Table of contents:

Quick Stock Overview

ZIM by the numbers.

1. Executive Summary

A brief discussion of ZIM and its potential appeal to value investors.

2. Extended summary

A more detailed explanation of ZIM ‘s business and competitive position

3. Industry Overview

A primer on the shipping industry.

4. ZIM profile

An overview of ZIM: business profile, business model, and its unique competitive advantages

5. Financials

ZIM by the numbers: balance sheet, free cash flow, and a high dividend yield

6. Conclusion

Why ZIM is worth a closer look.

Quick Stock Overview

Ticker: ZIM

Source: Yahoo Finance

Key Data

| Industry | Marine Shipping |

| Market Capitalization ($M) | $8,870 |

| Price to sales | 0.8 |

| Price to Free Cash Flow | 1.8 |

| Dividend yield | 13.4% |

| Sales ($M) | 8,623 |

| Free cash flow/share | $30.35 |

| Equity per share | $38.35 |

| P/E | 1.9 |

1. Executive Summary

ZIM Integrated Shipping Services is a shipping company specializing in container transportation. The company is a small actor in the industry, controlling only 1.5% of the total sea freight market. Stock Spotlight hasn’t covered a shipping company since DHL, and I wanted to wait for one with solid management at a decent price.

Based on 2021 numbers, ZIM is selling at a radical discount. But this would be ignoring the fact that the shipping industry is highly cyclical and supply chain problems have supercharged the whole industry’s earnings. So in that respect, we need to take the record-breaking recent results with a grain of salt. 2021 is in no way a normal year for the sector.

To illustrate that, we can look at ZIM’s valuation, which is somewhat in line with Chinese Cosco and cheaper than Danish industry leader Maersk. The whole industry is either cheap or making a lot of cash.

| ZIM | Cosco | Moller-Maersk | |

|---|---|---|---|

| Market cap ($B) | 9.2 | 30.4 | 54.5 |

| Revenue ($B) | 8.6 | 45.1 | 61.7 |

| Price to free cash flow | 1.7 | 1.5 | 3.1 |

| Price to sales | 0.8 | 0.7 | 0.9 |

What makes ZIM more worthy of attention than just relative cheapness is its business model. The company has a strong focus on innovation and on cost optimization. Its smaller size also means it operates smaller ships instead of the mastodons of the larger companies. As I will explain, this should give a hedge compared to larger ships in the middle of the supply chain clogging.

It also operates an asset-light business model, able to optimize the size of the fleet to market conditions, providing some margin of safety in case of a downturn. This model allowed it to quickly access LNG-fueled ships to reduce its exposure to rising fuel costs.

In addition to the long-term market positioning and costs, ZIM is also pursuing a prudent financial strategy with a focus on returning profit to shareholders. Debt has been reduced radically with the 2021 windfall, and dividends are high enough to ensure a strong and regular yearly yield.

Finally, ZIM has also aggressively positioned itself to benefit from rising energy costs, upgrading its fleet to newer fuels. With pollution regulation tightening, this will help avoid expensive upgrades or fines that will hit competitors’ less advanced or aging fleets. This might also raise ZIM’s ESG profile and help attract more attention from ESG funds and investors.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

2. Extended Summary: Why ZIM?

Why Shipping?

Shipping has turned from a loss-making industry to a cash machine since 2020. Normally, we’d expect this highly cyclical sector to be moving into a slowdown. But with durable damages to the world shipbuilding capacity, the shortage of shipping capacity is here to stay longer than normal. Aging fleets and clogged harbors are also going to help maintain high freight rates for a longer than usual period.

Poised to Rip the Shipping Boom

ZIM is a global company active in sea-borne freight, and a small actor in its industry (1.5% of total volume). It specializes in smaller and quicker ships. In addition to operating ships, the company is also providing SaaS solutions to its clients for shipping and international logistics. The company operates an asset-light business model, “renting” ships instead of owning them. This gives its more flexibility to manage unstable market conditions.

Armored Balance Sheet and High Dividends

ZIM has significantly de-risked against a recession thanks to prudent balance sheet management and debt reduction. Free cash flow in 2021 was equal to half of the current market cap. Thanks to the asset-light model, the company should be able to adapt to unstable market conditions. The dividend policy is very friendly to shareholders, with a current dividend yield of 25%.

3. Industry Overview

A Booming Sector

Often out of public sight, container shipping is the heart of the global supply chain. Only an exceptional incident like the Evergreen ship blocking completely the Suez canal brought it into the spotlight.

