September 11th, 2021

Quick Stock Overview

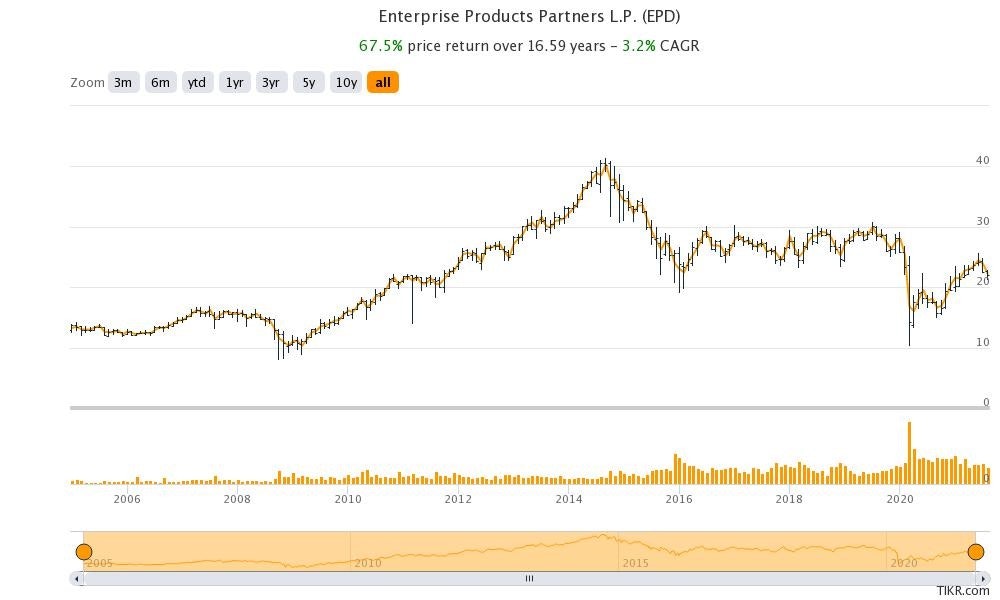

Ticker: EPD

Source: www.tikr.com

Key Data

- Sector: Energy

- Sales ($M): 32,572

- Industry: Oil and gas midstream

- Net Cash per share: $-12.89

- Market Capitalization ($M): 48,253

- Equity per share: $11.36

- Price to Free cash flow: 11.9

- P/E: 12.7

Investment Thesis

Buy When There Is Blood in The Streets

The sentence above is a famous piece of investment advice attributed to Rothschild. This is the heart of every contrarian investing method. Another way to say it is “buy low, sell high”. Seems logical and easy, right?

In practice, most investors do the exact opposite. If you want proof of it, look no further than the recent mania around Tesla and Cathy Wood’s ARKK ETF. It feels a lot better to buy a stock that has been going only up for a decade, than one that has consistently lost money.

Beyond perverse incentives about career risk in the money management industry, even retail investors are highly susceptible to this problem. We are social animals, and it simply goes against our nature to go against the crowd. Nevertheless, buying when it is cheap is the core of value investing.

So how to do it? One way is looking at countless companies and finding mispriced ones. I do that a lot, and many of the reports I publish here are found this way.

But sometimes it is even simpler than that.

An entire sector of the economy might have durably underperformed. It might be simply that it is out of fashion. Or that real economic and profitability problem hit the sector. Or there might be political and cultural reasons for this sector to be unpopular.

With the sector I will present to you today, all 3 reasons are present at the same time.

The Industry Everyone Loves to Hate

The industry of which I am referencing is the most maligned in the markets right now: the energy industry.

Of course, not the part that is going to save the planet: solar panels, windmills, etc… No, I am talking about the dirty, evil part of the energy industry: fossil fuels. All emitters of carbon will irreversibly destroy the planet’s climate, this is a fact. They are responsible for terrible things, like ecological disasters, the destruction of local water resources and be a even the primary culprit for conflict in the Middle East.

Ask anybody in the street, and you will be hard-pressed to find anyone in support of the oil and gas industry. And why would you support them? They are malicious, corrupt, and greedy polluters; at least that is the consensus. The same critics of fossil fuel energy will then hop in a car, get back to a gas heated home full of plastic-based devices.

I am not so much pointing out the hypocrisy of modern lifestyle with an ecological lifestyle (although this could be discussed too). But we need to remember that literally, everything in the modern world is possible thanks to abundant fossil fuel energy.

From food abundance thanks to gas-produced fertilizers, to high-tech and low-tech plastic gadgets, to quick and efficient delivery of the goods to your local supermarket. In most countries, electricity is still produced with the dirtiest of fossil fuels: coal.

Do not get me wrong, I am actually an ardent supporter of green energy, and would love to see fossil fuels phased out. I truly think it is the future and that in the long run, electrification and renewables will dominate the energy landscape.

However, I also know to not let my personal preferences or hopes go in the way of my analysis. Renewables are indeed the future, but the transition will sadly happen a lot slower than it should, and investors need to be aware of it.

When it comes to investing, people are currently unwilling to come anywhere near energy companies. This goes against the trend of ESG investing and for many, would simply make you a bad person. Besides, it is simply a bad investment. Just look at the oil and gas ETF: XOP.

It is significantly down since the 2014 peak, be even much lower since the 2009 low. So, does investing in oil and gas mean you are both evil and stupid?

Source: www.yahoo.com

Do you see where I am going with this? This is the typical “blood in the streets”, and the oil industry has bled out over the last decade. But why could it change now?

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A Postmortem

Several Storms at Once

The energy market, especially oil, has been suffering from a terrible image for a while now. This started with large oil spills, like the Amoco Cadiz, or the Deep Water Horizon in the Gulf of Mexico. And with the growing conscientiousness about climate change, a general concern that fossil fuels are quite literally going to kill the planet.

