So what is Warren Buffett’s Equity Bond? It’s a pretty simple method, really. Essentially, the Equity Bond is synonymous with earnings yield.

Here is the mathematical formula:

Earnings yield is simply the Earnings per Share (EPS) over the share price. For example, if a stock had a price of $100 and the EPS was $5.00, then the stock would have an earnings yield of 5%.

Why is this so important? It’s all about how Buffett views his investments. He isn’t looking for companies trading cheaply (like his mentor, Ben Graham) and selling them at fair value. As a quality investor, Buffett is looking for companies that can compound his original investment for years or decades to come.

Warren views the earnings yield of a stock the same as he would the yield of a bond, hence the name Equity Bond. The main difference between the Equity Bond and a normal bond is that the longer you hold an Equity Bond, the more it appreciates. The normal bond has a fixed yield over time.

For example, would you rather own a stock with an earnings yield of 5% that appreciates every year, or a bond that was yielding a fixed 2%? The answer is pretty simple, right?

Characteristics of Ideal Companies

Obviously, not every company has great earnings yields, or else every business would be up for grabs. Even those companies that do have great earnings yields still need to have other important characteristics to make the investment worthwhile.

Here are some characteristics of ideal companies for the Equity Bond method:

- Consistent increasing annual equity per share (or book value)

- Higher than average Return on Equity (ROE) over long time periods (>15%)

- An earnings yield more than the 10 year government bond (>1%)

- A fair share price

These are initial screens for selecting investment candidates.

Increasing Annual Book Value

Companies that have a consistent track record of increasing annual book value (also known as equity per share or shareholders equity) are the ideal candidates. Positive book value growth shows that a company and its management are increasing the equity base of the business without compromising shareholder value.

This is the foundation of our ideal company.

Return on Equity

Higher than average Return on Equity (ROE) is the second characteristic of quality companies. Here is the formula for ROE:

This equation can also be EPS / Equity per share for a per-share calculation. We’re looking for companies that can consistently increase shareholder equity while simultaneously creating over 15% yearly return on that equity.

Additionally, we prefer companies that retain most of their earnings and do not necessarily pay a dividend. This is not required, of course, as many companies do pay dividends. However, the theory behind this is that companies that are able to maintain a high ROE and do not pay a dividend can productively reinvest those earnings faster than companies that pay dividends.

As with shareholder equity and book value, the key here is long consistent annual stretches of ROEs that are above 15%. In order for the calculation to work, the company must be consistent in its returns.

Earnings Yield

Let me mention a quick caveat here. Over the past decade, we have had record low interest rates and bond yields. Therefore, it is easy to find companies that have an earnings yield above 1%.

I recommend finding companies with at least a 5% earnings yield in order to establish desirable returns.

A Fair Price

No company is worth more than its fair value, and overpaying for a company can lead investors to mediocre or even negative returns. This is why Warren Buffett and Charlie Munger talk so much about not overpaying for a company. The more you pay, the less your potential return will be.

Let me show you in an example of the Equity Bond method using Progressive Insurance (PGR) as an example.

Progressive Insurance Example

Progressive Insurance (PGR) is an amazing company for this type of valuation method. Let’s take a look at some of PGR’s characteristics.

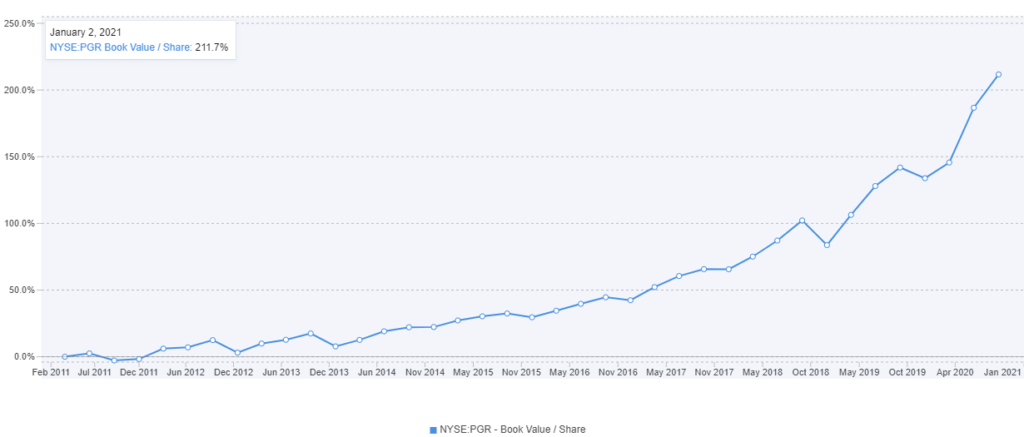

PGR Book Value per Share

PGR has compounded its book value (or shareholder’s equity) tremendously over the past decade, especially over the past five years. PGR’s book value has grown over 211% in ten years, over 21% per year!

