April 18th 2021

Quick Stock Overview

Ticker: GD

Source: www.stockrover.com

Key Data

| Sector | Industrials |

| Industry | Aerospace & Defense |

| Market Capitalization ($M) | 52,307 |

| Employees | 100,700 |

| Sales ($M) | 37,925 |

| Net Cash per share | -$40.41 |

| Equity per share | $55.23 |

| Debt / Equity | 0.9 |

| Interest coverage | 8.6 |

Summary

General Dynamics is one of the major actors in the US defense industry. Its headquarters is in Reston, Virginia, and it employs more than 100,000 employees, mostly in the US. The company is essentially active in 5 sectors: Aerospace, Combat System, Information Technology, Mission Systems and Marine Systems.

GD sectors of activity (source: www.gd.com)

This is the company producing some of the key equipment of the US military. Their product line includes some well-known platforms whose lifespans have spanned decades. Some examples include the M1 Abrams tanks, Virginia-class submarines, Arleigh Burke-class destroyers and the next-generation Zumwalt destroyers. It is also producing various other equipment in aerospace and IT.

Zumalt-class stealth destroyer (source: www.gd.com)

Abrams M1A2 SEPv3 (source: www.gd.com)

Strategic Analysis

General Dynamics (GD) is one of the pillars of the American defense industry and a key contractor for the Pentagon. The company has a long history of industrial achievements and technological innovation. GD produces advanced designs like the new Zumwalt stealth-destroyers. It also guarantees regular revenue streams for the company, as the US military will keep replacing its oldest ships by more advanced designs.

As a company deriving most of its income from defense contracts, a key factor to predicting the future of General Dynamics is to predict the future of US military strategy and spending. Since the end of the Cold War, the USA has been engaging in multiple counter-insurgency operations in places like Iraq and Afghanistan. During this time, the US military has put a lower priority in capacity against “equal adversaries” like for example Russia and China. This means more focus on infantry, the Marine Corps and light armored vehicles, and less on ocean-going ships or main battle tanks.

Global Power Competition

Resurgence of Russia as a world power and the growing assertiveness of China has forced the Pentagon to look back at its armored and naval capacity. More precisely, increasing tensions in the South China Sea and Taiwan have pushed the US Navy to re-evaluate its need in terms of mobile and powerful ships. This is especially true for stealth ships and submarines, which could be key to keep Chinese naval forces at bay or enforce an embargo if needed. This is a long-term trend, independent of who is the US president, and likely to become even more of a concern for the Pentagon over the next decades.

Similarly, Russian activities in Europe and the Middle East (for example, in Ukraine and Syria) have highlighted the importance of maintaining credible land forces, able to defeat other powerful nations, instead of only poorly equipped insurgents using guerrilla tactics.

Finally, military operations have become increasingly dependent on IT systems, and cyberwarfare is now considered an integral part of war preparation. To give you some perspective, The US army Cyber Command employs 16,500 people full time.

General Dynamics’ Tailwinds

This is great news for General Dynamics, as the company is well established in all 3 of these areas of growing military spending.

The Abrams tanks are still the backbone of the armored land forces, and GD experience in manufacturing them might help it to develop and win tenders for any future tank designs. The state-of-the-art Zumwalt Destroyer and nuclear submarines are designed to be central to control coastal areas like the South China Sea or the Gulf of Oman. trusted cybersecurity suppliers like GD are almost guaranteed to get regular new projects to keep the IT military infrastructure up and running.

While I expect its other operations to be stable cash-cows, I suspect that shipbuilding, main battle tank production, and cyber defense will be the areas where GD could experience tremendous regular growth over the next 20 years.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

General Dynamics has been operating since 1952. It used to produce an even wider variety of military equipment, but re-focused on military vehicles and submarines in the 1990s. It has since diversified again in private jets, IT and ship building through acquisition.

General Dynamics is present in 5 different sectors, each contributing more or less to a fifth of the company’s revenues. Each these segments has had a relatively stable operating margin over time.

| Sector | Details | Percentage of total revenue in 2019 | Operating margin in 2019 |

|---|---|---|---|

| Aerospace | Private jets and jet services | 20% | 12.1% |

| Combat system | Armored carrier, tanks, gun and rockets | 19% | 13.9% |

| Information Technology | Data center, Health IT solution, military training solutions | 21% | 6.4% |

| Mission Systems | Communication, cybersecurity and sensors | 13% | 13.6% |

| Marine Systems | Destroyers, nuclear submarines and service ships | 27% | 8.5% |

Each of the sectors has shown a remarkably stable activity, reflected in the strong performance of the stock in the last 10 years.

The ones with the most promising future are the Marine Systems and IT, due to the Pentagon’s plan to step-up cyber defense and rebuild the US Navy capacities.

The Combat System sector is highly dependent on the Abrams tanks production, which is an aging model, bound to be replaced within the next decade. After tentative stops in production during 2020, it has been announced that the replacement will not be decided before 2023, at least. GD has the know-how and connections to be in good position to manufacture this next generation tank for the US Army, but this is far from a done deal and could impact future profitability and revenue of this sector, most likely for the 2025-2030s time frame.

The aerospace sector is highly dependent on demand for private jets, which is itself correlated to the general economic conditions, so a lasting COVID-induced recession could significantly impact these revenues. Alternatively, the temporary high demand for jets at the end of 2020 could make it a valuable asset for GD. GD could even try to sell at a high price, but no indication of this has been given by the management yet.

GD’s main possible headwind is an overall reduction of military spending. This would drastically impact the company in all its activities, except for the private jets. While I consider this unlikely in a period of increasing geopolitical tensions and decreasing concerns about federal deficits, this is always a possibility.

