April 19th, 2021

Quick Stock Overview

Ticker: JOUT

Source: www.stockrover.com

Key Data

- Sector: Consumer cyclical

- Sales ($M): 632

- Industry: Leisure

- Net Cash per share: $15.49

- Market Capitalization ($M): 1,530

- Equity per share: $39.42

- Employees: 1,200

- Debt / Equity: 0.1

- Interest coverage: 651.9

Summary

Johnson Outdoors is a manufacturer and seller of outdoor sports equipment, with a strong focus on fishing gear. It is a solid brand in its main sector, and also branched out in other outdoor sports. This is a family firm, with 3/4 of the shares still owned by the Johnson family. By far its main activity is in the fishing segment, with a presence in other water- and fishing-related sports like diving and kayaking. It is also active in camping (cooking accessories and tents).

GD sectors of activity (source: johnsonoutdoors.com)

Strategic Analysis

Johnson Outdoors (JOUT) is steadily growing in a sector with increasing popularity. Quality of life in large cities has taken a severe hit in 2020 with the COVID-19 pandemic. So outdoor sports, especially out at sea or lake, away from sanitary restrictions, have prospered.

As you will see in the quantitative analysis, the company has experienced very strong and steady growth over the last years even before COVID-19.

A Large Addressable Market

The addressable market is massive, with 50 million Americans participating in fishing activities in 2019 for a $13.4 billion global market size. While Johnson is mostly selling in the US, it has room to expand to overseas markets and other markets like the camping sector. Americans are spending no less than $887 billion per year in outdoor sports, according to the OIA (Outdoor Industry Association). This includes $14 billion in water sport gear and $20 billion in nature trail gear in 2017.

Outdoor sports gear is a highly fragmented industry ripe for consolidation by strong and recognized brands. As a leader of the segment with strong brands and intellectual property, Johnson should be able to keep growing and expand into new segments. With only $600 million in sales in 2019, this leaves plenty of room for Johnson Outdoors to keep growing, even if it stays in the water sports and camping sectors only.

It is also worth noting that while Johnson Outdoors sells mostly through retailers, it also has direct e-commerce channels, and that these channels have been performing well during the pandemic and lockdowns, with malls closed.

Source: mordorintelligence.com

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

Johnson Outdoors has been operating for almost 50 years, and is controlled and operated by the descendants of the founder, Sam Johnson.

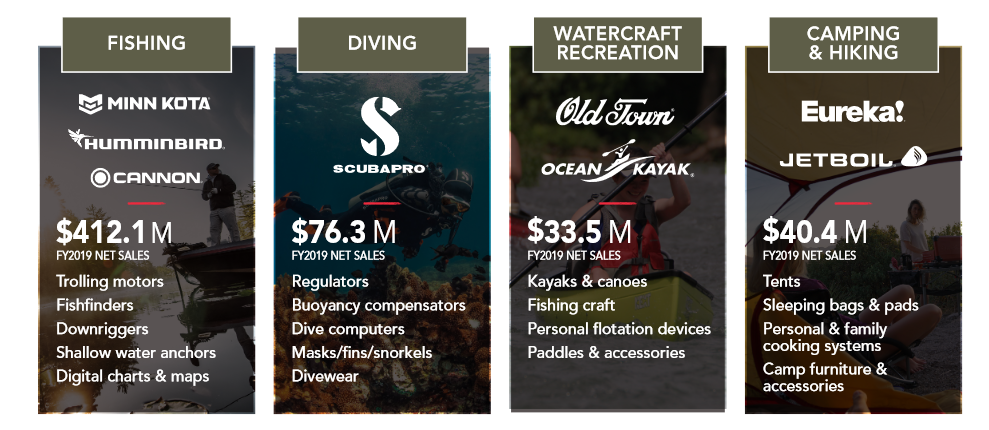

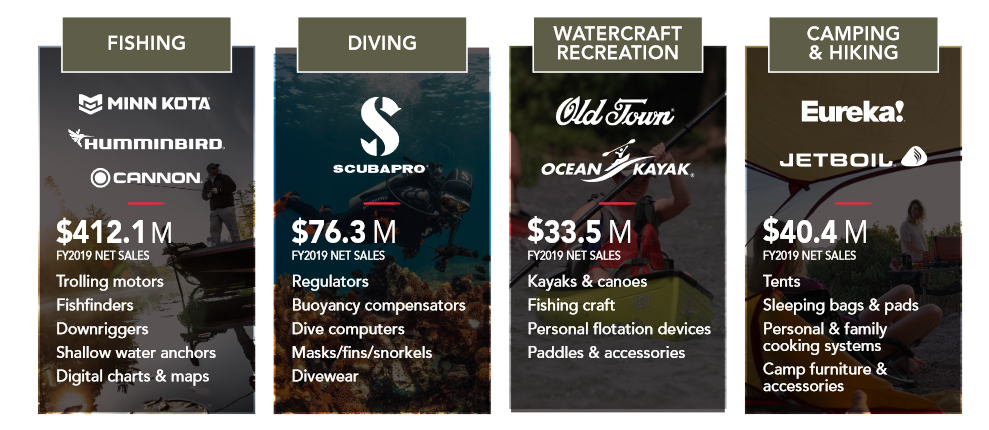

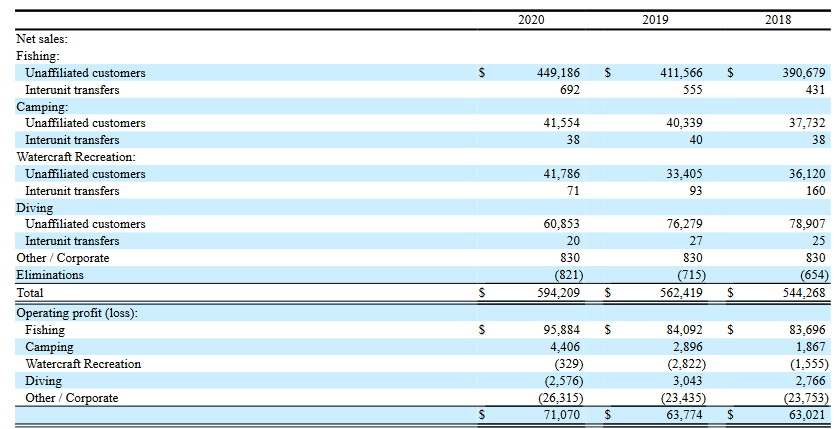

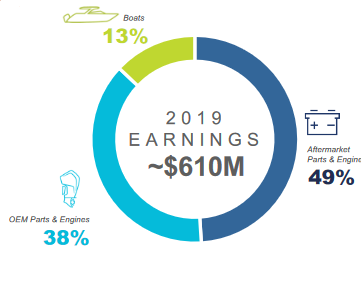

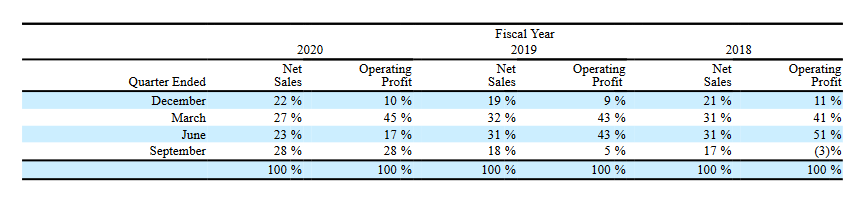

Sector Products Sales ($M) in 2020 Percentage of total revenue in 2020 Operating margin in 2020 Fishing Anchors, water radar, motors, maps 449 75% 21.3% Diving Dive computers, divewear, regulators 60 11% -4.2% Watercraft Kayaks, fishing craft, accessories, personal flotation devices. 41 7% -0.7% Camping & Hiking Tents, sleeping bags, cooking burners 41 7% 10.6%

It is worth noting that in 2019, diving was with a profit margin of 3.9% instead of a loss. This is an effect of the pandemic as travelling to diving destinations stopped, and should allow Johnson’s diving sales to get back to generating a profit of $2-3 million when the situation is back to normal.

