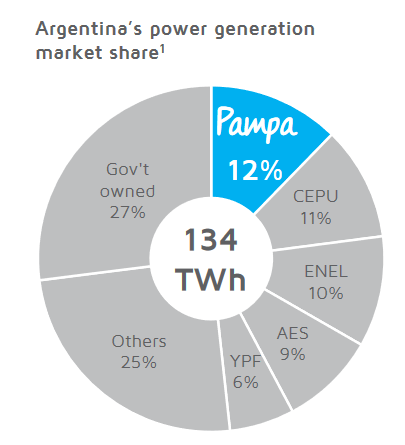

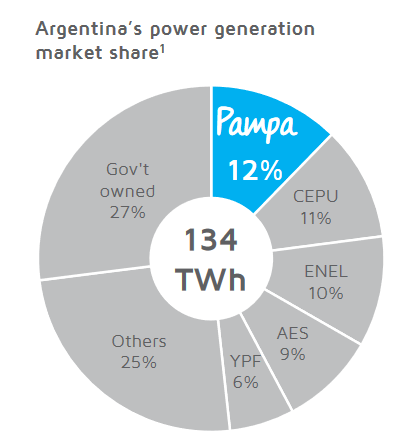

The company’s power plants are mostly located around the capital Buenos Aires and the north of the country. The large majority of the power produced comes from thermal power plants (3,811 MW), with also some hydro power in the Andes (938 MW) and some small wind farms around the capital. This represents 12% of the total country production.

Source: ri.pampaenergia.com

Source: ri.pampaenergia.com

Source: ri.pampaenergia.com

It is also active in transmission of this power, controlling no less than 80% of the Argentinian market. Until recently, the company was also involved in the distribution to the final consumers, but that activity is now being sold.

Source: ri.pampaenergia.com

The only 20% of market share of Edenor was the odd case, compared to the dominant position in power transmission, and was actually a source of losses. Pampa’s margin should strongly increase from having cut off that bad branch of the company. It came with a one-time impairment, but also allowed the company to now develop its profitable activity and let someone else struggle with the distribution. As a rule of thumb, I am happy to see the company focus on B2B, with electricity production and industry like gas, and stay away from the B2C consumer market of a country in crisis.

Source: ri.pampaenergia.com

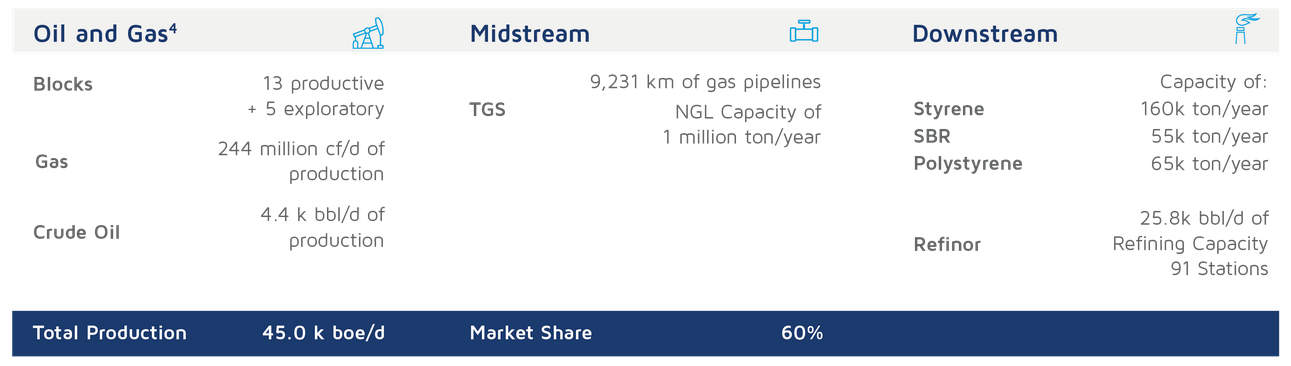

The hydrocarbonHydrocarbon Division

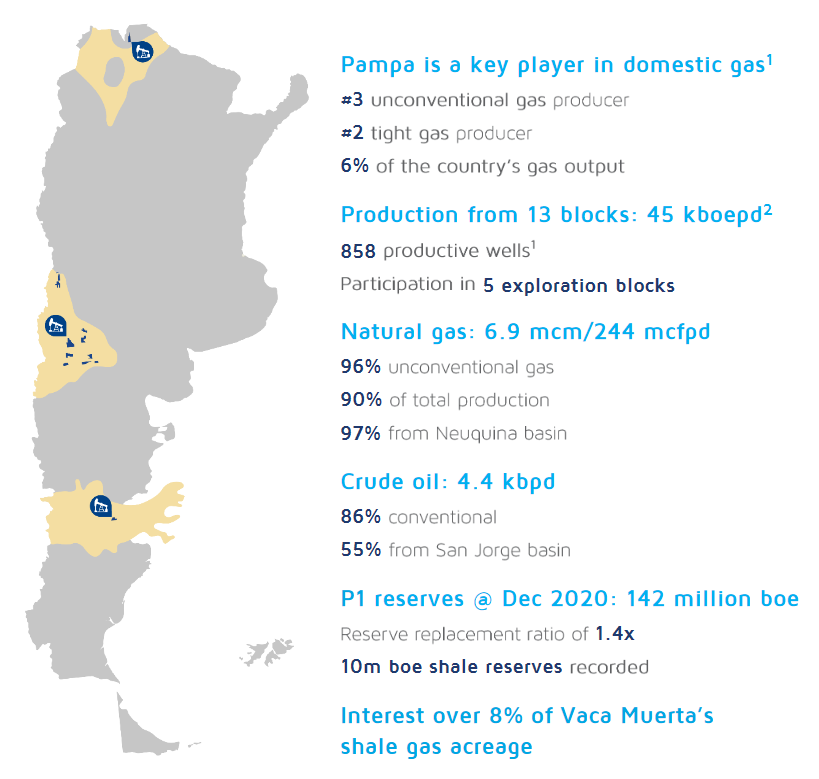

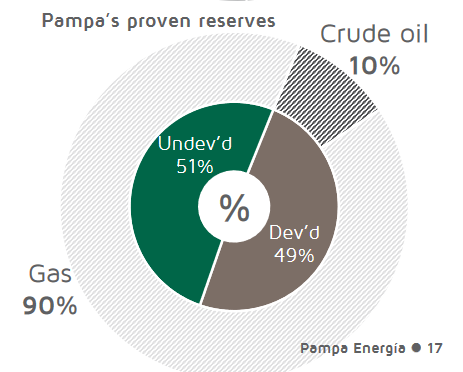

The other side of PAM activity is in hydrocarbons. It produces 45,000 barrels of oil equivalent (Boe) per day (Boe are a commonly used metric to measure the energy produced from both gas and oil to make the production volume of both form of hydrocarbon comparable). This is equal to 16.4 million Boe per year. The production is 90% gas and 10% oil.

It is also managing almost 10,000 km of pipeline, controlling 60% of the pipeline market of the country.

It also controls the production of plastic and chemical components like polystyrene and SBR. While not really significant in the company’s financials, it represents most of the country’s production of these materials (98% of the domestic market of polystyrene and 85% of SBR).

Finally, the company controls 28.5% interest in Refinor, the only refinery in the North of the country.

Source: ri.pampaenergia.com

The Vaca Muerta Potential

Due to its heavy gas portfolio, PAM is both a utility and an energy company. The Vaca Muerta (dead cow in Spanish) deposit has been one of the most controversial and disputed ongoing stories of the energy market the last few years. Geologically, it is a deposit very similar to the shale oil and gas deposits in the USA, responsible for major renaissance of US oil production in the last decade.

The Vaca Muerta is thought to be second largest major shale oil deposit in the world, and Argentina has been trying to replicate the American shale oil miracle for quite a while now.

With 10 million Boe reserve recorded, Pampa has 62 years of current production covered. In practice, I would not be surprised to see production double or triple, and PAM still having several decades worth of reserves in the ground.

Source: ri.pampaenergia.com

Source: ri.pampaenergia.com

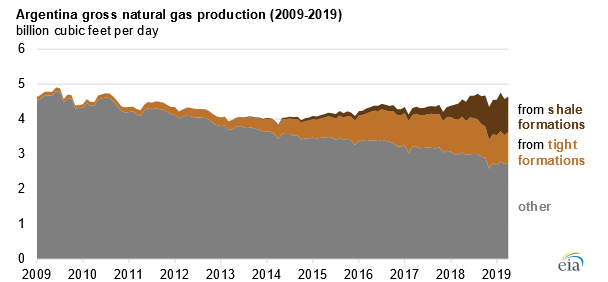

Obviously, becoming a major energy exporter would go a long way to stabilize Argentina’s ailing economy and currency. And it is already getting started, with shale and other unconventional hydrocarbon deposits having stabilized the previously declining production of Argentina.