As I explained before, the main tailwind for GD is increased defense spending to challenge growing or re-emerging great powers like Russia and China.

Economic Moats

In value investing terms, General Dynamics has several economic moats:

High Switching Cost

When military equipment are acquired and deployed, it means that tens of thousands of soldiers and mechanics learn everything about the equipment, which results in billions in training costs for the Pentagon. Being familiar and efficient with them is also, literally, a matter of life or death.

This means that new systems are adopted slowly, and that once approved, a design is likely to be used for decades. For example, the Abrams tank entered service in 1980; 40 years ago! And at this point, all the other equipment of the army is structured around the capabilities and weaknesses of the Abrams, so changing it would imply a massive re-thinking of the whole army strategy, tactics, and equipment.

In addition, sensitive technologies like nuclear-powered submarines are not something that will be tendered to newcomers in the market. This means that the access to the market is limited to a handful of defense companies that have the right reputation, factories, know-how and financial capacity. This is not a sector exposed to disruption by smart and aggressive start-ups. Very few companies are able to simply build a nuclear submarine from scratch!

If very large orders and military build-up are planned, the Pentagon is often taking special care to purchase from two or three different firms at once. This way, it maintains a healthy level of competition and does not lose key industrial capacities in the USA. Therefore, GD is very unlikely to be pushed out entirely by its competitors, even in the improbable case it would consistently fail at delivering top-notch products.

Intangible assets

Not all GD intangible assets are on the balance sheet. Of course, it has a wealth of patents, designs and a solid brand. But its knowledge of the inner workings of defense procurement and contacts in the Pentagon is also a precious capital, slowly built over several decades. This will be obvious when I present you the management team members, which include quite a few high-ranking generals and admirals, not to mention various politicians.

It would be a very tedious and expensive task to replicate this capital for a non-defense corporation to compete with GD. This can be done, surely, as the entry of Amazon into the government database business shows, but it is far from easy, and might be even more difficult for hardware like ships and tanks.

Infrastructure

Finally, GD enjoys even a third type of moat! Building ships is a capital-intensive business that requires massive infrastructure which simply cannot be built in a few years. And this infrastructure needs very specialized employees to run smoothly. No company can quickly replicate the infrastructure and know-how of GD in shipbuilding. In addition, such facilities would absolutely need to be built in the USA, so no firms abroad can try to compete with GD over lower labor costs, for example.

Management

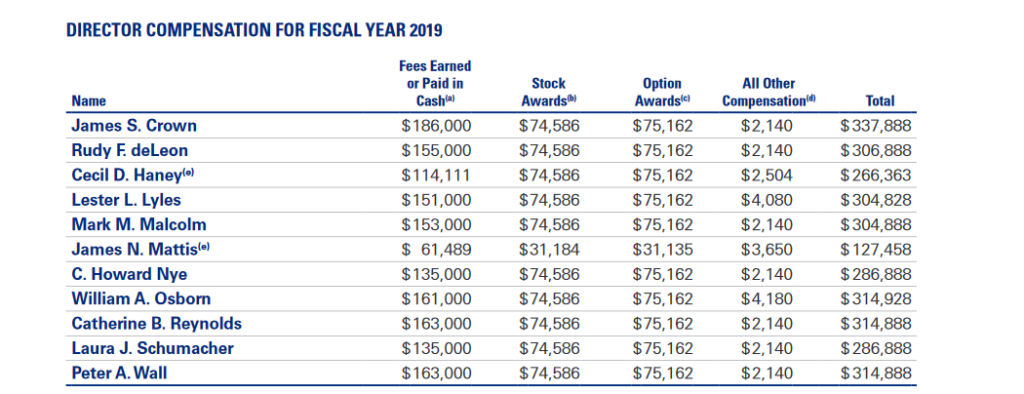

The CEO of General Dynamics, Phebe Novakovik, has received a total compensation of $18 million, which is just in line with the average compensation in the defense industry for companies similar to GD. Another plus is that Ms. Novakovik also owns $111 million in GD shares, making her personal financial interests well aligned with the shareholders’. Compensation of directors are around $310,000 yearly for each of the 11 directors, which is not cheap, but also not really outrageous for a company of this size.