Source: johnsonoutdoors.gcs-web.com

Geographically, JOUT is not really diversified, with only 12% of revenues out of the USA, of which 5% in Euros and 5% in Canadian Dollars and only 2% in other currencies. This obviously means that the company is mostly exposed to the American consumer spending, but also gives a large space to grow abroad, even if the American market was getting saturated.

Economic Moats

In value investing terms, Johnson Outdoors has several economic moats:

Brand

Sports and outdoors enthusiasts are ready to spend large sums to get good quality, reliable, sturdy and durable equipment to enjoy their hobby. Ask any hiking or fishing enthusiasts about their gear, and they will be delighted to discuss for hours the respective merits of different brands and designs. Outdoors activities are tough on devices and tools, as they are exposed to extreme hot or cold, salt water, tears and shock. This means that any serious hobbyist will have learned to prefer branded, reliable goods to cheap knockoffs. And when they find one they can trust, they stick to it for years or even decades.

Johnson’s financial results and price range seemed to indicate they are positioned in the upper part of the market, but not the most expensive either. I still checked their online reviews, and the typical listing shows the product quality as well as the money Johnson consumers are ready to spend. For example, these two frequently sold together products on a retail platform I am sure you will recognize.

Source: amazon.com

On top of being a brand known for the quality of its products, Johnson also cultivated a friendly, non-corporate, family-owned image that aligned perfectly with the value of its customers. After all, how many $1 billion companies are communicating this way?

The team member page showing them in shorts, backpack and wearing video game T-shirts

Source: johnsonoutdoors.com

A perfectly serious and normal head image for a corporate website

Source: johnsonoutdoors.com

Interestingly enough, the product quality speaks for itself in another way. While Johnson is essentially a B2C brand, it also supplies the US military with tents and other outdoors equipment, for a total of no less than $200 million in 2015 (with deliveries spread over several years), after multiple other successful tenders in 2004, 2005 and 2009. This is an area that the company has identified as a possible growth segment since at least 2017. This is the kind of positive surprise the shareholders of a quality company, selling sturdy and reliable products, can expect.

The military sales have decreased in 2020 compared to 2019, but this does not mean that further tenders will not be won down the road, just that government contracts tend to be irregular and do not fit the neat quarterly expectations of Wall Street.

Intangible Assets

Johnson Outdoors is re-investing a significant part of its profits into R&D, which produces valuable patents, supporting the performance and quality expected from a high-end brand.

For example, there are thousands of different designs of camping burners. But how many can – like the Jetboil – promise to boil water in just 100 seconds, while staying light, compact, efficient and durable? I would bet that once a camper got used to this kind of performance, he will never settle again for anything less. Especially if the price is still reasonable.

Source: johnsonoutdoors.com

R&D has been $24 million in 2020 (compared to a net income of $54 million), up from $20 million the previous years, so JOUT is definitively investing in the future of its product line and is likely to stay ahead of the competition.

Management

Being a family-owned business, Johnson Outdoors’ management is naturally expected to have the interest of the company at heart. The steady growth and attention to quality and branding reflect this, so this should not be a concern for an outside investor.

However, this also means that minority shareholders (so everybody but the Johnson family) might be at risk of the majority shareholders handling the company for its own profit, instead of benefiting all shareholders. This is commonly happening through excessive management compensation, stock options and other rewards for management from the pocket of the other shareholders.

For all practical purposes, the Johnson family’s control of the company is absolute, and this is something the other shareholders will probably have to accept permanently.

Source: johnsonoutdoors.gcs-web.com

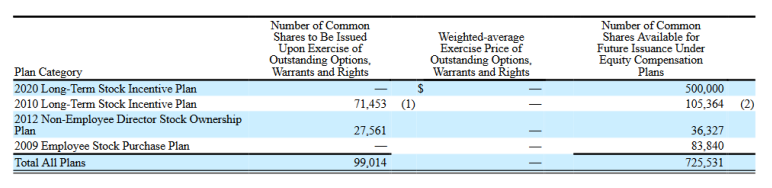

At the moment, there are around 10 million outstanding A and B-class shares. The long-term incentive plan for management and employees over the last 11 years have represented around 100,000 options and warrants, and 725,000 other shares available for future issuance. If they are all issued, it would represent a total of approximately 8% dilution over 11 years. So nothing out of the ordinary in management rewards for a company that has experienced an exceptional growth and financial performance.

Obviously, a reduction of the share compensation and an increase in dividends would be preferable for non-controlling shareholders, but this is also not a situation where the founding family is funneling all the company money out into their personal wealth.

Source: johnsonoutdoors.gcs-web.com

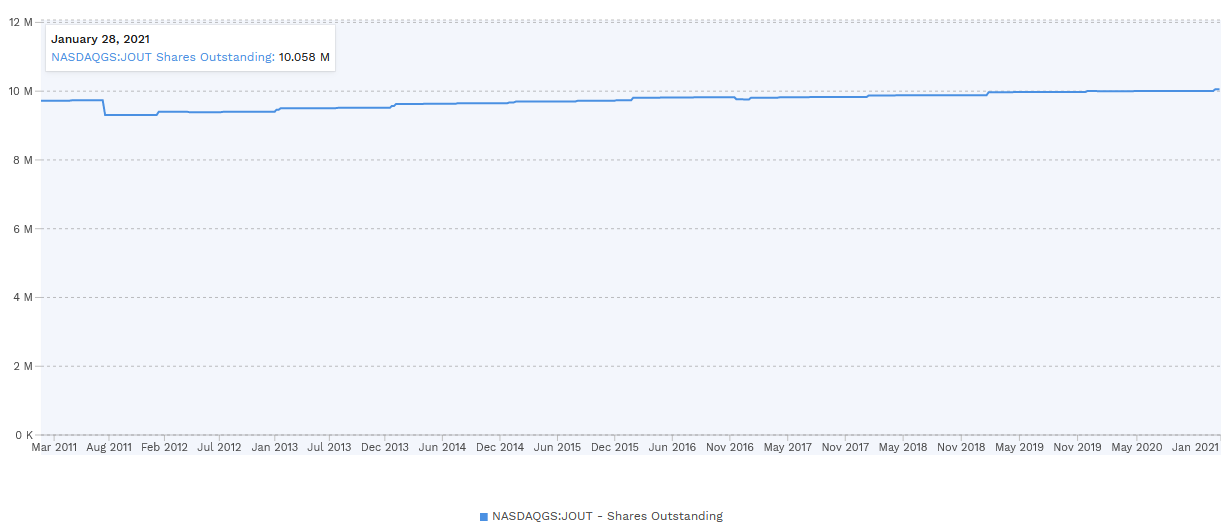

As you can see, the company did not either make a habit of emitting new shares that would dilute existing shareholders.