Source: www.eia.gov

At the moment, Argentina’s production is mostly covering only parts of its domestic needs. The plan is to quickly expand the capacity, both in production and transportation to cover all the country needs and even start exporting it.

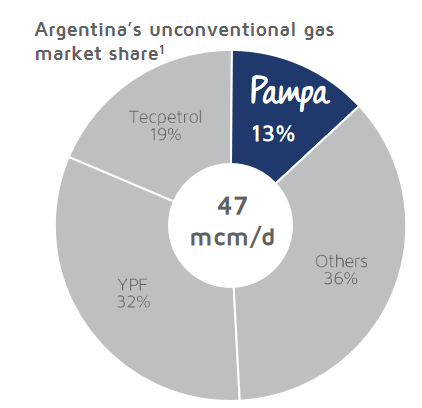

Pampa is producing 9% of Argentina’s gas and 8% of Vaca Muerta acreage, with concession, valid until the 2050s. Half of its reserves are still underdeveloped, giving a large potential for it to expand now that shale gas technologies have matured. So, while for now, Pampa is mostly producing to deliver the gas to its power plant, it could benefit greatly from the expansion of the Vaca Muerta.

Source: ri.pampaenergia.com

Source: ri.pampaenergia.com

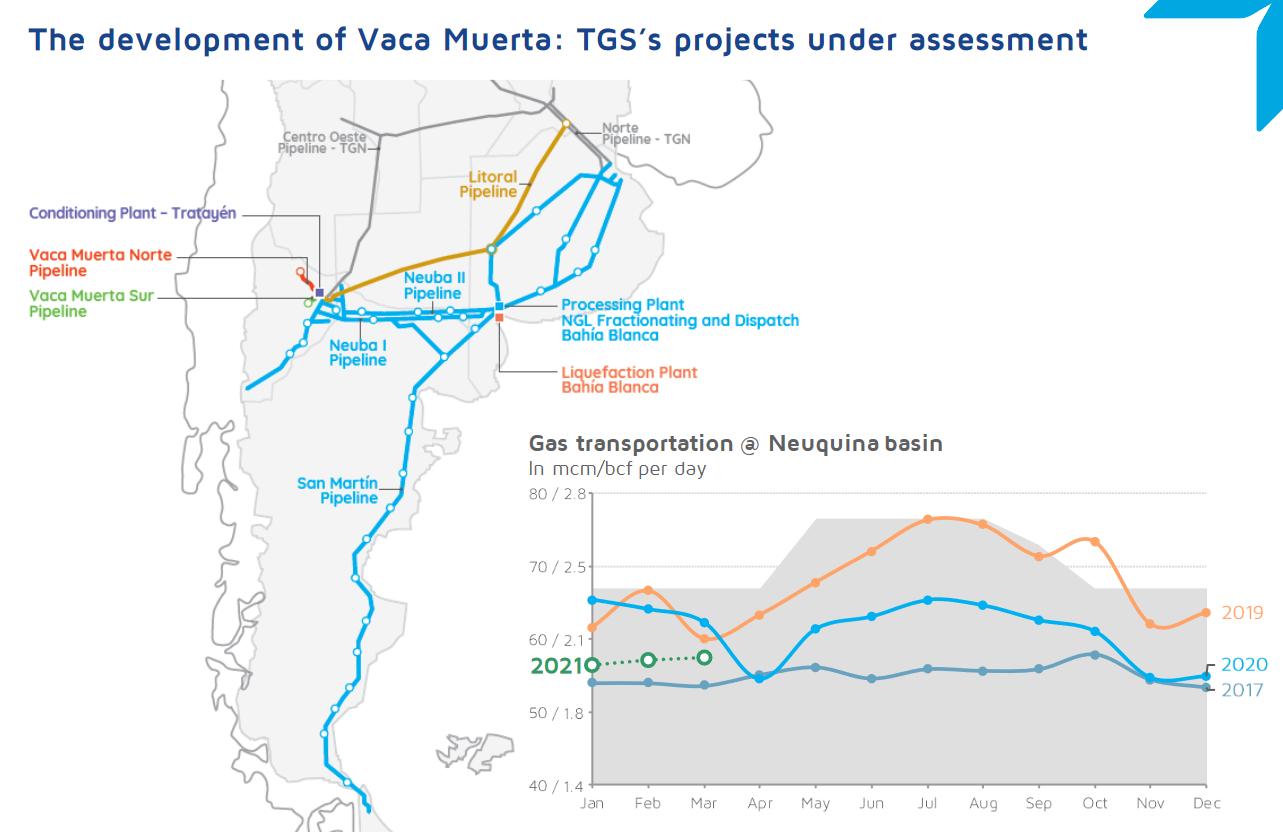

The future success of Vaca Muerta will be tied to the development of TGS’s new projects. They would allow to transport at low enough price the landlocked Vaca Muerta production for export and include pipeline and liquefaction plants.

Source: ri.pampaenergia.com

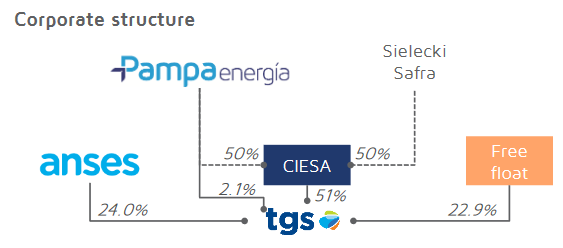

TGS is now fully owned by Pampa, but Pampa owned around a quarter of the company through a subsidiary called CIESA, co-owned 50/50 with Sielecki Safra, a major banking family of the country. The part called ANSES is basically the Argentinian government, owning another 24% of the company.

Source: ri.pampaenergia.com

Pipeline projects tend to be controversial (just look at the approved, then canceled, then re-approved, then re-canceled Keystone XL 2 in the USA). But considering how strategically vital is it for the country to develop its energy industry, the relatively low population density, and the direct participation of the government, I am reasonably confident that TGS’s projects will go ahead.

Maybe not as quick as possible, maybe even with serious delays, but Argentina establishment from all parties will benefit from its development. So, I can guess that it is likely to happen, and will represent a large potential for future growth, with Pampa controlling almost 1/10th of the whole Vaca Muerta resources.

The Corporate Structure

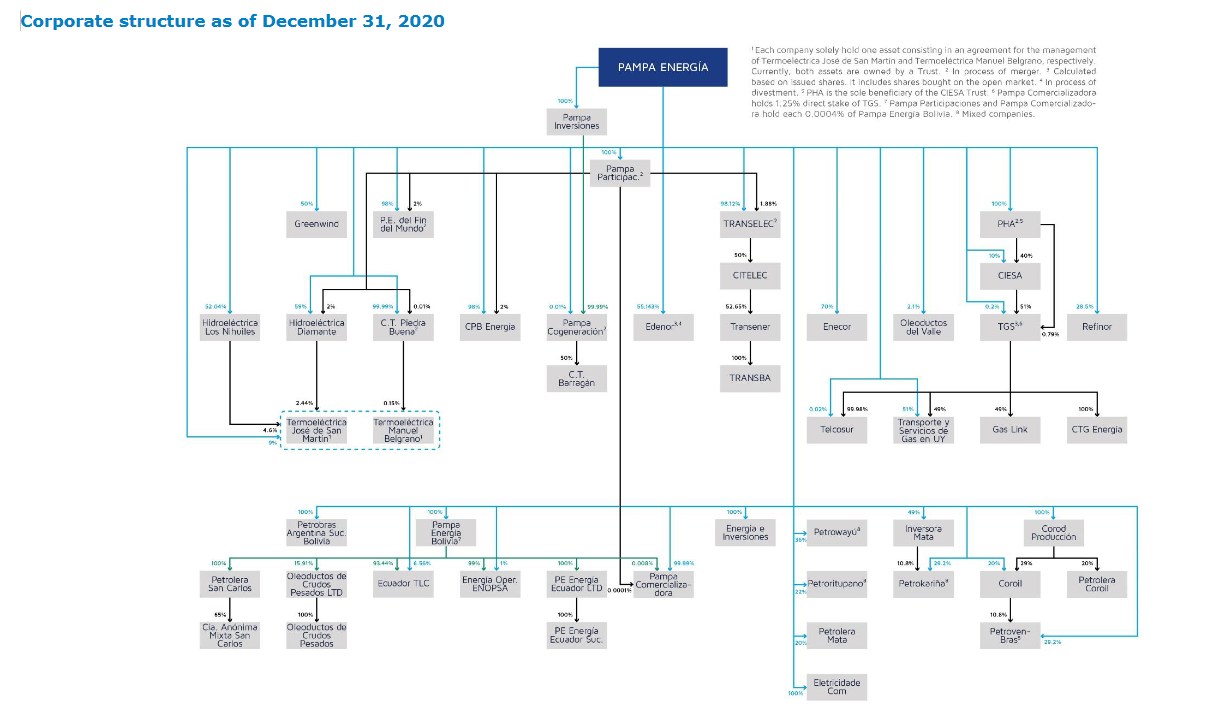

I need to make a confession here. Pampa’s corporate structure gave me a real headache. Like, enough to make me regret to have gotten an interest in the company in the first place.

