June 6th, 2021

Quick Stock Overview

Ticker: KL

Source: www.stockrover.com

Key Data

- Sector: Basic Materials

- Sales ($M): 2,181

- Industry: Gold

- Net Cash per share: $2.38

- Market Capitalization ($M): 11,116

- Equity per share: $19.04

- Employees: 1,981

- Debt / Equity: 0.0

- Interest coverage: 175.4

Summary

Kirkland Lake Gold is a gold mining company with growing production. Its mines are located in premium jurisdictions, 2 in Canada and 1 in Australia.

Source: www.s23.q4cdn.com

The company has been steadily growing and has produced consistently positive cash flow and earnings. Its reserves in the ground are good for more than a decade of operations, and it has no debt. Its production costs are also remarkably low in the industry. This is combined with a relatively low valuation at the moment.

All in all, if you are looking to add to your portfolio an exposure to gold, Kirkland seems like a low-risk asset, able to keep production profitable even if gold price declines.

Strategic Analysis

In the financial world, few topics inflame passion like gold. Gold has some industrial usage (electronic mostly) and is of course popular in jewelry. But what gets people really worked up is the role of gold in the monetary system.

We used to have every currency backed by gold, and entirely convertible. A dollar was worth a certain sum of gold and both were seen as interchangeable. While this is not the case anymore, central banks still hold tens of tons of gold in their vaults (out of the total of 200,000 tons), seemingly ”just in case”.

On one side you have the “gold bugs”. They are convinced that only gold is “real” money, compared to fiat currencies (dollars, euro, yen, yuan, etc.). They are also convinced that the current rate of money printing and debt rising is unsustainable and will lead to some imminent collapse in the monetary system. They would usher the return to a gold standard or gold-based currency, making gold price rise 5-20-fold.

On the other side, you have people convinced that gold is nothing but a “barbarous relic” and will never be used as money again. Noticeably, Warren Buffett is in this camp:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

I am personally not a gold bug. But it does not mean I am hostile to gold either. A large part of the financial community does believe in gold, and it is not likely to change any time soon. And it is true that central banks have steadily accumulated gold lately, with 650 new tons just in 2019.

But I am not really keen on actually owning gold itself. Its storage is costly, and it does not produce any yield. At best, it is a form of cash or dead money waiting to be invested on something productive. But as long as there is a demand for gold, gold miners with low enough production cost will turn out a profit. If such miners sell on the cheap, it makes them potentially good businesses.

So, I don’t think you need to be the doomsday prepper type to be interested in gold miners. You just need to find the right company.

The Importance of Mining Jurisdiction

One of the largest risks in investing in commodities, and especially major ones like oil or gold, is the jurisdiction risk. Many countries in the world have made a habit to outright nationalize such industries or levy heavy tax on it, in the name of “fairness” or “redistribution of the national resources to its people”. In practice, such redistributions usually end in the pocket of the local oligarchs or dictators.

This means that investors need to be careful of where they go. In bad jurisdictions, the more productive, money generating an asset is, the higher the chance it will get stolen by the local government. So paradoxically, a great company in such jurisdiction is maybe a higher risk than a bad company.

This is what got me interested in KL when I started to browse gold miners. Not only its financials were looking good, but its mines are in Canada and Australia. Both countries have strong rule of law, efficient taxation system, and business friendly environment. Of course, you can find cheaper assets in Zimbabwe. But they are cheaper for a reason, as you never know when they might just be taken overnight. As a value investor, I am looking for stable, safe, profitable long-term investments. Not having to worry about a military coup or a new nationalization wave is a must to sleep well at night.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

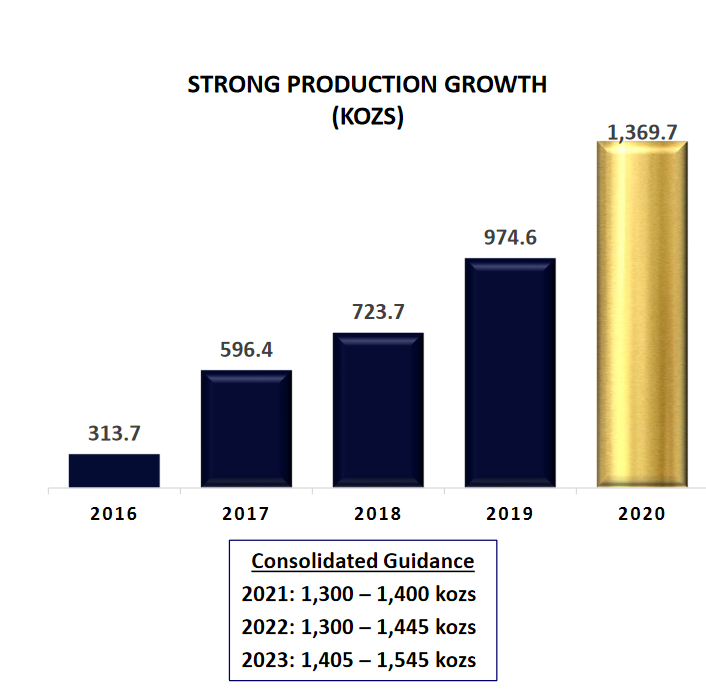

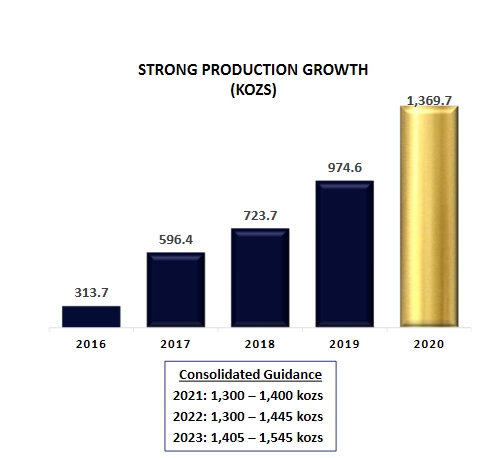

Kirkland Lake Gold produces around 1.3-1.4 million ounces of gold per year. Most of that production is actually done in Canada, so for practical purposes, KL should mostly be considered a Canadian miner.

Source: www.s23.q4cdn.com

It is worth noting that the production has been rising steadily over the last years and is forecast to still grow a little for at least 3 years.