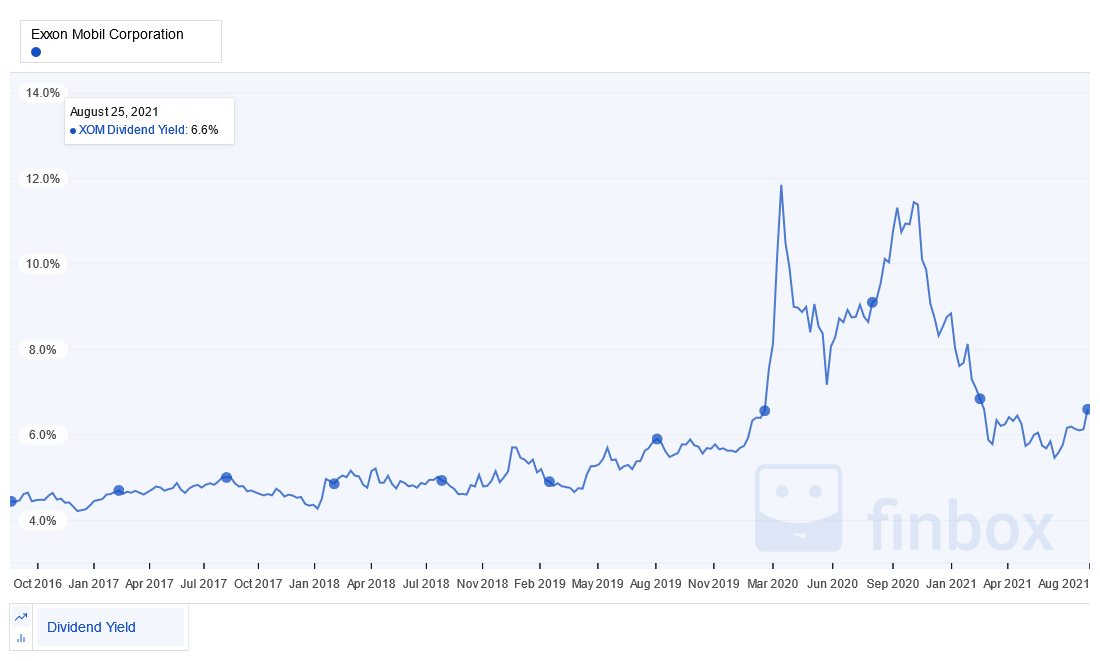

So, investors were already not happy with the PR of the oil industry. But it was giving very good and stable dividends, so many, including a lot of large pension funds, ignored it.

Source: www.finbox.com

But then came the threat of electrification. Oil is used largely for transportation, and with electric cars going mainstream, many have announced we passed peak oil demand. The IEA (International Energy Agency) is forecasting already 14% of the cars to be electric by 2030.

This might mean that most of the oil in the ground will become worthless before it is extracted and sold. This is a huge problem for entire countries like Russia or Saudi Arabia, but also for oil companies. Their largest assets are the oil deposits, and if it goes bust, so do they.

Terrible image control and bleak long-term prospects were looming over the industry, but at least profitability was still good. Most investors were getting worried, but not all left the boat…until the shale oil revolution.

Shale oil’s new technology allowed the USA to reverse dramatically a long-term trend of declining production. This also resulted in a sudden flood in the market of millions of barrels per day, outpacing demand.

In most circumstances, this would have led to lower prices, and then lower production. But with the US capital markets flushed with cash from the Fed, shale oil companies managed to keep raising more capital, more debt, to keep drilling more wells. The promise of lower production costs with economy of scale and technology maturing kept investors in shale oil complacent.

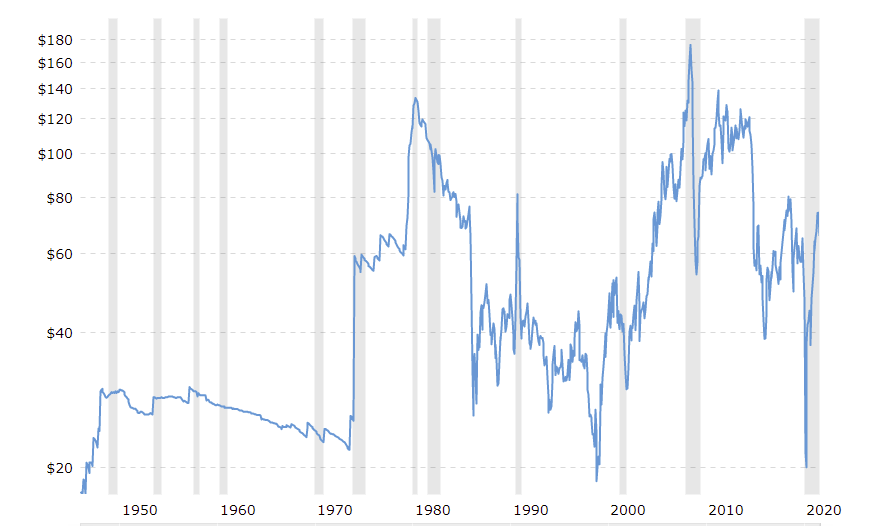

The result was the not so surprising collapse in oil prices. Adjusted for inflation, oil prices in 2016 were as low as in the mid-1980s. Shale oil producers started to lose investor confidence, OPEC production cut helped too, and oil price was starting to recover.

And then came Covid…

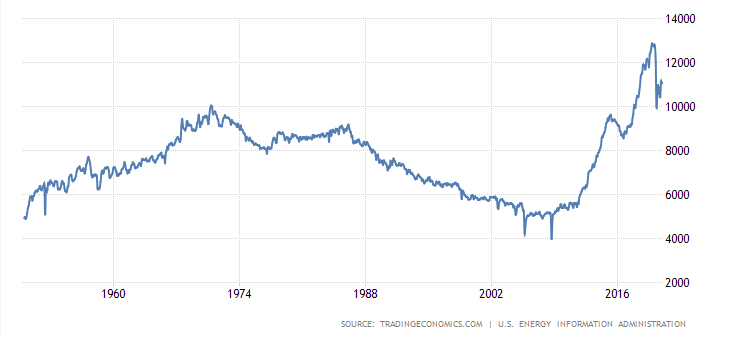

If you remember, in 2020, oil prices went negative for a few days. Producers are had to pay to get their oil taken away. If that is not a contrarian indicator and a signal of a bottom, I do not know what is.