The example above of TGS owned by Pampa through CIESA, but also a little bit directly is actually a simple case. Just look at the diagram below. Not really easy to interpret … actually it is unreadable without extreme zooming … And every name are acronyms or pretty obscure… I really cursed whoever in Pampa communication department left this without a few pages explanation.

Source: ri.pampaenergia.com

Luckily, after a deeper look, a lot of the various companies below are actually not that important, and just a few subsidiaries really move the needle for Pampa. Or they are 95-99% ownership on various holdings operating the individual power plants. But a few are worth mentioning with further detail.

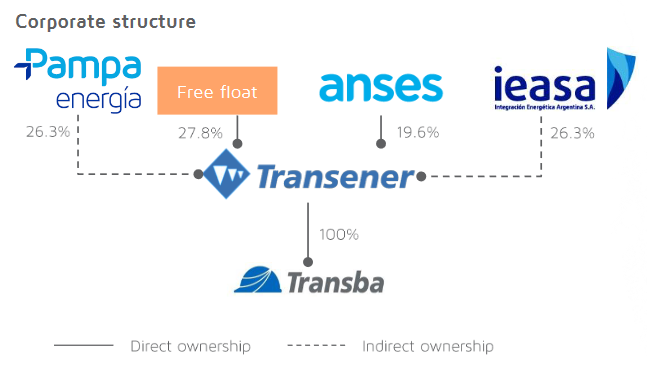

We already saw the participation in TGS, the largest pipeline operator in the country. The other major company co-owned by PAM, together with government structure and some free float is Transener, the main electric grid company. PAM owns 26.3% of Transener.

Source: ri.pampaenergia.com

Transener manages 21,000 km of High voltage electricity line, or 85% of the market. So, through Transener, it is not an exaggeration to say that PAM is the Argentinian electric grid, co-controlling it with the government agencies.

Source: ri.pampaenergia.com

Qualitative Analysis

Business Analysis

Electricity Production

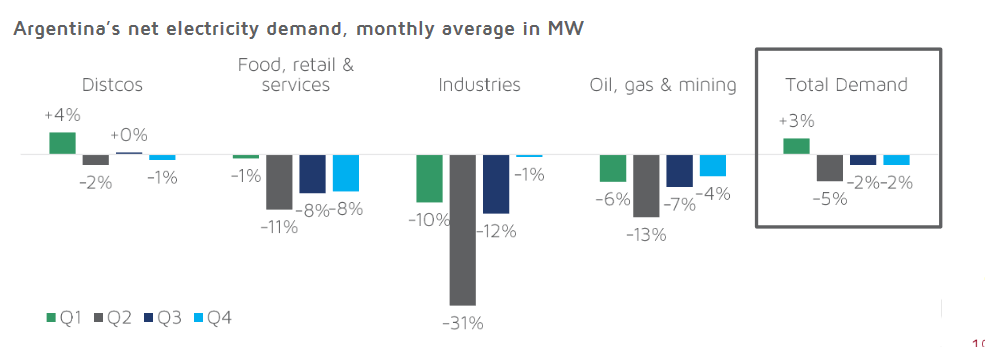

2020 was the year of COVID, and Argentina was not spared. But total electricity demand was barely affected, as residential demand going up compensated for the retail and industry reduction.

Source: ri.pampaenergia.com

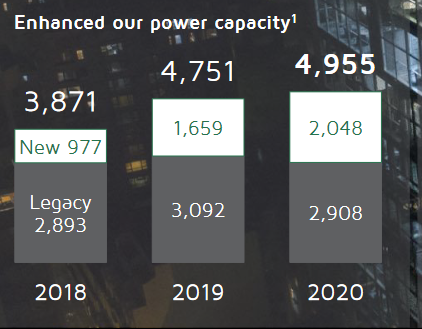

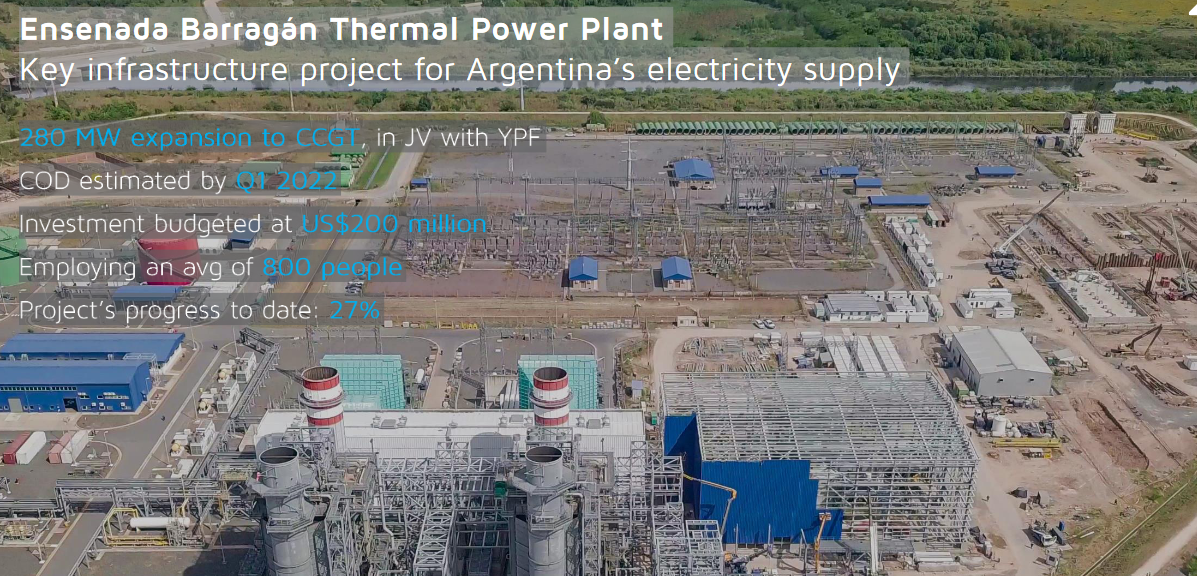

Pam has strongly increased its power generation capacity over the last 2 years. Another 680 MW are already getting built, with a price under budget so far.

Source: ri.pampaenergia.com

Source: ri.pampaenergia.com

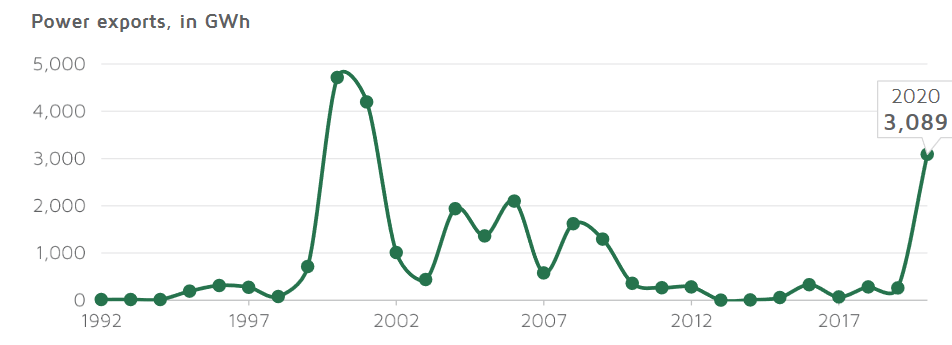

Electricity exports have also been growing strongly in 2020, mostly to neighboring Chile.

Source: ri.pampaenergia.com

The Issue of Electricity Pricing

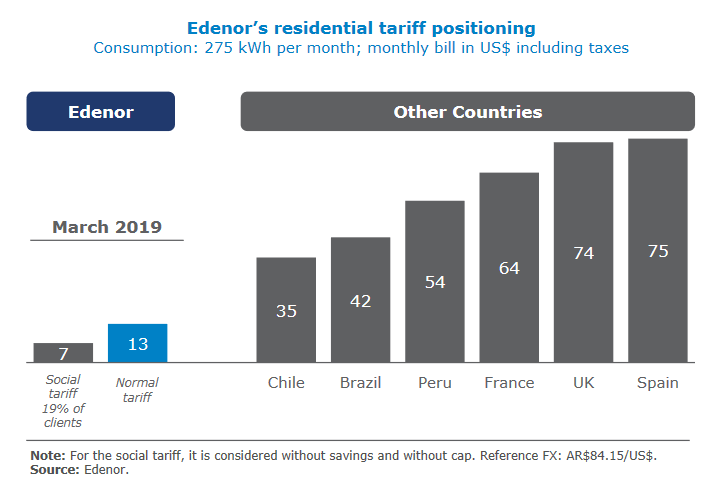

One significant issue with Pampa electricity production is its very low sale price. Due to the economic crisis in the country, when measured in USD, (the regulated tariff for electricity) the social tariff or normal tariff is very low, even compared to neighboring Chile or Brazil.

