Lexington Law

Lexington Law has long been a popular resource for people who don’t have time to repair their own credit. Lexington Law has been charged with illegal billing and deceptive marketing practices by the Consumer Financial Protection Bureau, raising serious questions about the Company’s business practices.

Pros

You're hiring a law firm

Extensive education tools

Multiple plan options

Cons

'C-' rating with BBB

Pending government lawsuit

Questionable business ethics

High plan costs

Lexington Law has been one of the largest and most popular credit repair companies for many years. In 2019 the Consumer Financial Protection Bureau sued Lexington Law for illegal billing and deceptive marketing practices, raising questions about the company’s integrity. Here’s what you need to know.

Lexington Law has long been a popular resource for people who have little knowledge of credit or don’t have time to repair their own credit. The Company advertises heavily and is well-known online

That reputation has been shaken by a federal lawsuit making serious allegations about Lexington Law’s marketing practices and about billing practices that are widespread in the credit repair industry. That lawsuit has been resolved, and the fines have forced Lexington Law into Chapter 11 bankruptcy. It is not clear whether the company will be able to remain in business.

In this review, we’ll look at the pros and cons of Lexington Law.

In this review:

- Is Lexington Law Legit?

- 2019 Lawsuit Against Lexington Law

- What Does Lexington Law Credit Repair Services Cover?

- What Does Lexington Law NOT Cover?

- How Much Does Lexington Law Cost?

- What To Expect After You Sign Up

- Lexington Law Contact Information

- How Do I Cancel Lexington Law Membership Online

- Lexington Law Alternatives

Top Alternatives to Lexington Law

We selected 3 companies based on historical performance, value for money, customer reviews, and industry awards.

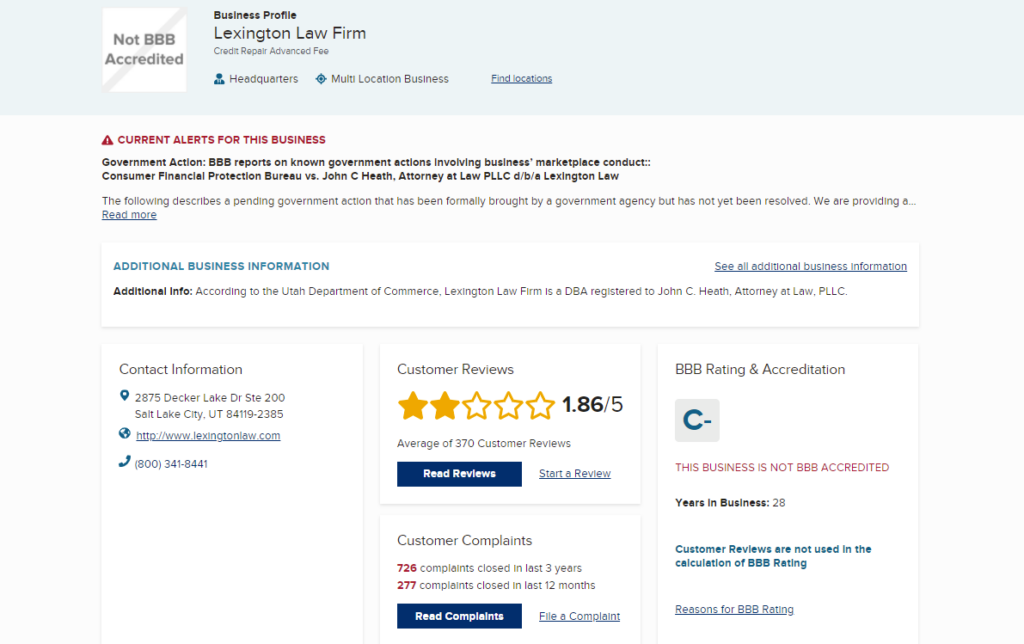

Who Is Lexington Law?

Lexington Law began offering credit repair services in 1991. It is an actual law firm and operates as a dba for John C. Heath, Attorney at Law, PLLC.