Source: www.finbox.com

One last management risk associated with family-owned companies is nepotism and being unwilling to bring managerial talent from outside. This is not the case here, as some examples below can show, from the board of directors:

- John M. Fahey Jr, retired chairman and CEO of National Geographic Society

- Richard Sheahan, former president of Patagonia.

- Edward F. Lang, CFO of New Orleans’ NFL and NBA teams (Saints and Pelicans)

Competition

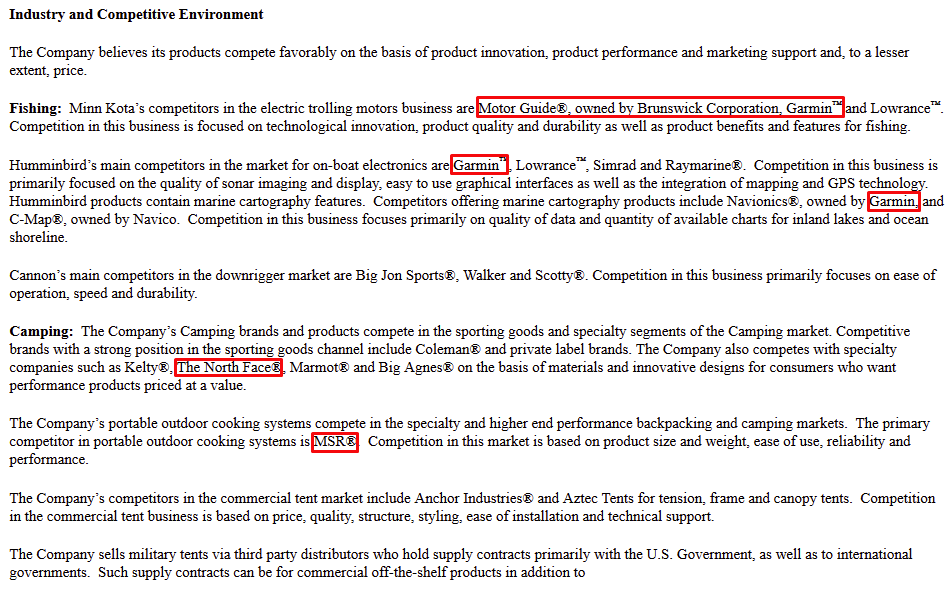

The markets in which Johnson Outdoors operate are not very concentrated, so there are a lot of different competitors. JOUT itself identifies them clearly in its annual reports (SEC filings). I have put at the end of this section the complete description of the competition by Johnson itself, but I will also look deeper into some of the larger and more serious competitors.

Many of them are private corporations, so it is not as easy to assess their strategy or strength as with public companies. JOUT is not giving publicly their assessment of their competitors, in order to not weaken their own position, so I will have to make an educated guess on it.

Garmin

Garmin, more known for its GPS devices, is a competitor of JOUT for the trolling motors, the marine cartography and the on-boat electronics. As a 22.4 billion dollars company, it definitely has the firepower to be a serious competitor to JOUT’s electronic fishing equipment. Garmin’s origins are actually in the marine market, when it started in the 1990s to sell a $2,500 GPS receiver for sea going ships.

I could not really decide how big of a threat Garmin is for the core sector of JOUT, its fishing sector (still representing 75% of sales) in terms of quality, as both have excellent reviews.

Garmin as a company seems mostly focused on competing on the general electronic segments (a MUCH larger market after all), with very strong focus on wearables like smartwatches and personal trainers, but also GPS (car and outdoors) and even avionics.

The only segment that seems a focus of Garmin which overlaps with JOUT’s core products is their marine section. It includes sonars, ice fishing kits, trolling motors and marine maps.

Johnson products seem quite a bit cheaper than Garmin’s, but frankly, I am not a fishing enthusiast, so I am not 100% sure I perfectly compared apples to apples in terms of technical specs for very specialized products.

Brunswick Corporation

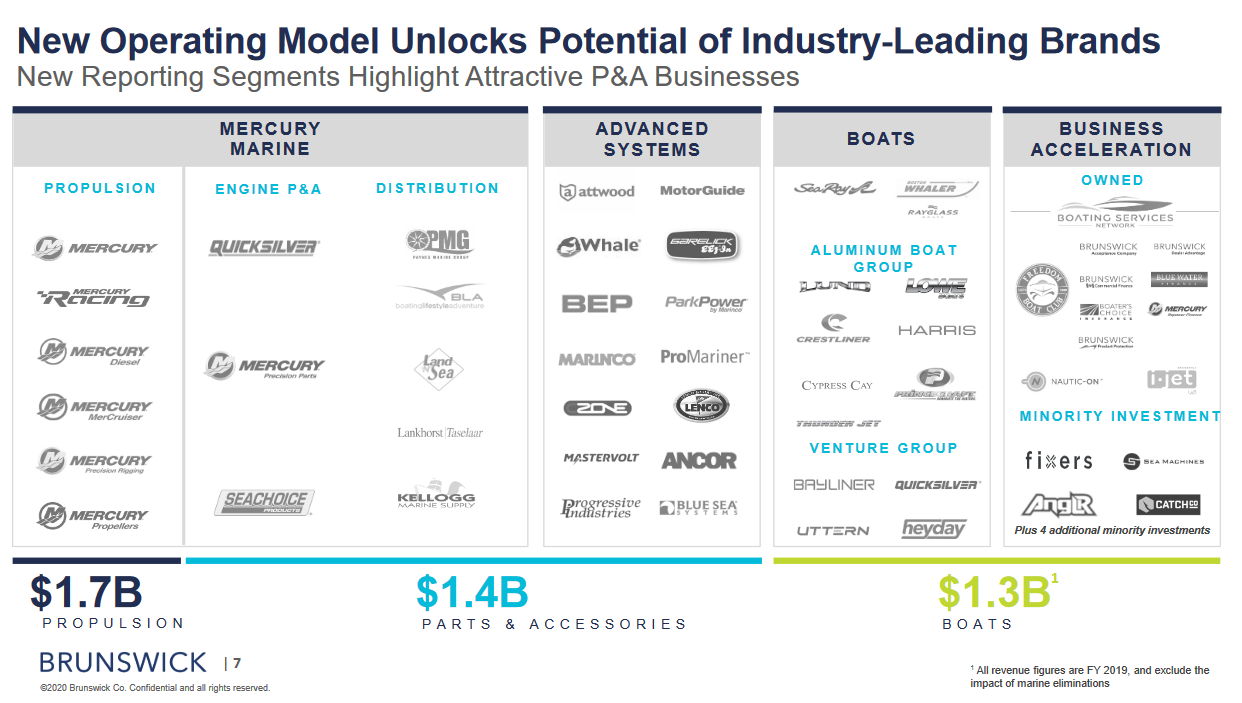

An almost $7 billion corporation and 13,000 employees, Brunswick is the elephant in the room when it comes to recreational boating and fishing, especially in the US market. The group has recently re-centered on marine activities, selling its Bowling, Billiard, Fitness and Cycling departments and acquiring a few marine-related businesses.