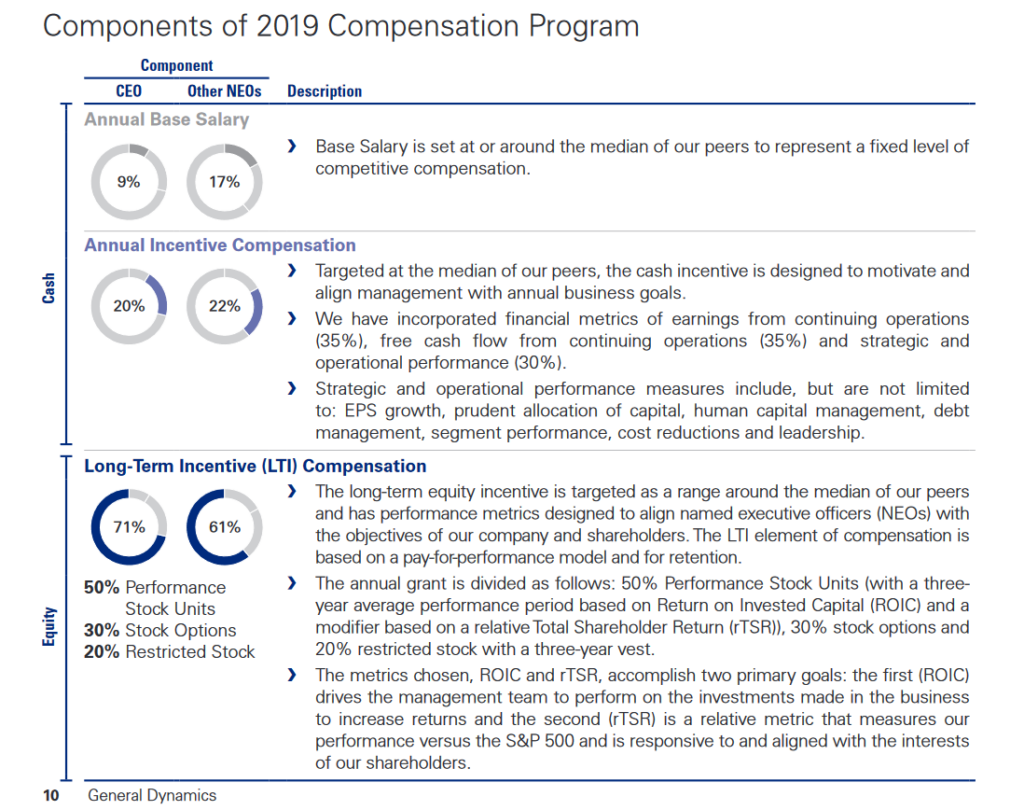

Another interesting element regarding compensation is its structure. Long-term compensation is making the majority of management income and is determined by the ROIC (return on invested capital) and the 3-year stock performance, encouraging the management to focus on long-term value creation for shareholders. This is especially crucial in a sector like the defense industry, were reputation is crucial, production is capital intensive and long-term R&D cycles are the norm. It is very valuable to see that management compensation does not give it incentives to cut corners or neglect long term investments.

It is also worth noting that insider trading has been overwhelmingly in the direction of buying and option exercising over the last 2 years, reflecting insiders’ optimism about the company prospects.

The management composition is of very high quality, and many directors have impressive military or defense industry experience, for example:

- Rudy F. Deleon: former senior vice president at Boeing

- Cecil D Haney: retired admiral, former Commander of the U.S. Strategic

- James N. Mattis: Former NATO Supreme Allied Commander Transformation

- Peter A. Wall: Retired general and Former Director of Operations for the United Kingdom Ministry of Defense

Source: General Dynamics Annual reports www.gd.com

Source: General Dynamics Annual reports www.gd.com

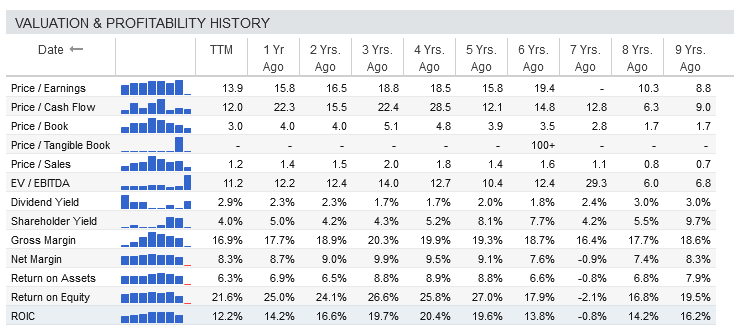

In the last 10 years, ROIC has been consistent and between 14%-20%, reflecting the high quality of the management and its ability to execute long term plans efficiently.

Source: www.stockrover.com

The only negative thing about the management is a lack of transparency regarding strategy. While guidance is relatively clear and reliable when it comes to financials, very little is said about how GD intends to stay one of the leaders of the US defense industry. A lot in the annual reports is written about the company’s general ambitions, but it is not clear for example if further acquisitions are planned or in discussion, or if R&D spending is expected to change.

I realize that part of this is due to the sensitive nature of such information, but this means that GD’s shareholders have to sign a blank check to the management regarding the company’s long-term strategy.

Competition

Due to the nature of the industry, competition is mostly coming from similar, large, well established defense companies. Threats from newcomers is not zero but is very limited and in more than 6 decades of operation, GD has proven its ability to keep delivering the highest quality products and win tenders from the Pentagon.

The Biggest Fish are Busy in Other Sectors

Three of the largest defense industry actors, Northrop Grumman, Lockheed Martin, and Boeing, do not seem to have plans to compete directly with GD. All 3 are focused on development of air and space systems, like fighter jets, bombers, missiles (including hyper-sonic missiles) and space capacities. That strategic focus means that neither of these large and potentially dangerous competitors of GD are likely to be a direct threat in the next 10-15 years. It might be true for even longer, if you consider the long time required for developing new weapons systems.

GD’s Biggest Rivals

IT, Cyber Defense and Mission Systems are likely to be the sector of GD activities under the most competitive pressure, with other significant actors. For example, Hewlett-Packard is responsible for the US Navy’s Intranet, Exelis is provides cyberwarfare to the F/A-18 aircrafts, and General Electric is active in multiple segments, from quantum computing and encryption to sensors and military wearables.

While Raytheon Technologies is more focused on missiles and missile defense systems, its extensive activities in cyber defense and electronic warfare makes it another large serious competitor for the IT division of GD.

Muted Vehicles Competition

Regarding vehicles, competition is generally smaller and rarer, actually almost nonexistent for tanks, but worth mentioning is Navistar Defense, which has with extensive experience in developing Mine-Resistant Ambush Protected Vehicles for the Iraq war. This industrial capacity could easily be extended to creating other vehicle models for countering state actors like Russia.

The same can be said of Oshkosh defense, already providing the US military with tactical vehicles, from armed 4×4 to heavy armored trucks.

A Ship Building Duopoly

Finally, there is only one serious competitor whose size can rival GD for ship building, which is Huntington Ingalls Industries (HII). Together with GD, HII is expected to be the driving force behind the US Navy plans to go from 290 ships today to 355 ships by 2035 and 500 ships by 2045. If this plan is put into motion fully, it is likely to completely saturate for the next 2 decades the ship building capacities of both General Dynamics and Huntington Ingalls. While HII is also an interesting company, GD is a larger and more diversified company, with HII being focused only on warship building.