Source: www.macrotrends.net

A Dead Sector? Not So Fast

After negative prices, you could believe the energy sector would be toast. But is it? Let’s look again at the XOP ETF, but with for the last 12 months. Roughly +100% performance. Not so bad if you had looked at negative oil price as a signal.

Now this was not for the faint of heart, and you will see, I will present a company less speculative than this. But I just wanted to show you the power of going against conventional wisdom.

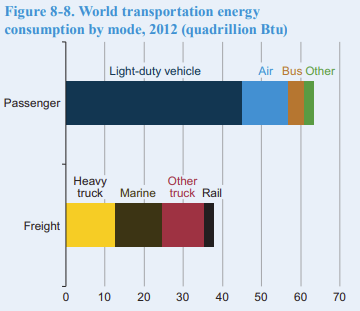

Let’s looks objectively at the energy sector prospect. Will oil demand go to zero in a decade or so? Hardly. You see, even in transportation, more than 60% of oil demand is not for cars, but for planes, buses, trucks, ships, or even rail.

So even if everybody by 2040 is driving an electric car, a dubious idea when a large part of the world is likely to lag behind, oil demand would still not so low. Changing the entire transportation fleet of the world will take a while, whether we like it or not.

Source: https://www.eia.gov/

Besides, a lot of fossil fuel is not used for transportation. When it comes to electricity, a lot of it is gas. Most heating for homes and offices are also consuming a lot of oil and gas.

All of those are going to switch slowly to renewable, but probably not as fast as we would like. In the first place, replacing coal with gas for electricity production will be the fastest and most impactful action on carbon emissions.

I cannot cover in this report the whole depth of the discussion about the future of fossil fuels usage. If you are interested to learn more about, I recommend this excellent report from Lyn Alden that was part of what triggered my interest on the sector.

Chapter 2: Not All Energy Stocks Are Created Equals

The Unfairly Punished Sub-Sector

You probably noticed that I only talked about the energy sector as a whole so far. This is because I need to first push aside the worries (or hopes?) that in 10-15 years, everything will be electrified, and fossil fuels will be history.

For better or worse, the world economy will still massively use fossil fuel for the next two decades.

The energy sector is usually split into three segments: Upstream, Midstream, and Downstream.

- Upstream: these are the oil and gas producers, the ones actually drilling and producing it (Exxon, Shell, BP, etc.).

- Midstream: these are companies transporting the petroleum products, usually in pipelines.

- Downstream: these are the refineries transforming the energy into final products, like gasoline, jet fuel, or plastic components.

Upstream companies are the most vulnerable to price downturns, as illustrated by the recent bankruptcy of Chesapeake Energy. Downstream companies are usually very low margin and very capital intensive, leading to brutal cycles of non-profitability when prices go down.

Midstream companies are different. They make their money not from the oil and gas price, but from the volume transiting in their pipelines. As long as people drive cars and need electricity, they are in business. This reliability gives midstream companies stable prospects and predictable cash flows.

Are Midstream Right for Value Investors?

In many ways, midstream companies are the ultimate defensive assets. They have very long-lasting assets (a pipeline can last for decades). Their revenues are easy to forecast and mostly in line with the broader economy. Because their assets are so durable, they are amortized over extremely long periods, leaving plenty of cash for the company to give back to shareholders in dividends or share buybacks.

Cheap Despite Good Results

To the risk of getting redundant, I will go back to the base tenet of value investing: buying assets for less than their real value. Midstream companies are broadly viewed as part of the “energy” sector and priced accordingly. When oil prices skyrocket, they are overvalued. And when oil is out of favor, they are undervalued.

This phenomenon has gotten more extreme with time, due to the rise of passive investing. Many, maybe most investors today, are not investing in companies. They are buying sectors, ETFs, funds, and other financial products quite blindly, not caring much about their exact composition or exposure.

When energy became the sector to avoid, all energy companies were sold off. Upstream, midstream, downstream; it didn’t matter. Profitable pipeline companies saw their share price collapse together with cash-burning shale oil drillers and refineries.

This allows us to buy them on the cheap!

The Ultimate Moat

The rejection of fossil fuels also had unintended consequences. One such consequence is that anything related to the sector has become politically radioactive. While some Republican politicians are still supporting the sector, the political class as a whole is not looking forward to being associated with a planet-killing industry. This also means very strong grass-roots opposition to any fossil-fuel-related project.

The perfect example is the cancellation, restart, and re-cancellation of the Keystone XL pipeline. In the current climate, building a new pipeline is virtually impossible, as this implies support the fossil fuel industry. Between environmental agency, local protesters, and reluctance from DC, it is unlikely any major pipeline project will be completed soon.

Such projects cost several billion (with a “B”) and many years to be completed. Investors are likely to be reluctant to approve such spending if, at any time, it can turn into a complete loss.

Existing pipelines are not exposed to this problem. They have been approved a long time ago,have a very good safety track record, much better than train transportation, for example. So, the existing networks of pipelines can operate without any new competition coming in to steal market share.

When we speak of a moat in value investing, we usually mean that it is very difficult for competitors to attack the position of the established company. But in this case, it is downright impossible. And with Big Oil’s image not improving any time soon, I can see this moat becoming even stronger over time.

An Undervalued Hedge Against Tail Risks?

Slowly, the topic of protection against inflation is becoming relevant again in the financial community. I am personally agnostic regarding inflation prospects, but I do prefer to have some protection against it in my portfolio, and to even profit from it if it ever becomes a real problem.

One popular way is gold, and I have covered this topic in my previous report about Kirkland Lake, a smaller Canadian gold miner. But another way to combat inflation is with energy companies. I am sure many of you have noticed the price of a full tank has risen quite a bit lately.