Bordering countries might trade by train and trucks, and light freight and mail go by planes, but almost everything else is shipped by sea. And if the pandemic showed us anything, is how interconnected the world has become. A coal shortage in China can stop production at a car factory in Detroit due to a $1 electronic component being out of stock.

Containerized shipping has made sea transport more efficient. Previously, ships would be loaded and unloaded manually by dockers, a lengthy and expensive process. Having all shipments first fit into a standardized container allowed all harbors in the world to have a standardized set of cranes, trucks, and rails to safely and quickly load and unload freight ships. You can learn more about how radical a change the standardized container was to the world trade system here.

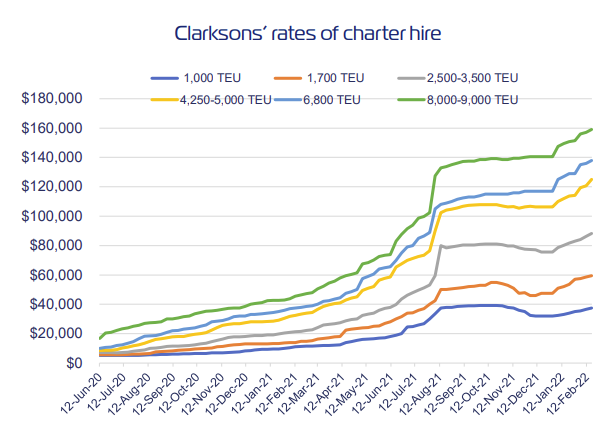

In this industry, these containers are referred to as TEU (Twenty-foot Equivalent Unit). As a result, freight ships are classified according to how many TEUs they can carry. In the last 2 years, the rates to charter these ships have gone through the roof, for all ship sizes.

Understanding the Shipping Business Cycle

Understanding the shipping industry starts with understanding the cyclical nature of that industry. The cycle goes as follows:

- Low charter rate and low margin. No new ships are built and the oldest ships are sent to the scrapyard.

- If it goes on long enough, this first phase leads to declining ship numbers and a crash in shipping companies’ stock prices. Weaker companies may close or be acquired by stronger ones.

- Reduced ship inventory leads to a shortage in capacity and rising charter rates. Companies with damaged balance sheets or serious debt or bankruptcy problems are not able to order new ships. Banks are also reluctant to loan to a sector “in crisis”.

- The persistent short ship inventory leads to an acute shortage of freight capacity. Freight rates go up quickly and profitability increases dramatically. More ships are being ordered.

- Arrival of new ships reduces freight rate. The freight market is now vulnerable to a recession that would bring overcapacity. Possible return to stage 1.

From this cycle analysis, we are somewhere between stages 3 and 4, but several years can pass between stages 4 and 5. This is due to the fact that building a ship is a massive endeavor and it takes several years from the ordering to the delivery of the new ship.

What makes the cycle we are in special is the extended duration of the previous stage 1. This chart from FreightWave says it all. Rates were last at an okay level in 2013. They then went on a decade-long depression, with rates essentially equal to the cost of shipping or below. For a long time, freight companies made little or no profit. Then Covid hit and rates went wild.

Source: FreightWave

A 2017 report indicated that shipyard capacity had declined by a tremendous 62%. 10 years without new ship orders led to the permanent closure of most of the world’s shipbuilding capacity. These closed shipyards cannot be re-opened easily, as the physical infrastructure is simply not there anymore, nor is the skilled workforce and know-how.

This also led to the global aging of shipping fleets. That left the world completely unprepared for the 2020 surge in demand for physical goods and a broken supply chain. Shipping companies want to order new ships but cannot find shipyards able to build what they need.

This means that the arrival of stage 5 of the cycle, where many new ships are delivered and the freight rate crash back down, will be significantly delayed. This time, it might take as long as 4-6 years to see a significant increase in capacity.

The aging of the existing fleet is also going to help. Many ships have been dragged on simply because the companies owning them could not afford to replace them. These ships are more costly to maintain and operate and more accident-prone. In the next 5 years, many of them will be sold for scrap metal or put aside for 1 to 2 years for upgrades, partially compensating for the arrival of brand new replacements.

Persistent Higher Demand for Shipping

Increased Demand

The pandemic has shifted a lot of consumption from entertainment to physical goods. This initiated the surge in freight rates, as we collectively bought more stuff, clogging the global supply chain. This effect might slowly fade away with the pandemic cooling off, but it is also possible that some durable shifts in consumption patterns are here to stay. Fewer restaurants and less travel, more online shopping.