So, while these are serious competitors, a hard constrain on shipyard capacities and the expected onslaught of orders by the US Navy should ensure that plenty of contracts are attributed to all. This would make the sector a de facto duopoly, characterized by a demand higher than production capacities, something usually highly profitable for the involved companies and their shareholders.

Multiple Partners

Other large defense companies are more likely to stay partners of GD instead of direct competitors, like for example Honeywell, which already provides parts for the Abrams tanks.

In conclusion, while competition does exist, it is likely to be only serious on the IT and Mission Systems sector of GD activities. Its other sectors should stay marked by low competition and durable economic moat.

Quantitative Analysis

Financials

Revenues

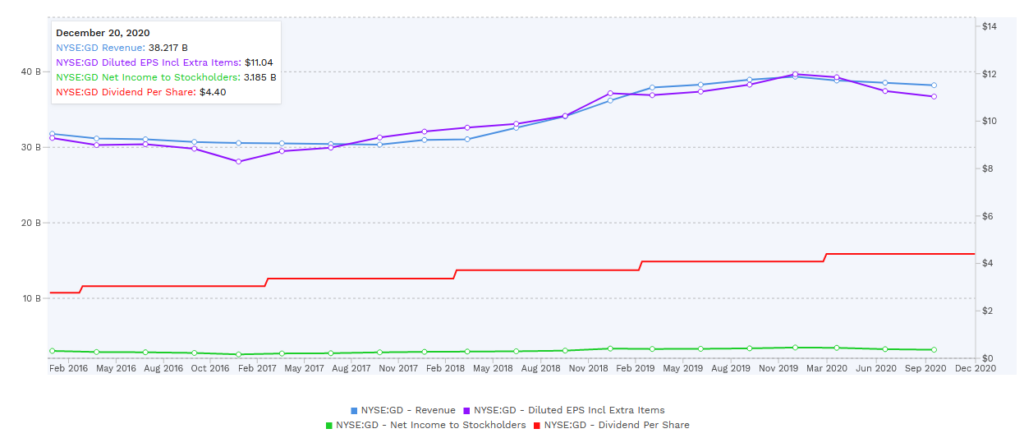

GD is a company with slowly growing business and very low volatility, as reflected in its Revenue, Earning Per Share (EPS) and Dividends. This is best resumed in the chart below. As you can see, GD revenues numbers are matching its profile of a stable quality company, with no sudden change in its activity, and a slowly growing EPS.

Source: www.finbox.com

Dividends

Dividends per share are not that high, with a yield averaging 3% over the past ten years, but it is a nice extra quality to add to the stock profile.

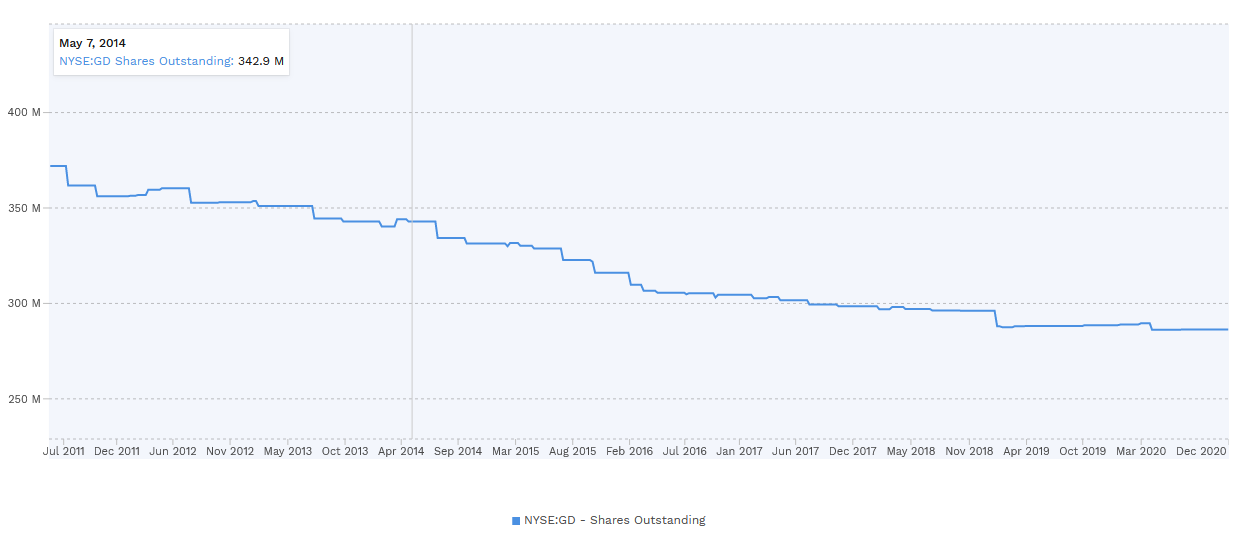

It is worth noting that the company is also consistently conducting stocks buybacks, with shares outstanding getting down from 377 million to 286 million in the last 10 years.

Source: www.stockrover.com

Source: www.finbox.com

Debt and Balance Sheet

GD is not heavily indebted, but its debt has risen massively in 2018, without a corresponding rise in earning or performance to show for the use of that money. This led me to investigate deeper in the 2018 annual report to understand what was done with this $10 billion of debt.

To my discovery, it was mostly used to purchase the company CSRA to improve and extend General Dynamics’s IT offer.

Maybe it might have been needed for strategic reasons, but the low impact it had on EBITDA leaves me a little skeptical it was worth loading the balance sheet with a debt worth as much as a quarter of today’s valuation.