Many credit repair companies have come and gone over the past 25 years, but Lexington Law has been a stalwart in the credit repair industry. However, that longevity doesn’t necessarily come with the best reputation.

The Better Business Bureau (BBB) grades Lexington Law Firm a ‘C-‘ with over 700 complaints filed in the last three years. Complaints include overpromising on credit score gains, failure to get results, and overcharging for services.

If you are considering a credit repair service, you probably have one core question: Can Lexington Law remove late payments, collection accounts, repossessions, and inquiries from your credit report?

The true answer is ‘maybe.’ No credit repair company can guarantee that they can remove negative entries from your credit report, and there is no way to compel a credit bureau to remove a negative entry from your credit report. This success depends on each specific account and the circumstances around it. There are no assurances.

Does Lexington Law Work?

Lexington Law claims that it has removed over 80 million negative items from consumer credit reports since 2004.

While that number is definitely impressive, you can do it yourself just as effectively with the help of articles like ‘How Can I Dispute a Credit Report Entry’.

Lexington Law sends intervention letters to creditors and challenges letters to credit agencies on behalf of their customers. Customers can take advantage of the following legal services in selected states:

- General Litigation & Services

- Child Custody

- Bankruptcy

- Divorce

- Criminal Defense

- Property & Water Rights

- DUI Defense

- Select Pro Bono Cases

What Makes Them Different?

Lexington Law’s education tools are some of the best offered in the credit repair industry.

They also address harassing communications from collections companies and creditors, which is a standard service offered by most credit repair companies.

The clout that comes with your credit repair company being a legitimate law firm, whether perceived or real, is definitely alluring to consumers.

2019 Lawsuit Against Lexington Law

Lexington Law and CreditRepair.com are well known in the industry for aggressive marketing tactics. These companies are closely related entities, parts of a complex cluster of entities focused on credit repair services.

These companies include PGX Holdings, which owns Progrexion Marketing, Progrexion Teleservices, eFolks, and CreditRepair.com. Progrexion Marketing and Progrexion Teleservices provide marketing and other services to Heath PLLC, which does business as Lexington Law.

On May 2nd, 2019, the Consumer Financial Protection Bureau (CFPB) filed a lawsuit against “PGX Holdings, Inc. (PGX Holdings), and its subsidiaries Progrexion Marketing, Inc. (Progrexion Marketing), Progrexion Teleservices, Inc. (Progrexion Teleservices), eFolks, LLC (eFolks), and CreditRepair.com, Inc. (CreditRepair.com), and John C. Heath, Attorney at Law, PLLC (Heath PLLC), d/b/a Lexington Law Firm or Lexington Law”.

Despite the complex corporate structure, these entities appear to be effectively part of the same enterprise. The complaint states that:

Heath PLLC is a law firm based in North Salt Lake, Utah that does business under the trade names Lexington Law Firm and Lexington Law. Heath PLLC has been associated with Progrexion, or its predecessors, and has licensed the trademark “Lexington Law” since at least 2004. Progrexion conducts most of Lexington Law’s core business operations, but Heath PLLC, operating as Lexington Law Firm, serves as the face of Lexington Law.

The CFPB clarifies that the technical separation of these companies does not exonerate one from the actions of the others.

The Progrexion Defendants operate as a common enterprise. They have

conducted the business practices described below through interconnected

companies that operate under common control, have common business functions, officers, employees, and office locations, and share advertising and marketing. Accordingly, an act by one entity constitutes an act by each entity comprising the common enterprise.

The suit alleged that these companies were actively involved or complicit in deceptive and abusive practices perpetrated against their consumers.

The CFPB alleges that Progrexion engaged or was complicit in deceptive and abusive marketing practices. One particularly disturbing allegation was the use of completely fictitious claims to lure customers into retaining credit repair services. The complaint states:

To generate credit repair sales, Defendants rely on a network of marketing

affiliates who advertise a variety of products and services, often related to

consumer credit products. As alleged below, Progrexion’s marketing affiliates have used deceptive, bait advertising to generate referrals to Lexington Law’s credit repair service. For example, one of Progrexion’s most productive marketing affiliates falsely advertised that it “guarantee[d] ANYONE a 0-3.5% Down Home Loan no matter how bad their Credit is when we start!” In reality, the affiliate did not provide any loans at all. Interested consumers were told that, to participate in the (non-existent) loan program, they had to sign up with Lexington Law. The Progrexion Defendants paid this marketing affiliate for each credit repair sale that resulted from its efforts, despite knowing that it engaged in deceptive practices.