Source: www.s23.q4cdn.com

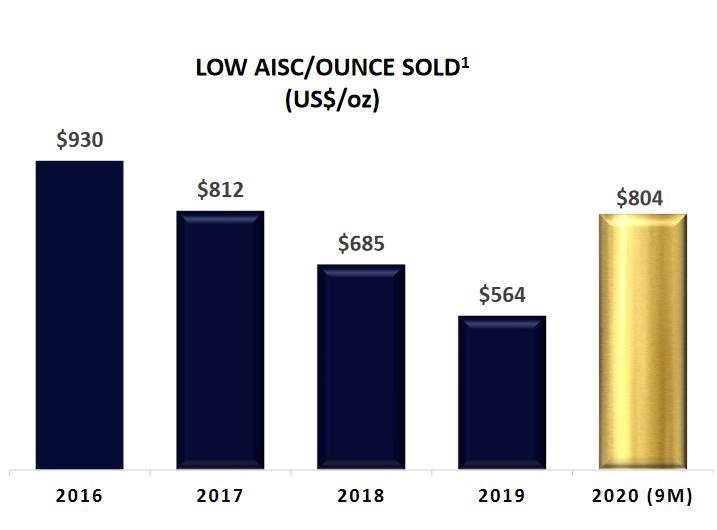

It has a remarkable low cost of production, shown in its AISC. This acronym means All-In-Sustaining-Costs, and was introduced and standardized in 2013 by the World Gold Council. It is not necessarily a perfect measure of production costs, but by being a standardized measure, it allows to compare different miners with each other.

Most of the industry have a AISC of $900-$1,300. KL’s is $790-$810. And the $800 range is even rather high for the company’s historic performance.

Source: www.s23.q4cdn.com

This means that even at low gold price, like the 2010s, when gold hovered around $1,200, KL could make a comfortable $400 per ounce produced, while most of its competitors could barely stay afloat.

It is important to understand that in the mining industry, low production costs are mostly a consequence of geology. It derives from the concentration of the ore, the depth of the deposits, the difficulty to mine and so on. Good management, efficient machinery, good infrastructure play a role too, but only so much.

This means that when you find a low-cost producer, it is likely to stay that way in the future. And if the production costs are high, no matter what improvement management does, it is likely to never really get better.

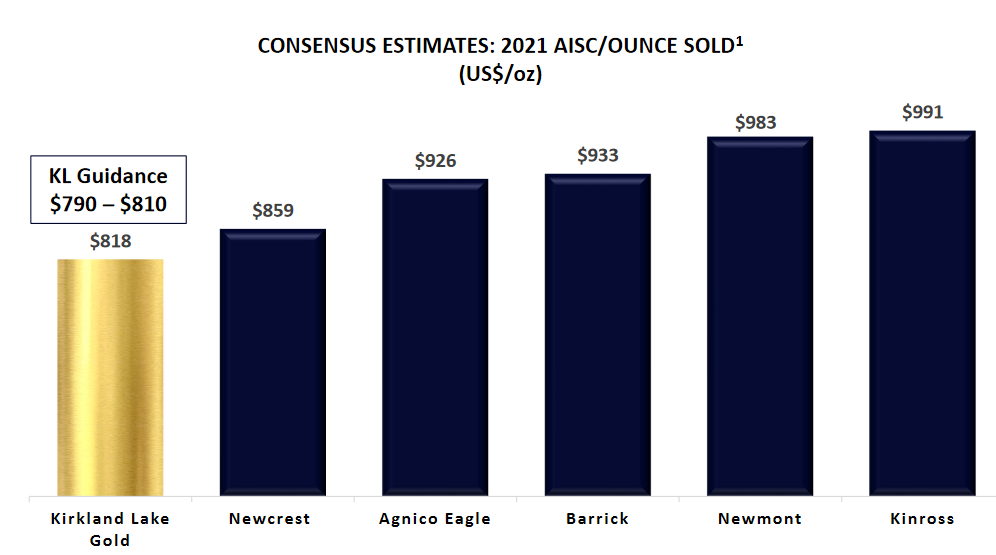

As you can see below, even the largest, most well-run companies in the industry have 10-20% higher AISC than Kirkland.

Source: www.s23.q4cdn.com

Gold can go up very strongly, like it did from 2002-2012, but also can crash much lower. So, it is crucial, with gold as with all commodities to pick a low-cost producer, that could keep making positive cash flow even in time of low prices. Commodities are a very cyclical industry, and the marginal high-cost producers usually go bankrupt in downturns. You just do not want to invest in those companies if you are looking for long term return.

Source: https://goldprice.org/gold-price-chart.html

Reserves

Contrary to a company producing goods or offering services, mining business models obviously depend on having ore to extract from the ground to be refined into pure metal. This means that every mine has a total amount of resources as well as an expiration date that depends on how quick the resource gets depleted.

Therefore, it is important to know how much gold is left in KL mines if we want to properly judge its valuation. The reserves are separated in 3 categories.

The first is proven and provable. This means that drilling and digging have found this resource already, and the company is sure of its quality and quantity.

The second is measured and indicated. This is the very probable resource, known to be there from the ongoing production, but not accessible for production yet.

The third is inferred. This is the resource the company thinks are likely to be in the ground. These reserves are judged by an expert guess depending on local geology, previous returns and limited sampling in the area.

This is the most uncertain part of the reserve. They might be revised downward, but also upward. It is actually rather common that the more a mine is exploited, the more resources get found.

The detail of KL’s reserves can be found on its website, but I will put a short version of that reserves here. Reserves are expressed in ounces of gold.

Most gold miners are planning for a production life of their mine of 10-20 years. KL is sitting on remarkably larger deposits than normal. On top of that, most of it is in the safer categories of Proven or Measured, instead of the more speculative Inferred resources. This give a very good visibility of KL’s production in the future.

The Detour Lake mine was recently acquired, and have more than doubled the total reserves of the company. The AISC of the mine is not the lowest in 2020 (at $1,171) but is forecast to decrease to only $900 in 2021 once running fully under the new management.

The company is doing some exploration to keep growing the reserves. This can be exploration around the existing mines to find nearby deposits. Or it can be negotiating with exploration junior miners to acquire new deposits. KL’s management is not describing any of these in a way that an investor could judge it, so I decided to ignore it in this report. Obviously, good surprise could come from it in the future, but considering the lack of data, I prefer to no take into account for reserves and valuation.