Source: Finbox

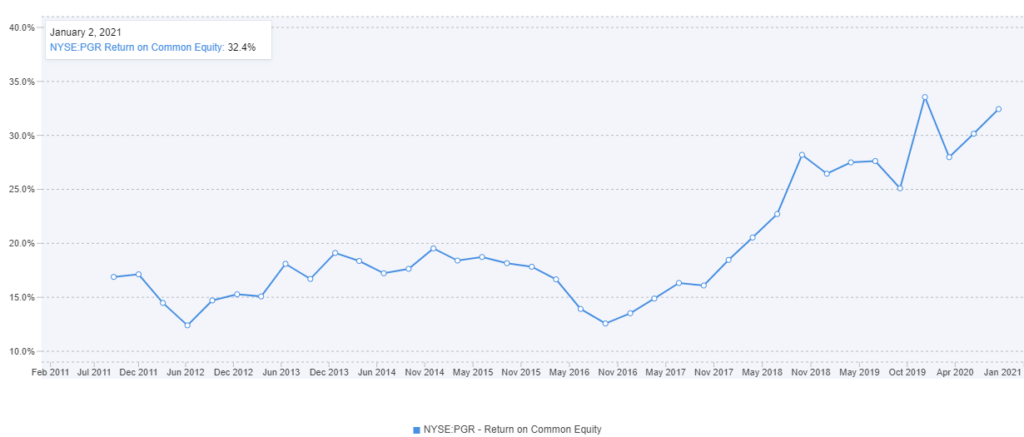

PGR ROE

PGR has had a near-perfect ROE track record, only dipping below 15% during a couple of quarters over the last decade. To make things even better, the ROE has skyrocketed the past three years, surpassing 30% ROE.

Source: Finbox

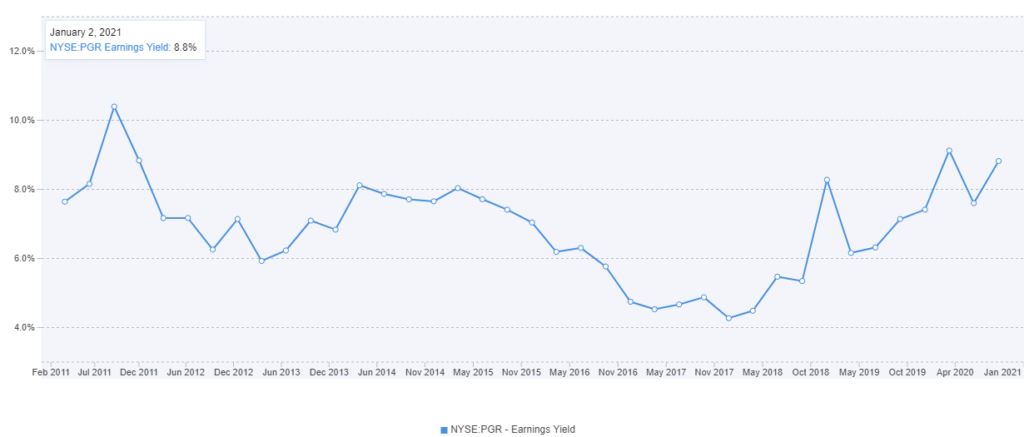

PGR Earnings Yield

PGR is currently offering investors an 8% earnings yield (equity bond). This is an extremely attractive yield, especially with the 10 year treasury bond currently yielding less than 1%.

Source: Finbox

Additionally, PGR’s earnings yield has stayed above 4% over the entire last decade. This is proof that PGR has created solid earnings over time.

We will get into the fair price portion later on in the valuation process.

Calculating the Return

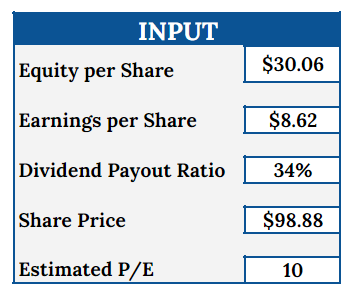

Here are the required inputs we need for the Equity Bond calculation:

Equity per Share: Found on the Balance Sheet as Shareholders Equity. To calculate it, take this number and divide it by the number of shares outstanding.

PGR’s current equity per share is $30.06.

Earnings per Share: Found on the Income Statement. Always use diluted EPS numbers.

PGR’s diluted TTM EPS is $8.62.

Dividend Payout Ratio: This is a calculation that shows the percentage of earnings the company is paying out as dividends. Most platforms will calculate this for you, but you can find out the payout ratio by dividing cash paid for dividends (found in the Cash Flow Statement) by net income.

PGR’s current dividend payout ratio is 34%.