Essentially, marketing affiliates offered credit services that did not exist and advised potential customers to retain Lexington Law to repair their credit in order to qualify for those services. Potential clients were directly transferred to Progrexion call centers.

These offers allegedly included a wide range of financial services:

Partners have used advertisements that included fake real estate ads, fake rent-to-own housing opportunities, fake relationships with lenders, false credit guarantees, and false and unsubstantiated statements about past consumer outcomes. The ads have also included false and unsubstantiated statements about consumers’ likelihood of success in obtaining products and services such as rent-to-own housing contracts, mortgages, or personal loans.

Marketing is a natural function of any company, but these claims raise serious questions about this company’s ethics and practices.

Smoking Gun E-Mails: Management Knew

Lexington Law executives and management staff exchanged multiple emails amongst themselves and the affiliate that indicate Lexington Law was involved in this scam or at the least knew of it and did nothing to stop it.

In one instance, Lexington Law staff exchanged emails discussing how the affiliate’s script included promises that were clearly deceptive and contrary to CFPB rules.

…in a July 2016 email, a Progrexion employee reported concerns to another Progrexion employee that certain… partners offering rent-to-own housing were making implicit guarantees that credit repair would result in consumers obtaining the rent-to-own housing advertised. The Progrexion employee suggested that this situation be handled by changing the scripting used… in order to “avoid our agents hearing those expectations. The logic being that it is easier to plead ignorance if you’re truly ignorant.”

Instead of demanding the affiliate to cease and desist, they tried to find a way for Lexington Law associates not to be on the phone with the affiliate when the client was illegally misled to specifically induce the client to sign up for Lexington Law’s credit repair services.

The complaint also alleged that marketing personnel strongly implied that Lexington Law could remove even legitimate items from the credit reports of clients.

Illegal Billing Practices

The complaint also alleges that Lexington Law charges up-front fees, a violation of the Telemarketing Sales Rule.

The Telemarketing Sales Rule states that “the company may not request or receive fees until it has provided you with a credit report generated more than six months after the promised results that shows the results”.

Note that this rule only applies to companies that use telemarketing as defined by the Telemarketing Sales Rule.

Both telemarketing and advance billing are widespread practices in the credit repair industry, though not all companies use them. It is possible that the CFPB focused on the largest and most visible credit repair firm to deliver the point that this practice is illegal.

Are They Guilty?

This case has yet to be settled, but the allegations are serious and very detailed. They cast doubt on the business ethics of the companies involved. If a company uses unethical practices in one part of its business, would you trust them to conduct any part of its business ethically?

While Lexington Law and CreditRepair.com have gotten results for some clients, these allegations suggest that they may not be trustworthy partners.

👉 There are many more very troubling and unethical business practices alleged in the 48-page complaint which you can read for yourself here.

Update

On August 28, 2023, the CFPB announced that it had entered into a proposed settlement with Lexington Law. The settlement will have to be approved by the court.

The settlement imposes a $2.7 billion judgment and over $64 million in civil penalties against Lexington Law and its partner companies. The group behind Lexington Law is also banned from any telemarketing activities for 10 years.

Lexington Law has filed for Chapter 11 bankruptcy protection, laid off 900 employees, and shut down 80% of its operations. It is not clear how much of the fine will be paid or whether Lexington Law, CreditRepair.com, and their related companies will remain in business.

What Does Lexington Law Credit Repair Services Cover?

Lexington Law works with customers to ensure that their credit reports only contain fairly reported, accurate, and fully substantiated records.

They will work with the client to identify questionable records and then dispute those negative reports.