Another effect of the pandemic was that every company on Earth learned how fragile their supply chain actually was. We spent the last 3 decades developing a sophisticated just-in-time supply chain that brought inventories as low as possible. With the now years-long shortage in semiconductors, raw materials, and components, industries worldwide are rebuilding inventories in a rush.

Just-in-time is being replaced by just-in-case, and this trend is not going away. This will lead to consistent higher demand for shipping for a few years until the inventories are rebuilt.

Clogged Harbors

Shipyards are not the only logistical infrastructure that has suffered a long period of under-investment. Ports have been also not properly sized to the growing trade volume. As a result, the 2020 surge led to a line of ships waiting at sea for a spot to unload their cargo. It is hard to overstate how unprecedented this phenomenon is. This means a lot of ships are not carrying cargo but just sitting there waiting, reducing the capacity available even more.

This problem is far from being resolved, with the new record number for ships waiting reached in January 2022. This shows this is not just an effect of the Christmas season but a durable trend. We will see later how this should benefit ZIM specifically.

International Disorder

The Ukraine invasion is an additional shock to the shipping system. Unexpected production interruption, re-routing of trade lanes, interruption of Russian export of raw materials, and the general chaos of the war have created more demand for cargo in general and longer trade routes.

Altogether, these trends are creating a durable increase in shipping demand. As we all experienced during the pandemic, shortages tend to breed more shortages as panic buying and hoarding increase the supply shortages. Carmakers, furniture shops, and supermarkets are as sensitive to this as toilet paper hoarding crowds.

4. ZIM profile

Posed to Rip the Shipping Boom

ZIM is a global company active in sea-borne freight, and a small actor in its industry (1.5% of total volume). It is specialized in smaller and quicker ships. In addition to operating ships, the company is also providing SaaS solutions to its clients for shipping and international logistics. The company operates an asset-light business model, “renting” ships instead of owning them. This gives its more flexibility to unstable market conditions.

A Globalized Business

ZIM is based in Israel but operates as a truly multinational business. Its trade exposure by volume carried roughly reflects the world trade itself. The largest routes are on the Transpacific (Asia to America) and the second-largest in intra-Asian trade.

Source: Investor Relations | ZIM

The company is operating a fleet of smaller ships than its larger competitors, with its larger ships at 12,000 TEUs. It is operating since 1947 and now operates 98 vessels. In 2020, the company chartered 98.9% of its capacity, compared to 56% of the fleet for its competitors (that was before most of the shortage in freight hit, today the industry’s numbers are much better).

The very large majority of ZIM freight is so-called dry freight, with a little bit of high-margin specialized cargo like especially large cargo or those that need refrigeration. The customer base is very large (30,080 in 2020) with the top 50 customers representing a third of total revenue.

Source: Investor Relations | ZIM

Besides their freight activity, ZIM also provides a complete suite of software for sea-borne freight, both for internal use and as a service for the clients. This includes tracking cargo, online booking platform, CRM, cybersecurity solutions, or cross-border shipment assistance.

Source: Investor Relations | ZIM

Some of the largest freight ships can carry up to twice as much as ZIM’s ships. Larger ships can be theoretically more profitable, as they carry more at once and spread fixed costs on a large base of orders. However, their absolutely massive size is a limitation as well. Only a few harbors in the world have a design able to cater to them, limiting possible routes. If the receiving harbor is clogged by already 100 other ships waiting for weeks, there is no possibility to re-route to a secondary destination with a shorter waiting time.

Smaller ships are also quicker and have short turnaround times which come at a premium when customers are worried about growing delays. Interestingly, when air freight got slowed down in the pandemic, ZIM quick ships managed to take away business from air freighters, something a less flexible or slower fleet of giant boats could not do.

ZIM has been recognized for its flexibility and efficiency by some of the largest actors in the sector. Notably, ZIM signed an agreement with Alibaba to get buyers on Alibaba.com (the B2B international site of Alibaba) to directly purchase freight from ZIM on the Alibaba platform.

Forward-Looking Management & the Asset-Light Model

For every capital-intensive industry with mobile assets, like airline or sea freight, comes the question of asset ownership strategy. Many companies prefer to outright own the ships or planes themselves. This gives them more control over how the equipment is operated and maintained and maximizes profits during booms. But this also means that during a crisis, these assets can become liabilities if they are not in demand.

The alternative option is to “rent” the ships. This is the model that ZIM follows. By not owning the ships, ZIM is able to quickly modify the size and composition of its operating fleet according to market conditions.