I am not exaggerating when talking about the elephant in the room, just give a look at a slide from their investor presentation displaying all their brands.

Source: d1io3yog0oux5.cloudfront.net

The company also moved from making most of its money selling boats to mostly selling motors and mechanical parts. This new re-focused, leading in the motor segment is a serious competition for JOUT.

I would however say that Brunswick seems to prefer to communicate about the power of its engines, and have a focus on bigger, high-speed boats for leisure, than for fishing.

Brunswick’s communications, Source: d1io3yog0oux5.cloudfront.net

In contrast, Johnson has its communication centered on shallow water fishing and the silence of its engines.

To me, both companies’ communication strategies align very well with their respective customers, and they seem for now to be fine keeping it separate that way.

Nevertheless, I consider Brunswick the most dangerous of JOUT’s competitors. It could, if it wanted to, easily invest massive amounts of money into the shallow water fishing segment (the cash maker of JOUT) and develop a strong competing brand in that niche, while still cashing on the high-speed boating leisure segment.

At the moment, the deeper commitment of JOUT to the fishing segment only, and its complementary offer of sonars, motors, anchors, and maps is probably its biggest asset, as it offers all fishing gear from one supplier, while Garmin and Brunswick each offer only a part of the full fishing gear set.

But Brunswick is active in the fishing segment, especially at sea, and JOUT will have to maintain the strong focus and product development of the last years to maintain its position in the segment against Brunswick.

Any shareholder in JOUT will have to regularly monitor that the competitive situation on this segment is still unchanged, and that JOUT products stayed on par with Brunswick’s.

The North Face

A private company, the North Face is a giant, with a respected brand and strong reputation in hiking, camping and mountaineering. The brand has evolved over time, and is now mostly focused on apparel more than equipment. Nevertheless, it is still selling tents, at a very steep price range (from several hundreds dollars to $5,500). So despite its size, I would not consider it a large threat to Johnson Outdoors, as it is essentially targeting the highest-end of the market, while Johnson is more focused on delivering great quality for a good price.

You can also learn more about The North Face’s rather fascinating business history here.

MSR (Mountain Safety Research) / Cascade Design

Part of the Cascade Design group, MSR manufactures cooking gear for camping, with a focus on mountaineering and alpinism. Its products are definitely of high quality and even its design looks similar to Johnson cooking gear. I frankly have no idea who copied who here.

The price range seems a bit higher than Johnson’s stove lineup, so I think while it is a serious competitor, it is one that JOUT might be able to compete successfully with. In addition, MSR’s focus on mountaineering allows for Johnson to have a different marketing approach, less focused on absolute efficiency and engineering, and more on practicality and good price/quality ratio.

Camel Expeditionary

Camel is a private company manufacturing 45% of all US’s Armed Forces tents, for a total of 750,000 tents over the years. This is clearly the well-established insider in this market, and Johnson Outdoors will have to keep hard at work to keep taking military tenders away from Camel.

Source: johnsonoutdoors.gcs-web.com

Quantitative Analysis

Financials

Revenues

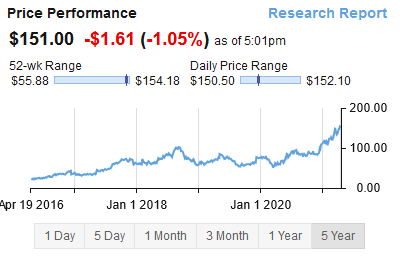

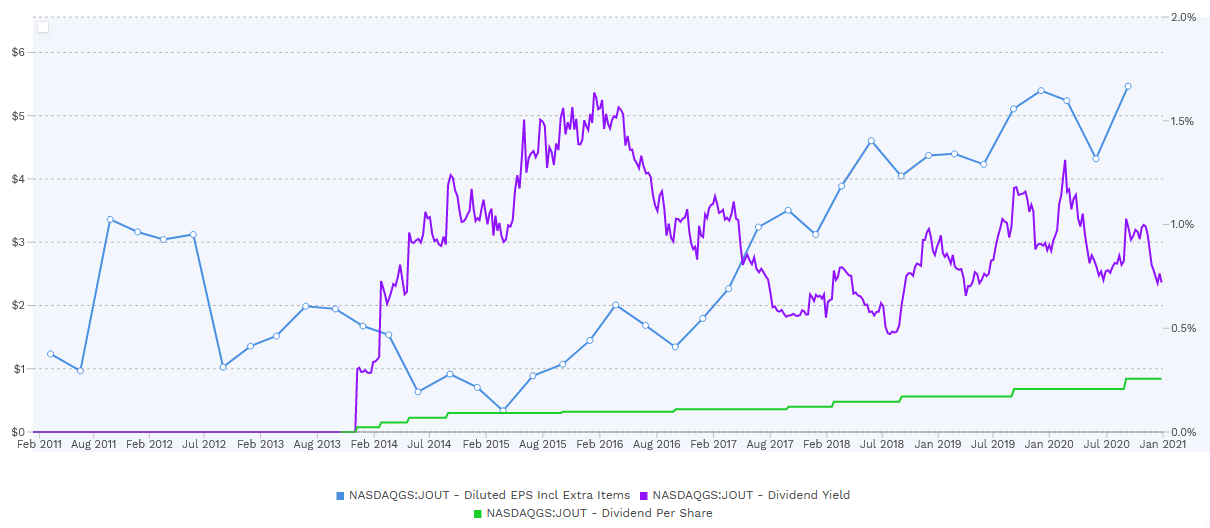

Johnson Outdoors (JOUT) is a company which has experienced steady growth in revenues since 2015, and its share price nicely reflects it.

JOUT earnings per share have also steadily grown, showing that the company has managed to generate this growth in revenue without sacrificing margins.

Dividends

Growing revenues and earnings also allowed it to start paying a dividend in 2014, which has been steadily increasing since. The dividends’ yield is not really high, only 1% on average, but the steady dividend per share growth allows for some hope it might inch somewhat higher in the future, or at least, keep up with the rising share price.