Such surprise just arrived when I was studying the company. In late April, Kirkland announce that it was buying 9% of companies involved in exploration projects next to its Macassa mine. Kirkland will have an option to buy up to 75% of the firms in the future, depending on spending on exploration and results.

This should extend even more the reserves size of KL, but I prefer to left it out of the analysis that risking overvaluing this very fresh deal. It is however a good example of how capital discipline and local expertise can help KL extend its reserves and acquire more gold ore at a good price.

Economic Moats

In value investing terms, moats are usually not really applicable to miners and commodities. By definition they produce the same metal than everybody else in the industry, every 5kg gold bar is the same as the next one. So, no branding, design or uniqueness of any sort. They also generally do not have patents or unique procedures in production. Its buyers are not especially faithful and are uniquely price oriented. And despite the emergence of giants like BHP, the industry is far from having a monopolistic structure.

Production cost

However, KL is somewhat special in that respect, by having some of the lowest production cost in its industry subset, while also being big enough to diversify risk between several mines. Its location in premium jurisdictions is also a structural advantage versus its peers operating in poorer underdeveloped countries, with less safe legal systems.

So, in the case of a downturn, many of competing mines would have to slow down operations, close or might even go bankrupt. Instead, KL is likely to keep producing enough to produce cashflow no matter what. Considering how hard, borderline impossible really it is to drastically change the AISC of a mine, the advantage of KL in production cost is going to last and give an edge against its competition and any drop in gold price.

Management

I will not go in detail about every member of the management because to speak frankly, there are too many of them. Really, just give a look at the corresponding page on the company website. To be totally honest, I am a bit wondering if the company does not have a little bit too many vice-presidents, no less than 18, to support the CEO, CFO and COO. Mostly because they are accompanied by another 10 Directors and 6 Independent Directors on the Board.

It might be that the company is just generous with titles and exposure for some personnel that would otherwise be qualified as middle management. It might also reflect the overly technical and heavily regulated operation of KL.

Or the company is the proverbial Mexican army, with way too many generals. Hard to tell. So, I will focus on some of the key members and do a general review of the rest.

Jeffrey Parr. Chairman of the Board

A CPA by training, Mr. Parr has worked for 30 years in the mining industry in multiple companies. I am not enough of an expert in gold mining to really judge, but his background seems solid, and the result of KL’s capital allocation indicates good decisions from its board. The company has not done overpriced acquisitions and kept a very clean balance sheet, two of the most common pitfall commodities companies fall into.

Anthony Macuch. President and CEO

A MSc of Engineering and Geology as well as with an MBA, Mr Macuch has joined KL in 2016. Interestingly, he was already working on the Macassa mine between 1992 and 1998 when it belonged to Kinross Gold.

Natasha Vaz. COO

A bachelor in Mineral Engineering with a background in multiple technical roles in the mining industry before, she also has an MBA and seems a good technical complement when the CEO has a more accounting oriented profile.

The Others

The rest of the management team have solid experience in mining and overall a dominantly technical expertise (engineering and geology). This rarity of more business profile type is not really rare in the mining industry, but it is to be appreciated. When the operations need to be perfectly executed to keep costs down and avoid environmental disasters, I am happy to see a large team of very technical people leading the company.

Compensation

I must admit that when seeing the size of the management team, I wondered how much it cost. A top-heavy company might mean a lot of money going toward the many directors and vice presidents and less to shareholders.

Stock option payments come at approximately $2.75 million

There is a complex “restricted share units (“RSUs”) and performance share units (“PSUs”) (collectively, “Share Units”) that may be granted to employees, officers and eligible contractors of the Company and its affiliates.” I am actually not sure how to understand this nor I am sure to have the total amount of spending in entail.

I regret that the details are not made a bit clearer between the legal and accounting jargon used on this topic. As you will see in my conclusion, if I have only one problem with the company, it is its handling of performance-based compensation and share issuing.

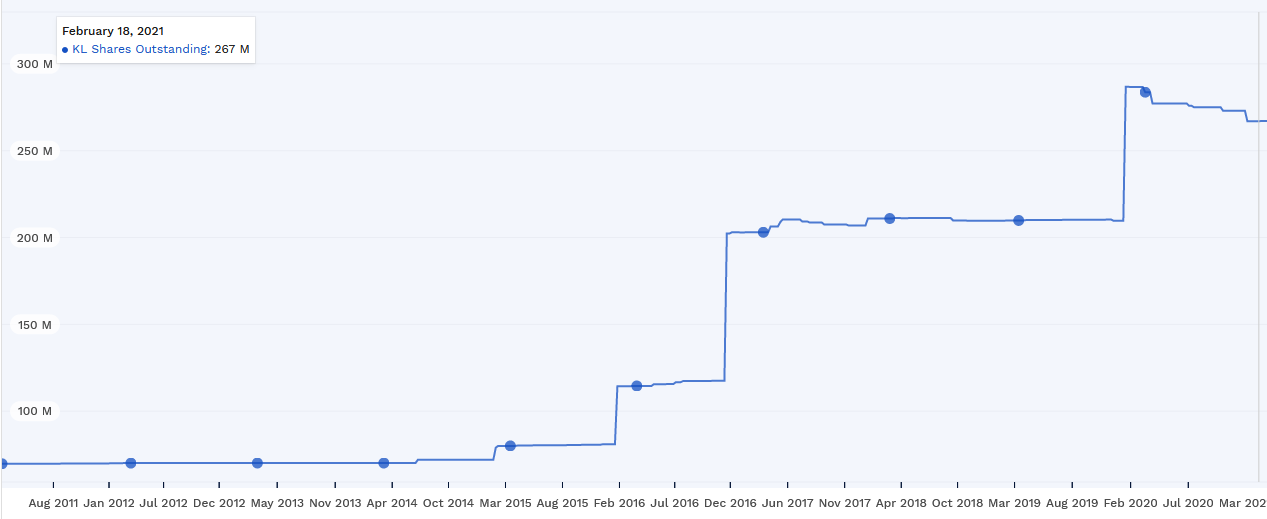

Overall, I am under the impression that a total of 372,640 + 386,767 shares are given as compensation to management so more than 750,000 shares in total. This is not that much for a total of 266 million shares outstanding, but nevertheless represents $24 million, a not so small sum when net earnings are at 787 million. So around 3% of the company total net income is distributed to management.

I personally feel that this number is little inflated and would benefit from a reduction in the head count of directors/vice-presidents. It has however a positive point of linking remuneration to share price and giving management a partial ownership into the company. So in the long run it will probably guarantee management interests alignment with shareholders’ interests, with the exception of management remuneration itself.