On the other hand, it is not impossible that the integration of CSRA and winning the associated tender might take a few years, as we are talking of very sensitive strategic systems, for which purchase decisions might be especially slow. But all in all, this acquisition, including up to $2.1 billion in goodwill, does not seem to have been worth it, at least not yet.

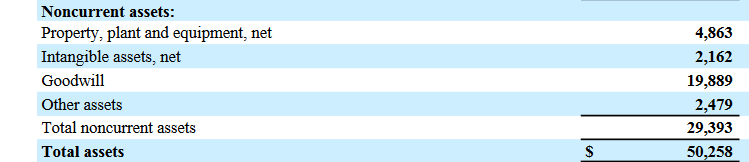

When it comes to goodwill, it is also something a little troubling in the GD balance sheet, with almost $20 billion out of $29.3 billion of non-current assets being marked as goodwill. It is not so much that goodwill does not represent real value, but that it is really hard to judge its proper evaluation or not for non-insiders.

At this point, I would only judge the balance sheet as OK, with total liabilities being $5 billion higher than the total assets minus the goodwill, something that might have been avoided without the acquisition of CSRA in 2018.

Source: www.finbox.com

Source: General Dynamics Annual reports www.gd.com

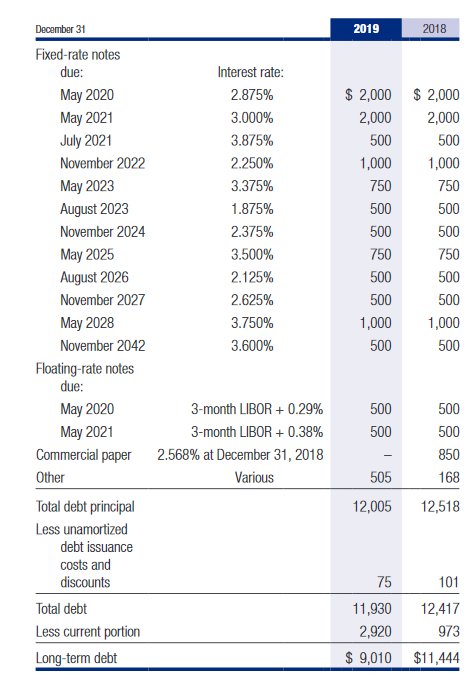

Regarding credit risk, GD has a large amount of its debt reaching maturity in 1-3 years, to the total of $7.6 billion, or more than half of the total. Reflecting the general .lack of transparency regarding the strategy, there is no explanation for keeping such a short debt maturity.

This is especially a matter of interest when low interest rate could be used to lock in the long-term debt at advantageous terms, instead of having to continuously roll-over billions per years.

While the very moderate rate of 3-3.5% is a reflection of GD quality, I think that more fixed rates of 1.875% like the one due for August 2023 would be better and offer more room to breathe regarding re-financing.

It is also not clear if the debt will be quickly repaid or not.

Source: General Dynamics Annual reports www.gd.com

Cash Flow

Now when it comes to cash flow metrics, GD has been remarkably consistent, once again reflecting the steadiness of the company performance. The cashflow might at first look very variable, but the long-term rolling average is actually remarkably stable.

This is due to the nature of GD sales, which depend on signing very large contracts with the government, each the result of multi-stage tenders taking years to be negotiated and won, themselves the result of projects formulated years and sometimes a decade or two ago. This means that when a quarter is abnormally high, it is likely to be followed by an abnormally lower quarter.

I personally consider that as a good thing, as it forces GD management to be focused on the long term instead of the next quarter results.

Source: www.finbox.com

When discussing cash flow, we need to discuss if we trust the management to use it well. While Management seems very competent in using the cash generated to sustain the company’s activity and competitive advantages, I am a little more reserved on other uses.

Acquisitions are not very clearly explained or presented in advance, and acquisition price is not very well justified either. Stock buybacks seem more on an automatic setting than dependent on a cheap enough price to justify them.

I still trust GD management to do an acceptable job at managing the cash generated, but more transparency and a more active approach to the balance sheet management and stock buybacks would be a good change.

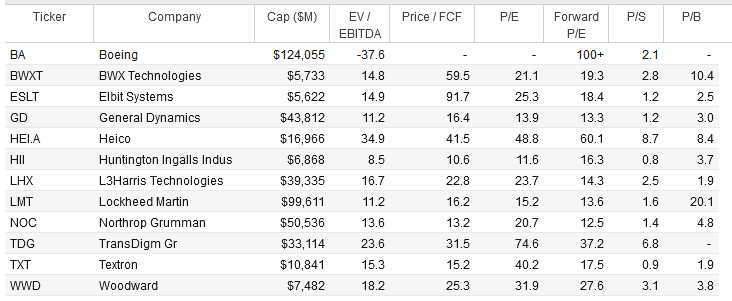

Peer Comparison

Compared to its peers, GD valuation displays rather low multiples, and has one of the lowest P/E in the industry, together with HII. This seems to indicate that the market has so far dismissed the potential of defense naval manufacturers. This is somewhat surprising, despite clear announcements that the USA strategic attention is shifting back to the sea and Asia/Eurasia, something that will require to use its shipyards at full capacity for years to come.

Source: www.stockrover.com

Categorization and Valuation

Investment Category

I can squarely put General Dynamics in the Quality Company category. It has a stable business, solid margins, economic moats, as well as quality management.

Even if somehow, it would experience no growth at all, it would still be a valuable asset in a portfolio. Here is an amazing edge that GD has: as geopolitical landscapes change, like the rise of China for instance, they are poised to ride the ever-increasing wave of rising US military spending. Basically, as long as the USA is the dominant military power and intends to stay that way (which is very likely), GD will make money and receive more orders.