If inflation picks up, it is likely to be partially due to energy prices. You see, the depressed energy prices for the last seven years have forced a lot of non-shale oil companies to cancel or postpone investments in traditional fossil fuels, both onshore and offshore.

A new oil field can take 10 years to be developed from discovery to full-speed production. Also, a discovery can only be made if exploration budgets have been high enough.

The whole industry has chronically under-invested in future production during the lean years of the 2010s. Despite a level of already too low capex spending, another $44B of capex has been slashed due to Covid in 2020. This leaves the largest oil companies with decreasing oil reserves.

I fully expect that in the next 3-5 years, the combination of rising inflation, rising energy costs, and the communal realization that the green transition will take a while, will all happen at the same time. This same phenomenon has depressed all energy stocks in unison is also likely to lift them all up the same way.

The same result would happen in the case of black swans like a war with Iran, a successful terrorist attack on a Saudi oil field, a flare-up of tension in Taiwan or Ukraine, etc…

Overall, midstream companies can provide a super solid moat, predictable business, good cash distribution back to shareholders, and a hedge against inflation and geopolitical black swans.

Chapter 3: Why Enterprise Product Partner?

Picking The Right Target

The more I research the topic, the more I was convinced of the general idea of the energy sector, and midstream companies in particular. But this still left me to narrow it down to a specific target. So here was my list of criteria:

- US-based to reduce geopolitical risk

- Large enough to operate at scale and manage the growing regulatory burden, ideally one of the top five in the country

- Manageable debt

- History of responsible capital spending and cash distribution to shareholders

- Low exposure to crude transportation, as this would make it depend on the (mis)fortune of shale oil. I prefer other chemical products and gas instead.

This narrowed it quite a bit. Some of the good candidates were not publicly traded, so I could not invest in them. Some are now parts of larger entities, like Berkshire Energy Partners (16,400 miles of pipelines). Of course, noticing the presence of Buffett in the sector was somewhat reassuring, more precisely, Berkshire bought for $10 billion worth of extra pipelines in 2020.

Some other candidates in the top 10 midstream companies were too centered on Texas and shale oil. Some had poorly managed debt and the downturn, showing me substandard management.

I ended narrowing it down to two companies: Magellan Midstream, and Enterprise Product Partner. Both had a very similar profiles and good qualities, but EPD is almost 5x bigger, so I think it will be more able to operate at scale than Magellan.

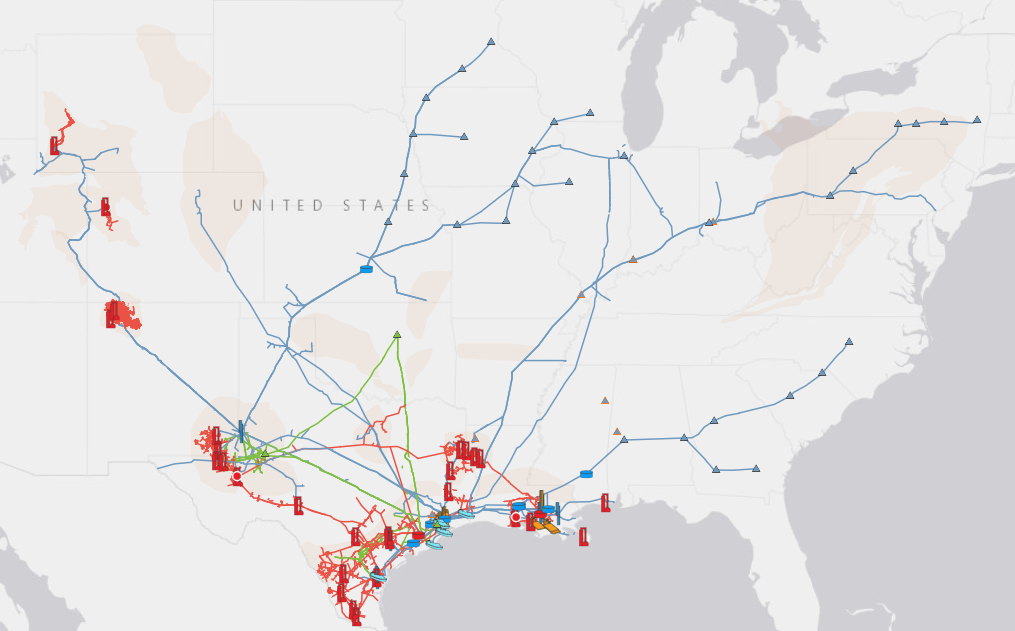

EPD’s Operations

Except for the West coast, EPD is at the core of the whole US energy infrastructure. It manages 50,000 miles of pipeline transport all types of energy products. These pipelines connect together gas fields, 22 natural gas processing facilities, and 23 fractionators (they separate the different components of natural gas into pure products), as well as very large storage facilities.