Recently this has paid off in multiple ways. In 2020, the company let go of 20 ships that were idle in the initial stage of the pandemic, before the surge in demand for shipping. They were then able to quickly increase the fleet size above pre-pandemic levels to exploit the massive surge of demand and charter prices.

ZIM is booking around 60% of its ships for 1 year, and the rest for 1-5 years. This seems like a reasonable plan for me. If demand crashes, they can quickly not renew the bulk of the fleet without a loss or having to cover the costs of the idle ships. But the 40% long-term ships allow it to also keep under control a rise in the price for “renting” ships if demand stays elevated.

In a business as unpredictable and cyclical as shipping, a business model flattening the ups and downs seems a plus to me. Maybe ZIM will not benefit as much as others from a persistent boom in shipping, but their downside is a lot more limited as well.

Another advantage of the asset-light model is flexibility not in the number but in the type of ships. With demand staying elevated longer and higher than any other cycle, ZIM is modifying its fleet composition. This also comes at a time when oil prices have gone up significantly and supplies of the bunker oil used by ships are not necessarily easy to find. This was true before the beginning of the Ukraine war, which increased the pressure on oil supplies.

The solution for persistent higher demand of freight volume and fuel costs rising was to charter, since 2021, 10 ships of 15,000 TEUs capacity (the largest ever operated by ZIM) and 13 ships of 7,000 TEUs capacity. Each of these ships is LNG-fueled. By using them on the Asia-USA East Coast route, ZIM will be able to utilize the much cheaper American LNG costs to save money.

This will also make ZIM one of the least carbon-intensive actors in the sector. With climate change a growing concern, this will provide ZIM with 2 benefits. They will have a competitive advantage if carbon taxes get higher and they will offer an ESG-friendly investment profile, a rarity in the shipping industry, which is generally powered by the dirtiest fuel, known as bunker fuel.

These ships will be delivered starting next year. If demand stays steady or reduces they can partially replace the existing “rented” fleet. If demand stays explosive they then just add up to the total fleet. This is the beauty of this model in times of instability. ZIM can relatively effortlessly change its fuel requirement and size or number of its ships to adapt to market conditions. Considering that all the last 3 years’ decisions have been on spot in anticipating problems, we can feel reasonably confident in management skills in using this flexibility well.

5. Financials

Armored Balance Sheet and High Dividends

ZIM has significantly reduced recession risk thanks to prudent balance sheet management and debt reduction. Free cash flow in 2021 was equal to half of the current market cap. Thanks to the asset-light model, the company should be able to adapt to unstable market conditions. The dividend policy is very friendly to shareholders, with a current dividend yield of 25%.

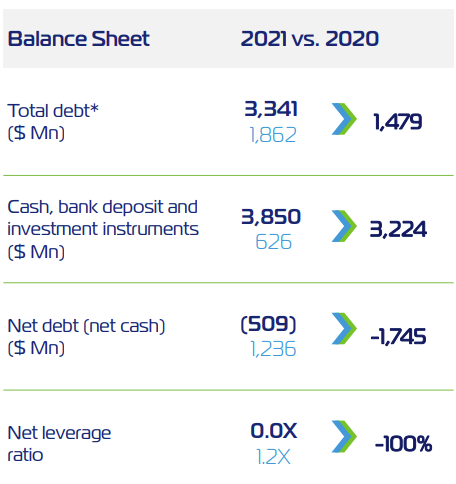

A Reinforced Balance Sheet

I have lately tried to focus reports on the “big idea” than the nitty-gritty of financial data. This stems from the idea that if an investment is a good one, it should be obvious and not rely on complex financial models to reveal it. With a company operating in an industry so exposed to market cycles and potential outside shock, we have to talk more about debt and cash.

At current earnings, ZIM is valued very cheaply (P/E of 1.9). As I said, these earnings are somewhat exceptional, so this is not enough to assume the company offers enough margin of safety. Where ZIM shine is in the very cautious management of the balance sheet. A lot of 2021’s outsized profits have been used to reinforce the balance sheet.

First, total debt has been more than halved, from $3.3B to $1.5B.

With a parallel rise in cash on hands, this has brought net debt from a good -$500M to a great -$1.7B.

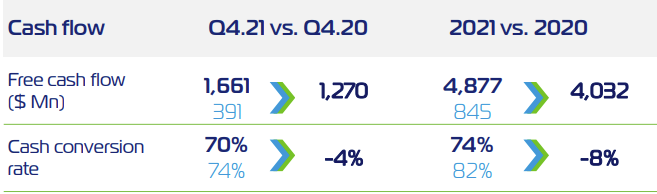

With such a strong balance sheet and bankruptcy concerns firmly put aside, let’s look at cash flows. Free cash flow has gone up in 2021, standing at $4.8B

When seeing these numbers, we can keep in mind that the current market capitalization is $9.8B. If 2022 is as profitable as 2021 was, the free cash flow should represent as much as half of the company’s current valuation.