In addition, GD is relatively cheap at the moment, so while not a purely value play, its valuation does not rely on future growth to meet investors’ expectations. And this is without considering upside potential in case of unexpected accelerating military build-up.

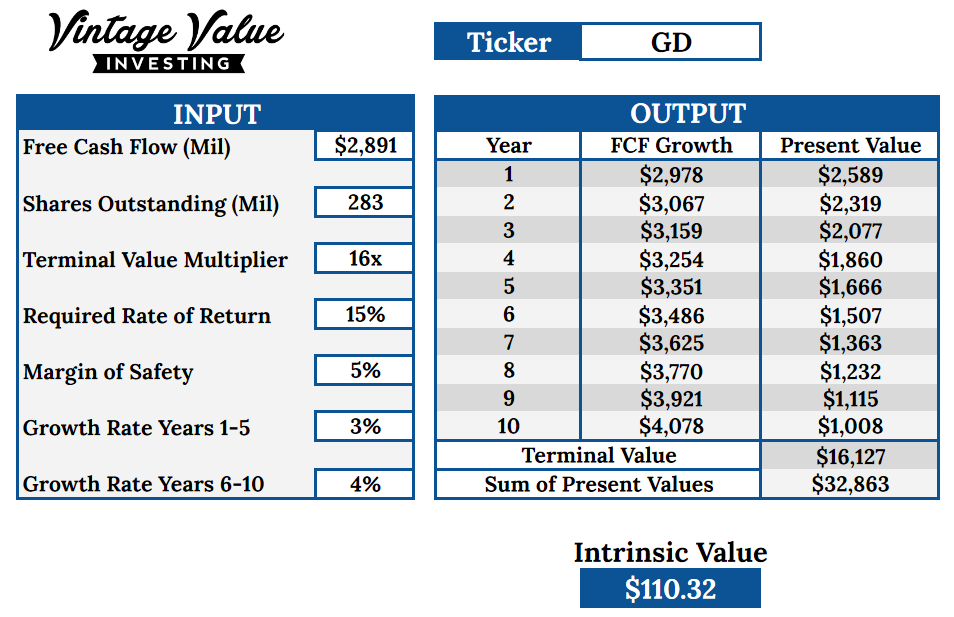

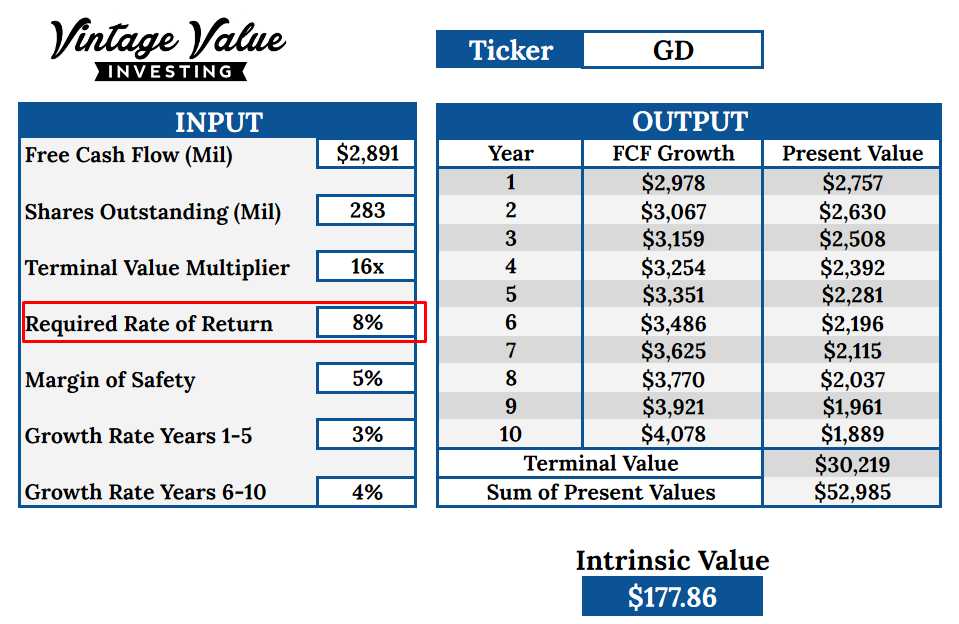

Discounted Cash Flow

One way to calculate GD valuation is using the discounted cashflow model. You can see what it means and how it works here.

According to my discounted cash flow model, even with incorporating a steady growth rate in the next 10 years, the intrinsic value is around $110 per share. You will notice I used an unusually low margin of safety, as this kind of quality steady companies have already incorporated some margin of safety in its business model, thanks to its relation to the US military spending.

With the company trading at $184, it is not at the moment cheap (it actually rose quite a lot the last few months) and might not deliver the 15% annual return we are looking for. Actually, with its current price, we should be ready to satisfy ourselves with “only” 8% rate of return. So not outstanding returns, but also nothing terrible either, especially when considering how stable the company prospects are.