Share Price: Current share price of the company.

PGR’s current share price is 98.88.

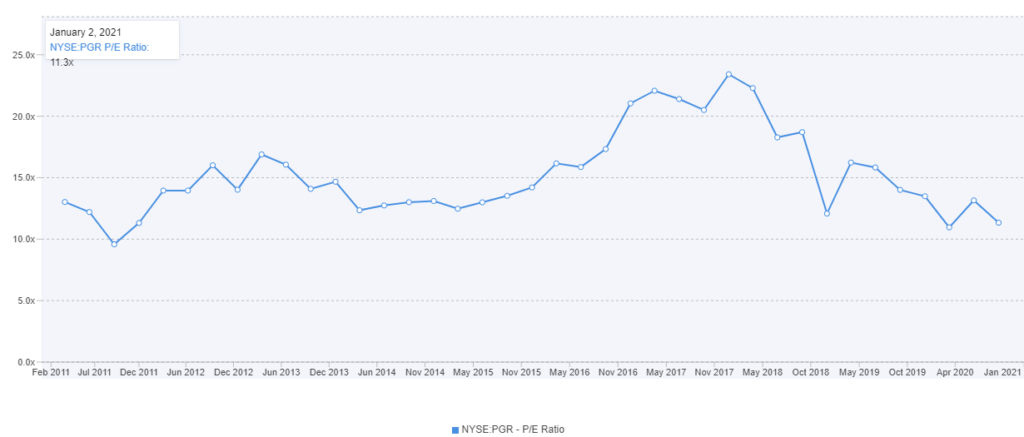

Estimated Price to Earnings (P/E) ratio: P/E is simply calculated as share price over earnings per share. A standard P/E ratio is 15, but it may help to calculate the historical P/E ratio of the company you are analyzing. This serves as a final calculation to determine the assessed stock price and what our return would be after 10 years.

Source: Finbox

We can see that PGR’s P/E has been consistently between 10 – 15 over the last decade. Let’s be conservative and use a P/E of 10 to assess the future stock price.

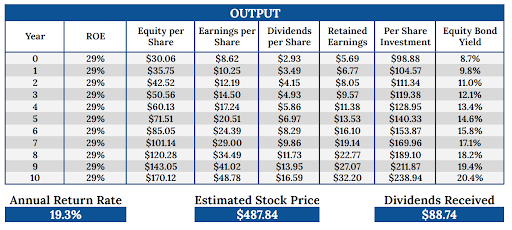

After inputting all the numbers, let’s see what the output looks like.

The Magic of Compounding

According to our calculations, PGR has an ROE of 29%. We can see that PGR will pay $2.90 (or 34%) of its $8.62 in earnings as a dividend. This will allow the company to retain $5.72 (or 66%) of its earnings to its equity base, which will be $35.78 per share the following year.

Additionally, that $5.72 of retained earnings gets added to our own per share investment base of $98.88, bringing it to $104.57. We are essentially looking at our own investment of $98.88 per share as our own equity base, and PGR gets to reinvest our retained earnings, thus increasing our Equity Bond yield.

Essentially, since PGR’s earnings are likely to increase each year, so will our Equity Bond yield.

The Ever Expanding Coupon

Now the key to this calculation is the ability of PGR to maintain its 29% ROE over time, which will deliver returns to shareholders. If PGR can manage to maintain that 29% ROE the following year on $35.78 of equity per share, then we can assess next year’s earnings to be $10.26 per share.

If PGR maintains its 34% payout ratio, then it will pay out $3.46 as a dividend and add $6.80 to its equity base. Our own per share investment increases to $104.57 from the retained earnings, which increases our earnings yield to 9.8%.

As you can see, the beauty of this method is that the longer you hold, the greater your yield and returns will be. If we hold on to the stock for the next ten years, our equity bond would be yielding over 20% from our original purchase price of $98.88!

We can also calculate our average annual return after 10 years. According to our calculations, at year 10, PGR would have an estimated EPS of $49.14. If we take that EPS number and multiply it by our estimated P/E (10), we would have an estimated stock price of $491.38.

We can also account for the dividends we received over that time. Over the course of 10 years, we would receive $88.38 of total dividends. When we include the dividends into our calculation for annual returns, we come to an annual return rate of 19.3%!

