If your credit score is between 670 and 739, you have good credit. It’s a solid level and you’ll get approved for many credit cards. With so many options, finding the best credit cards for good credit may not be easy. This guide is here to help.

Remember that no card is right for everyone. Look for the option that best fits your individual needs and spending patterns!

| Annual Fee | Regular APR | Intro offer | Rewards | |

|---|---|---|---|---|

| Chase Freedom Unlimited | $0 | 20.49%–29.24% (Variable) | Yes | Yes |

| Credit One Bank® Platinum X5 Visa® | $95 | 29.24% (Variable) | No | Yes |

| Discover it® Chrome | $0 | 17.24% – 28.24% (Variable) | Yes | Yes |

| Blue Cash Everyday® Card from American Express | $0 | 19.24% – 29.99% (Variable) | Yes | Yes |

| BankAmericard® credit card | $0 | 16.24% – 26.24% (Variable) | Yes | No |

| Chase Sapphire Preferred | $95 | 21.49%–28.49% (Variable) | No | Yes |

| Marriott Bonvoy Boundless® Credit Card | $95 | 21.49%–28.49% (Variable) | No | Yes |

| Capital One SavorOne Cash Rewards Credit Card | $0 | 19.99% – 29.99% (Variable) | Yes | Yes |

| Citi Custom Cash℠ Card | $0 | 19.24% – 29.24% (Variable) | Yes | Yes |

9 Best Credit Cards for Good Credit

When looking for the best credit cards for good credit we took the following things into account:

- Is there an annual fee?

- Is there a fee on international spending?

- What other fees does the card have?

- What is the APR (Annual Percentage Rate)?

- Does the card offer rewards?

- Does the card have a signup bonus?

- Does the card have any other perks?

Here are our top picks for the best credit cards for good credit:

BEST NO FEE CARD

Chase Freedom Unlimited

Annual Fee

$0

Regular APR

20.49%–29.24% (Variable)

Intro offer

Yes

Rewards

Yes

🎁 Rewards: The Chase Freedom Unlimited card gives you an unusually high range of rewards for a no-fee card. In the first year, you’ll have these benefits:

- A $200 bonus if you spend $500 on purchases in your first three months.

- Earn 5% cash back on travel purchased through Chase Ultimate Rewards.

- Earn 3% on drugstore purchases.

- Earn 1.5% on all other purchases.

Cash rewards do not expire as long as your account is open.

💳 Intro Offer: You’ll also have a 0% Intro APR on purchases and balance transfers in your first 15 months. After that, the APR will be between 20.49%–29.24%, depending on your credit score.

👎 The downside: you’ll have to activate your participation in each quarterly spending category.

REWARDS FOR EVERYDAY SPENDING

Credit One Bank® Platinum X5 Visa®

Annual Fee

$95

Regular APR

29.24% (Variable)

Intro offer

No

Rewards

Yes

The Credit One Bank Platinum X5 Visa is a rewards card that gives you a good chance at earning enough rewards to cover the (rather steep) annual fee.

🎁 Rewards: You’ll get 5% cash back on the first $5,000 of eligible gas, grocery, internet, cable, satellite TV, and mobile phone service purchases each year and then 1% thereafter. You’ll get 1% on other purchases within the card’s terms.

That covers a large part of most people’s daily spending. There’s no limit to the rewards you can earn, and the cash back is credited to your statement automatically.

👎 The downside: the annual fee is $95, so you’ll need to spend roughly $1900 in those 5% categories before you’re getting ahead.

There is a foreign transaction fee, so this isn’t the card to use for travel. The APR is high at 29.24%, so you’ll want to pay off your balance in full each month.

BEST FOR FREQUENT ROAD TRAVELERS

Discover it® chrome

Annual Fee

$0

Regular APR

17.24% – 28.24% (Variable)

Intro offer

Yes

Rewards

Yes

If you spend time on the road for work or pleasure, consider the Discover It Chrome Credit Card. The regular APR ranges from 17.24% to 28.24%. There’s a handy app that lets you pay your bill, track and redeem your rewards, and view your FICO score from your phone.

🎁 Rewards: You’ll get 2% cash back at gas stations and restaurants, up to $1000 in combined purchases each quarter. That’s up to $800 a year! You’ll earn 1% cash back on all other purchases as well, and at the end of your first year with the card Discover will match your rewards in a 2x promotion. There’s no annual fee, so the rewards stay with you.

💳 Intro Offer: There’s a 0% intro APR for 15 months on both purchases and balance transfers.

👎 The downside: if you don’t spend a substantial amount on gas and restaurants, this probably isn’t the card for you.