Source: www.enterpriseproducts.com

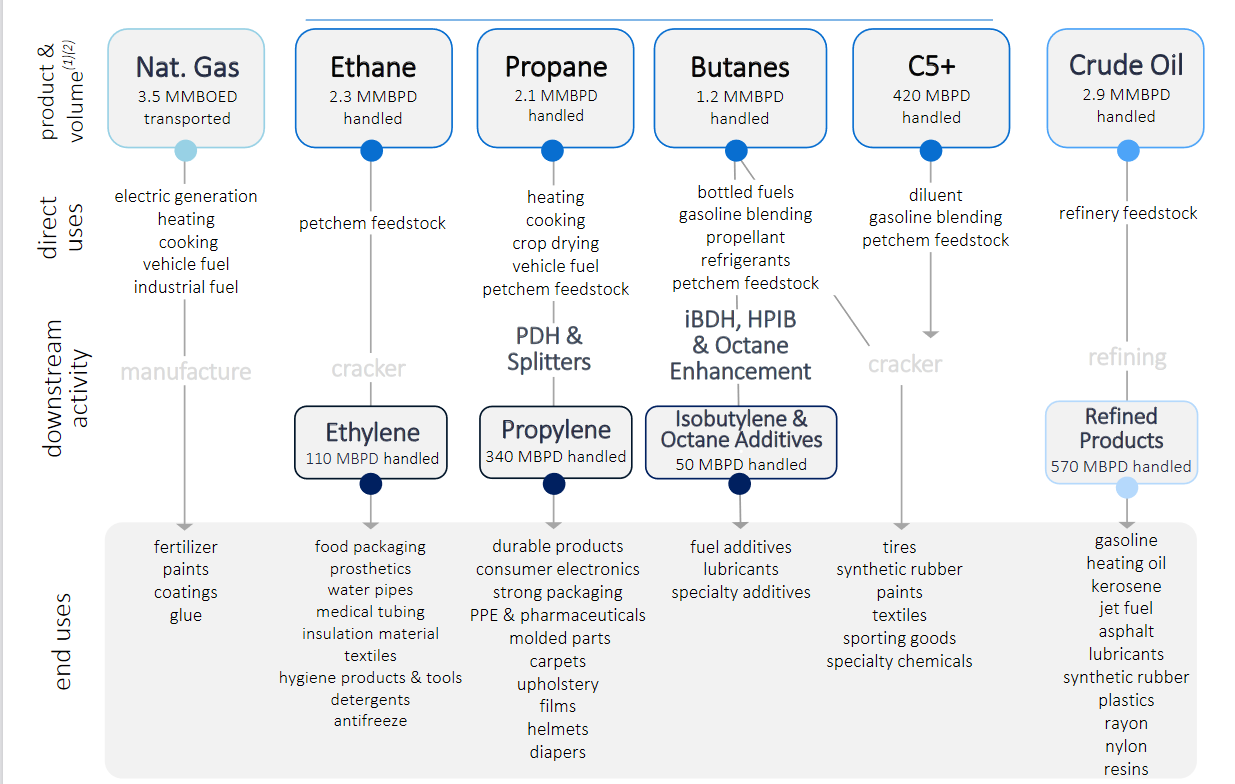

The bulk of EPD business is with natural gas and Natural Gas Liquids (NGLs), 65% of the total activity. The rest is split between petrochemicals (14%) and crude oil (21%). This is perfect in my opinion, as I am still not sure if shale oil will ever be a really profitable technology. In addition, if I underestimated the impact of electrification on transport, oil will be the sector the most damaged, not gas. Instead, EPD carries products required in almost every manufacturing process of the modern world.

Source: www.ir-west.enterpriseproducts.com

Management seems top-notch, with many of them in the company for a decade or more. The business is ultimately simple to operate, as long as management is careful to not overstretch with debt or acquisitions. The company keeps collecting fees as long as power plants and refineries need natural gas and NGLs.

During the worst of the downturn, margins were somewhat compressed as clients renegotiated as much as they could with transit fees in EPD pipelines. But ultimately, pipelines have such a strong moat that only temporary rebates occurred before the company returned to business as usual.

This was reflected in the growing net income and an ROIC that stayed positive even in the worst moment of the oil price crash.

Source: Finbox.com

Overall, I really appreciate how simple it is to look at this company. They put upfront capital to build billions of dollars’ worth of infrastructures, and then everybody in the industry needs to pay the toll charges for the decades to come if they want to use it. The pipelines themselves are a tried and tested technology, and competition is reduced to a minimum.

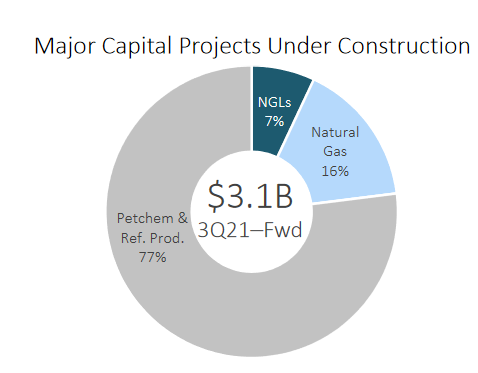

Historically the company has expanded with a mix of acquisitions and building new facilities. It seems that with the sector largely consolidated or in strong private hands like Berkshire Energy, any future growth will come from building. At the moment, $3.1B of projects are under construction, most of it in the petrochemical segment. The sector is only 14% of EPD’s gross margin, so I assume this is the area where there is room to grow.

This is also the least susceptible to disruption from electrification, renewables, and carbon taxes, so good to see EPD’s long-term vision is not blind either to changes coming in the 2030s and 2040s.

Source: www.ir-west.enterpriseproducts.com

The Financials

EPD has made $32B in sales in 2020, with a consistently growing gross profit margin over the last 10 years, from 6% to almost 20%. Despite that, the stock price has gone nowhere for most of the decade, before being hammered by covid and recovering recently. This means that the P/E ratio of the company has declined strongly, from 32 in 2012 to just 12-13 today.

Source: www.finbox.com

One special characteristic of EPD, as well as most midstream companies in the US, is that it is not registered as a standard corporation. Instead, the company is structured as a Master Limited Partnership (MLP).

These are very special structures that offer some taxes advantages and force the company to distribute most of its profit to the owners/shareholders. In return, they are not required to pay corporate taxes. The details are quite a lot more complex, and you can learn more about it here.

The major problem with that structure is that it will significantly complicate the tax declaration of the owner of shares in an MLP. As every individual situation is different, I strongly recommend you would consult a trusted tax advisor about it before investing a large amount in EPD or any other company with the MLP structure.