KL’s shares outstanding have been steadily rising in the past, but this was related to the acquisition of mines and the capital need for mine expansions that are now done. So, the increase in share number is not due to management compensation. It is worth noting that since 2020, the company is starting to do share repurchasing to decrease the overall amount.

Source: www.finbox.com

The increase in share in 2016 correspond to capital needs for launching the full speed production of its mines. The 2020 increase was for the $3.7 billion acquisition of Detour Lake mines. Considering it more than doubled the reserves of the company, for less than 30% of its market cap at the time, I would consider this a good capital allocation than created value for the shareholders.

Competition

As miners produce a fungible commodity, the only relevant competition is the industry as a whole. This is because a gold bar from a miner is exactly the same as a gold bar from another miners. So the only competitive risk is the whole industry flooding the market with more product than their is demand for. In that respect, for fully commodities products, the only competition is from the industry overall production, and not any individual companies.

Gold miners have a habit of overspending and opening too many new high-cost mines during boom, to suffer under crushing debt burdens and high production costs during bust.

The 2012 bear market in gold taught solid discipline to the industry, which has not so far repeated the mistakes of the past. As new mines take at least 5 years, and often 10 years to come online, the low number of new projects lets me think that the commodity boom is there to last for a while.

Quantitative Analysis

Financials

Revenues

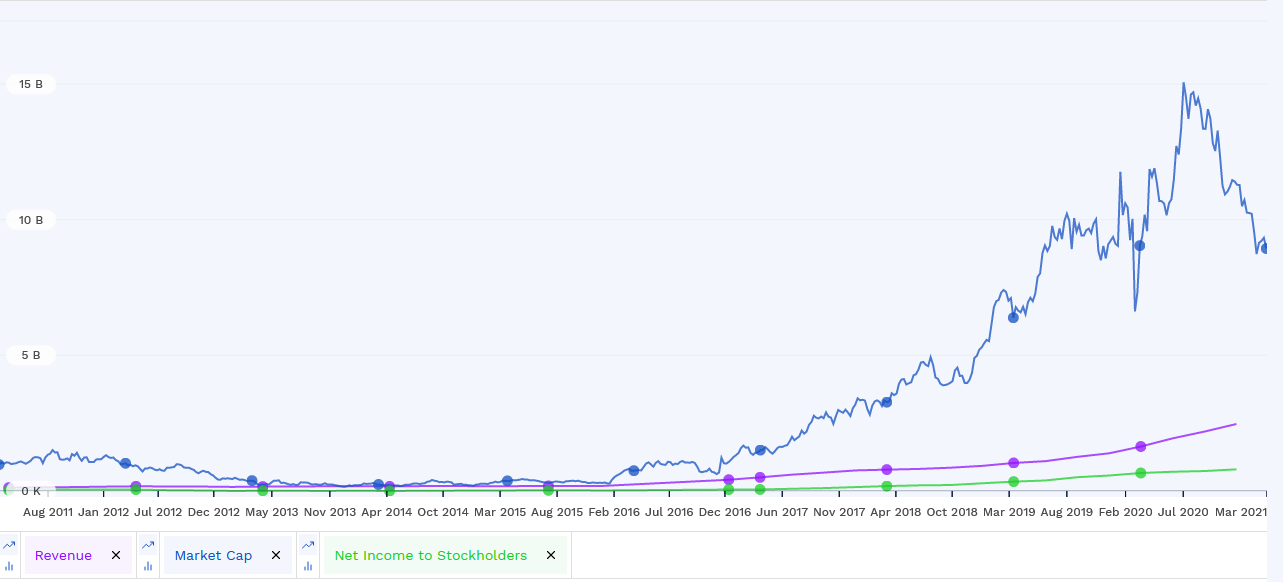

KL has steadily grown its revenues and net income over the last 5 years, reflecting the growing production of its mines. The last year has been one more tumultuous for its stock price, that spiked with gold price in the summer of 2020. But actual profits and earnings do not really justify such a short-term focused sell-off.

Source: www.finbox.com

Dividends

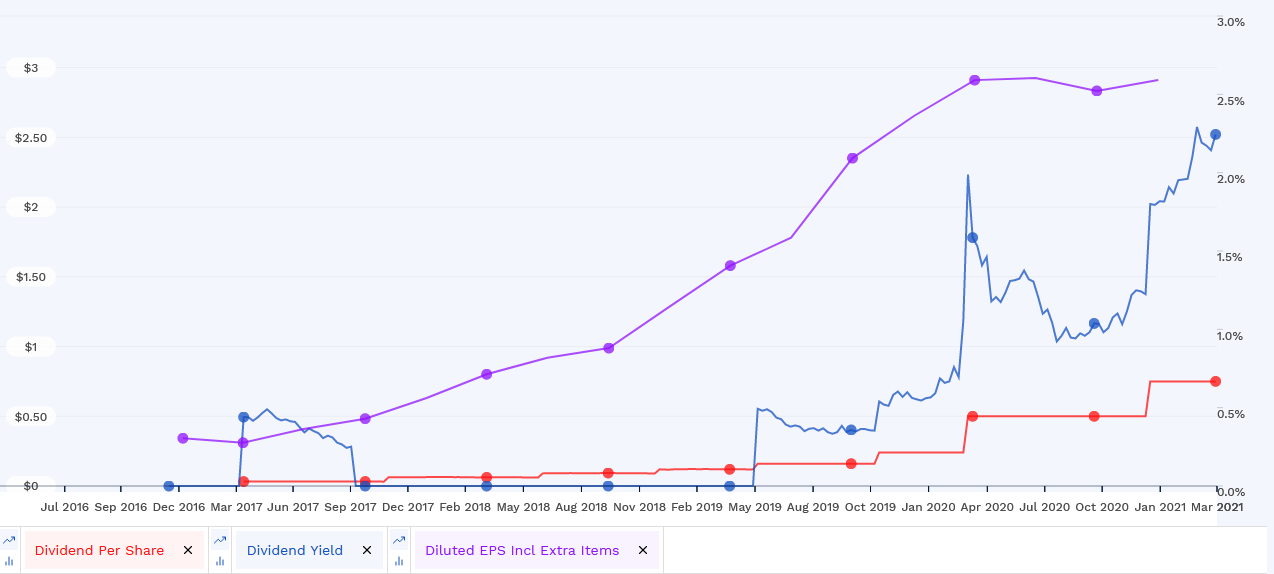

Since KL started to produce generating cash, it also started to distribute dividends. For a while the company cash also went to pay back all the long-term loans, so the dividends have been growing rather slowly.