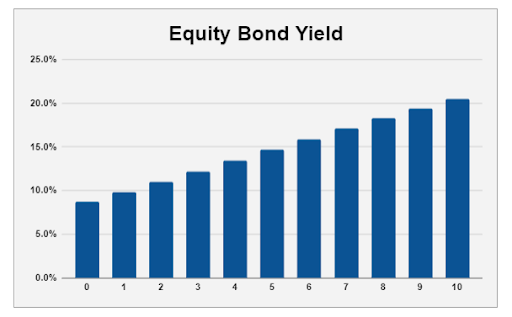

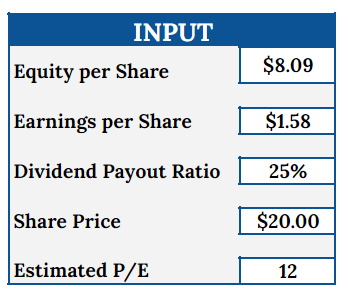

Backtest

If you think this is too good to be true, let’s just run a little backtest. Ten years ago, PGR was trading for around $20.00 per share, adjusted for splits. It had equity per share of $8.09, EPS of 1.58, a dividend payout ratio of 25%, and a P/E of 12. Let’s input these into the calculator.

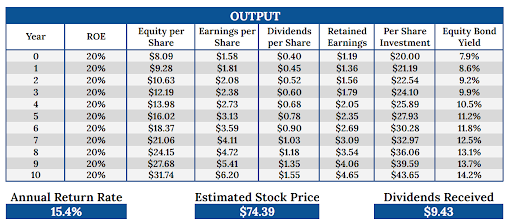

As we can see based on our results, PGR had an ROE of 20% and an earnings yield of almost 8%. While the numbers aren’t exactly how things played out in real life, the equity per share estimation at year 10 is $31.74; that’s pretty darn close!

Our estimated return is over 15% back in 2011, with an estimated stock price of $74.39, and $9.43 of dividends received. This is actually less than the current stock price of $98.88, so we technically undershot our actual returns. PGR was able to earn well over 20% ROE over the last decade, which helped boost returns even higher.

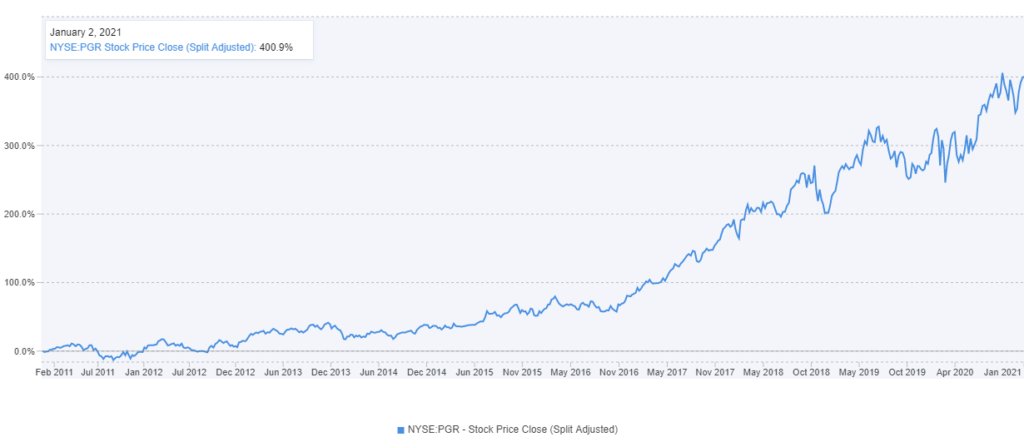

In fact, PGR did much better than our estimates. Its stock price ended up compounding over 400% in the last ten years. That equates to a 40% annual return!

Source: Finbox

A Fair Price

All of this compounding sounds incredible, and it is. But the thing to remember is that in order to have amazing returns, you still have to buy the company at a fair price. Overpaying for a stock can eat into your returns.

For instance, if we had paid for PGR at a P/E of around 20 today (which it was a few years ago), the current stock price would be around $172 per share. If we paid that much, our annual returns would be around 12%. While not terrible, it still is a big damper on potential returns.

This is why Warren Buffett and Charlie Munger talk so much about not overpaying for a company. The more you pay, the less your return will be.

What Can Go Wrong

Of course, if predicting winners were this easy, everyone would be doing it. The model assumes that retained earnings will be productively invested and that the company will continue to perform as it has in the past.

This of course is not guaranteed. Companies don’t always invest effectively: mergers and acquisitions can go wrong and expansion doesn’t always make a company stronger. New competitors can emerge and industry trends aren’t always favorable.

Analysis of purely financial factors has to be undertaken in conjunction with rigorous analysis of the Company’s industry, competitive position, and management capacity.

Conclusion

The Equity Bond valuation method is a unique method of valuation that I find very useful. It is one of my favorite methods to use, and I find it most beneficial when I want to calculate returns for those long-term, buy and hold, high-quality stocks.

It is not advisable to rely exclusively on this method, or any method. It’s an addition to your toolbox, not a substitute for other methods of evaluating a company!

If you liked this method, I highly recommend you read Buffettology. The book takes this concept to much more detail than I did. Plus, you’ll learn other methods as well!

Which tool was used to calculate and backtest the input.