A hard inquiry can damage your credit. If you find hard inquiries on your credit report that you didn’t authorize, a credit inquiry removal letter can help you get rid of them and give your credit score a quick boost. Here’s how you can compose a credit inquiry removal letter that will get the job done fast and easily.

What Is a Credit Inquiry Removal Letter?

A credit inquiry removal letter is a tool that you’ll use to remove an unauthorized hard inquiry on your credit report. This letter requests the credit bureau to remove the inquiry, asserting that it was not authorized by you. We’ll explore how these unauthorized inquiries can appear on your report, steps to address them, and actions to take if they result from identity theft.

How to Write a Credit Inquiry Removal Letter

When you write a credit inquiry removal letter, there is some key information that you’ll need to include. For example, you’ll need to provide your personal information, information on the inquiry you are disputing, and your official request to open an investigation (dispute).

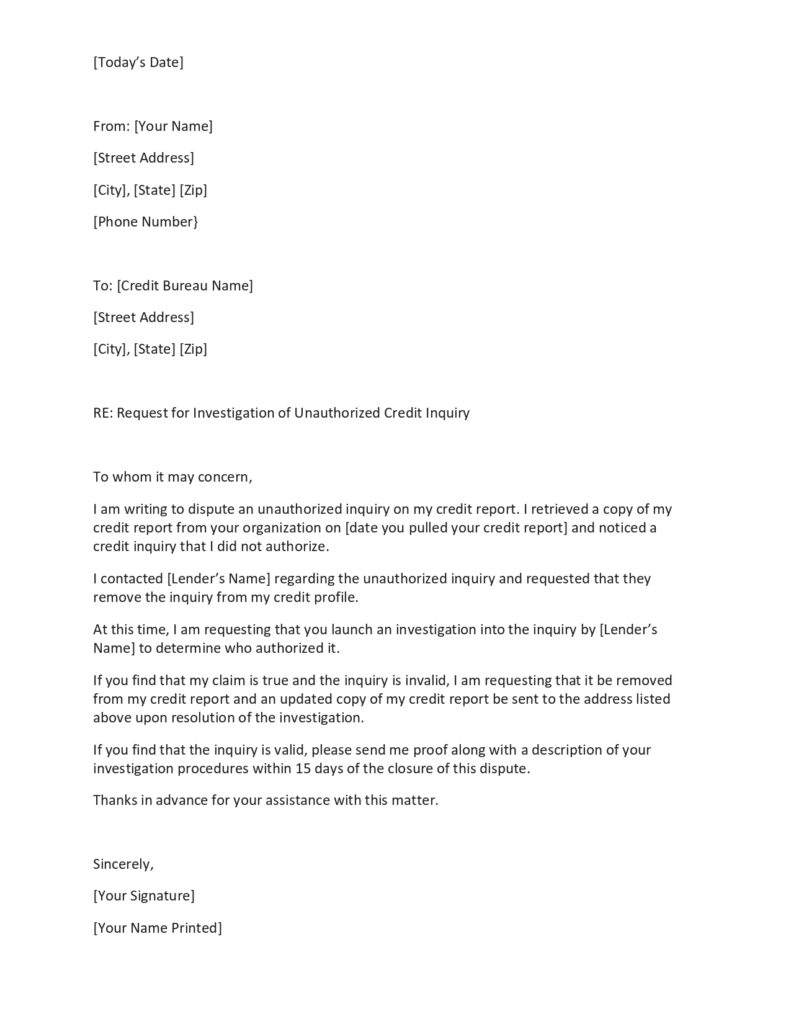

Below is a sample credit inquiry removal letter to help you get started.

[Today’s Date] From: [Your Name] [Street Address] [City], [State] [Zip] [Phone Number} To: [Credit Bureau Name] [Street Address] [City], [State] [Zip] RE: Request for Investigation of Unauthorized Credit Inquiry To whom it may concern, I am writing to dispute an unauthorized inquiry on my credit report. I retrieved a copy of my credit report from your organization on [date you pulled your credit report] and noticed a credit inquiry that I did not authorize. I contacted [Lender’s Name] regarding the unauthorized inquiry and requested that they remove the inquiry from my credit profile. At this time, I am requesting that you launch an investigation into the inquiry by [Lender’s Name] to determine who authorized it. If you find that my claim is true and the inquiry is invalid, I am requesting that it be removed from my credit report and an updated copy of my credit report be sent to the address listed above upon resolution of the investigation. If you find that the inquiry is valid, please send me proof along with a description of your investigation procedures within 15 days of the closure of this dispute. Thanks in advance for your assistance with this matter. Sincerely, [Your Signature] [Your Name Printed]

Download credit inquiry removal letter templates:

⏬ Credit inquiry removal letter template for Microsoft Word

⏬ Credit inquiry removal letter template for Google Docs

⏬ Credit inquiry removal letter template in PDF

Once this letter is complete, you can mail it to the appropriate credit bureau. Each bureau may have additional requirements for what information you need to send with your dispute letter. This can include proof of identification, your social security number, proof of residence, etc.

While it doesn’t cost anything to initiate a dispute, it is highly recommended that you send your letter by certified mail; this way, you have clear documentation of when it is received.