Now that the company is seeing higher gold price and low debt charges, I think the dividends might have room for more growth in the future. This is especially shown in the gap between earnings per share and dividends per share.

You can see that the recent fall in the stock price has also contributed to increasing the dividend yield, which stands at a not so bad 2.2%

Source: www.finbox.com

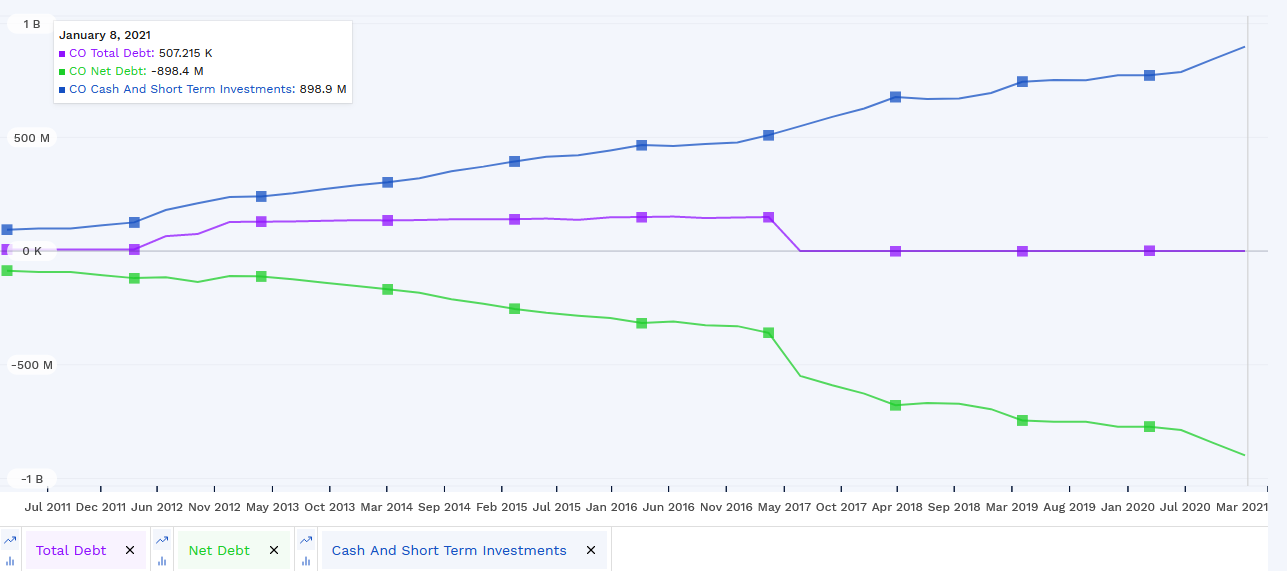

Debt and Balance Sheet

Mining is a very capital-intensive business, and it usually means massive debt to pay for building up the assets, buying heavy machinery and vehicles, and so on. So, debt must be a major concern for any investor in commodities.

The overly indebted mining companies simply do not survive downturns in price, as the temporarily reduced cash flow becomes insufficient to cover the debt. This is usually when the more conservative and prudent competitors can buy their assets at a discount.

The company has been accumulating cash over the last 3 years, while also completely reimbursing its debts. This made the net debt going negative in 2016 to a very impressive -$820 million.

This is great optionality in KL right there. Gold prices are very cyclical, so an investor in the sector needs to be ready for downturn lasting 5-10 years at worst. If gold price goes up, the company, while making massive profits, will be able to either repurchase its shares or grow its dividends.

In the event that gold price crashes, the company has very low risk of bankruptcy and should instead be able to buy valuable assets from its distressed competitors and wait for the gold price to go up again.