They do this by offering three levels of service plans:

Lexington Essentials

The Lexington Essentials plan at $59.95/month is the most basic plan that Lexington Law offers. You get up to four disputes per cycle with Equifax and TransUnion and up to three per cycle with Experian. You also get up to two creditor interventions per month: Lexington Law will request that the creditor remove a disputed record.

The plan provides up to $25,000 in identity theft insurance.

This is an affordable option for people with only a few disputable records on their credit reports. If you’re in that position, though, you should also consider the possibility of simply filing the disputes yourself.

Concord Standard Service

The Concord Standard Service at $99.95/month is a basic plan that includes up to six challenges per cycle at Equifax and TransUnion and up to 3 challenges at Experian per cycle. You also get up to 3 creditor interventions: Lexington Law will request that the creditor remove a disputed record.

The plan provides up to $25,000 in identity theft insurance.

This plan provides only slightly more service than the Lexington Essentials plan and is substantially more expensive. You’ll have to decide whether the added cost is worth it…

Concord Premier Service

The Concord Premier Service at $119/month gives you the same disputes, creditor interventions, and identity theft insurance as the Concord Standard plan.

By bumping up to the Concord Premier plan you gain access to several other services.

- InquiryAssist provides prepared letters to help you challenge hard inquiries that affect your score.

- Report Analysis provides additional information on your credit report and what items are helping and hurting it.

- Report Watch Alerts notify you every time there’s a change on your credit report.

- DebtHandler gives you a personalized analysis of your debt situation based on your specified goals.

These services will help monitor your credit reports and better understand your credit score and your debt situation.

You’ll need to decide whether these added features are worth an extra $20 a month.

👉 Keep in mind that many of these same services offered in this plan can usually be accessed for free from your existing tradeline providers or free credit score sites.

Premier Plus Service

The Premier Plus Service plan at $139.95/month is the Cadillac of Lexington Law’s product offerings.

You get up to 8 disputes per cycle with Equifax and TransUnion and up to three with Experian, along with up to six creditor interventions a month. The plan carries up to $1 million in identity theft insurance.

You also get all the added services of the Concord Premiere plan, plus access to a TransUnion FICO score, lost wallet protection, a junk mail reduction service, and a personal finance manager.

Can Lexington Law Remove Unpaid Collections?

Lexington Law can help you remove unpaid collections from your credit report only when the information reported is inaccurate and can’t be verified. Valid and verified entries cannot be removed from your credit report.

What Does Lexington Law NOT Cover?

They will not (or should not) promise that you will see positive results and cannot guarantee that your credit score will improve.

The Fair Credit Reporting Act has specific statutes and provisions that do not allow credit repair companies to mislead or exaggerate to prospective consumers.

☝️ Because of the guidelines laid out by the CROA, no credit repair company can guarantee the fixing of bad credit. They can, however, guarantee that they will return your money if they fail to improve your credit, as long as they fully disclose any limitations or restrictions on the guarantee. A money-back guarantee is not a promise that your credit will improve. It’s an indication that a company selects its clients carefully and works only with clients they truly believe they can help.

How Much Does Lexington Law Cost?

The first step is to select one of the three credit repair service plans offered.

Lexington Law no longer charges a start-up fee. The three service plans offered progressively get more expensive as you elect to have more services provided.

| Plan | Monthly Cost |

|---|---|

| Lexington Essentials Service | $59.95 |

| Concord Standard Service | $99.95 |

| Concord Premium Service | $119.95 |

| Premium Plus Service | $139.95 |

What To Expect After You Sign Up

After you sign up, you will receive your credit reports electronically at your designated email address, along with a copy in the mail.

Lexington Law does not accept faxes, and you will need to send your credit report to them by email or mail.

Lexington Law Mailing Address:

360 N Cutler Dr

North Salt Lake, UT 84054

Once they receive your credit report, they will enter all negative items into the Case Valet program for you to review.

The next step will be for you to provide details on how each negative report affected your credit or identify records with possible inaccuracies.

💡 Lexington Law credit repair specialists will be able to start helping you as soon as you fax or email your credit reports and identify questionable records in Case Valet.