This explains partly why the company was so eager to grow its exports (also getting hard currency in the process), with Chile happy to use the depressed conversion rate to get cheap electricity.

Source: ri.pampaenergia.com

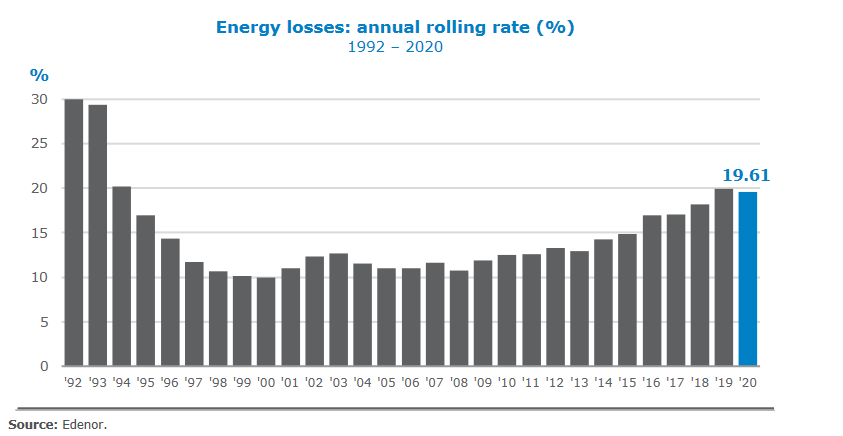

Another problem is a high and growing amount of energy losses. In practice, these are not “lost” but stolen. The poor economic conditions have encouraged a lot of people to “pirate” the grid, more or less safely, to get free electricity.

Source: ri.pampaenergia.com

Both low prices mandated by law to keep the light on in the impoverished country, and poor law enforcement regarding stealing power are to be expected in a country suffering massive economic upheaval.

Will the situation get better? I would not really count on it. Argentinian people are unfortunately likely to stay poor for the years to come, and political dysfunction at the heart of the Argentinian issues are unlikely to get solved overnight.

But will it get worse? Argentina is actually likely to be heading for brighter days. Its main production and export, food commodities (especially beef), are going up in price quickly, and growing energy exports should help to at least stabilize the situation. So, I would say these problems are already reflected in PAM revenue and earnings and should not bring a bad surprise.

Vaca Muerta Production Bright Future

You would not be able to tell for the share price, but Pampa is heading great growth, at least in regards to its hydrocarbon production. The steady production of the last year should make way for strong growth, and the petrochemical business is doing just fine after much needed upgrades.

Source: ri.pampaenergia.com

This is perfectly consistent with the incredible volume of reserves the company owns. As soon as the pipeline transportation and liquefaction facilities question will be solved, Argentina will likely become a powerhouse in LNG, and Pampa with it.

With a lot of the world switching from coal and oil to gas to reduce its carbon footprint, I expect the world’s appetite for LNG to keep growing, and Argentina will be at the forefront of it (together with Russia, Qatar and the USA).

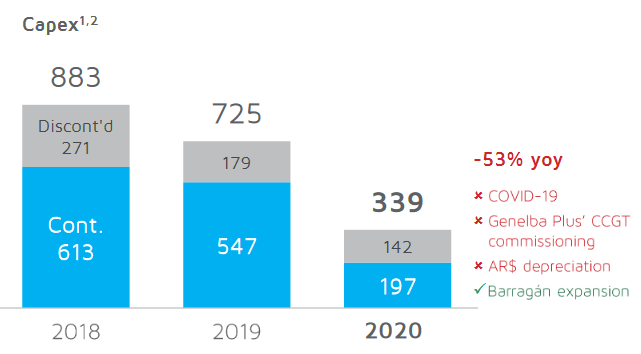

CAPEX

Capex in 2020 has decreased significantly, due to construction frozen by COVID restrictions. On top of that, the Genelba + commissioning means that their largest project had just ended. Another reason for the very sharp decline in capex is that even if constant in pesos, the currency devaluation makes it seem larger than it actually is.

Capex will be something to keep an eye on for PAM shareholders, to be sure the company keeps investing into its assets properly. However, previous years Capex seemed adequate, and the combination of COVID delays + brutal devaluation seems to me more responsible for the odd case of 2020 than consistent under investments.

Economic Moats

Similar to Copel, Pampa is very rich in economic moats, as any good utility company should be.

Unique Assets Hard or Impossible to Replicate

PAM’s part in the Argentinian electric grid is something that took the best of two decades to build, and represents a massive capital investment. Some newcomers might use the current crisis to buy assets cheaply, but this would not constitute a radical change for PAM, just a change in the name of its competitors.

Besides, its local knowledge and expertise allowed it to grab almost 1/10th of the acreage of the second largest shale oil deposit in the world, with concessions running for 30+ years. One of the failures of the shale oil patch in the US was an excessive fragmentation of the acreage, increasing costs and making impossible any production discipline. Vaca Muerta, controlled by a few key actors from the beginning, should be able to avoid this risk.

Regulatory and Regional Monopoly

The co-ownership of TGS and Transener with the state agencies, as well as a long-established operation in the country implies a good knowledge of the inner workings of Argentinian politics and regulatory environment. In a country known for persistent levels of governmental inefficiency and corruption, this is actually an asset that only a few companies in the country can claim to have.

Management

With a company operating in such an economically troubled country, with weak rule of law, I absolutely needed to see that the management’s interests are aligned with the shareholders’. Else, it would simply be too risky to be exposed to frauds.

Source: ri.pampaenergia.com

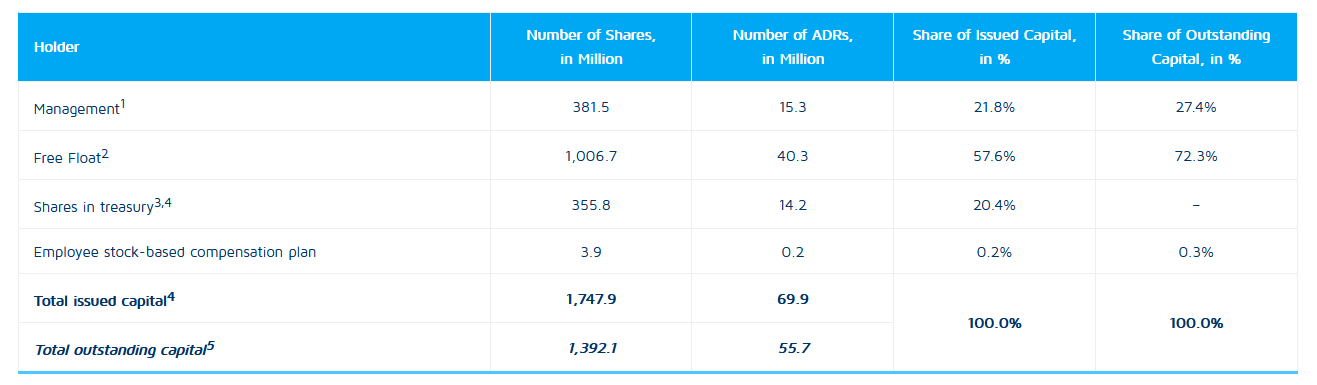

With more than a quarter of PAM shares (27.4%) owned by the management, the company passes this test with stellar results. I am sure the company management is not happy of the recent share price performance and will do everything in their power to correct it.

At the same time, management seems to judge that the price is too low, as they are actively repurchasing shares with the company cash. They even say it outright in the annual report:

“Given the difference between the value of Pampa Group’s assets and the quoted market price, the buyback of own shares and bonds continued in 2020by efficiently applying liquidity.

The market price does not reflect either the value or economic reality they currently hold nor its upside potential, resulting in detriment to shareholders and bondholders’ interests.”

The maximum price set for share repurchase is $15 and $16 USD, reflecting the management’s intention to use the low current price, but also to not overpay. It should both put a minimum low to PAM share price, but also reflect the good quality of capital allocation pursued by the management team.

Marcos Marcelo Mindlin, Chairman

Mr. Mindlin is a key actor in the Argentinian financial elite, having been a board member of some other major Argentinian companies, through his ownership of Grupo EMES, like real estate giants IRSA and Cresud or the leading mortgage bank, Banco Hipotecario.

While investigating the profile of Mr Mindlin, I found a very interesting interview from 2011, where he said:

“Our debt purchase was possible because we had plenty of liquidity when the crisis erupted – we were prepared. The key to our business strategy is to always have liquidity to take advantage of opportunities as they arise.

A crisis like the current one does not occur frequently. But we were able to move quickly to take advantage of the situation because we had high liquidity levels and a financially solid business.”

