Like any sophisticated area of study, the field of personal finance has evolved over the years. Innovative technologies have developed, new investment vehicles have emerged, and consumer attitudes have shifted significantly.

As a result, many modern best practices in personal finance are different from those proposed in previous decades. Analyzing the evolution of personal finance can help you learn some valuable lessons, as can finding the ideas that have stood the test of time.

To that end, I’m going to compare and contrast today’s financial wisdom with the ideas of Sylvia Porter, one of the original finance gurus, in Sylvia Porter’s Money Book: How to Earn It, Spend It, Save It, Invest It, Borrow It – And Use It To Better Your Life.

I know the title is a bit wordy, but the book was one of the most prominent personal finance books in the 70s, and it gives us a convenient framework. Let’s go through her recommendations on those five fundamental skills.

How to Earn

The section in Sylvia’s book that focuses on earning money revolves entirely around optimizing your career path. She spends an entire chapter on how to choose a lucrative, fast-growing occupation, finding job leads, writing cover letters, and nailing interviews.

Sylvia also acknowledges the benefits of a college degree but emphasizes that they’re not necessary for everyone. In fact, she’s quite firm on the stance that you can have a thriving career without higher education, even though credentialism was already on the rise in the 70s.

In some ways, her ideas are familiar. People still love to read about the best career tracks and imagine the possibilities. Modern best job lists focus on the same criteria Sylvia discussed, like potential salaries and the projected growth rate of the market.

📗 Learn More: Incidentally, we have some great occupation suggestions for you. Check out some of our favorite job lists: 10 Best Trade Jobs: Earn a Great Living Without a Degree + 15+ Part-Time, Work From Home Jobs That Pay Well.

However, one difference that jumped out at me was the noticeable absence of side hustle mania that’s rampant today. Sylvia warned readers about going into business for themselves, while modern personal finance is more about building additional income streams than optimizing your primary one.

Side hustling has become mainstream thanks to the invention of rideshare apps, home and auto-sharing platforms, and freelancing websites. More people are branching off on their own than ever before, with roughly 45% of Americans reporting a side hustle in 2021.

😃 Fun Fact: Sylvia also claimed that Americans were shifting toward a four-day workweek and that unions were pushing for 1,600-hour work years. She said, “This is a trend virtually sure to prevail in the years directly ahead.” Whoops.

What’s the Takeaway?

The increased accessibility of side hustles has been a boon for many Americans. It’s never been easier to supplement your income by moonlighting after finishing your nine-to-five job responsibilities.

However, it’s possible we’ve gone a bit too far. Nowadays, people often waste time on income streams that are unscalable at best and outright scams at worst. For example, it’s a tragedy that anyone tries to make money by taking surveys online.

Many of us could benefit from refocusing on optimizing our careers, just as Sylvia suggests. For example, you’d probably be better off fixing up your resume, switching to a new job, and negotiating a $10,000 raise than trying to build a furniture-flipping business in your free time.

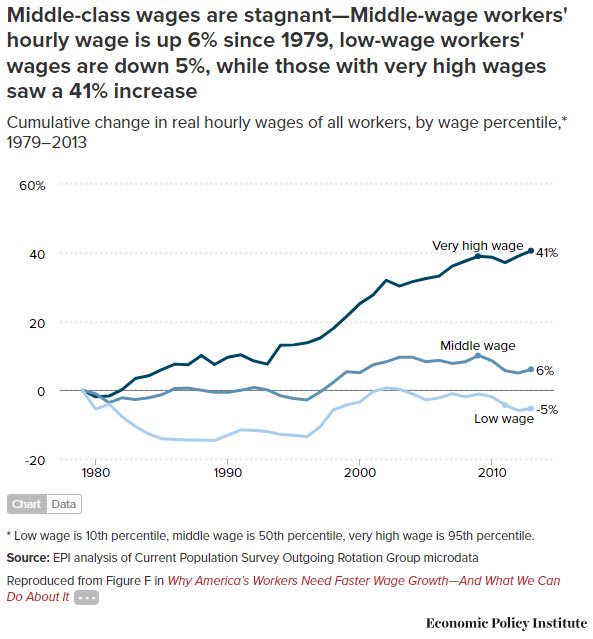

There’s another reason why side hustles have become so prominent. Wages have stagnated for many Americans.

Stagnant wages combined with the prevalence of student debt and the high costs of healthcare, housing, and other essentials led to the creation of an environment where many people simply can’t survive on their salaries.

How to Spend

Spending the right amount of money on worthwhile expenses is an underappreciated skill in the United States. It’s not as glamorous as hustling for a higher income, but the ability to live happily with less is one of the best financial superpowers that you can have.