BEST FOR GAS AND GROCERIES

Blue Cash Everyday® Card from American Express

Annual Fee

$0

Regular APR

19.24% – 29.99% (Variable)

Intro offer

Yes

Rewards

Yes

🎁 Rewards: The Blue Cash Everyday Card from American Express focuses its rewards on basic spending categories.

- 3% cash back at US supermarkets up to $6000 per year, 1% after you pass the $6000 mark.

- 3% cash back at US gas stations up to $6000 per year, 1% after you pass the $6000 mark.

- 3% cash back on U.S. online retail purchases up to $6000 per year, 1% after you pass the $6000 mark.

- 1% on all other purchases.

- You earn a $200 statement credit if you spend $2,000 in the first 6 months.

Terms apply to all benefits. Read your cardholder agreement carefully.

💳 Intro Offer: There’s a 0% intro APR on purchases for 15 months after you open the account. After that, the APR is from 19.24% to 29.99%.

👎 The downside: the minimum credit score is 700, so you’ll need to be in the upper half of the “good” range.

BEST BALANCE TRANSFER CARD

BankAmericard® credit card

Annual Fee

$0

Regular APR

16.24% – 26.24% (Variable)

Intro offer

Yes

Rewards

No

Balance transfer cards are a popular way to consolidate credit card debt. If you’re looking for a card for this purpose, the BankAmericard Credit Card will be a strong contender.

The card has no annual fee, and there’s no penalty APR: if you make a late payment, you won’t lose the 0% intro APR. You even have free FICO score access, and there’s a range of security features.

The regular APR is from 16.24% to 26.24%, and the minimum credit score is 670.

💳 Intro Offer: There’s a 0% intro APR for 18 billing cycles for both purchases and balance transfers made in the first 60 days, giving you plenty of time to pay off those transferred balances. You will pay a 3% fee for each balance you transfer.

👎 The downside: you won’t be able to transfer a balance from another Bank of America card.

BEST TRAVEL CARD

Chase Sapphire Preferred

Annual Fee

$95

Regular APR

21.49%–28.49% (Variable)

Intro offer

No

Rewards

Yes

The Chase Sapphire Preferred Card is a top pick for an all-around travel card.

There’s no foreign transaction fee. The APR is 21.49% to 28.49%.

🎁 Rewards: The card offers a range of rewards:

- 80,000 bonus points if you spend $4000 on the card in the first 3 months.

- Up to $50 in statement credits each account anniversary year for hotel stays purchased through Chase Ultimate Rewards.

- 3x points on dining, takeout, and eligible delivery services.

- 3x points on online grocery purchases (excluding Target, Walmart and wholesale clubs).

- 3x points on select streaming services.

- 1 point per dollar spent on other purchases.

- If you redeem your points through the Chase Ultimate Rewards program, you get 25% more value. 80,000 points are worth $1,000 toward travel when redeemed through Chase Ultimate Rewards.

- 1 to 1 points transfer program to many hotel and airline loyalty programs lets you combine your points for maximum effect.

👎 The downside: there’s a $95 annual fee. If you travel frequently, it may be worth it. If you don’t, it’s probably not.

BEST FOR FREQUENT HOTEL USERS

Marriott Bonvoy Boundless® Credit Card

Annual Fee

$95

Regular APR

21.49%–28.49% (Variable)

Intro offer

No

Rewards

Yes

If you regularly spend on hotels, consider the Mariott Bonvoy Boundless Credit Card.

The APR is from 21.49% to 28.49%, depending on your credit. There’s no foreign transaction fee.

🎁 Rewards: There are numerous travel and hotel-related rewards.

- 3 free night awards plus 10x total points if you spend $3000 in your first 3 months.

- 3x total points for every $1 on the first $6,000 spent in combined purchases each year on gas stations, grocery stores, and restaurants.

- 6x points for every dollar spent at 7,000 participating hotels.

- 10x points from Mariott.

- 2 points for every dollar spent on other purchases.

- Free night award every anniversary.

👎 The downside: there’s a $95 annual fee. If you’re a heavy spender on hotels and travel it’s probably worth it. If you aren’t, look elsewhere.

BEST FOR FREQUENT RESTAURANT DINERS

Capital One SavorOne Rewards Credit Card

Annual Fee

$0

Regular APR

19.99% – 29.99% (Variable)

Intro offer

Yes

Rewards

Yes

Here’s one for the foodies: the Capital One SavorOne Cash Rewards Credit Card. There’s no annual fee or international transaction fee.

🎁 Rewards: Here are the rewards:

- Unlimited 3% cash back on dining, entertainment, grocery stores, and popular streaming services.

- 5% cash back on hotels and rental cars booked through Capital One Travel.

- 10% cash back on purchases through Uber and Uber Eats.

- 1% cash back on other purchases.

- Use your rewards for PayPal or Amazon purchases.