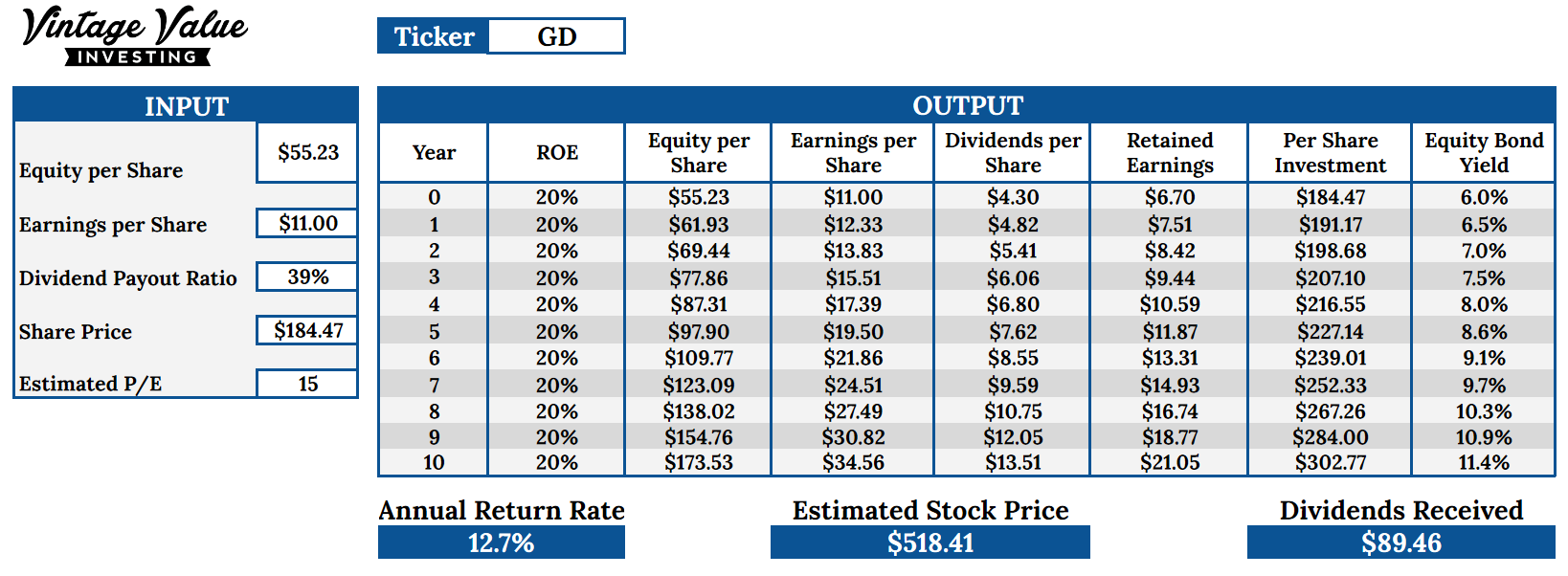

Equity Bond Yield

Equity bond yield is a method that considers GD stock as if it were a bond and calculates the yield it would bring. Instead of basing its calculation on free cash flow, this model uses the Return on Equity (ROE) as a base. You can learn about it in my article here.

This model shows an estimated annual return rate of 12.7%, which would make GD an okay buy, even if below my preferred 15% returns.

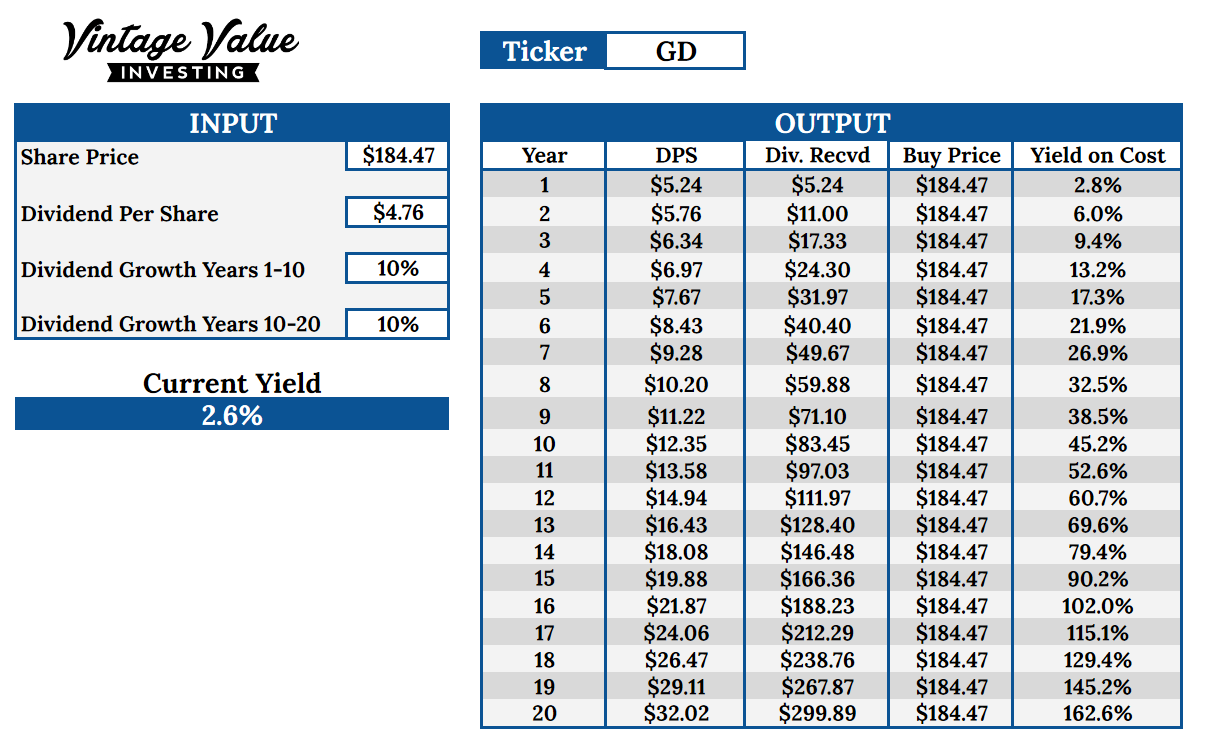

Yield on Cost

The Yield on Cost calculation method is made to evaluate the value of a stock according to its dividend yield only. As GD dividend yield is pretty low, this is probably not the best method to judge the company. Most returns to shareholders will be in the form of stock buybacks and company growth, both contributing to an increase of the shares price.