Source: www.finbox.com

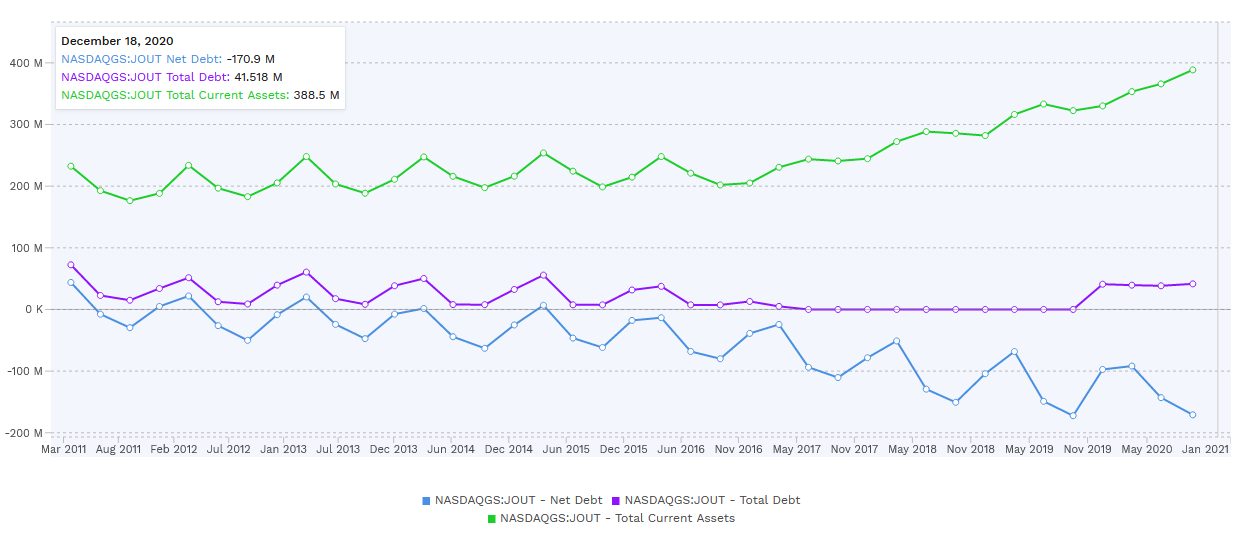

Debt and Balance Sheet

JOUT revenues and earnings are showing a good quality, steadily compounding company, with ample room to keep growing. But where it really shines is in its balance sheet.

As you can see below, JOUT has virtually no debt at all, especially when compared to the massive amount of cash and current assets on its balance sheet. The total net debt is a negative $-170 million. As it is standing at the moment, JOUT is an extremely financially solid company, which would be able to handle an economic downturn very well.

In fact, with such a pristine balance sheet, I suspect JOUT could benefit from a recession, by being able to maintain marketing budgets when competition is cutting them, acquiring smaller distressed brands or expanding in new markets by deploying the cash at hand.

Source:www.finbox.com

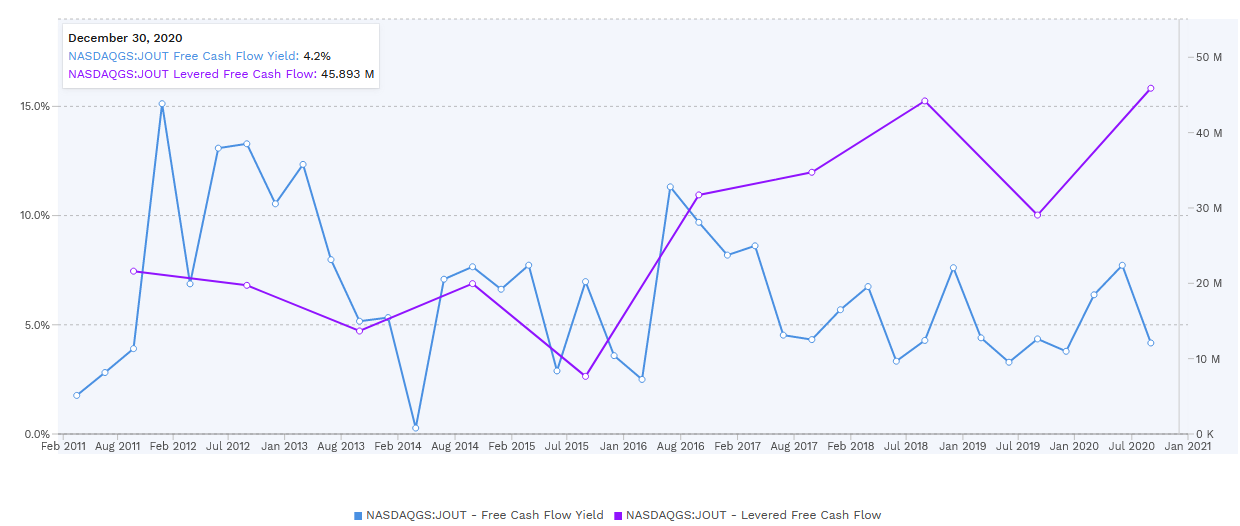

Cash Flow

As cash flow is strongly tied to the ultimate return an investor can expect from a stock, let’s take a look at JOUT’s cashflow metrics.

The cash flow has been steadily rising, and while unstable partially due to seasonality of JOUT sales, has been at an average of 5% for the last decade.

Source: www.finbox.com

Source: johnsonoutdoors.gcs-web.com

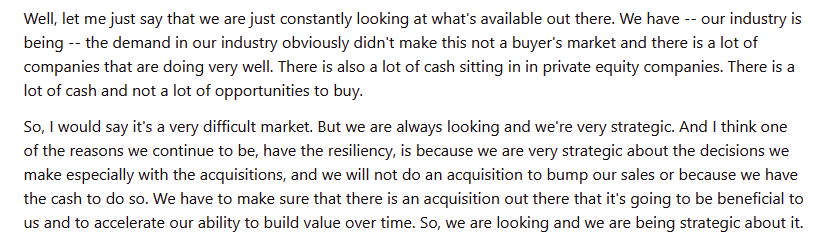

When discussing cash flow, we need to discuss if we trust the management to use it well. Cash is being reinvested in creating valuable patents resulting in top-of-the line products. There have been no botched acquisitions wasting capital in inefficient diversification. The company stayed laser-focused on its core competency, outdoors equipment for camping and water sports.

They are actually able to wait patiently for a good opportunity with a good price, and not rush to make overpriced acquisitions. This was very well expressed by the company CEO, Helen P. Johnson-Leipold:

Source: www.fool.com

Combined with the family ownership, this gives good reason to expect good management of the cash generated, and to see it channeled toward more growth without the company losing its focus and competitive advantage.

Well used capital and the brand strengthening is apparent when looking at the ROIC (Return on Invested Capital), which has been rising from a lower 6-8% in 2011-2015 to a 10-15% in 2015-2020.

Source:www.finbox.com

Categorization and Valuation

Investment Category

I can squarely put Johnson Outdoors in the high-quality companies category. It has a stable business, solid margins, strong brand and quality management. It also has plenty of room to grow to become a steady compounder for the decades to come.

I expect JOUT to increase its market share in its core sector (fishing) while steadily expanding in its main growth sector (camping), both in B2C and with government contracts.

Over the next 10 years, I would not be surprised if they added to the camping segment a lineup of backpacks, trekking shoes, walking sticks, etc… that would capitalize on their existing industrial facilities and experience with fabrics and polymers. The diving section should get back to normal once the COVID-19 crisis subdues, and the kayaking section should either become profitable or be abandoned.