Source: www.finbox.com

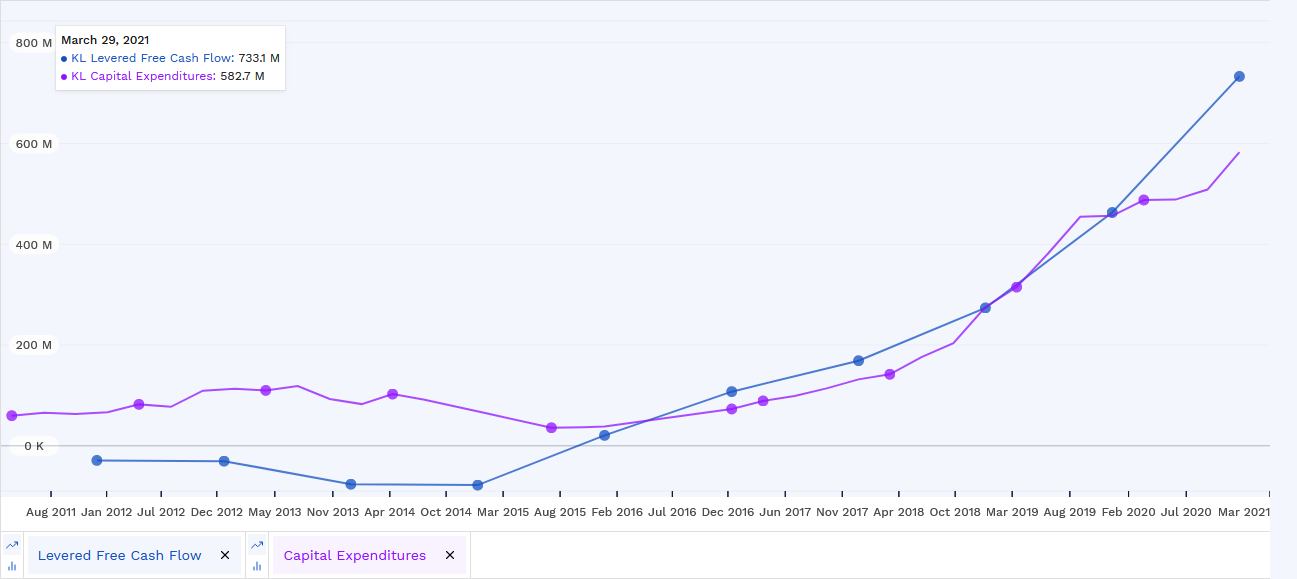

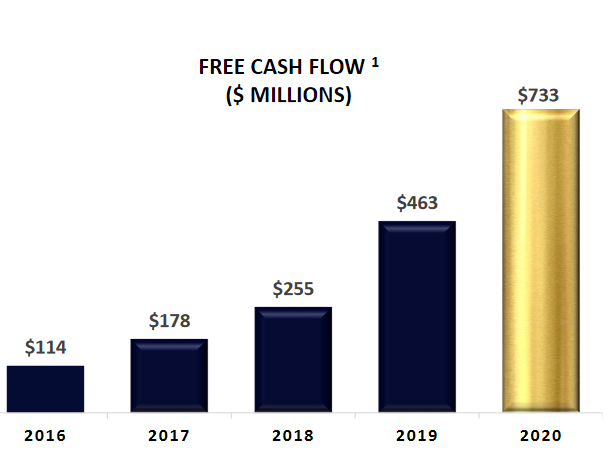

Cash Flow

2016 was the turning point for KL, when its mines started to produce enough to turn the cash flow positive. 5 years ago, sentiment around gold price was not so optimistic as it is after the sudden rise of summer 2020. So, the company made the right choice by using this cash to reimburse debt to secure its future against gold volatility.

It can also be noted that the free cash flow growth has not been generated by too low capital expenditure. To the contrary, CAPEX has increased over the last years to get the mines operating at full speed and supporting the cash flow growth.

Source: www.finbox.com

To assess the quality of capital allocation, we can look at various rations, like ROIC, ROA and ROE. All have grown to around 20% in 2019 and are likely to stay in that range. It slightly decreased in the end of 2020, reflecting some operation issues with COVID and the decreased price of gold/ounce. But short of a collapse of gold price, I expect the company to maintain good returns on invested capital, equity, and assets.

Source: www.finbox.com

Categorization and Valuation

Investment Category

KL is a quality mining company, as reflected by its good return ratios, growing dividends, and strongly negative net debt. Most quality companies should be bought for the long run, and KL is not different. However, its gold deposits have a finite quantity of gold in them, so the company should be valued as such, instead of a potentially unlimited compounder like and Apple or Coca-Cola.

The Mining Company Model

Every company can be valued in multiple ways. But for KL, I think the best way is simply to look at the value of what is actually in the ground, and how much it costs to dig it up. This of course implies that we need to assume a gold price for the period and judge if production costs can stay stable. So, you need to be aware that any mistake in these estimations would strongly affect the valuation.

For this reason, I will try to calculate it with 2 scenarios, one somewhat optimistic and one pessimistic. I will leave the super optimistic moonshot to the true gold bugs.

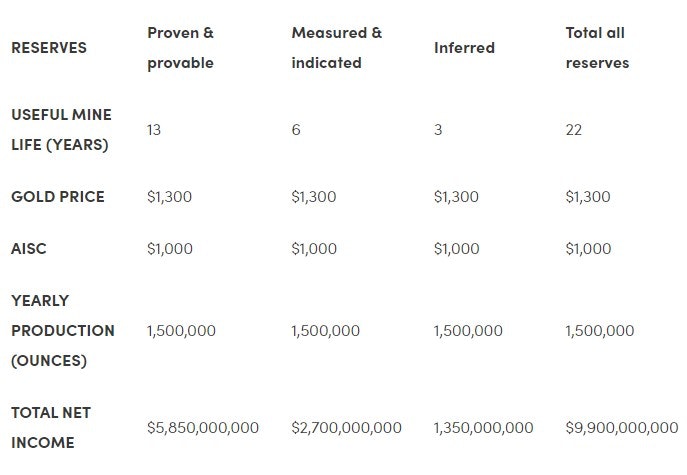

Scenario One: Low Gold Price, High Production Cost

In this scenario, I consider that gold falls strongly below the current price, down to $1,300. I do not really think it is realistic with the worldwide enthusiasm for money printing and growing inflation concerns, but this gives me a worst-case scenario for KL. I also consider higher production cost, that can come from various causes, from rising oil price to stronger taxes or environmental regulations.

For good measure, I also added more bad news and removed two years from the duration of the more uncertain reserves.

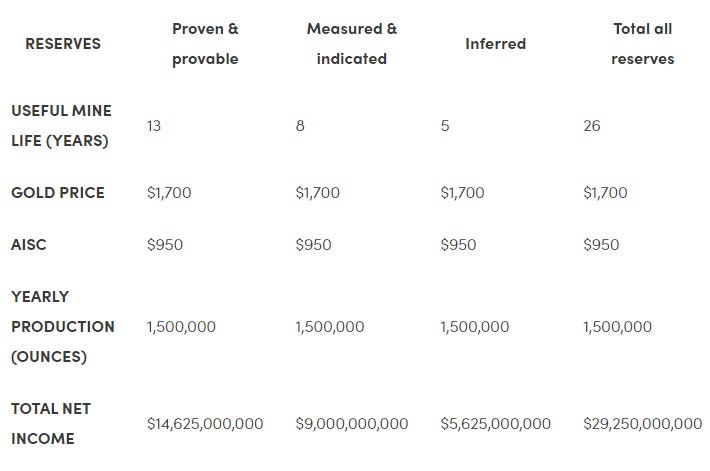

Scenario Two: Stable Gold Price, Constant Production Cost

In this scenario, I consider that gold stays at the level of $1,700 for the foreseeable future. This is not the best case, at it touched the $2,000 mark just a year ago, but this is still higher than most of the 2010s.

I also considered rather constant production cost, growing to just $950.

These calculations do not include almost a billion in negative net debt, but ultimately, this is not truly impactful to the lifetime value of the business, even for the worst-case scenario. So, I prefer to consider it as a cherry on top, and not include it in the calculation. At today’s market cap of $11.7 billion, KL seems priced for something close to the worst-case scenario.

Therefore, we could call KL a little overvalued if mining production cost increases, gold price crashes to $1,300 and stays there for 22 years and the reserves are revealed to be a bit less good than expected.

Or really undervalued if the situation with for gold mining turns better than that at any time in the next 26 years.

I tend to be of the opinion of the latter. At the least, KL is already priced for bad circumstances, and offers a strong optionality on the upside.