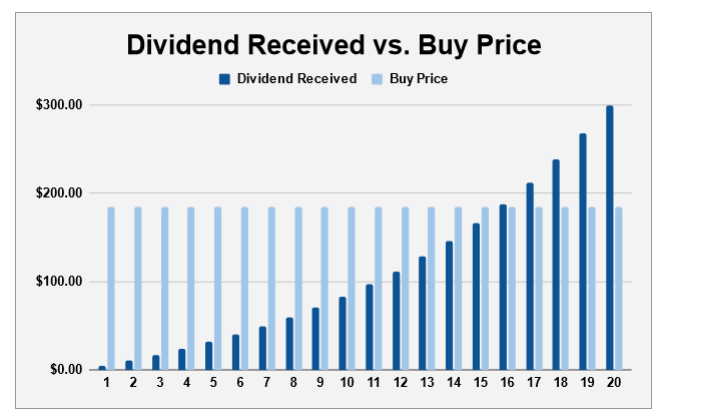

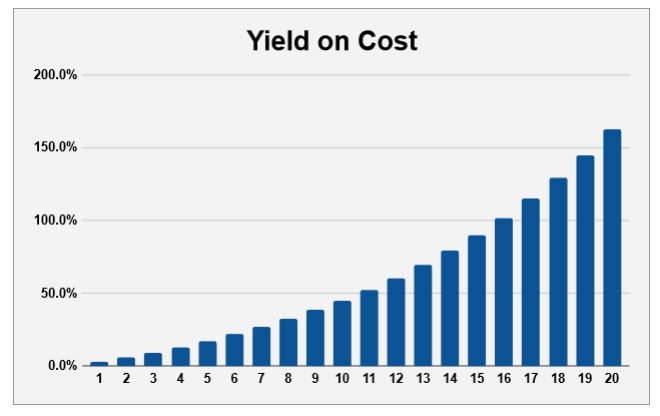

So, if the dividends is not bad in itself, it should not be the reason to purchase GD stock, nor is it a good way to value the company. As you can see in the graphs below, relying on dividends alone, it would take a decade and half for the dividends to even just cover the buy price of the stock.

Final Assessment

Company Synthesis

General Dynamics is a solid company, with exceptionally stable earnings and good prospects. It benefits from multiple very solid moats, reduced competition, and very low disruption risk.

Its main client is one the most consistent and solvable on Earth (the US Military), and short of a complete doom and gloom economic collapse, it is likely to keep doing fine over the next decades. But obviously, if you think that the USA is going to go bankrupt any time soon, you would not be interested in General Dynamics in the first place. I would even argue that any perception of weakness by USA competitors is likely to lead to increased tensions, which would translate in more orders to GD. So even a weakening of the USA international position should not impact negatively on the company, quite the contrary.

On the upside, if tensions with China and Russia keep rising over the next decades, a likely scenario no matter who is the president, GD has massive potential to overshoot. Not only thanks to rising cash flow and earnings, but also with increasing multipliers when the defense industry comes back into favor with the market.

Short-Term Projection: 1-5 years

In the short term, GD is very likely to keep a very steady cash flow and return on capital, most of its income coming from tenders and contracts already signed.

The backlog was at the staggering amount of $87 billion in 2019, and is probably the best number to keep eyes on for monitoring GD’s short term income.

Long-Term Projection: 5-10 years

GD management is rather shy of explaining extensively their long-term strategy. This might be due to defense secrets, or to not inform their competitions. But in my opinion, GD long term results will depend on a few factors:

- The continuation of the massive shipbuilding program of the US Navy plans, and no significant budget cut to defense spending.

- The successful proposal of a successor to the Abrams main battle tank.

- A growing activity in cyberdefense.

- Well targeted acquisitions only at a proper price.

While GD does not need to perform perfectly on each of these topics to stay a good company, any serious failure would severely damage its prospect in one of its key sectors or waste shareholder capital in unneeded or too expensive diversification.

Very Long-Term Projection: 10+ Years

It is hard to predict military strategy and technology in the very long term. But as a high-quality company, GD should be able to still be a success story in the 2030s and beyond if does the following things:

- Keep sufficient R&D spending in the 2020s to keep its technology up to date.

- Progressive switch to unmanned vehicles and weapon platforms and increase automatization for its manned systems.

- Adaptation to new threats, like drone swarms, hyper-sonic weapons or advanced robotics.

- Keep core activities in its centers of focus: cyberdefense, land vehicles and ships. Diversification into military aerospace or small arms would consume a lot of capital and expose it to a much larger competitive pressure.

- Continuation of USA’s capacity to maintain a very large military budget.

Valuation

GD is at the moment a little expensive for me to confidently expect it to bring my targeted 15% annual return. While the equity bond yield model paints a rather good picture, the discounted cash flow model does not, and I prefer to err on the side of caution.

But this does not mean it is not a possible buy, as it is also a stock that, at current valuation, is offering very high chance of stable and decent return, probably somewhere in the range of 8-12%. This comes with good upside optionality, considering the current instability in international affairs. Actually since I started looking at GD, the situation in Ukraine or the Sea of China just seems to get worse. So even with conservative expectations, GD should hold well as an investment compared to the S&P500 or other index funds.

GD could be a capital safe haven, possibly reducing your portfolio volatility, without giving up on decent returns. With the S&P 500 at an all-time high, GD might offer a greater margin of safety than index funds.

If for some reasons unrelated to a degradation of the business quality, the market starts to price GD lower and closer to the $100 mark, it would then turn it into a great compounder to hold for the next 10-20 years and expect annual 15% returns from it.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in GD and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.