It’s important to keep track of your credit score. It’s a financial report card that can give you an idea of how well you’re managing credit accounts. It can also have a dramatic impact on the rates you pay for loans and credit cards.

Did you know you have more than one FICO score, and lenders can use different FICO scores for different loan types?

Most lenders use FICO scores, and different lenders use different ones. There’s one place to access ALL of your scores and the other information you need to stay on top of your credit game. It’s called myFICO.

MyFICO

MyFICO is the only platform that allows you access to all your FICO scores. The biggest advantage of myFICO is that you get an in-depth, full picture of your credit profile. The downside is that the service is not cheap, with the most basic plan starting at $19.95 per month.

Pros

Access to all 28 FICO scores

Credit monitoring included

Identity theft protection included

Cons

The cheapest plan includes only one bureau coverage

High price

MyFICO Review: What Is MyFICO?

MyFico is the official consumer division of FICO, the company that invented the credit score. That makes MyFICO the most comprehensive way to check your credit score. The app makes it easy to check all of your FICO scores and much more, which can help you get and keep your credit on track. The service includes:

- Your FICO scores

- Credit scores for mortgages, auto loans & more

- Credit reports

- Credit monitoring

- Identity theft insurance

- 24/7 identity restoration

It’s a comprehensive approach to monitoring your credit file.

What You Need To Know About FICO Scores

If you apply for a car loan, home loan, or credit card, your credit score will have a lot to do with your approval and the rates you’re offered. Your credit score even makes a difference if you’re applying for a new cell phone account, home or auto insurance, or even a new apartment. And do you know what?

☝️ FICO scores are used by 90% of lenders when making lending decisions.

We already talked about there being more than one type of FICO score. But did you know, FICO scores come in 28 different varieties? And the only way to access all of them is through myFICO.

Why MyFICO Is The Top Dog For Credit Scores

FICO, short for the Fair Isaac Corporation, is the original creator of the credit score. Because they were the first, FICO is recognized as the industry standard for analyzing risk for lenders and other financial services.

I can hear you now: “My credit card issuer gives me a FICO score for free, isn’t that the same thing?”. Well, yes and no. Remember I said several FICO scores exist? Your bank or credit card company gives you access to just one out of the 28 available options.

For instance, Wells Fargo provides your FICO Score 9 from Experian, while Discover shares your FICO Score 8.

👉 You can’t rely on one credit score when lenders can look at any of the 28.

When you use myFICO, you get quick and easy access to the same scores that lenders can see.

MyFICO vs Credit Karma

Credit Karma is a well-known name in the credit score arena. The biggest difference between myFICO vs. Credit Karma is that Credit Karma doesn’t give you a FICO score.

☝️ Credit Karma gives you a VantageScore. And it can be very different from FICO’s scores.

So, is Credit Karma safe to use? It depends on your goals. Because you don’t get a FICO score, it’s hard to know whether you could qualify for an auto loan or home mortgage. You won’t be looking at the score that your lender is looking at.

If you’re just curious about your credit score, Credit Karma isn’t a terrible option. Just know that it could be different from your FICO score by as much as 100 points.

MyFICO vs Experian

Experian has a lot of good things going for it. The company has a long list of services to help you monitor, repair, and rebuild your credit. A free Experian membership gives you access to your credit score. It’s even a FICO score! But again, it’s just one of the many FICO scores out there.

How Much Does MyFICO Cost

Like most credit monitoring services, myFICO isn’t free. You could use the free FICO Scores Estimator tool to get a ballpark idea of your FICO Scores. And the myFICO community forum is an excellent place to get insight from others to understand credit scoring and advice on handling certain situations.

But the real value comes with a paid membership. You can choose from three subscription plans starting at $19.95 per month. More advanced plans are $29.95 and $39.95, so the cost depends on how much you want to know about your credit file.

No matter which tier you choose, every membership comes with:

- FICO Scores

- Scores for mortgages, auto loans, and credit cards

- Credit reports

- FICO score monitoring

- Credit alerts

- Identity restoration

- FICO Score Simulator

- “How lenders view you” tool

- Education and community support

That’s an impressive package, but you’ll have to decide whether you really need it.

Is It Worth It?

MyFico provides a comprehensive package: all your FICO scores, credit report access, credit monitoring, and identity theft protection. The question is whether the average American consumer really needs all that.

Your FICO scores from the three major credit bureaus may vary: not all creditors report to all three credit bureaus. For most people, though, periodically checking a single FICO score is probably enough, especially when you can check your credit score for free.

If you’re trying to repair your credit, you’re at high risk of identity theft, or you have a reason to want to track every aspect of your credit file, a MyFico subscription will get you what you want to need. If you don’t have those needs, you’re probably buying more information than you need and more than you can effectively use.

MyFICO Review: The Bottom Line

The biggest advantage of myFICO is that you get an in-depth, full picture of your credit profile. If you’re about to make a major financial decision – buying a house, refinancing a loan, or buying a new car – the service is valuable.

If not? It’s still an excellent way to get a personalized analysis of your credit score. A myFICO membership gives you the most comprehensive look at your credit standing that you can get.

FAQ:

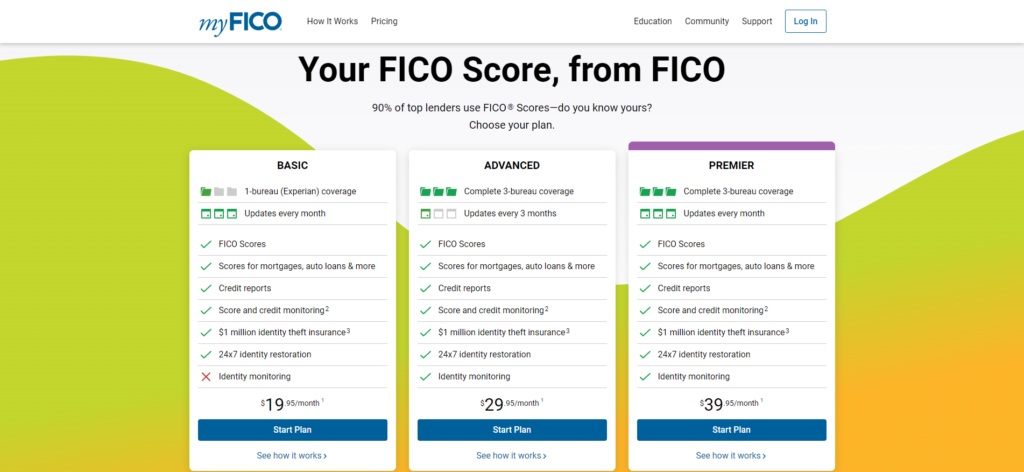

MyFICO offers three subscription plans which vary in bureau coverage and update frequency:

– Basic, $19.95/month, 1 bureau (Experian), updates every month

– Advanced, $29.95/month, 3 bureaus, updates every 3 months

– Premier, $39.95/month, 3 bureaus, updates every month

If you go for the $19.95 subscription plan or the $39.95 one, your score will update every month, whereas if you get the $29.95 plan, your score will update every 3 months.

Checking your credit with myFICO will not affect your FICO Scores.

You may cancel your subscription online via the My Subscriptions page, or via the Subscription screen on the iOS or Android app. You can also call at 1-800-319-4433. (Monday – Friday 6:00 AM to 6:00 PM PT or Saturday 7:00 AM to 4:00 PM PT).