Credit Strong provides credit builder loans and a range of products tailored for creating personal and business credit. These offerings are crafted to put both installment and revolving accounts on your credit record.

Credit Strong

Credit Strong provides credit-building products with no credit check. They can help build your credit score by diversifying your credit mix and improving your payment history with timely payments. Credit Strong’s products will be most effective if you have a thin credit file with few or no installment loans.

Pros

Easy to qualify

No credit check

Effective at building credit

Wide variety of account options

Cons

Expensive compared to secured credit cards

Credit Strong is legit, and their accounts can definitely boost your score if you use them correctly. They’re especially effective if you have a thin credit file with a small number of accounts.

They also have several options to choose from, which lets you prioritize the type of account and the terms that are most appropriate for you.

You’ll have to pay interest and fees for the privilege, so it’s not the cheapest way to raise your score. There are ways to build credit for free.

What is Credit Strong?

Credit Strong’s primary purpose is to build credit, and it does a reasonably good job. They claim to have studied 50,000 of their customers’ accounts and found that people saw the following changes to their FICO 8 score on average:

- A 25-point increase within three months

- An almost 40-point increase after nine months

- Just shy of a 70-point increase after a year if they made all payments on time

👉 People who started the process with no score and paid on time for a year finished with a credit score between 630 and 650.

These are solid results but not irreplicable. You could probably get the same or better results by sticking with a traditional installment loan for a year.

The advantage of Credit Strong is that it’s easy to qualify for their accounts. They hold onto your loan proceeds until the end as collateral, so they don’t even have to check your score.

In addition to helping you build credit, Credit Strong claims that they help you save money. That’s true in some sense, but only in that signing up for your monthly Credit Strong payments commits you to put some of your paychecks aside.

Once you’ve paid off your account, you get back the portion of your monthly payments that went toward paying off the principal amount of the loan.

⚠️ You’d save far more money if you just committed to putting the same amount each month into a savings account, so don’t use Credit Strong as a way to save money.

Build credit while you save money. No credit required, no security deposit, easy approval!

How Does Credit Strong Work?

Credit Strong offers several types of accounts, all designed to help you build credit.

Instal

Credit Strong’s Instal product offers credit-builder loans. These loans work like reverse installment loans. The money you borrow is placed in a locked account. You make monthly installments toward principal and interest. When the loan is fully paid, the entire sum is released to you.

Because Credit Strong keeps the money, there’s no real risk to them. They can offer loans with no credit check.

You can choose from three plans. Each plan carries a one-time fee of $15.

- The 24-month plan has a $48/month payment and reports a $1,000 installment account. You get 24 months of credit history, and you get $1000 at the end of the loan period.

- The 36-month plan has a $38/month payment and reports a $1,100 installment account. You get 36 months of credit history, and you get $1,100 at the end of the loan period.

- The 48-month plan has a $28/month payment and reports a $1,010 installment account. You get 48 months of credit history, and you get $1,010 at the end of the loan period.

Longer loan terms will have a greater impact on your credit score, as you will build the length of your credit history and your payment history simultaneously. Of course, you will have to make on-time payments to build credit effectively!

You can cancel the loan, and the money you have paid toward the loan principal will be refunded. You should be aware that a large percentage – up to 44% – of your early payments will be applied to interest. If you cancel early, you may get less back than you expect!

Revolv

Credit Strong’s Revolv product adds a revolving credit account to your credit file, making it a good choice if you are already paying an installment loan (like a student loan) but don’t have a credit card.

If you have a credit card already, Revolv can increase your credit limit, which can lower your credit utilization and boost your credit.

As soon as you open your account, a $500 revolving credit account will be reported to the three major credit bureaus. You choose an amount to pay monthly, which is placed in a locked account. 100% of this amount is released to you when the account matures.

If you make three on-time payments in a row, you will get a $100 credit limit increase, up to a maximum of $1000. This should further improve your credit utilization. You’ll also get free FICO score access.

The account works as a digital credit card with a 0% APR.

Revolv requires a $99 annual subscription.

CS Max

Credit Strong’s CS Max is a specialty product designed for people who “have the cash but not the credit”. It’s a credit-builder loan but with much larger amounts than the Instal loans.

CS Max is designed for borrowers who want to place a larger loan on their record to demonstrate that they are capable of managing larger credit obligations.

All CS Max loans have 60-month terms, a one-time $25 administrative fee. The four plans vary only in their sizes.

- $49/month, reporting a $2500 installment account.

- $99/month, reporting a $5000 installment account.

- $199/month, reporting a $10,000 installment account.

All plans can be cancelled at any time without penalty.