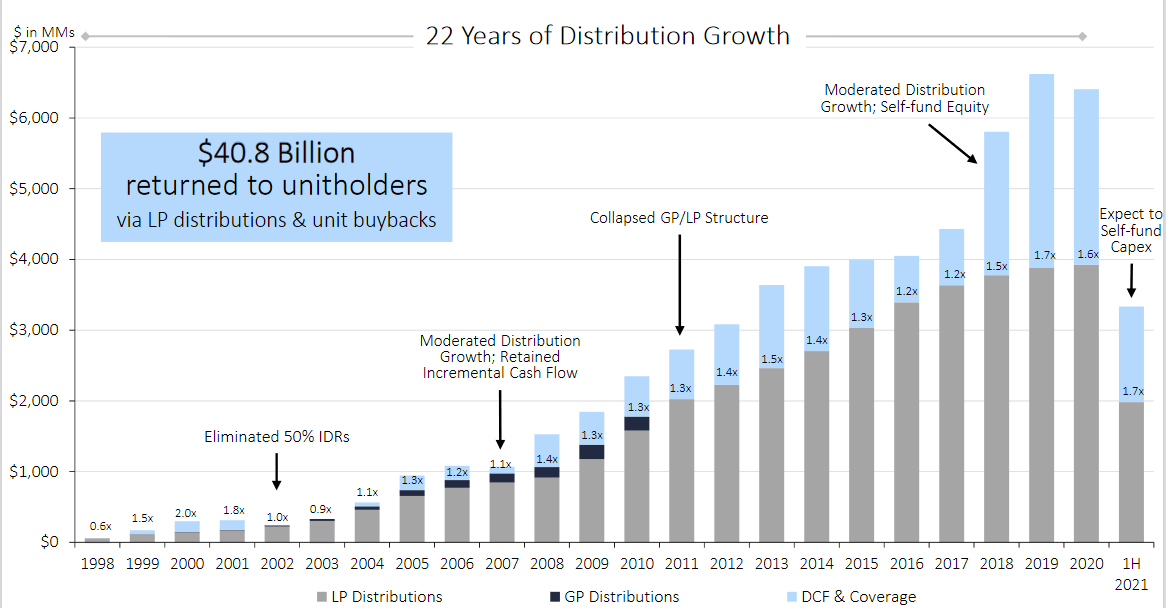

This said EPD has a rather impressive track record of cash distribution to its shareholders. 22 years of continuous growth in distribution, mixed between dividends and buybacks when the stock price justifies it. Buybacks have been smartly used, mostly at the moment the company stock was very depressed, including at the height of the Covid panic in 2020.

This smart practice buying back stock at depressed levels is rarely seen in management nowadays and it is refreshing to see being implemented at EPD.

The distribution did not either hinder the company’s ability to reinvest in the future, with 20-40% of cash flow still used to reinvest and grow the bottom line.

Dividends have grown slowly but steadily, and dividend yields have oscillated between 6-15% for the last 10 years. In many ways, EPD stock is acting more like a perpetual bond of the company than a stock. The possible upside of the stock price is a nice bonus if it happens, but the dividend yield is the base return expected by the shareholders.

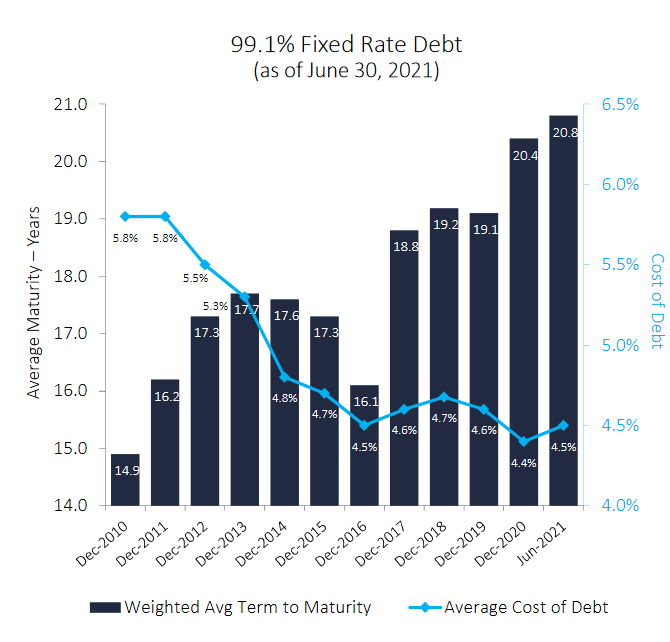

One last element to look out with capital-intensive industries like this one is debt. A too-large debt or too-high a cost of capital could hurt the company, or even kill it. Hence why management quality and track record are so important. Debt maturity can be a concern too, as most of the company income is stable and occurring far in the future.

The amount is significant, no less than $32B. This is not surprising for a business with a very large capital expenditure, but not a pristine balance sheet either. Half of EPD debt is due in 30 years or more, and 83% of the total debt is due in 10 years or more. This has been a determined strategy of EPD to lengthen the debt perspective, to lock in lower interest rates. This succeeded, as the average cost of debt for EPD has gone down from 5.8% to 4.4%.

This might look small, but on $32B, this represents $450M fewer interest costs per year. With net income at $3.8B, proper management of the debt interest has contributed largely to the company’s net income growth.

All in all, the debt is consequential while not being worrying. Management has protected the company against a rise in interest rates for the next decades. The long life of pipeline assets should also shelter them from any eventual rise in inflation.

Source: www.ir-west.enterpriseproducts.com

Judging Future Risk

I am in general pretty optimistic about EPD’s future, but I think I must still add a word of caution. By being a central piece of the US energy infrastructure, EPD is at the center of the storm about global warming and ESG. We have recently seen the pressure from ESG focused activists affect policies and prospect of some of the Big Oil companies.

For example, Royal Dutch Shell has been ordered by a court to reduce its carbon emissions by 45%. Another example is the small activist investor fund able to grab board sit at Exxon despite owning just 0.02% of the company. Or simply all major banks freezing funding for artic oil projects.

Can it happen to EPD too? Could government, court, or activist force it to redirect its cash flow into a green project? Yes, I think so. I do not think it is likely in the next 5-10 years, but it could happen.

Energy policy is very rarely just rational. You can look at the emotions any discussion about nuclear energy to have a proof of that. Carbon emissions are becoming as politically and socially heavy as nuclear with global warming becoming more and more of a concern.