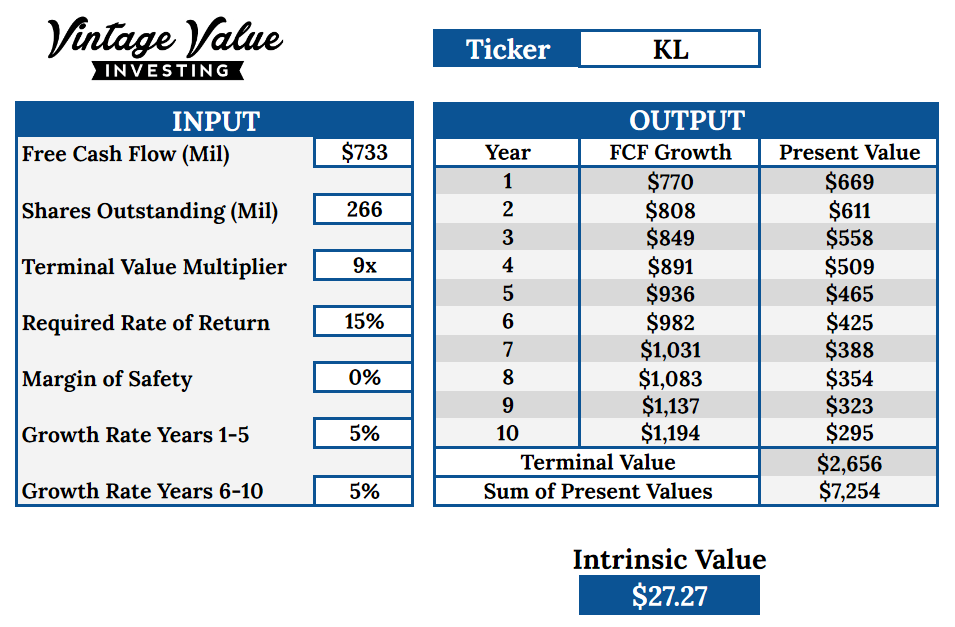

Discounted Cash Flow

Another way to calculate KL’s valuation is using the discounted cashflow model. You can see what it means and how it works here. To me, this is the best method to calculate the value of a quality steady compounder like Kirkland Lake Gold.

It is a bit difficult to settle for a value for cash flow growth. The recent years explosion in free cash flow was the result of the mines opening and getting into full production, so we should not expect the same in the future. Therefore, I gave it a low 5%, reflecting the guidance for a growth of production to 1.5 million ounces and slowdown in CAPEX spending.

Source: www.s23.q4cdn.com

Source: www.s23.q4cdn.com

I used as a terminal value multiplier the lower range of the price / free cash flow ratio of 9. It has varied a lot over time but seems to always stay above this level.

Source: www.stockrover.com

This gives us an intrinsic price of $27.27 per share, way below the $42 stock price. The required rate of return would need to drop to 8% to make the stock a buy.

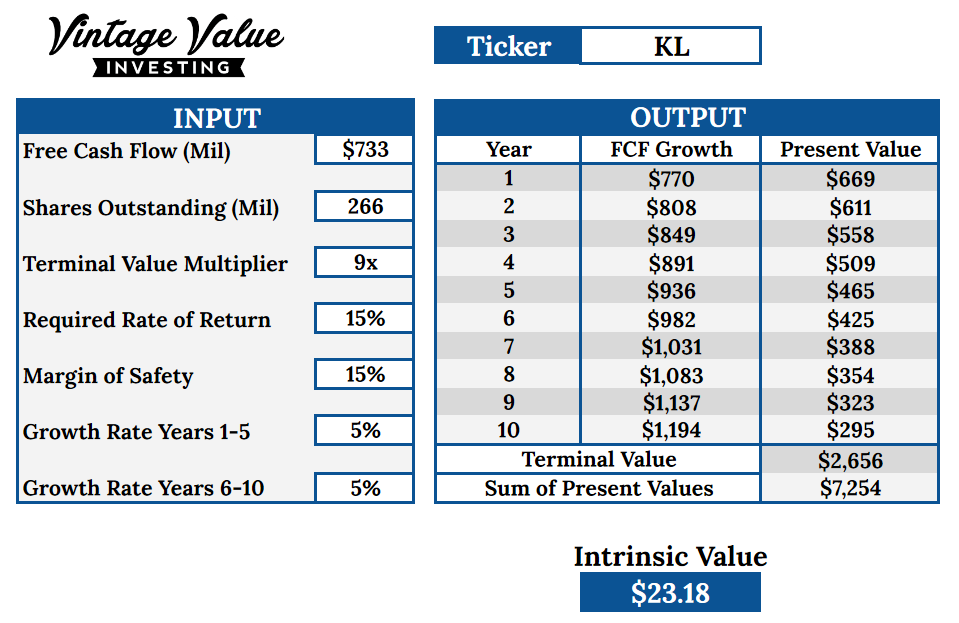

In order to stay safe, I also used a 15% margin of safety to determine the ideal buying price of the stock.

So, is KL overvalued? There are two ways to look at it.

One is that the discounted cash flow simply gives a warning that the price is still too high, and returns are likely to be “only” in the 8-10% range.

Another one is that discounted cash flow calculation neglects the fact that KL is a very predictable business. In 10 years, it will still have another 16 years of reserves to operate with. So, these levels of cash flow are not going anywhere until 2047. Therefore, it has intrinsically a higher margin of safety than most businesses more exposed to distribution, new technology, etc. As long as gold price does not utterly crash, KL will generate money steadily.