Unfortunately, much of today’s personal finance wisdom takes it for granted that Americans are bad at saving money. Our annual savings rates have been dismal for decades, usually tracking well below the 15% to 20% that most experts agree is the minimum necessary to retire on time2.

📗 Learn More: Raising your savings rate is the key to shortening your time to retirement. Find out our favorite tips and tricks for retiring earlier: How to Retire Early: The Shockingly Simple Path to Freedom.

As a result, most modern budgeting advice comes across as a desperate plea for people to get their spending habits under control. People like me create budget methods, frugality hacks, and temptation avoidance strategies to help trick people themselves into spending less.

While Sylvia spends some time on these ideas, she also emphasizes the importance of addressing the mindset behind your spending habits. In one of my favorite sections of her book, Sylvia suggests:

“Start from the premise that no income you will earn will ever be large enough to cover all your wants. Accept the theory that the more income you have, the greater will be your desires. Make up your mind that if you want something badly enough, you will sacrifice other things for it.

Take the trouble to think out your own philosophy of living and your ambitions for the future. Develop a plan of control over your spending. Then you will make progress toward the kind of living which means most to you.”

What’s the Takeaway?

It’s possible some people fail to stick to their budget because they’re using the wrong system. However, I find it more likely that most people who struggle with their budget would do so no matter what template they follow. In reality, all budgets work. You just need the discipline to stick to them.

Instead of trying for the umpteenth time to find the perfect tool or trick to get you to stick to a spending plan, you may benefit more from revisiting your needs, motivations, and ambitions. Ask yourself questions like:

- What lifestyle can you realistically afford that would make you happy?

- Which expenses are non-negotiable, and which ones are you willing to sacrifice?

- What goals are dearest to you, and how much do you need to save to reach them?

With these answers in mind, you’ll have a much easier time creating a budget that meets your needs without sacrificing your happiness. Understand yourself and define your goals as Sylvia suggests, and then budgeting becomes easy.

How to Save

Saving money is closely related to spending it. However, there’s enough separation between the two that they deserve their own sections. Sylvia spends a significant amount of time in her book getting into the weeds of saving, including:

- How much you should have saved in cash

- What types of accounts are best for storing cash

- How to shop for a bank or credit union

Some of Sylvia’s ideas are less relevant in the modern world, where you can peruse savings account options online alongside scores from other users and interest rates. However, there’s still a lot of discussion today around optimizing your approach to savings.

For example, the debate around the proper emergency fund size is as contentious as ever. In addition, many are scrambling to find places to store cash that will generate a high enough yield to protect them against inflation without undue risk.

Though Sylvia bases her emergency fund calculations on monthly income instead of using the modern expense approach and recommends banking products that are outdated, the concepts behind her advice are consistent with modern ideas.

In essence, you should keep enough cash on hand to weather emergencies. Store those funds somewhere you can access them quickly and without market risk, but try to minimize your exposure to inflation as much as possible.

👉 Quick Insight: I-Bonds are an attractive option in today’s high-inflationary environment. If you buy before October 22, 2022, you’ll receive a guaranteed yield of 9.62% for the first six months. You can buy up to $10,000 per calendar year online: Individual – Buying Series I Savings Bonds.

What’s the Takeaway?

Though the specifics of Sylvia’s recommendations differ slightly from some of today’s saving wisdom, the principles are the same. My key takeaway is that you can’t overstate the importance of maintaining a healthy emergency fund.

When you live paycheck-to-paycheck, you’re incredibly vulnerable. A single unexpected expense could force you into debt, which can be the beginning of a spiral that’s often very difficult to rectify.

So don’t take that risk. Make it a priority to keep enough cash on hand to cover at least a few months of your expenses. If you ever have to dip into your emergency fund, rebuild it as soon as possible to minimize your exposure.

How to Invest

Investing is arguably the most expansive area of study in personal finance. There are so many different investment accounts, vehicles, and strategies that it’s tough to compare specific best practices. Instead, I’ll focus on higher-level concepts, which are easier to identify.

For example, Sylvia emphasizes the idea that everyone should begin investing for retirement as soon as possible. Compound interest is one of the most powerful forces in existence, and everyone should learn to harness it. This investing concept is still fundamental today.

Sylvia also recommends dollar-cost averaging, which involves purchasing investments regularly over long periods to avoid the chances that you’ll enter markets at unfavorable moments. That’s still the most popular approach to acquiring securities among personal finance experts.

Beyond these high-level concepts, Sylvia’s suggestions differ from much of today’s leading investment advice. There’s good reason for that, though. Namely, Sylvia wrote for an audience of active investors because that was the only option in the 70s.

In modern times, much of the personal-finance gospel on investing promotes passive investing in index funds instead. Studies have repeatedly shown that active investors struggle to beat market returns and most stock traders lose money. 71% of U.S. investors now say index funds work better than stock picking.