Five to ten business days after you complete your detailed examination of the negative items they will determine the best strategy for your account.

They then will prepare necessary intervention letters for your creditors and challenge letters to the credit bureaus.

You will regularly receive updated credit reports from the big three credit agencies.

How Long Does Lexington Law Take?

Lexington Law does not state how long their services take because the recovery time differs for everyone. According to customer reviews, some people saw improvements in as little as 90 days, while others did not see any results even after 6 or more months.

Here’s a general idea of how long it takes for your credit to recover after a financial setback:

| Event | Average credit score recovery time* |

|---|---|

| Bankruptcy | 6+ years |

| Home foreclosure | 3 years |

| Missed/defaulted payment | 18 months |

| Late mortgage payment (30 to 90 days) | 9 months |

| Closing credit card account | 3 months |

| Maxed credit card account | 3 months |

| Applying for credit | 3 months |

*These are no guarantees. The numbers are rough estimates.

Lexington Law Contact Information

Lexington Law has offices and professional legal affiliations in many locations around the U.S.

Here is a list of all of Lexington Law Firm’s locations, phone numbers, and addresses.

| State | City | Phone Number | Address |

|---|---|---|---|

| AL | Birmingham | (833) 792-6000 | 2100 South Bridge Parkway, Suite 650, Birmingham, AL 35209 |

| AZ | Phoenix | (919) 568-3835 | US Airways Center, 201 E Jefferson St, Phoenix, AZ 85004 |

| AZ | Phoenix | (833) 333-7566 | 2133 W Peoria Ave, Phoenix, AZ 85029 |

| AZ | Phoenix | (844) 236-5024 | 20620 N 19th Ave, Phoenix, AZ 85027 |

| AZ | Tucson | (833) 333-8077 | 203 W Cushing St, Tucson, AZ 85701 |

| CA | Los Angeles | (919) 568-3832 | 4550 W Pico Blvd, Los Angeles, CA 90019 |

| CA | San Diego | (919) 568-3838 | 969 Ninth Ave, San Diego, CA 92101 |

| CO | Denver | (919) 568-3849 | 2540 Holly St, Denver, CO 80207 |

| FL | Jacksonville | (919) 568-3842 | 2199-2031, Clemson Rd, Jacksonville, FL 32217 |

| FL | Jacksonville | (833) 333-7466 | 111 N Julia St, Jacksonville, FL 32202 |

| ID | Idaho Falls | (833) 792-9000 | 1935 International Way, Idaho Falls, ID 83402 |

| IL | Mundelein | (833) 791-6000 | 24370 West Old Oak Dr, Mundelein, IL 60060 |

| IN | Indianapolis | (919) 568-3847 | 2998-2900, Boulevard Pl, Indianapolis, IN 46208 |

| KS | Overland Park | (833) 791-4000 | 7015 College Blvd Suite 375, Overland Park, KS 66211 |

| LA | Gretna | (833) 791-7000 | 401 Whitney Ave Suite 126, Gretna, LA 70056 |

| LA | New Orleans | (800) 768-2305 | 3520 General De Gaulle Dr #1035, New Orleans, LA 70114 |

| MA | Boston | (919) 573-8472 | 98-50 Turner St, Boston, MA 02135 |

| MI | Warren | (919) 568-3829 | 25879 Hoover Rd, Warren, MI 48089 |

| MI | Sterling Heights | (919) 568-3830 | 37399, 37201 Maas Dr, Sterling Heights, MI 48312 |

| MI | Waterford Twp | (833) 333-7266 | 2745 Pontiac Lake Rd, Waterford Twp, MI 48328 |

| MS | Jackson | (833) 333-8177 | 234 E Capitol St, Jackson, MS 39201 |

| NY | New York | (833) 336-0339 | 225 Broadway #3800, New York, NY 10007 |

| NC | Charlotte | (919) 568-3846 | 2399-2301, Warburton Rd, Charlotte, NC 28211 |

| OH | Columbus | (919) 568-3845 | 3462-3614, Greenwich St, Columbus, OH 43224 |

| OK | Oklahoma City | (833) 792-7000 | 7725 W Reno Ave #370, Oklahoma City, OK 73127 |

