If you have Jefferson Capital Systems on the phone or on your credit report, one of your debts has been sent to collections. This is a situation you need to deal with: they won’t just go away. Here’s how you can resolve the account and put your credit back in order.

Who is Jefferson Capital Systems LLC?

Jefferson Capital Systems, LLC., is based in Minnesota. They’re one of the largest third-party collectors in the US.

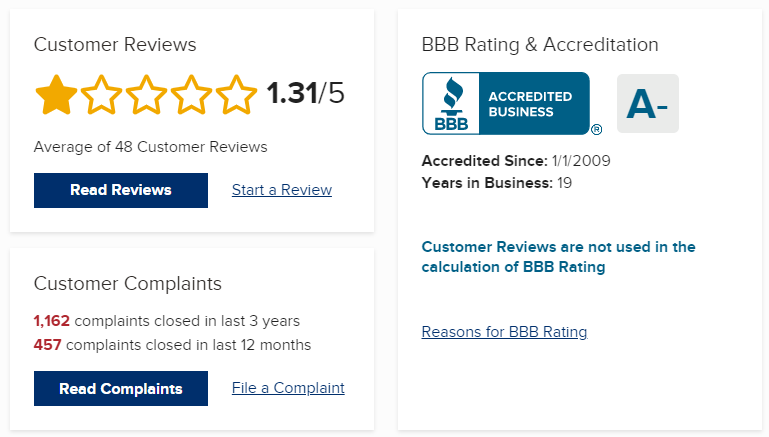

Jefferson has been accredited by the Better Business Bureau since 2005 and has a B rating from the BBB.

You’ve never heard of them?

I’m not surprised. Because they specialize in third-party debts, they buy past-due accounts from other businesses.

If you see Jefferson Capital Systems, LLC, JCap, “jeffcapsys” or “jeffersncp” on your credit report, your debt was sold to them by the original creditor.

If you have an account in collections, you have two challenges.

- You have to resolve the account. A collection agency will harass you and could even sue you as long as the debt is not resolved.

- You have to address the damage to your credit. Collection accounts are a serious drag on your credit score.

These two challenges are related, but they are not the same thing. One involves dealing with the collection agency, the other involves dealing with the three major credit bureaus: Experian, Equifax, and TransUnion.

Who Does Jefferson Capital Systems Collect For?

Collection agencies like Jefferson Capital Systems rarely disclose who they are collecting for. If you see Jefferson Capital Systems on your credit report, they might have acquired your debt from any financial institution, healthcare provider, educational organization, any type of business, or government organization.

Jefferson Capital Systems Reviews And Complaints

Reviews of Jefferson Capital Systems are overwhelmingly negative which is not unusual for a debt collection company. They have a 1.31/5 rating on their BBB page and a 1.6/5 rating on Google reviews.

At the time of this writing, they had over 1100 customer complaints filed on BBB alone. No complaints were unresolved or unanswered. Most complaints are from people that were unaware that their debt was sold to a collection agency or that had problems verifying their debt.

Here’s What You Can Do

📰 New Federal debt collection regulations took effect on Nov. 30, 2021. The new rules will have a far-reaching impact on the debt collection industry. If you have delinquent debts or accounts in collection these rules will affect you.

Learn more about Regulation F and what will it mean for consumers with debts.

If you’re hearing from Jefferson Capital Systems – or any collection agency – there are things that you can (and should) do. There are also two things that you should not do:

- Don’t panic. It won’t help.

- Don’t ignore the situation. That won’t help either. They won’t go away.

That’s what you shouldn’t do, but what should you do?

Here’s where to start.

1. Know Your Rights

The Fair Debt Collection Practices Act (FDCPA) spells out the rights of debtors and the obligations of debt collectors. Here are some key points.

- A debt collector cannot call you before 8AM or after 9PM.

- A debt collector cannot call your place of employment.

- If you have a lawyer, the collector must communicate with your lawyer.

- A debt collector may not communicate with your friends or family members or tell them about your debts.

- Debt collectors cannot threaten to harm you, your reputation, or your property, or use profane language.

- Debt collectors must identify themselves and the company they represent. They cannot claim to be law enforcement or other officials.

- A debt collector cannot threaten you with imprisonment or seizure of assets.

For a full review of your rights under the FDCPA see this summary from the Consumer Financial Protection Bureau (CFPB).

If you believe that a debt collector is violating the rules, you can report them to the FTC, the CFPB, and your state’s attorney general.

2. Validate and Verify the Debt

Under the new regulations that came into effect on Nov. 30, 2021, debt collectors must send you a Notice of Debt within 5 days of their first contact with you. This notice must contain much more information than the notices that collectors sent under prior rules.