This is the kind of long-term thinking about economic cycle that is needed to navigate the tumultuous waters of South American economies, and it seems that Mr. Mindlin is a hidden valuable asset of the company not displayed on the balance sheet.

Gustavo Mariani, CEO

Also a shareholder and Director of Grupo EMES, he is a graduate of Finance and a CFA. Interestingly, he joined Grupo EMES in 1993 as an analyst, and never left. Together with Mr. Mindlin, I think he is the brain behind Pampa’s capital allocation strategy.

Horacio Jorge Tomás Turri, Executive Director of Oil and Gas

An industrial engineer, he is the former CEO of a power company. Before that, he was an investment analyst for oil & gas for SAFEIC, then Arthur Andersen & Co. And then Schlumberger (top oil service company). Considering how crucial the developing of Vaca Muerta gas resources is to the future of Pampa, he seems like the right man with the right profile and connections to know which acreages to develop and which to not waste money on.

Competition

Pampa is the largest privately operated electricity producer in Argentina. Thanks to the growing abundance of gas resources in Argentina and how it holds the key to its economic recovery, I do not expect the country to turn hostile on fossil fuel in the next decade, contrary to many other places.

Due to the highly regulated (even more so in a country with strong social policies) and capital-intensive nature of the electricity market, competition is very low, each actor happy to enjoy an oligopoly.

The only threat I can imagine is not so much from competitors but from the government itself, who might decide to nationalize, or to force even lower electricity prices. If that did not happen in the middle of a major crisis, I do not think it is very likely, but this is always a possibility. This is something I will discuss further when it comes to the investing strategy for both Pampa and Copel.

Quantitative Analysis

Financials

Revenues

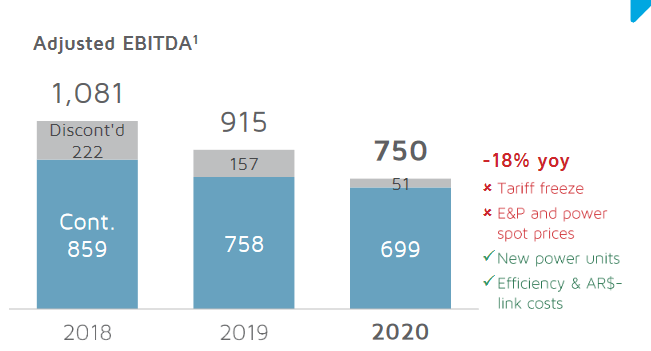

Measured in USD, revenues have drastically contracted in 2020, mostly due to tariff freeze, crash in energy price (remember that in the US, oil price was briefly negative in 2020) and low power spot price. Another factor is that the revenues (made in pesos) are here converted in USD, with the pesos loosing a lot of value compared to the dollar. So even stable pesos revenues would have been declining in dollar terms. The smaller decline in 2019 was similarly the result of the pesos decline compare to the USD.

The EBITDA have also strongly contracted, but a little less, due to increased efficiencies in the company’s operations. Overall, the revenue decline reflected the current Argentinian economic crisis, as well as tough negotiations with the country’s government regarding electricity prices.

So, 2020 was somewhat the perfect storm for Pampa, the country was already deep into an economic and monetary crisis, before the arrival of COVID. The worldwide crash in fuel consumption depressed the value of the gas produced, while electricity prices were under pressure from government negotiations and impoverished customers.

These are the kind of conditions when the solidity of a company will be exposed. Despite all that, PAM did turn a profit in electricity generation, petrochemical, and its subsidiaries. The oil and gas turned out with a small loss. If that would have been all, the company would actually have managed to turn a profit.

But then, the electricity distribution registered one final large loss, completely sinking the whole company’s yearly profit.

The good news is the distribution business has been sold (at a loss) once and for all. Such exceptional losses are not going to happen again. The rotten part has been surgically removed, and the healthy part of the company can now recover and strive. At least as long as the debt burden is manageable, which we will discuss just below.

Dividends

Pampa still has a large debt burden and made clear that no dividends are planned for the foreseeable future. All available cashflow will be dedicated to deleveraging and maintaining high levels of investment in new power generation and developing the Vaca Muerte (both gas production and pipelines to get it to the sea).

Debt and Balance Sheet

It is quite common for utilities companies to carry a large debt load, as their assets are productive for decades, and will be amortized over a long period.

The debt of the company is standing at $1.6 billion USD, with $466 million in cash. This brings the net leverage (net debt to EBIDTA) at 2.4x. Not really great, but not terrible either for a utility/energy company.

One bad part is that most of the debt is in USD, meaning that compared to revenue in pesos, the debt could quickly snowball out of control compared to the cash flow of the company, which are in pesos.

The reimbursement calendar is having a large 186 million pesos reimbursement in 2021, followed by USD debt in 2023, 2027 and 2029. Most of the interest on this debt is in the 7-9% range.

So now the question is, can PAM manage this debt load? Mostly, if the situation in Argentina stabilizes, yes. Especially if oil & gas prices stay in the much higher $60-$70 USD/barrel we have seen in 2021 so far.

I am somewhat inclined to believe the worst is behind regarding Argentina. Money printing by the major economies following COVID have unleashed inflation on virtually all commodities, be it lumber, beef, corn, soybeans or copper. This should strongly help Argentina to get back on track. The country went through regular crises, and they tend to play out similarly each time. After a nasty 60-80% crash, its stock market tends to recover and the economy to stabilize.

Alternatively, if the pesos crashes even more and Argentina goes into an even nastier inflation or hyperinflation, revenues in worthless pesos might not be enough to cover the debt repayment of Pampa.

So, there is definitely a risk. It’s up to you to see if you would be willing to roll the dice on this.

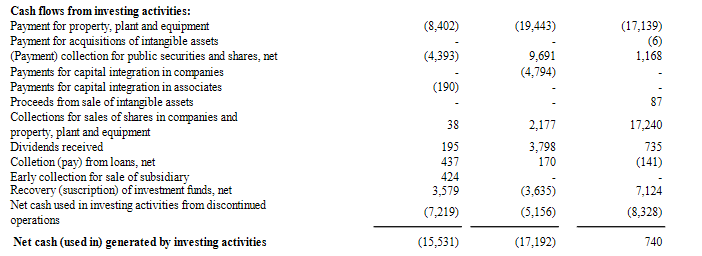

Cash Flow

But at least, could PAM manage its debt and acquire investment if the situation stays stable? This we can judge from the cashflow statement. It is more relevant than revenue or income, which have been severely impacted by the underperformance of the distribution department, now finally sold away. I will look at each segment of the cashflow statement separately, starting from the operation cash flow.

2020 has been such an abnormal year, that I will compare the 2020 cash flows to 2019, in order to estimate what should have been the cash flow.

2020’s operating cash flow were quite a mess. The profit from operation declined, but a very large “adjustment” seems to compensate for that. The discontinued activity (electricity distribution) muddies the water even more.

Investing activities were reduced in spending on plants and equipment, but we already knew that from capex. If 2020 had been a normal year, without construction work being suspended by COVID, something of 15 +11 billion pesos would have been spent on property, plants and equipment activities, and I will use that as the estimate of a normal capex to be expected in 2021.

Financing activities were dominated by 3 larges items, proceeds from loans, repayment of loans and interest on loans, reflecting the still large debt of Pampa. 20 billion pesos were reimbursed in 2020 but 25 borrowed.

Purchases of own shares, and redemption of corporate bonds also account for 13 billion pesos.

The reimbursement of interest jumping from 5 billion pesos to 12 billion, reflecting the crash of the currency, as the company has to reimburse in dollars, not pesos.

Discontinued operations were also somewhat impactful.

So, what can we say about the cashflow for 2020? And can we have a picture of possible cash flow for 2021?

The discontinued department of electricity distribution will really be over this year, so can be finally ignored.

Cash flow from operations were exceptionally poor, but that is not surprising considering how bad 2020 was. If 2021 goes back to even a semblance of normalcy, we can expect a return to the 2019 levels (crisis in Argentina, but no sudden and unexpected pandemic). A 25-30 billion pesos could be reasonable from operating activities.

Investing activities at 15-20 billion, mostly in plants and equipment, can be expected, and should support growth in electricity and gas production, and help boost operating cash flow for 2022.

While not in perfect conditions by far, Pampa has been able to refinance its debt in 2020, in the heart of the storm. I think this should also hold true for 2021 with COVID slowly receding and commodities prices, especially energy, recovering. So, we should see again a 12 billion in interest paid. And both old and new borrowing canceling each other out. Considering low stock price, it might make sense to persist with the current levels of 7 billion of share purchase too.

20212022Operating cash flows+25 billion+30 billionInvesting cash flows-15 billion-15 billionFinancing cash flows-12 billion interest

-7 billion share repurchase

-12 billion interest

-7 billion share repurchase

TOTAL– 9 billion pesos-5 billion pesos

Overall, PAM cash flows should be high enough to pay interest, maintain investment at high levels to support growth and keep rolling over the debt. The only thing that would push cash flow to negative is share repurchases.