| PA | Philadelphia | (919) 568-3836 | 1501-1599, N Woodstock St, Philadelphia, PA 19121 |

| PA | Pittsburgh | (833) 792-3000 | 437 Grant St Suite 1240, Pittsburgh, PA 15219 |

| SC | Bluffton | (833) 333-8377 | 181 Bluffton Rd Suite F-202, Bluffton, SC 29910 |

| TN | Nashville | (919) 573-9217 | 666 Alley, Nashville, TN 37212 |

| TX | El Paso | (844) 236-5024 | Union Bldg East, El Paso, TX 79902 |

| TX | Houston | (919) 568-3834 | 10100, 10148 Sangerbrook Dr, Houston, TX 77038 |

| UT | North Salt Lake | (833) 333-7977 | 360 N Cutler Dr, North Salt Lake, UT 84054 |

| VA | Stafford | (919) 568-3831 | 59 Quarry Rd, Stafford, VA 22554 |

How Do I Cancel Lexington Law Membership Online

Unfortunately, there is no way to cancel Lexington Law services online.

I know this news is frustrating since most of us would prefer to click a couple of cancel buttons and fill out a quick feedback form.

The only way to cancel your membership with Lexington Law is to contact them by phone at: (800) 341-8441 between the hours of 7 a.m. – 7 p.m. (MST) Monday – Friday.

I have seen Lexington Law BBB responses to complaints that seem to indicate that you may also be able to cancel by email.

Lexington representatives refer to cancellations received by email in their responses to BBB complaints.

In any case, make sure that you receive confirmation of your cancellation in writing.

👉 Keep in mind that once you cancel they will bill you one final time on your monthly billing date because they charge for services after they are completed.

Lexington Law Alternatives

Understandably with everything going on with Lexington Law, you may want to consider another credit repair company.

Credit Saint received the best reviews of any company we looked at. They have been in business since 2004 and have an attorney as their founder. Read our review of Credit Saint to see why it’s our top pick.

Other companies we recommend are:

Credit Saint and The Credit Pros have an A+ from the Better Business Bureau and offer competitive pricing with unlimited disputes.

I’m very disappointed with Lexington. My credit score went from a 711 to 493. I have asked for services to be discontinued and the person I spoke to was doing and saying everything to keep that from happening. I received an email for a cash advance which the person I spoke to claims I was approved then they transferred my call to Lexington. I never heard from that person again and of course never received the advance. I spent two years repairing my credit and now it’s back to shit again and they’ve collected close to $600.00 from me!

I have been in jail for months now and Lexington law has charged me 129 dollars a month plus 19.95 cause I was broke instead of them stopping they kept on charging me and took well over 1000 dollars they are getting rich off fucking people over I will find a way to get my money back this can’t go on they are snakes

Lexington law is a rip off. They have taken over 2 grand from me in a year with promises unmade. I had excellent credit over 800, never late on bills and my ex husband used a charge in my name which I was never notified about until I found my credit score dropped to near 600 and dropping daily. My creditors were sending me letters, due to your delinquency, we are lowering your credit limit. I went online to credit reporting agencies and found my ex had me in collections on a bill I never new existed as he changed the address and phone number, so I was never notified. I gave no permission for him to use anything in my name as divorced long before the incident of this. When I figured out what was going on, I called the bank he charged and paid them the over 6K that was in collections for 4 months. To date, I have paid Lexington Law over 2 grand has been one year since occurrence and they have not fixed anything. I cancelled them today. Due to this, I am now over 8K I paid on something I never charged and have… Read more »

Is there really anything that the credit repair companies actually do that you can’t do on your own if you just go to the website for consumers about your credit score Experian or Transunion and the other one I can’t remember what it’s called but they have a lot of tools to help you keep your credit up because they like it when you have credit also what are the name of the companies that will give you a fake loan to help you build a positive credit history but also referred us to but we don’t know why they did that Lexington Law Lexington Law sucks Lexington Law

Truth spoken this place is a rip off.