These plans will add a substantial amount to your debt-to-income ratio, so they are probably not a good idea if you are considering applying for a mortgage or car loan soon.

Be sure that you can make the payment you commit to, because late payments will harm your credit score.

Credit Strong Business Accounts

Credit Strong’s business accounts are designed to build a business credit profile for businesses that have an EIN (Employer Identification Number). These accounts work much like the Instal account, but for a business.

There are several plan options, all with 25-month terms.

- A $200/month plan with no interest but a $349 one-time fee, reporting a $5000 installment account.

- A $400/month plan with a $549 one-time fee, reporting a $10,000 installment account.

- A $1,000/month plan with no interest but a $749 one-time fee, reporting a $25,000 installment account.

- A $2,000/month plan with a $999 one-time fee, reporting a $50,000 installment account.

There are also several plan options with 50-month terms.

- A $100/month plan with no interest but a $349 one-time fee, reporting a $5000 installment account.

- A $200/month plan with a $549 one-time fee, reporting a $10,000 installment account.

- A $500/month plan with no interest but a $749 one-time fee, reporting a $25,000 installment account.

- A $1,000/month plan with a $999 one-time fee, reporting a $50,000 installment account.

These accounts report to Equifax, Paynet, and SBFE, with plans to add Dun & Bradstreet and Experian.

How to Sign Up for Credit Strong

Signing up for Credit Strong is a lot easier than applying for a traditional installment account. They don’t pull your credit report or check your credit score, so the only requirements for getting an account per their website are:

- Have a cell phone number, Google Voice account, and email address.

- Be 18 years old and a permanent U.S resident with a physical U.S. address.

- Have a valid social security number or individual taxpayer identification number.

- Have a checking account, debit card, or prepaid card in good standing.

- You will need an EIN number to use the business products.

☝️ Credit Strong is available in every state except for Wisconsin and Vermont. These states have laws that prevent secured consumer lending or make it too costly to implement.

You can sign up by filling in the application form on Credit Strong website.

How to Use Credit Strong

While your Credit Strong account is open, you make payments on it like any installment debt. The amounts go to both principal and interest, with more going toward interest in the earlier years.

You can make your payments through your checking account or debit card, including some prepaid cards. There are often fees if you pay with a card, so it’s better to use your bank account.

👉 Tip: You can set up an autopay to make sure you never miss a payment. If you don’t, you have a 14-day grace period before they’ll report you as late and charge you for it.

As you make your payments, Credit Strong reports them to all three major credit bureaus: Experian, Equifax, and TransUnion. They’ll give you your Transunion FICO 8 Score monthly so you can monitor your progress as you go.

How to Cancel Credit Strong

One of the primary benefits of credit builder loans like Credit Strong is that they generally let you cancel your account at any point. That significantly reduces the risk of you hurting your score because you can’t afford your payments.

There are no fees for canceling, and you’ll get back any principal that you’ve accumulated to that point. The easiest way to tell Credit Strong that you don’t want to continue is to call their customer support at (833) 850-0850.

👉 Important Note on Cancellation: If you cancel your loan you will get back the money that has been applied to your loan principal. In the early stages of repayment, Credit Strong applies most of your payment to interest. If you cancel early you may get back only a small amount of what you put in.

Credit Strong Pricing

Credit Strong offers several types of installment accounts and one revolving credit option, each targeting a different audience. Within each category, there are at least two options, all with different pricing.

The Credit Strong website has clear pricing information, so when you’ve identified your preferred option you can check the cost and compare with other options.

You always have the option to pay your balance in advance or cancel your account entirely, so the repayment terms aren’t a requirement. Cancellation will reduce the account’s impact on your credit by reducing the number of timely payments you make.

The account will remain on your credit report after it is paid off, but its impact on your credit score will be greatest while the account is active.

Build credit while you save money. No credit required, no security deposit, easy approval!

Credit Strong Customer Reviews

Like many credit-related products and services, Credit Strong receives mixed customer reviews. It’s hard to find an accurate average rating for them because crowdsourced reviews often include fake profiles, and upset people are more likely to leave comments.

However, there are some noticeable trends.

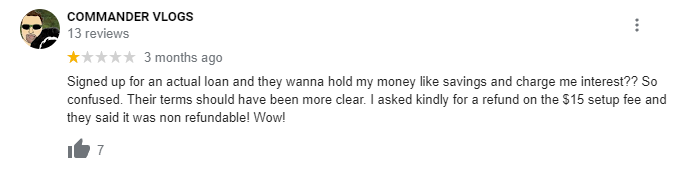

👇 For example, many of their negative reviews are due to confusion over how the accounts work. People who apply expecting to get an installment loan are, of course, going to be severely disappointed.