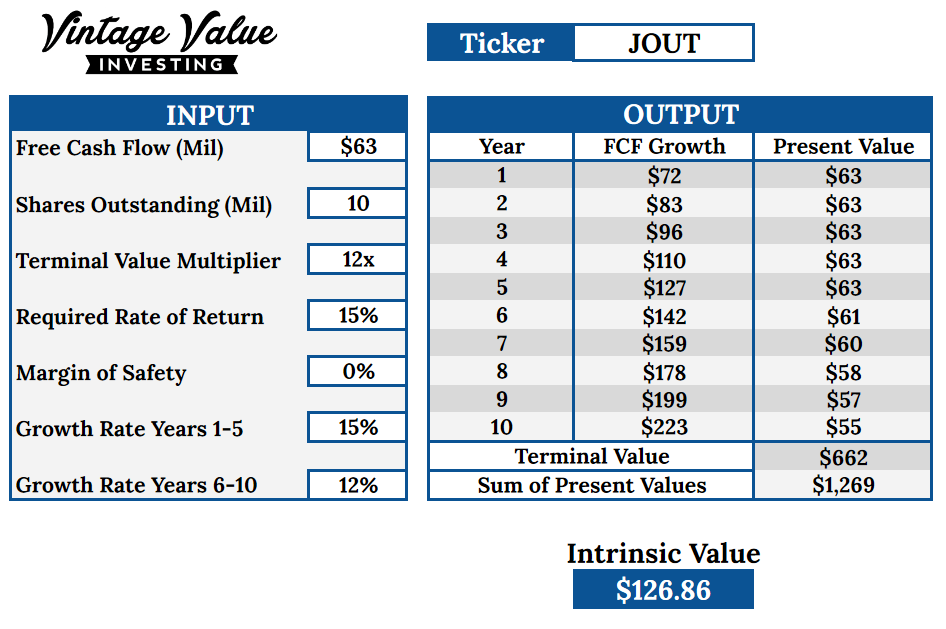

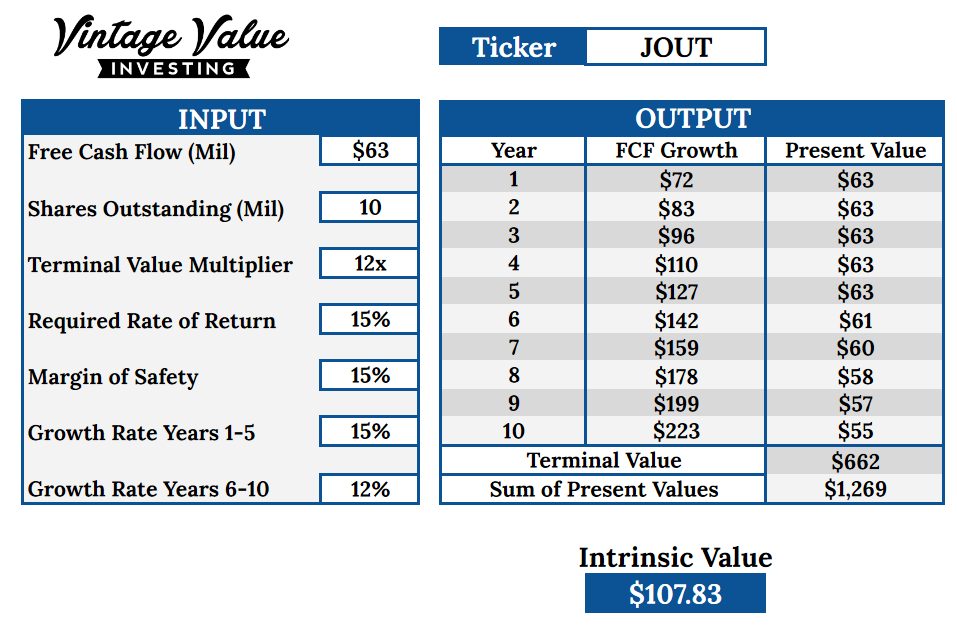

Discounted Cash Flow

One way to calculate JOUT’s valuation is using the discounted cashflow model. You can see what it means and how it works here. To me, this is the best method to calculate the value of a quality steady compounder like Johnson Outdoors.

Free cash flow has been growing over the last year at an impressive 19% CAGR (Compound Annual Growth Rate). I prefer to assume that such returns might not always stay and picked an expected growth of 15% for the next 5 years, and “only” 12% for the five years after that.

This gives me an intrinsic value of $126 per share, below the $151 in April 2021. You will note that I put 0% in margin of safety, as I was interested to know what the intrinsic value of the business is.

I used as a terminal value multiplier the lower range of the price / free cash flow ratio. It has varied a lot over time but seems to always go back to a baseline around 12 and not below.

In order to stay safe, I also use a 15% margin of safety to determine the ideal buying price of the stock. So, with the recent increase, JOUT would be slightly overvalued, and somewhat lacking a margin of safety, expect for the quality of the business itself.