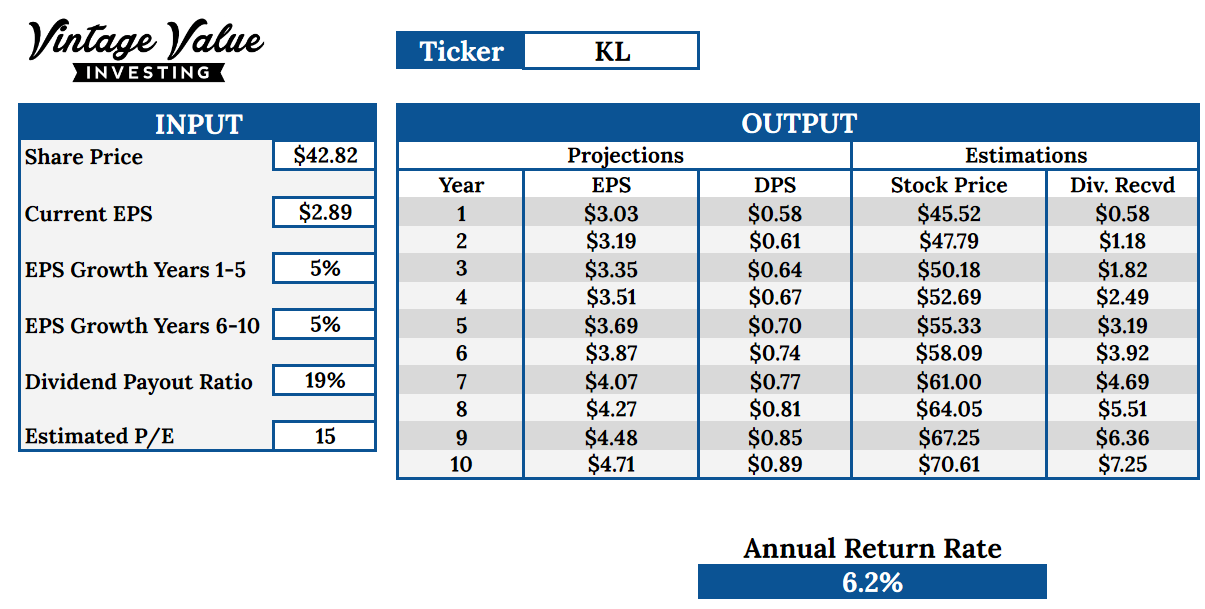

Earnings Growth

Earnings Growth is a method that considers KL stock essentially from its ability to grow its earning over time.

This would give us an expected return rate of 6.2%, so also showing a strong tendency to overvaluation, at least if you are looking for 15% returns or more. But 6.2% returns are not dreadful either for a rather safe inflation hedge.

This method is highly dependent on the P/E ratio used, and I took a conservative one to stay safe. The P/E has been very unstable, and generally higher than that.

Similarly, I used a rather low earnings growth metric, just in case no new deposit is found and gold price stay not-so-great for the next 10 years.

Source: www.finbox.com

However, I frankly doubt that model capture the whole value of KL for several reasons. First it does not reflect the fact that KL should have very stable earnings for the next 26 years, not just 10 years. Second, it do not consider the not-so-low chance that in the next decade, inflation might pick up, gold price might rise or anything that could easily double KL earning very quickly.

So, the 6.2% returns is more of a baseline/worst case scenario than the more likely returns. In that respect, I would consider this calculation tell us more that returns should be expected to be at least 6.2%, with a small but significant chance of it being way higher.

Other Calculation Methods

Low dividends for now and expectation of relatively stable earnings limit the usefulness of other valuation methods like Equity Bond and Yield on Cost.

Final Assessment

Company Synthesis

As gold miners go, KL is a high-quality company. It has large reserves lasting decades, no debt, and impressively low production costs. At the moment, the price seems quite low. The only thing I do not really like about the company operation is somewhat large number of directors and management member, but I can live with that if the operations run smoothly.

Whether it is undervalued or not depends mostly on the outlook for gold. If you expect the enthusiasm for gold to die out, the company is simply not a good one. If you think that somewhere down the road in the next 10-20 years, there will be a comeback of inflation or some serious monetary issues, then KL is drastically undervalued.

Personally, I envision something in the middle. Contrary to many high-cost gold miners, KL does not need doomsday predictions about the fall of the dollar and financial collapse to make an okay or good investment.

All it needs is investors and the financial community to stay moderately positive about gold as a hedge against inflation or other consequences of QE and deficits. In the current geopolitical context, we can also expect many central banks, especially in Eurasia, to keep accumulating gold “just in case” as a sort of neutral currency, not exposed to the risk of US sanctions.

In fact, the recent run-up in price of the share show that such concerns are already pilling up, in the midst of an (hopefully transitory) spike in inflation.

So really, allocating some part of a portfolio to KL is not so much turning into a gold bug than buying a relatively cheap asset with large optionality on the upside. Can it go down? Definitely! But can it be a good insurance against volatility or the return of inflation? Absolutely.

The more classic valuation models seems to indicate a likely return of 6-8% if nothing positive happens to gold. So this is basically an insurance against monetary or inflation issues, that still give you some not so shabby returns if nothing happens. And if gold price and/or inflation shoot up, you have 26 years of production with an extremely high margin ahead of you, and maybe more if exploration bring some good surprises.

Therefore, your decision about incorporating KL to your investment strategy, and its relative weight in the portfolio will depend on two factors.

- How much of a stomach do you have for the high volatility typical of commodities producers? I guarantee you that KL will not have a smooth, regular, and peacefully growing market capitalization. Plan accordingly and be prepared mentally.

- How concerned are you with inflation and currency devaluation, and do you already have other hedges for that (like for example, real estate, farmland, physical gold, other commodities producers, etc.)? It is important to not be blindsided to black swans in an increasingly unstable and changing world. Are you really sure that bond yields and inflation will forever stay low? Can anyone be?

Valuation

KL valuation according to cash flow and earnings seems to indicate that it is still a little expensive to safely produce a 15% return. So, if you are absolutely looking for this, I think you will be better off with other recommendations I have or will publish.

But if you are ready to accept an 6-8% yield, and are looking for a potential explosive upside, KL might be for you. Remember, value investors buy shares like if they bought the whole business. By buying KL, what you actually buy is a whole lot of gold at $800-$1,000/ounce. Actually, a total of 39,000,000 ounces to divide with the other shareholders.

The main factor if this will turn into a just OK or a great investment, is the future price of gold. If gold stays in the same price range it has been since 2008, KL investors should be ok and make returns in line with the general stock market long term average of 7-8%. If gold rise back and stay to where it was in June 2020, you will do great. If it shoot higher any time in the next 10-15 years, this is a homerun.

The main factors in KL outcomes are not economical but political, so I will not risk myself at an estimation here. Do you think the developed economies in the world will try to keep inflation low and cut their stimulus programs? Or do you think deficits and the printing press will keep running for a while?

You can see right there why people are so sensitive when a discussion about gold price comes along. Your perception of it highly depends on your opinion about welfare, stimulus checks, deficit spending, Wall Street bailout, etc… And it is a dangerous attitude to let such opinions affect your investment strategy. The market does not care if you are Republican or Democrat.

But with KL at its current price, you mostly bet that some investors and central banks will stay concerned enough to keep buying gold. And I think that is not so unlikely.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in KL and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.