So, while not great, due to the large USD debt overhang, PAM’s situation is not as dismal as its current valuation would let you think. As long as it just maintains itself where it is, it can keep growing and investing into its future, to the point where the Vaca Muerta assets turn from dead cow to a cash cow.

A lot of the future cash flow of Pampa depends on the successful development of the Vaca Muerta. If the gas never makes it into a major export, the company is likely to struggle for years under the debt load.

If the investments in the deposit pay off, the extra cash flow will improve the situation of the Argentinian pesos, both strongly reducing Pampa’s debt load in USD and increasing massively its free cash flow.

Categorization and Valuation

Investment Category

Pampa is both a rather typical utilities (lots of moats) and a deep value play. The reason is that despite solid moats and assets, it is operating in the very unstable Argentinian economy. In many ways, the future of Pampa and of the Argentinian pesos are identical. Both depend heavily on global inflation to increase the price of commodities.

If international LNG price goes up, so goes the profit of Pampa and the pesos. With the pesos constant fall in value stopping, Pampa’s debt load gets also easier to manage, increasing even more the company’s cash flow.

Therefore, Pampa’s returns are more likely to come from a turnaround of market perception. From a struggling utility in a struggling country, to one of the main actors in the newest, greatest energy play on Earth in a quickly recovering emerging economy.

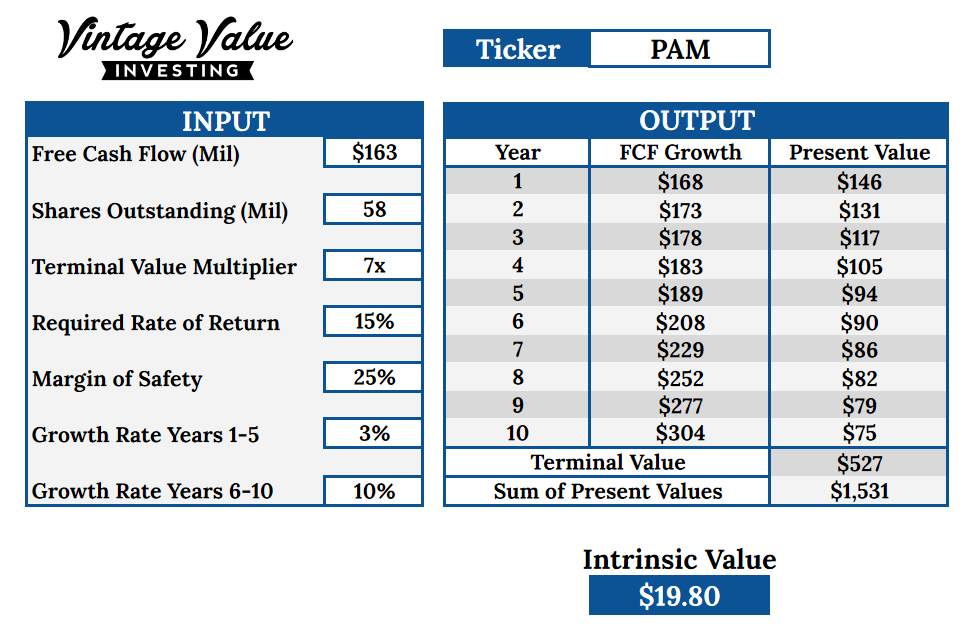

Discounted Cash Flow

One way to calculate Pampa’s valuation is using the discounted cashflow model. You can see what it means and how it works here.

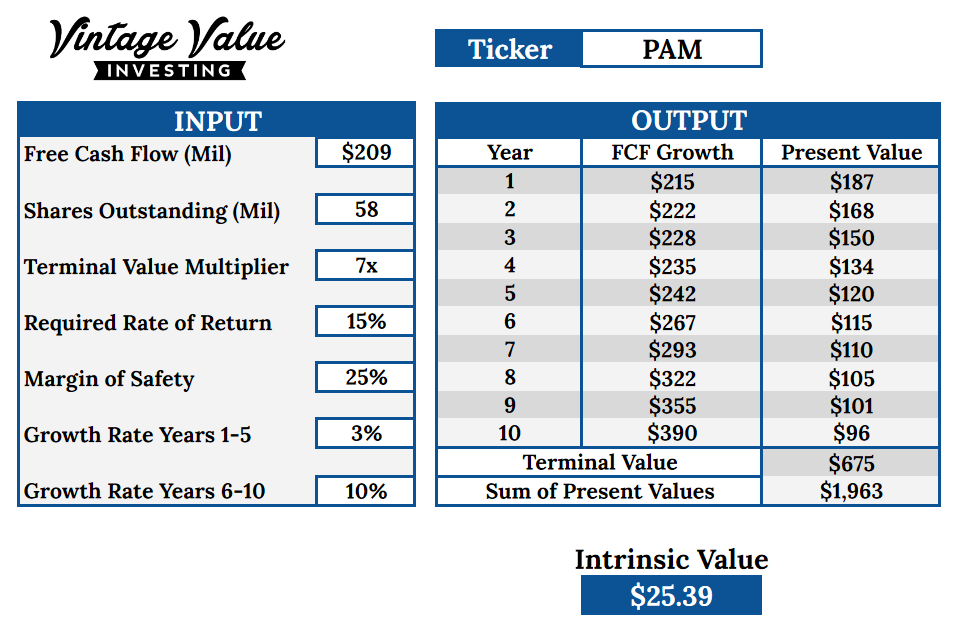

I again will use the free cash flow simplified formula of free cash flow = Operating cash flow – Capex. This involves some level of uncertainty, as capex was unstable in 2020, and also incorporated the capex of the discontinued distribution operation.

So, I will run the calculations with 2 set of variables for free cash flow:

- Taking the numbers of 2020 at face value.

- Taking into account only the cash flow from continued operation

In the first case, operating cash flow was 51 billion pesos, or $548 million USD.

This gives a free cash flow of 548 – 339 = $209 million USD.

In the second case, the operation cash flow is 34 billion pesos (51-17 billion pesos) or 360 million USD. Capex is 197.

In total, free cash flow is 360 – 197= 163 million USD

For terminal value multiplier I will use a very conservative 7. This is rather low for a utility business with large energy assets to be developed, but would reflect persistent pessimism about Argentina as a whole.

I considered a low 3% growth rate for the next 5 years, reflecting the still struggling economy and the time required to ramp up the Vaca Muerta operations. A much higher growth rate of 10% for the 5 years after reflecting the growth in production is shale gas and Argentina’s (temporary?) recovery.

Margin of safety is set at the very high 25%, reflecting the large uncertainties about the future of Argentina and Pampa.

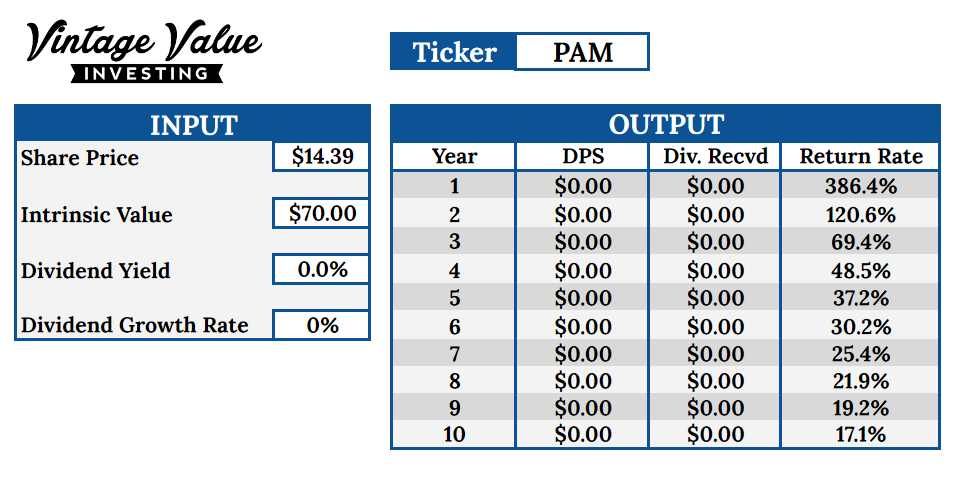

This would give us an intrinsic value of $25.39 USD, much higher than the current price.

I will not look at the vale without margin of safety, as but I am pretty sure a large margin of safety is required when it comes to anything Argentina related.