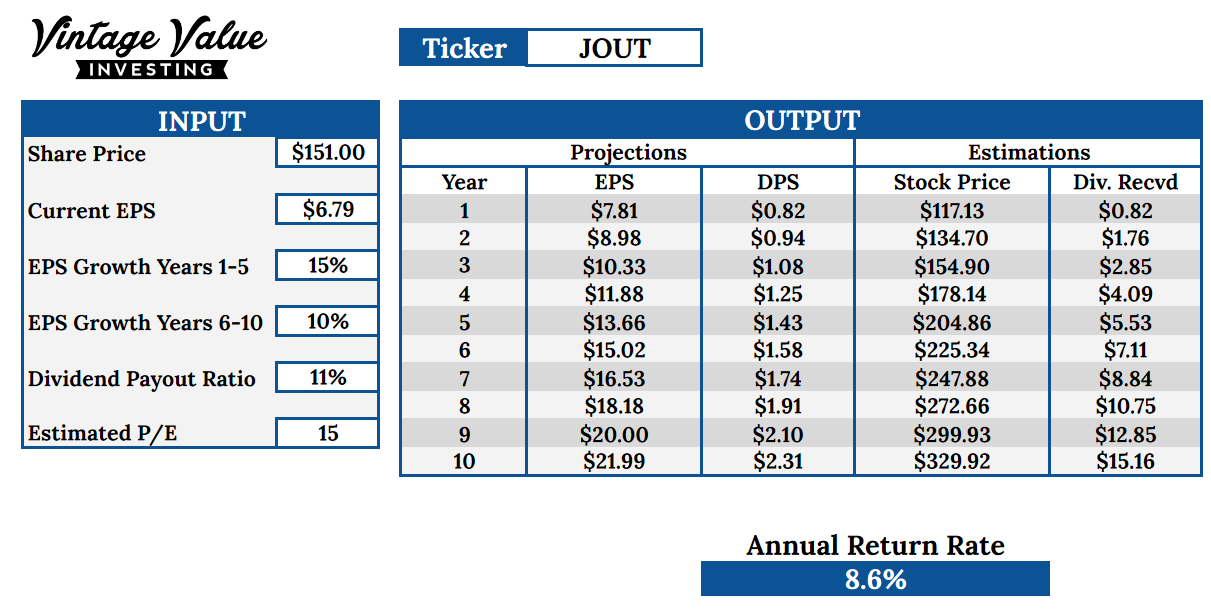

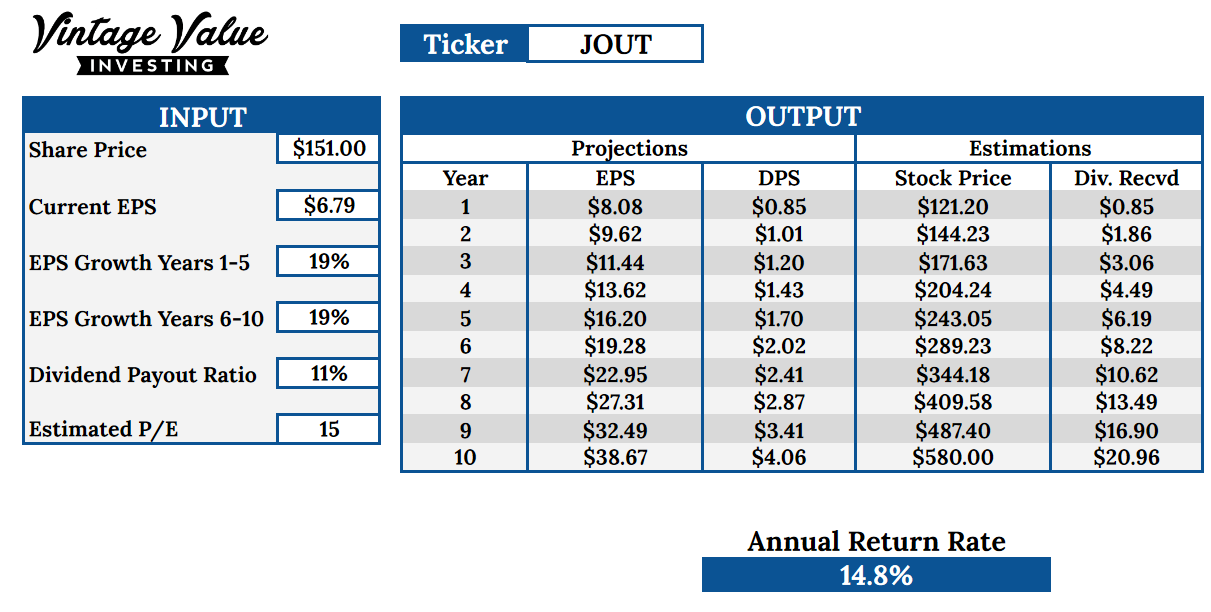

Earnings Growth Model

I expect JOUT to keep growing, so another way to guess its future returns is to look at earning growth. Over the last 10 years, earnings have grown at the rate of 18.1%. To keep a margin of safety, I took an expected growth of 15% in the next 5 years, and only 10% in the next few years. With this relatively conservative expectation, this would give JOUT an annualized return rate of 8.6%. So, it would fall quite short of the 15% I usually aim for, but this would not be too shabby either.

In order for JOUT to actually deliver a 15% annual return rate, it would have to perfectly stay on track with its 18-19% earnings growth rate for the next 10 years.

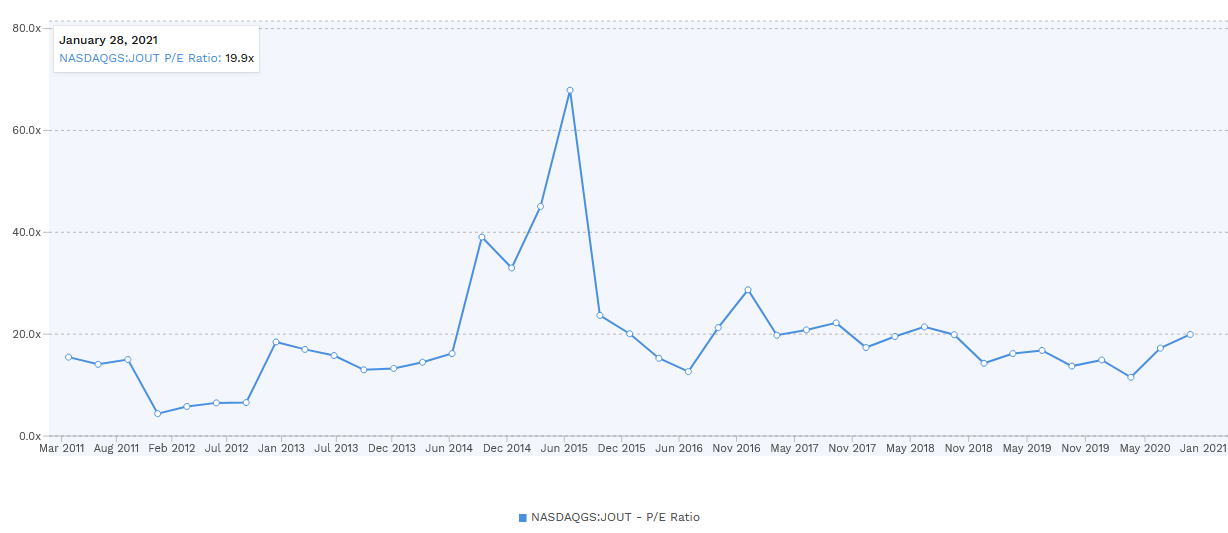

This is not impossible, but 10 years is a long time. In that period, a recession can for example impact the budget of its customers, reducing their willingness to gear up for fishing trips or visiting national parks on the other side of the country. P/E has been very variable in the past, so I picked a conservative 15 instead of a more optimistic 20.