So, I think that EPD is a great value and probably has a good future prospect. But if the political or judicial landscape change quicker than expected, I might have to reconsider it. Just keep that in mind if you decide to invest in EPD and balance your portfolio accordingly.

Chapter 4: Valuation

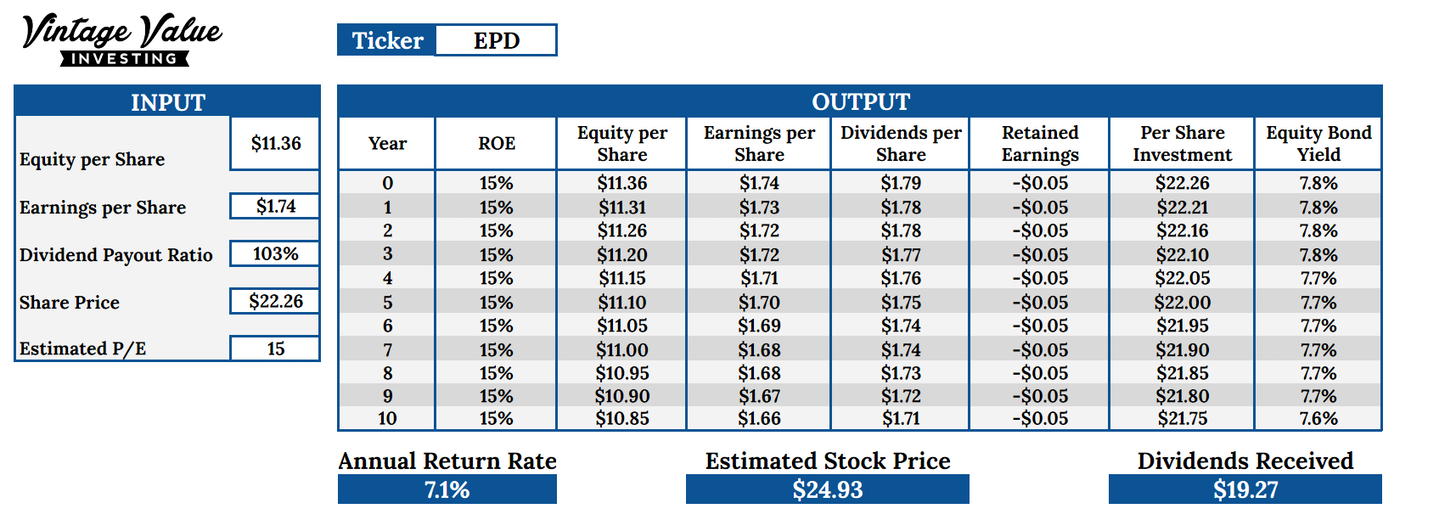

When it comes to picking a valuation method, I was split between the equity bond and the discounted cash flow method (DCF).

On one hand, the extreme stability of EPD yields well to the equity bond method. But this valuation method is likely to underestimate any growth potential coming from extra capex and improving moat.

The DCF method takes better growth into account, but with the very unstable multiplier markets have applied to the company, it is a less robust valuation.

So, I think that the equity bond method represents more of a base minimum return EPD should provide, while the DCF is more realistic.

In both cases, I used relatively conservative numbers and a high margin of safety, just to consider the volatility of the energy markets.

The equity bond method gives me an annual return rate of 7%, which is in line with the current dividend yield of 7-8%. Again, I think this is a bit pessimistic as the EPD dividend has increased constantly for the last 22 years.

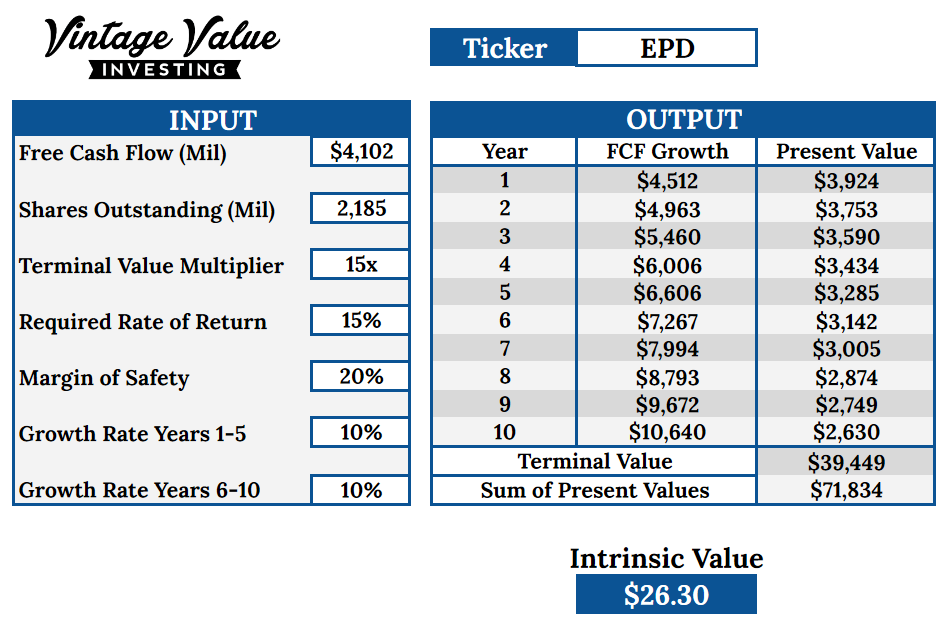

Free cash flow has increased at the astonishing level of 28% in the last 10 years. I took an “only” 10% growth rate and still get an intrinsic value of $31, to compare to the current $22. By this metric, EPD is really undervalued. I think this is likely considering how out of favor the whole sector is. This also explains why Buffett was so interested in large acquisitions in the sector.