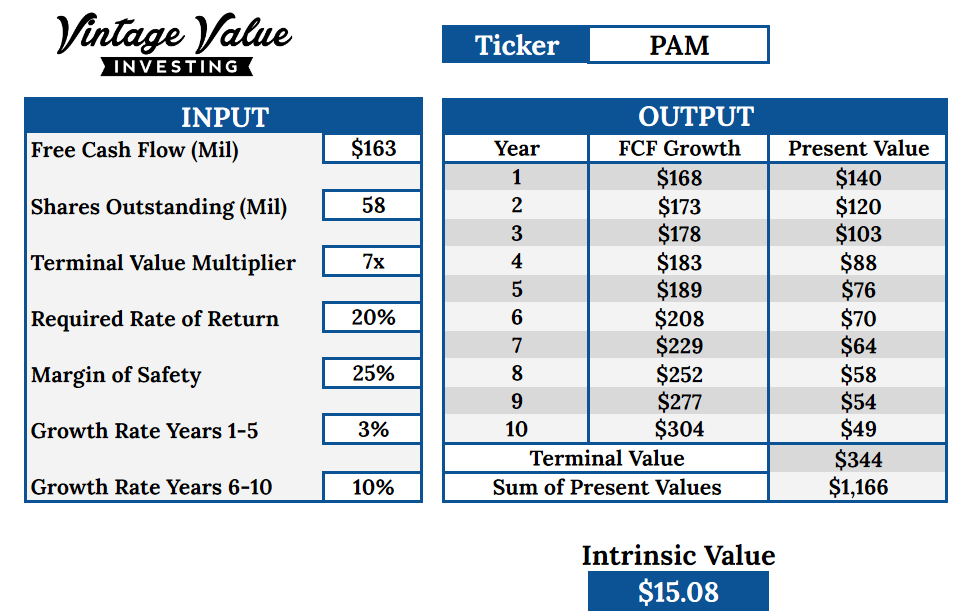

With the second, lower estimate of free cash flow, intrinsic value would be at almost $20, still much higher than the current price.

In practice this means that the current price, even with the smaller cashflow, would support a return of 20%.

Overall, Pampa seems able to sustain a return rate of 15-20% if the situation stabilizes and Vaca Muerta becomes a major actor in the gas market in the next 10 years.

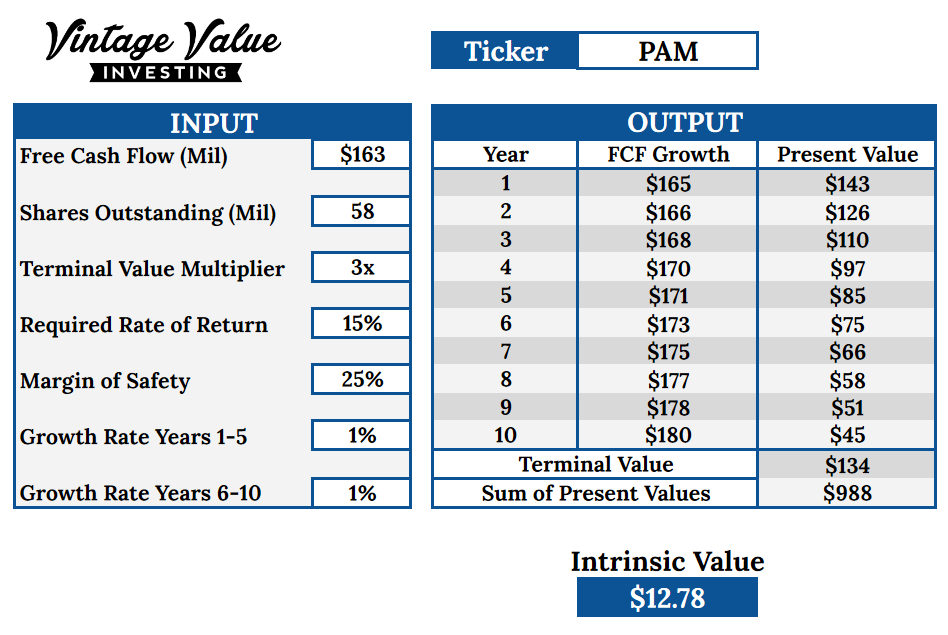

But I wanted to see what would happen if Vaca Muerta do not turn out so well. So I also did a calculation with a negative scenario. The lower cash flow estimate, and much lower terminal value multiplier and almost no growth.

t $12, this is not much below the current price. Maybe this is not that surprising, as markets have been pricing the company for failure and totally ignored the Vaca Muerta potential.

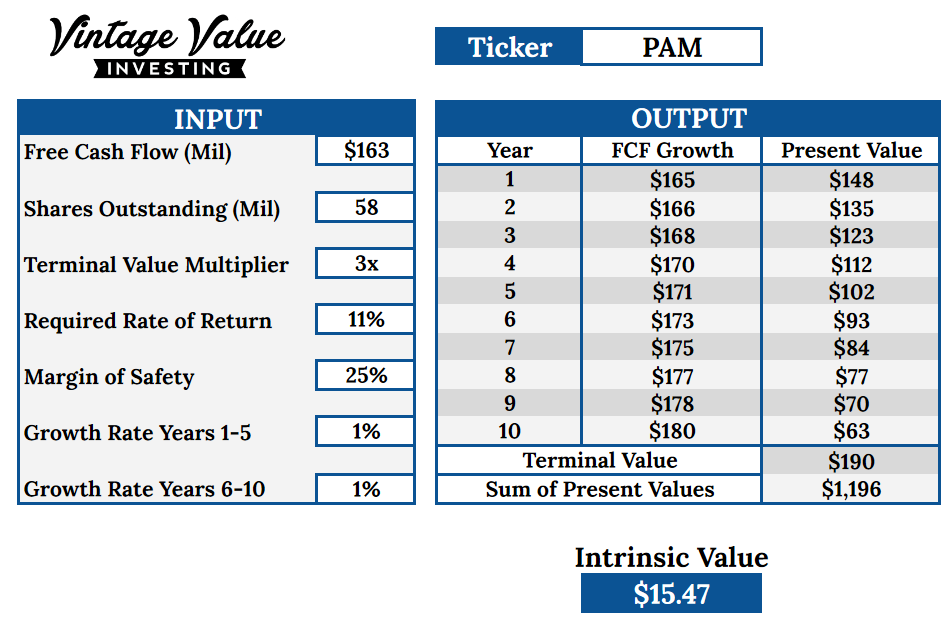

But her eis the funny thing. With terminal value multiplier of just 3 and no growth, Pampa should still provide 11% returns.

Ultimately, according to cash flow calculation, Pampa should provide a minimum of 11%. Awesome right? But I must add an extra warning here. All these calculations are only valid if the company can keep operating normally. This mean no total destruction of the Argentinian peso in hyperinflation, something happening regularly in Argentina.

If this would happen, the USD-denominated debt of Pampa would be become unbearable, and the company could go bankrupt. So basically, Pampa should provide awesome returns, as long as it does not die. While this can be said for almost any investment, this is a real, always present risk here, to not forget.

Deep Value Valuation

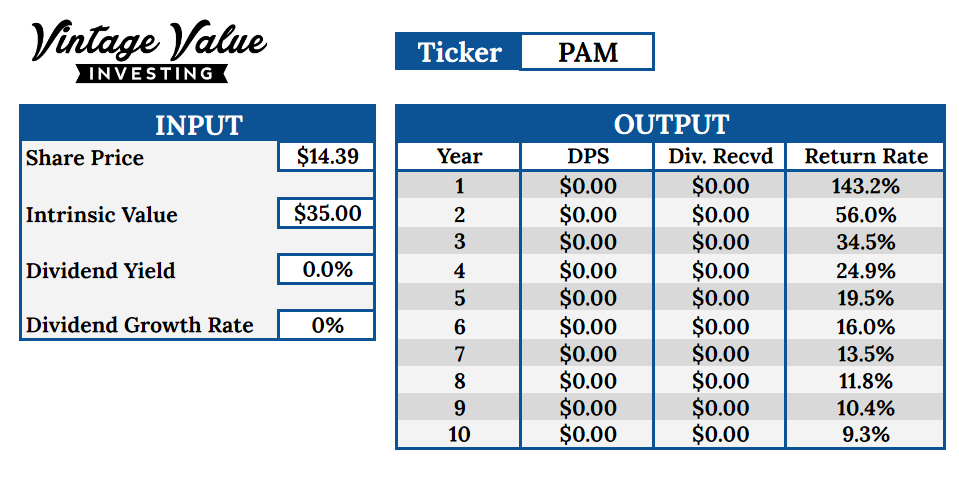

With a company in a deep crisis, it is hard to judge what the real price should be once the crisis passed. I decided to simply use the price the company used to be valuated at in 2017. This might be a bit crude, but basically represent the scenario of a return to normal, without counting any growth at Vaca Muerta. I also considered no dividend ever again in the future.

According to the deep value calculation, if Pampa take as long as 10 years to recover to its former stock price, returns would still be at 17%. If this happen in just 6 years, annualized returns would be 30%!