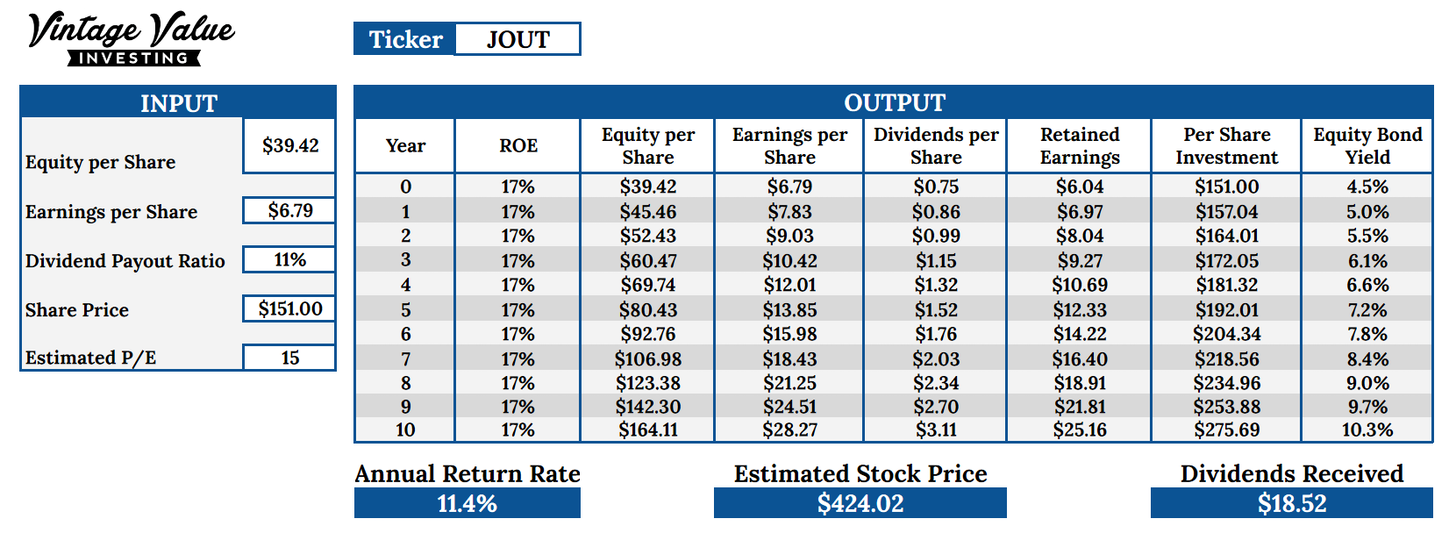

Equity Bond Yield

Equity bond yield is a method that considers JOUT stock as if it were a bond and calculates the yield it would bring. Instead of basing its calculation on free cash flow, this model uses the Return on Equity (ROE) as a base. You can learn about it in my article here.

This model shows an estimated annual return rate of 11.4%, which would make JOUT an okay compounder, but not an exceptional one.

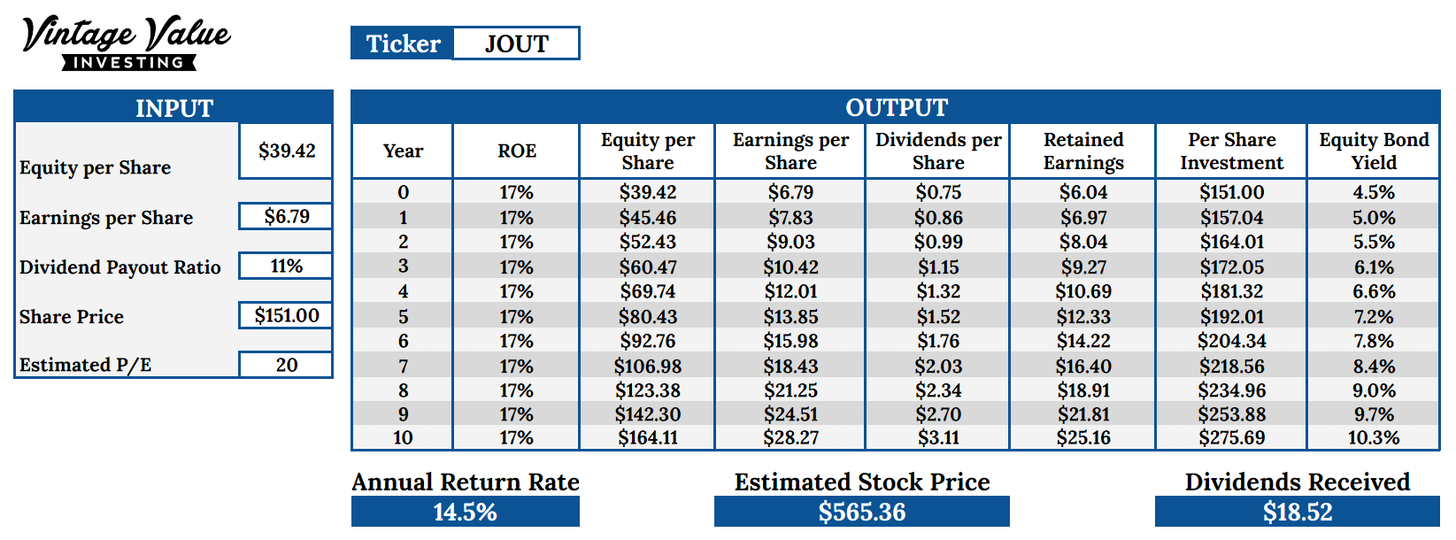

However, I do not think that this method is the best to judge JOUT, as the calculation is highly dependent on the estimated P/E ratio. And that ratio has been all but stable in the last years, so it is anyone’s guess what should be the right number here, making the calculation inherently less reliable. If the P/E ratio used was 20, that would give an annual return rate of 14.5%, illustrating how sensitive this valuation method is to that data point.

Source: www.finbox.com

Other Calculation Methods

Considering the very low dividend yields, other valuation methods like yield on cost are not relevant for Johnson Outdoors.

Final Assessment

Company Synthesis

Johnson Outdoors is a quality company, offering the combination of a rock-solid balance sheet, a family-owned business honest with outside shareholders and a steady compounder with large addressable markets. Outdoor sports are not going anywhere, and the cultural shock of the COVID-19 crisis might create a durable shift toward less crowded activities outside. Long months of lockdown in cities will also likely create a longing for open space and nature.

Will that be a long term trend or just a short term reaction, it is hard to tell. I can easily imagine that many people might try holidaying mask-less by camping in a national park instead of a densely packed beach resort, and discover they liked it and keep doing it in the future.

In a period of increasing speculation and market volatility, a very solid balance sheet is also a good place to park cash, at a time where most valuations do not make sense in regard to fundamentals. It is a fool’s errand to try to call a market top, but the intense speculative mood of 2020 and early 2021 is definitely reminiscent of the Tech bubble of 1999, so a no debt, growing company like Johnson Outdoors might be safer than over-hyped technology plays.

Short term projection: 1-3 years

In the short term, JOUT is likely to do well, as the business fundamentals are very good and likely to stay this way in the immediate post-COVID era.

Long term projection: 3-10 years

A lot of the long-term growth will depend on the ability of Johnson Outdoors to accomplish the following tasks:

- Expand overseas. While very popular in the US, the brand is not yet well established in Europe and almost not at all in Asia.

- Become a regular supplier of the military and other similar organizations, which would provide it large volume contracts and help it scale up its production

- Use its R&D budget to create new high-quality products in the sectors it is already profitable in and have a client base who trusts them, like camping (shoes, backpack, etc…) or fishing (fishing rods, boats, etc…)

- Get diving back to profitability when travel comes back to normal.

- Turn the kayaking sector into a profitable and growing activity, maybe by expanding to white water sport (down river torrent).

In any case, Management is unlikely to dilute existing shareholders or waste the company cash on pointless acquisitions and diversifications. So the higher probability for a bear case is that growth slows down and JOUT stays a profitable, well established sports brand that slowly turns from a growth story to an established and “boring” cash cow.

Valuation

JOUT’s current price is seemingly a little bit too pricey according to the earnings growth model and other valuation methods. Always erring on the side of caution, I would tend to believe the price is a little bit high at the moment. This is rather clearly reflected in the quite high P/E ratio of 22, showing the market already priced-in future growth.

At the same time, it does deserve higher multipliers thanks to its pristine balance sheet, steady growth and excellent management. So, I suspect this is a typical case of an “okay price” for a great company, or in Warren Buffett’s terms:

“It’s far better to buy a wonderful company at a fair price, than a fair company at a wonderful price”.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in JOUT and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.