If the notice is incomplete, it is invalid, and the debt isn’t collectible. That makes it important to know what’s required.

A valid Notice of Debt must contain an itemization date. This can be one of five different dates.

- The date of the last statement or invoice provided to the consumer by the creditor.

- The charge-off date.

- The date of the last payment applied to the debt.

- The date of the transaction that gave rise to the debt.

- The judgment date, if there is court judgment on the debt.

This date will help you establish whether the Statute of Limitations on the debt has expired and when it will drop off your credit report.

The Notice of Debt must also contain extensive information about the debt:

- The debt collector’s name and mailing address.

- The consumer’s full name and mailing address.

- If the debt is related to a financial product (like a loan or credit card), the notice must contain the name of the creditor to whom the debt was owed on the itemization date.

- The account number associated with the debt.

- The name of the creditor to which the debt is currently owed.

- The amount of the current debt and an itemized list of any payments made and added fees, interest, or other charges.

The Notice of Debt must contain a statement advising you of your rights under the Fair Debt Collection Practices Act (FCPA), including a statement that you have the right to dispute the debt within 30 days of receiving the letter.

The notice must also contain a returnable form allowing you to declare that you are disputing the debt and allowing you to select one of three reasons for a dispute:

- This is not my debt.

- The amount is wrong.

- Other (you will need to supply additional information.)

The CFPB has published a sample Notice of Debt that will help you determine whether the one you receive is complete.

Why It’s Important

Many debt collectors who purchased debts before the new regulations came into effect will not have the required information. They may not be able to get it from the original creditor. They may still try to bluff or intimidate you into paying them or admitting that the debt is yours.

If you receive a Notice of Debt, examine it in detail to make sure it complies with the law. If it doesn’t, inform the collector that you will not discuss the debt until you receive a Notice of Debt that complies with Regulation F.

Always Dispute the Debt

If you do not dispute the debt within 30 days, it is presumed valid. Always dispute debts held by collection companies.

If you are using a dispute or debt validation letter template, be sure that the template is designed for notices received after the implementation of Regulation F on Nov. 20, 2021. Much of the information that debtors used to ask for is now required in the Notice of Debt.

Send the debt collector a certified letter addressing these issues.

- Ask for documentation that verifies that you owe the debt, such as a copy of the original contract.

- Ask whether the statute of limitations on the debt has expired. The collector doesn’t have to tell you, but they can’t lie. If they won’t say, the statute of limitations may have expired.

- Ask whether the agency is licensed to collect debt in your state. Again, the collector is not allowed to lie. You can ask for the date of the license, the license number, and the state agency that issued the license as well.

- A copy of the last billing statement sent by the original creditor.

Send the letter to Jefferson Capital Systems by certified mail.

Once you receive the debt validation letter, you have 30 days to send your debt dispute letter.

Remember that even if you know the debt is yours, the more important issue is whether they know it’s yours.

Because guess what?

If they can’t prove it’s yours, they can’t collect it or report it to the credit bureaus.

They might not be able to come up with that proof. Remember, Jefferson Capital Systems purchased your debt, in bulk with a bunch of other debt, from the original creditor.

Who knows what was lost in the shuffle?

The onus is on them to provide proof. If they can’t, they’re required by law to remove it from your credit report.

Remember the Statute of Limitations

Always check the date of the debt against the statute of limitations in your state. If the statute of limitations has expired, the collector cannot pursue legal action against you.

The statute of limitations clock begins on the date when the debt was first reported as delinquent.

Remember that making a payment or acknowledging that the debt is yours can restart the statute of limitations.

The expiry of the statute of limitations will not remove an account from your credit record. If the statute of limitations has expired or will expire soon, there’s a good chance that the seven-year period of appearance on your credit record is also nearly up.

If the statute of limitations is nearly up, your best bet might be to just wait it out.

3. Stop Calls from Jefferson Capital Systems NOW

Before Nov. 20, 2021, you could get as many as 15 calls per day from a debt collector, according to a Consumer Credit Card Market Report.

That’s way too many.

That has changed. Regulation F places strict limits on collection calls.

- A debt collector cannot call you more than seven times within seven consecutive days.

- If a debt collector speaks to you on the phone, they must wait seven days before calling again.

Debt collectors can now contact you by email and text message as well, but you can tell them how they are permitted to contact you and when.

You can stop all communication from a debt collector.

Follow these simple steps to stop the calls.

- Write a “stop contact” or “cease” letter telling them to stop contacting you.

- Make a copy for yourself and mail the original to Jefferson Capital Systems.

- To prove you sent the letter, send it by certified mail with “return receipt requested.”