Actually, if the company recover only half of its former in the next 6 years, annualized returns would still be at 16%. Not bad…

Other Calculation Methods

I considered using the Earning Growth model, but with earnings negative in 2020 and very unstable before that, I do not think it really makes much sense to use this method.

The absence of any dividend payments now or in the foreseeable future also forgoes other valuation methods, like Equity bond or Yield on cost. So, for once, I will have to rely solely on Discounted Free Cash Flow.

Partial Conclusion

Pampa is at the moment priced for a permanent struggle to keep the head out of its debt and the general Argentinian economic debacle. But prices are now so low that a reasonable case can be made for 15-20% returns. This expectation has however a large level of risk, both upward and downward.

The main downward risk is a complete collapse of the pesos, meaning that most of Pampa’s pesos-denominated revenues are useless to reimburse the USD-denominated debt. This most likely would involve some kind of default or freezing of the debt, until Argentina gets (again) a new currency. This is unfortunately out of Pampa’s hands, and considering Argentina’s economic history, a very real risk.

So there is a chance of Pampa going to zero, following the peso. How high is this risk is anybody’s guess, but it for sure exist, and might be as high as 20-30%. So remember it before getting too greedy here.

The upside chances are also strong. If oil prices (to which gas prices are strongly correlated) surge into the upper $80-$100 range, the Vaca Muerta will become highly profitable (production costs are estimated from $30-$50 USD depending of the sources). This would turn Pampa into a large export-driven energy company, while at the same time boosting the Pesos, making Pampa’s debt a minor problem.

In a way, I suspect that the 15% estimate is probably wrong. Without high commodities and energy price, Argentina’s prospects are rather gloomy and losses might be totals. And with high commodities and energy price, its future is really rosy and 25-30% is not impossible.

So even if this a bit uncomfortable for most value investors, a strong opinion about macro-economic (especially regarding commodities inflation) will be needed to decide if Pampa is a good or a bad investment. And this is very much an investment where it either go really well, or go really wrong, with not much in the middle.

Final Assessment

Brazil Versus Argentina

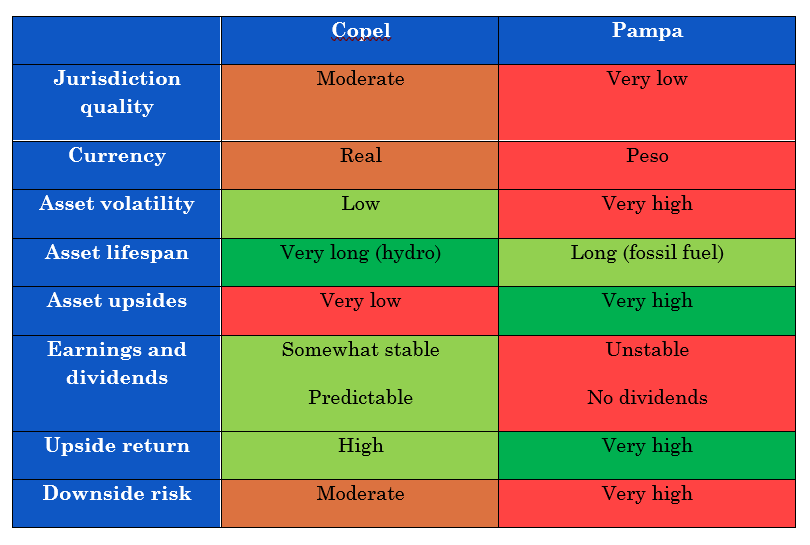

Both Copel and Pampa, being regional utilities, will be dependent on the economic future of the country in which they operate.

Personally, I expect the more resilient and diversified Brazil be less risky. It will experience volatility, but does not seem to be heading for major cataclysmic events, just some typical occasional emerging market struggles. The only risk is the currency risk, which I will discuss in the next paragraph below.

Argentina is a completely different case. This is a country famous for regular and spectacular economic and monetary collapses. It is also a country famous for spectacular and quick recoveries surprising the markets. So timing is the crucial point here. Did the ongoing Argentinian crash hit rock bottom? The recent stabilization at -80% of the MERVAL index seems to say so, but this is a large risk to take into consideration.

Currency Risk

Something I have been hinting at during the whole report is currency risk. It is pretty pointless for an overseas investor to make 20% returns if the currency of these returns devalue at the same time by 20%. You get more Brazilian reals for example, but these reals do not get you more dollars.

So, it is important to be sure that the returns are likely to outpace the currency exchange rate changes.

When it comes to Brazil: the real has steadily devalued against the US dollar, at a remarkably regular rate if you look for a long enough time frame. Every 5-6 years, a crisis occurs (usually linked to low commodities price), and the Brazilian real loses against the USD.

Essentially, it devalued at an annual rate of 12%. Now that the last outburst of devaluation seems to have stabilized, we can probably expect some level of stability for the next 3-5 years, before a new wave of instability.

Therefore, I think a maximum of -12%, and a minimum of -6% should be expected for the next 10 years when it comes to Brazil’s currency effect. Definitely not good, but way below the returns number we calculated for Copel.

Source: www.xe.com

The Argentinian pesos is a completely different story. The devaluation over the last 10 years has been extremely brutal. This represents a total devaluation of 95% over 10 years, an absolutely terrible annual -27%.

Actually, the devaluation was going at the more “normal” rate of -16% annualized until 2018, when it suddenly accelerated, and the peso completely collapsed.

Source: www.xe.com

Real Return Taking Currency Risk into Account

As we saw, Brazil’s currency is far from being well managed, but is also somewhat predictable. The expected -6% to -12% sure is a bummer, but the returns on Copel were expected in the 20-30% range. This would give a +8% to 24% returns expectation range for Copel. By this metric, I would say that Copel passes the test, and would still be able to produce positive returns relatively safely.

Argentina being Argentina, practicability is not a given. In a very large way, Pampa is similar to a Forex bet. If the pesos stabilizes, Pampa should provide ample profits to the daring investors that dared touch it when no one else did. If the pesos continues its collapse, Pampa might turn into a disaster.

The real outcome will be highly dependent on global commodities markets and if central banks’ actions during the COVID crisis unleash durable inflation or not.

Possible Strategies with South American Utilities

No matter the specific company, emerging market investing is not for the faint of heart. Expect plenty of volatility and alarming headlines along the way. This already means that many investors should simply avoid it, as most are not able to avoid panic selling in a crisis.

The two companies share a lot of similarities. Both are operating in countries highly dependent on global commodities price. Both are utilities. Both are trading at depressed price. But as often, potential returns are in the proportion of the risks.

In that respect, Pampa and Argentina are the more extreme version of Copel and Brazil. While Copel offers reasonably good prospects of higher returns with relatively lower risk, Pampa is the most extreme very high risk/very high reward play I ever analyzed.

Both companies, through currency effect, will be sensible to global commodities price. This means that they can be used as a hedge against the risk of globalized inflation in a more diversified portfolio.

Copel is likely the best option for most investors, as it has more stable earnings, dividends, and cash flow, which will avoid them reacting emotionally. Pampa is more of a speculative play, or a very aggressive hedging tool.

In both cases, despite being utilities, the greater economic context means that both are somewhat speculative, compared to safer and lower return utilities in the developed world.

So, Which One?

Copel

I can easily imagine an investor putting 3-5%, maybe up to 10% maximum of his portfolio in Copel, looking for the possibility of 8-24% returns. The exact numbers going up and up and up if inflation becomes a worldwide problem. And if not, the returns should not be totally awful, and not drag the whole portfolio down.

Pampa

Being a much more aggressive option, Pampa should probably not be a large part of any portfolio. But a 1-3% might make sense as a hedging tool against inflation risks, similar to a gold miner for example.

Considering the brutal volatility to be expected on this stock, I image the best option would probably be to buy and forget it for the next 5-7 years. Looking at the quotation price anxiously is almost a guarantee for making bad decisions.

By then, the picture should have become clear. Either this turns out in a catastrophic loss or a brilliant idea. In the worst case, the small total exposure in the portfolio will have contained the damages. In the best case, the company will now be a cash cow exporting massive amounts of valuable natural gas, while also selling electricity in a booming Argentina.

Being such an aggressive speculation, it single-handedly could increase of decreased portfolio performance by a few percent. The main interest in doing so is that the downside maximum risk is known (-100% or total loss of the investment), while the upside could be a 3x, 5x or maybe even a 10x over the next decade. This kind of asymmetry/optionality can strongly help to boost a long-term portfolio return, but will need proper risk management.

Both?

It could also be possible to spread out the risk between the two companies. Maybe 4% of the portfolio in Copel, and 1% in Pampa for example. The more stable dividends of Copel could compensate a disaster for Pampa, but the Pampa exposure would boost the upside chances.

This is really up to you but stay careful as the combination of currency risks and high volatility will almost certainly bring surprise and worries along the way.

As usual, remember this is for information and educational purposes only, and to consult at least one accredited advisor before taking any decision.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in PAM nor ELP and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.