As a result, passive investing in the United States’ domestic equity-fund market overtook active investing in 2018 and accounted for approximately 54% of the market share by 2021. If trends continue, passive investing, in general, is likely to overtake all active investing by 2026.

What’s the Takeaway?

If there’s a lesson to learn from the evolution of investing since the 70s, it’s that you should pay particularly close attention to this aspect of your personal finances. It’s the most complex and the fastest-changing. Market conditions, tax laws, and your risk tolerance will change significantly over time, and you have to adjust.

It’s also breathtakingly easy to lose your hard-earned savings by investing in the wrong assets without sufficient education, so don’t take anybody’s word for granted. Spend the time to do your own due diligence and optimize your investing approach, as it can make or break your finances.

How to Borrow

Last but not least, let’s look at the evolution of the best practices around borrowing money and managing credit. I was pleasantly surprised by Sylvia’s take on the subject, as she approaches it from a noticeably different angle than most modern advice.

Nowadays, there’s a general assumption that most people carry significant amounts of debt. We take student loans, auto loans, and credit card debt as a given, and a lot of personal finance wisdom assumes you have them as a starting point.

As a result, most content on the subject focuses on debt paydown strategies, relief options, and ways to rebuild your credit or finances in the wake of debt. However, there’s a refreshing absence of this attitude in Sylvia’s book.

Instead, she emphasizes the importance of understanding the following:

- The right and wrong reasons to borrow money

- How to recognize when you’re nearing unmanageable debt levels

- The significance of borrowing costs and the value of paying with cash

If you must take on debt to finance an expensive but meaningful purchase like a home, Sylvia also preaches the importance of minimizing its burden on your finances. As she says, there’s always a cost to borrowing money, but you can reduce it significantly by paying more upfront and pursuing shorter repayment terms.

What’s the Takeaway?

Debt is one of the primary reasons people in the U.S. struggle financially despite having a stable income. Too often, we assume that the burden of debt is unavoidable or acceptable, then do our best to dig ourselves out on the back end.

While it’s unrealistic to expect everyone to get through life debt-free, many of us could benefit from working harder to avoid borrowing in the first place. Think twice before you take out a loan or charge something to your credit card.

When possible, try to save up cash and pay for things outright. If you don’t have time to wait, try to look for an alternative good or service that can get you what you need without forcing you to go into debt. If there’s no other option, calculate the price of your purchases after financing costs and ask yourself if it’s still worth it.

📗 Learn More: People assume they have to take on student loans to get an education, but that’s not necessarily the case. You can find other ways to pay your college tuition or attend trade school instead. Check out our guides to both subjects: College Without Debt: Where to Get Help Paying for College + Trade School or College? What’s the Difference? Pros and Cons of Each.

😳 Reality check: One of the most effective ways of wrapping your head around the true price of a purchase is to consider the number of working hours a purchase is worth. Try our price to hours worked calculator to see just how much time you’d have to work in order to pay off a purchase. And then ask yourself if it’s really worth it.

What’s Different?

Sylvia Porter’s Money Book was the personal finance gospel of the 1970s. How well does it hold up today?

Some Things Change

Obviously, some things have changed. For example, modern personal finance discourse revolves heavily around credit scores and how to understand them, improve them, and protect them.

Sylvia doesn’t mention credit scores because they didn’t exist in any organized fashion when she wrote her book: the first FICO score wasn’t introduced until 1989.

Modern personal finance offers many tools that were unknown in the 1970s. You couldn’t prequalify for credit online or open an account with an online discount broker. Today’s methods are very different, even when the goals are similar.

Some of the prevailing assumptions have changed, as have many costs. Housing, health insurance, and student loan payments take up much bigger chunks of the average budget today than they did in the 1970s. We can no longer assume that an average household can survive on one salary, or even two.

Some Things Don’t

Despite the many changes, the core principles of personal finance in the 1970s are in many ways very similar to the core principles today. Budgeting, saving, managing your spending and separating wants from needs are all just as important today as they were in the 1970s.

Investing early is still good advice. Keeping debt to manageable levels and using credit only when you really need it is still a very sound policy. “Spend less than you earn” has been a good idea for centuries.

Overall, while the methods and the environment have changed, the core principles have remained very consistent.

Further Your Education

There’s a lot to learn in the personal finance world, and the landscape is forever changing. However, the American education system doesn’t do the best job of teaching you how to manage your money. That means it’s on you to find and fill the holes in your knowledge.

Fortunately, you don’t have to do it alone. Whether you need to learn how to earn, spend, save, invest, or borrow, FinMasters is here to help. Take a look at our library of resources below, and if you still have a question you’d like us to answer, contact us!