Make sure you follow these exact steps.

If you do, the National Consumer Law Center states, “the collector can only acknowledge the letter and notify you about legal steps the collector may take.”

When you stop the phone calls, you get some breathing room. Remember that you still owe the debt, and the collector can take legal action.

Then you can tackle the next step.

4. Contest the Debt With the Credit Bureaus

If you believe that you do not owe the debt or that the collection agency has failed to validate the debt, you can file a dispute with the credit bureaus. You will need to dispute the account separately with each credit bureau.

Credit Reporting Bureau Mailing Addresses

| EQUIFAX | EXPERIAN | TRANSUNION |

|---|---|---|

| P.O. Box 740256 Atlanta, GA 30374-0256 | P.O. Box 9701 Allen, TX 75013 | P.O. Box 2000 Chester, PA 19016-2000 |

You can also dispute it online:

The credit bureau must investigate and verify your debt. If they cannot, they must remove it from your credit record.

Remember that even if the debt is removed from your credit record, the collection agency can still pursue collection efforts.

Get Your FREE Credit Dispute Letter Template

Get our winning dispute letter, plus free tips to help you boost your credit.

5. Settle With A Pay For Delete Agreement

While occasionally the collection debt isn’t yours, most of the time, it is. If that’s the case, a settlement is one way to resolve the situation.

Remember that debt collectors pay, on average, 4 cents for every dollar of debt that they buy. That gives you room to negotiate. A collector can accept less than you owe and still make a profit.

An article from U.S. News & World Report found that collection agencies will settle for between 40-60% of the balance – which could mean thousands of dollars saved.

You might offer 10% of your balance to see what they say.

They’ll probably ask for more, but don’t let them push you around. With a little negotiation, you can reach an agreement you’re comfortable with.

Pay for Delete

A collection agency may agree to remove your account from your credit record if you settle your debt. This is a “pay for delete” arrangement.

When you discuss a settlement, ask the collection agency representative if they will delete your record if you pay. Send a formal “pay for delete letter” to confirm the arrangement and ask for a written commitment.

Remember that you cannot compel a credit bureau to remove a legitimate account from your record. It will be recorded as paid, but it may remain on your credit report for seven years from the date when the account first became delinquent.

A pay-for-delete arrangement is a gamble. It may not work, but it’s worth trying. If they accept the settlement, you will no longer have to deal with the collection agency, and that’s a big plus.

Get Your FREE Pay for Delete Letter Template

After much testing, we have put written a great pay to delete letter you can use to get started.

Hire A Credit Repair Company

If you don’t want to go through all the trouble of writing letters and negotiating with Jefferson Capital Systems on the phone, consider hiring a credit repair company to help.

A credit repair company is equipped to deal with aggressive debt collectors to help you get the best possible outcome.

The credit repair industry has earned a terrible reputation, and you’ll have to look out for disreputable companies and credit repair scams. There are still some companies that are legitimate and helpful.

Choosing to work with an expert sooner rather than later can save you a lot of time and money in the long run.

Get Professional Help

We analyzed 21 credit repair companies based on price, service, and results, and picked our top three choices.

Then you can sit back and relax while the credit pros do all the work.

If you’d rather do it yourself, that’s okay, too.

What If They Sue?

Collection agencies will take you to court, sometimes over quite small amounts. If a debt collector sues you, don’t ignore the case.

If you don’t respond, the judge will probably issue a summary judgment against you. You will be ordered to repay the debt. If you don’t, your wages could be garnished. In some states, your assets could be seized.

Not all companies will exercise their right to file a lawsuit against you, but a lawsuit is always a possibility when dealing with an aggressive debt collector.

⚠️ Important! Read up on what to do if you get sued by a debt collector to make sure you take all the right steps.

Free Yourself From Jefferson Capital Systems

Debt collectors will not go away on their own. They will keep harassing you, and you might end up in court. Running away is not an option.

Instead, take the initiative. Learn how to communicate with debt collectors and know your rights. You can control the process and the situation if you’re aware and proactive.

It’s not going to be a pleasant experience, but it will be a better experience if you’re in the driver’s seat!

Very informative article. But there is no need to glorify a bottom feeder. All this outfit does is buys old debt, for pennies on the dollar, then starts their less the minimum wage paid scam talkers to go to work, in hopes of a bonus after coercing some sort of payment. The best way to get rid of them is to call your own state's attorney general's office and report them. Oh I forgot, record their message and any conversation you had with them.

I claimed bankruptcy and put it in there but somehow it was sold to Jefferson llc so now I done remember which third party Verizon initially sold it too to get it off my report . Do you have any suggestions