You can send your letter and copies of other required documents to the three credit bureaus at the following addresses:

Experian

P.O. Box 4500

Allen, TX 75013

Equifax Information Services, LLC

P.O. Box 740256

Atlanta, GA 30374-0256

TransUnion Consumer Solutions

P.O. Box 2000

Chester, PA 19016

Why Should You Be Concerned About Unauthorized Inquiries?

A hard inquiry or hard pull occurs when a creditor or lender checks your credit

👉 Nobody can make a hard inquiry on your credit report unless you authorize it. Usually, your signature on an application form authorizes the hard inquiry. Any hard inquiry that is not supported by your signature is unauthorized.

It’s important to understand the difference between hard inquiries and soft inquiries. Soft inquiries may be made without your authorization. You’re the only one who can see them and they don’t affect your credit.

Hard inquiries will affect your credit. They are part of the New Credit portion of the FICO score calculation. Having too many inquiries can indicate to a creditor that you are financially unstable.

When you’re looking for unauthorized inquiries on your credit report you are concerned with hard inquiries. An unauthorized hard inquiry can hurt your credit score. It could also be an early warning of identity theft.

How to Tell if an Inquiry Is Unauthorized

If you are not already signed up for a credit monitoring service, it can be difficult to spot a fraudulent or unauthorized credit inquiry.

You will start by pulling your credit reports. Not just one, but all of them. Many lenders will pull just one credit bureau when making a hard inquiry, so you will have to search through all of your reports.

Hard inquiries will appear in your credit report’s Inquiries/Requests for Your Credit History section. Each inquiry will display the lender that performed the inquiry along with the date the inquiry was completed.

💡 If you don’t immediately recognize the inquiry, a good first step is to contact the lender listed. They will be able to help you confirm why your credit was pulled and who authorized it.

If the inquiry was a simple mistake, i.e., someone typed in the wrong social security number, they should be able to resolve the error for you. You may have also authorized an inquiry without realizing it.

If the lender confirms that the inquiry was unauthorized and not a clerical error, you will need to remove the inquiry from your report (dispute) and take steps to prevent future fraudulent activity.

Dispute a Hard Inquiry Online

All three major credit bureaus support initiating a dispute online. Starting an online dispute can save you time and money over initiating a dispute by mail or via phone.

To begin a dispute, you’ll need to create an account with the credit bureau. This account will allow you to initiate disputes, upload documents, and check on the status of your dispute.

Once you create an account, you can file a dispute. The credit bureau will then review the information, ask you for supporting documentation as needed, and communicate with the lender to obtain further information. For full details on creating an account and initiating a dispute, check the dispute webpage for each credit bureau.

💡 Some credit bureaus offer additional features with an account, such as setting fraud alerts, viewing updated credit reports, etc.

How Long Will the Dispute Take?

A dispute can be resolved in a few short days if the lender agrees with the dispute and replies to the credit bureau quickly. The Fair Credit Reporting Act requires the credit bureau to respond to your dispute in writing within 30 days.

If the dispute results are in your favor, the unauthorized inquiry will immediately be removed from your credit report. If the dispute results are not in your favor, you can always try re-initiating a dispute with additional documentation of your claim.

Halting Future Fraudulent Inquiries

When you find fraudulent inquiries on your credit report(s), you’ll want to take steps to prevent future fraudulent inquiries as you begin the dispute process. You’ll have to assess the situation. Was there one unauthorized inquiry or many? Did someone actually open an account in your name?

👉 If you determine that identity theft occurred, your first stop should be the Federal Trade Commission’s identity theft website. You’ll find full instructions on how to report and recover from identity theft.

Some of the actions you can take include:

- Filing a police report

- Sending an identity theft complaint to creditors and banks

- Notifying the credit bureaus of fraudulent activity

- Place a fraud alert on your credit

- Setup a credit lock or credit freeze

- Utilize identity theft insurance and restoration services

Most importantly, you’ll want to continue to monitor your credit reports for any future fraudulent activity.

Will Disputing an Inquiry Improve Your Credit?

In the case of fraud, it is always important to take steps to investigate the unauthorized inquiry as this can help prevent future fraudulent activity. There is no guarantee that disputing the inquiry will impact your credit score. FICO estimates that a single inquiry has less than a 5 point impact on your credit score.

Hard inquiries are part of what makes up the New Credit portion of your credit score. However, this factor accounts for only 10% of your overall credit score. Not all hard inquiries are weighted the same way. Newer inquiries have the most significant impact. Once inquiries are 1 year old, they no longer affect your credit score. And after 2 years, they fall off your credit report.

Final Thoughts

When you are suffering from identity theft or fraud, having a hard inquiry removed from your credit reports is likely the furthest thing from your mind. And that is okay. You may choose to address the fraud first and worry about fixing your credit later.

But once you do get around to initiating disputes with the credit bureau(s), the process is thankfully simple. You can file a dispute by mail or online yourself, free of charge, and you are guaranteed a response within 30 days.

So don’t stress out. Initiate the dispute and the problem should be solved quickly.

More Letter Templates

Our collection of free, fully-customizable letter templates is there to help you write effective letters when you need to set up, cancel or complain about something.