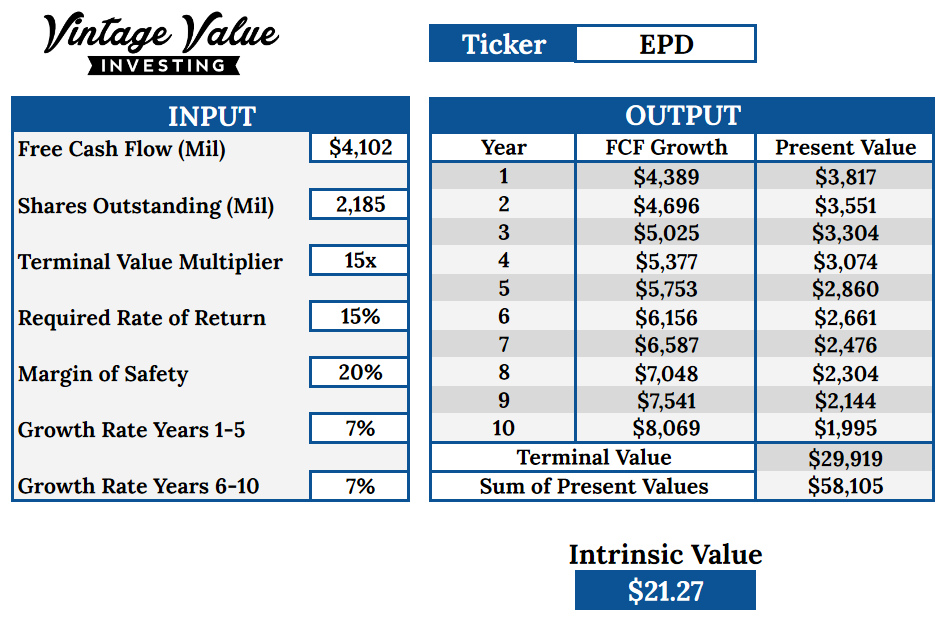

I was curious to see what free cash flow growth would justify the current price, and it turns out that with only 7% of growth per year, EPD price would still be quite cheap and offer a 20% margin of safety.

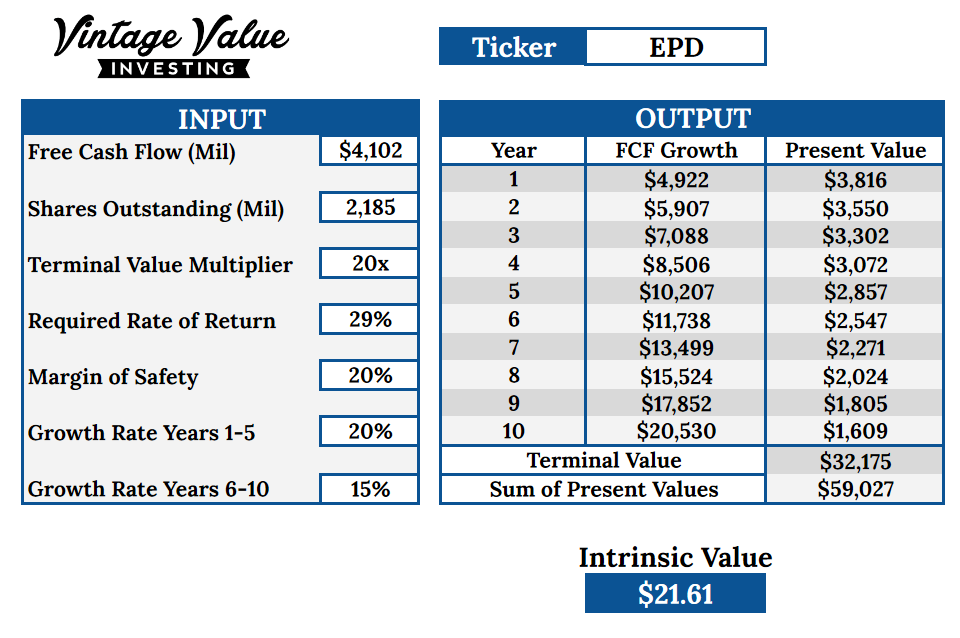

Finally, I was curious about what a best-case scenario could look like. If the market gives a better multiplier to the company, and growth slows down from the current 28% to 20% and then 15%. This would mean a 29% yearly return rate. I am not saying this is what will happen, but the fact that it could is still very appealing.

Conclusion

When I started my research for this report, I went the other way than usual. Normally I find a company with something promising, a good moat, a cheap price, and dig up from there. This time I went from top to bottom, starting by picking the energy sector and narrowing it down to a specific segment and then a specific company.

I think both methods can work, even if I will probably keep doing the bottom-up approach more often.

Enterprise Product Partner is similar to a utility company but selling at the price of a cyclical at the bottom of the cycle. The price at which is sold is really low, and I am sorry to not have thought about even earlier during 2020 when the dividend yield was 15%. I mostly can thank the general lack of knowledge of the energy sector, ESG, and passive investing for the current mispricing.

EPD benefits from all the strengths of its sector: stable business, stable margins, low cost of debt, strong and reinforcing moat. But it adds to that the right product mix, good management, and economy of scale.

I have no doubt other companies in the energy sector could be a good pick, but if I am looking for exposure to energy and protection from inflation out of gold and other metals, EPD seems like a good choice.

I am not sure what returns I should expect from this stock. A bare minimum of 6-8% from the dividend yield is likely, with some upsides possible. The upside will depend on many unpredictable factors, so I do not know if it is possible to accurately measure it. But if any of the following happen, EPD is likely to provide an extra 3-5% yearly return to the 6-8% base rate:

- Geopolitical crisis in an oil-rich region

- Inflation spiraling out of the Fed control for a few years

- Delays in the green transition

- Reindustrialization of the USA

I do not know if or when any of these could happen. But with the recent withdrawal from Afghanistan, tension with China, money printing, and so on, I expect the next 10 years to be somewhat unstable in one way or another. And I think EPD can help provide some hedge to a portfolio against all of these.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in EPD and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.