Here’s an example from Google Reviews.

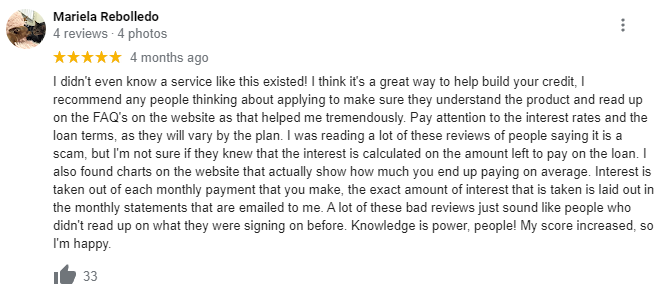

There are some complaints from people who have difficulties logging into the account or found the customer service people unhelpful. But for the most part, users who understand the nature of credit builder loans are often satisfied with their results, more or less.

Here’s another example from Google:

The lesson from these reviews is simple: if you understand the product before you sign up, you’re less likely to be disappointed.

Credit Strong Alternatives

There’s no shortage of credit builder loans on the market, and all of them follow a similar pattern. You can apply and qualify without a credit check. Once you get approval, you make payments until you’ve paid off the principal balance, at which point you’ll get that amount back in cash.

There are differences in their terms, though. Here’s an overview of some other options.

| Self | MoneyLion | Digital Federal Credit Union | |

|---|---|---|---|

| Minimum Monthly Payment | $25 | $43 plus $19.99 monthly membership fee | $43.87 per $1,000 in principal |

| Principal Amounts | $600 to $1,800 | $500 to $1,000 | $500 to $3,000 |

| Max Repayment Term | 24 months | 12 months | 24 months |

| Annual Percentage Rate | 15.65% to 15.97% | 5.99% to 29.99% | 5% |

| One-Time Admin Fee | $9 | N/A | N/A |

| Learn More | Learn More | Learn More |

Before applying for a credit-building account, make sure you confirm that it reports to all three credit bureaus. Some products don’t.

Learn More: Read our detailed comparison of the best credit builder loans available today to see how Credit Strong measures up.

Is Credit Strong Worth It?

Credit Strong can legitimately help you rebuild a damaged credit score or create one from scratch. It’s most effective if you have a thin credit file with few or no installment loans.

If you are starting out with credit building, you may have revolving credit, like a secured card or even being an authorized user on someone else’s card, on your record. If you don’t have an installment loan on your record (like a student loan or car loan), a credit builder loan could be an effective way to improve your credit.

☝️ The main problem with Credit Strong is inherent to credit builder loans in general. You’re paying money for the privilege of building your credit.

Say you take the $15 Build Credit Strong account and keep it open for a year. You’d end up putting $180 into the account after twelve months, but if you cancel then, you’d only get back $52.

If you use a secured credit card instead, you could build your credit without paying interest. It won’t diversify your credit mix if you lack installment accounts, but it should be about as effective at improving your score over time anyway. Payment history is more important to your credit score than your credit mix.

The downside to secured cards is that you have to fund a deposit (which will tie up some money) and undergo a credit check. You also don’t have the luxury of canceling your account for free if you think you’re going to miss a payment.

However, you can get a secured card with a deposit as low as $200. Because of the cash collateral, they’re easy to get even with bad credit. Once you have the account, you can spend as little as you need to build credit without risk.

If you do decide that a credit builder loan is the right move for you, Credit Strong offers a very useful product that’s worth considering. The main question you’ll need to answer is whether you want to use a credit builder loan or not.

How We Review the Products in This Category

We rate products by comparing them to similar products. In this case, that means comparison to other credit builder loans and, to a lesser extent, to other credit-building tools. Here’s a summary of the rating criteria.

Effectiveness

This is based on the number of credit bureaus reported to, the type of account reported, and the length of history provided. Credit Strong reports an installment loan to all three major credit bureaus for a relatively high score, reduced only for a potentially short loan term.

Cost

Building credit doesn’t have to cost money. Credit-builder loans can run up substantial interest expenses and generally get mediocre marks in this category.

Ease of Use

Ease of use is primarily determined by user reports from customer reviews. Most reports suggest that setting up a Credit Strong account is easy and straightforward, hence the high score.

Support

Support scores are also based largely on customer reviews. All products have some issues, and you want to be sure that you can get quick and effective solutions if something goes wrong. Reviews indicate some customer service issues with Credit Strong. These may be partly due to misunderstanding or unreasonable expectations on the part of some users, but there’s still cause for concern.