- Earn a one-time $200 cash bonus if you spend $500 on purchases within the first 3 months from account opening.

💳 Intro Offer: There’s a 0% intro APR on purchases for 15 months and a 19.99% – 29.99% APR after that.

👎 The downside: you’ll probably need a credit score over 700 to qualify. That figure is not provided by Capital One, and a higher score does not guarantee approval. If you have defaults, bankruptcies, or very late payments on your record, you may not be approved.

Capital One also offers the Savor Rewards from Capital One card, which has a higher introductory bonus and higher rewards. There’s no 0% intro APR, though, and you’ll have to eat out a lot for the extra rewards to be worth the $95 annual fee.

BEST CUSTOMIZED CASH BACK

Citi Custom Cash℠ Card

Annual Fee

$0

Regular APR

19.24% – 29.24% (Variable)

Intro offer

Yes

Rewards

Yes

The Citi Custom Cash Card offers a uniquely flexible rewards program with no annual fee.

🎁 Rewards: The card breaks your spending into categories: restaurants, gas stations, groceries, selected travel & transit, drugstores, home improvement stores, fitness, and live entertainment. You’ll get 5% cash back on your highest spending category in each billing cycle, up to $500. You’ll get 1% cash back on purchases in that category over $500 and on all other purchases. You don’t have to select a category: the card adjusts to your spending.

You can redeem your rewards as a direct deposit, a statement credit, a check, or other redemption options, including gift cards, travel, and Amazon shopping.

💳 Intro Offer: There’s a 0% intro APR for 15 months on purchases and 15 months from the date of your first transfer for balance transfers. The regular APR is 19.24% – 29.24%.

You’ll earn $200 cash back if you spend $1,500 on purchases in the first 6 months with the account.

👎 The downside: A penalty APR may be applied if you make a late or returned payment, and there’s a foreign transaction fee.

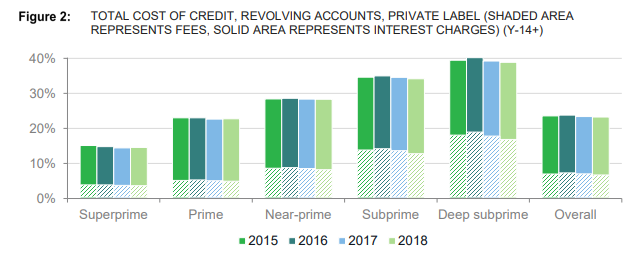

Watch Those APRs

All of these cards offer a range of APRs. The lowest rates will be reserved for cardholders with very good or excellent credit. If your credit is good, and especially if it’s at the lower end of the “good” range, your APR will be at the upper end of the cited range.

Look at the difference in the cost of credit between the “superprime” and “prime” categories and you’ll get a sense of the difference.

Source: Consumer Financial Protection Bureau

Even if you aren’t “superprime”, you can control your interest costs. Pay each bill in full on or before the due date, and you won’t pay interest at all!

Choosing the Right Credit Card for Good Credit

If you have good credit, you are eligible for a huge range of credit cards. None of them is “best” for everyone. You need to consider your spending style and your personal needs.

Many credit cards offer rewards. These can be a real bonus, but they aren’t always.

Credit card companies don’t offer rewards out of the kindness of their hearts. Credit card companies don’t have kind hearts. They don’t have hearts at all. They offer rewards to encourage you to spend more, carry balances, and pay them interest. That works for them, but it may not work for you.

Consider these points before you choose a card because of its rewards.

- Does the card have an annual fee? If it does, how much will you need to spend on the card every year for the rewards to be worth more than the fee?

- Do the rewards align with your spending habits? Different cards offer rewards for different types of spending. You need to choose one that fits the way you spend.

- Will you spend more just to earn rewards? Many people fall into the trap of using their cards to earn rewards. If you end up carrying a balance, your interest spending will quickly exceed the value of the rewards. The Company wins.

Always be aware of your credit limit. You want to keep your balance as far under 30% of that limit as you can. That keeps your credit utilization low and helps your credit.

If your credit limit is low or if you just don’t want to use your card much, you might want to look for a simple zero-fee card rather than pursuing rewards. Rewards exist to encourage you to use your card a lot. If you were planning to do that anyway, that works for you. If you don’t see yourself as a high credit card spender, rewards shouldn’t be your priority.

One More Step

Good credit is not a guarantee of approval for any of these cards. Your entire credit record will be considered, and if you have serious black marks in your past, you may not be approved, especially if your credit score is at the lower end of the “good” range. If you want sure approval and the best terms, you’ll want to step it up to “very good” or even “excellent”.

Good credit is an accomplishment. If you’ve gotten that far you probably have a good idea of how to take that final step up to the top credit tier. Manage your cards and other credit well, and you can get there!