Dividends and Shareholder Returns

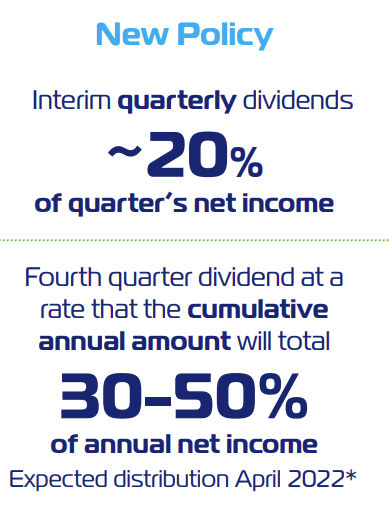

Of course, a lot of cash flow is irrelevant if the cash never makes its way into the shareholders’ pockets. A friendly profit distribution policy is a must. ZIM already had a solid dividend history, with $21.5 / share distributed since the January 2021 IPO (roughly 1/4 of the current share price)

The new policy aims at guaranteeing a strong quarterly dividend, equal to 20% of the quarterly net income. This comes from a special dividend in the fourth quarter so that the yearly distribution reaches 30-50% of annual net income.

For reference, 2021 annual net income was $4.6B, so the total distribution under the new policy would have reached $1.4B to $2.3B. Again, to compare to the $9.8B market cap.

The fact that the dividend distribution is quarterly is also great, as this ensures that money is transferred to shareholders continuously, instead of being hoarded and possibly never actually distributed.

Valuation

Considering how full of surprises 2022 seems to be, I feel a precise valuation tool, like discounted cash flow, would likely give me a “precisely wrong” estimate. So many factors can affect the demand and pricing for shipping:

- A slowdown in the European and/or Chinese economy

- A steep rise in inflation

- Supply shock from commodity shortages

- Change in rates policy by central banks

- Sanctions against China in response to support for Russia

- A peace agreement signed in Ukraine

- An escalation of the Ukrainian conflict

- New conflict in another region (Iran, Turkey? Or God forbid, the Baltics or Taiwan).

So my assumption for a base case scenario will be the persistence of 2021 trends. High shipping rate, but not growing. Constant high demand but not rising either. In these conditions, dividends alone would bring roughly a 25% yearly return. This would also leave $2B+ in free cash flow to completely extinguished the debt and some spare cash leftover.

One more year like that means the company’s free cash flow will cover half of the current market cap. So from 2023, even a decline in free cash flow could provide a decent return through the generous dividend policy.

A scenario where profits go up is not unlikely, but I expect that higher shipping rates might be compensated by higher shipping costs in 2022. Cost increases from fuel, salaries, and the cost of “renting” ships are likely, especially considering that the new LNG-powered ships will only arrive in 2023.

All in all, I think ZIM could deliver anywhere between 10%-25 % yearly returns from the dividends alone in the next few years. A speculative move on the stock price itself could add some extra profit or losses, but this is almost impossible to predict.

The bear case would lie in a radical slowdown in the world economy. Higher energy prices, various commodity shortages, and a deflating tech and real estate bubble in China could derail demand and shipping rates.

A catastrophic bear case would be exploding tensions with China, following open support of Putin’s Russia or an attack on Taiwan. Frankly, after the last few weeks, I don’t feel I can completely rule this out. But I also feel that in that scenario, there would be very few places in the market to hide anyway.

6. Conclusion

ZIM is almost the opposite of Rakuten, the company we covered in the last report. Rakuten is centered in one country, with very diversified activities and expanding in a capital-intensive segment. ZIM is fully globalized geographically, razor-sharp focused on sea-borne freight and operating a capital-light business model.

From an industry perspective, ZIM seems set for a few great years. Shortages of container ships, limited shipyard capacity, and restricted harbor unloading facilities have created an environment conducive to shipping rates higher for an extended period. This is not dissimilar to how energy companies are now seeing record profits thanks to years of insufficient CAPEX spending.

ZIM seems uniquely positioned to profit from this situation, as its asset-light structure allowed it to expand capacity much quicker than its competitors waiting for new ships to be built and delivered. The smaller size of the ships in its fleet permits quicker and more flexible deliveries at a time when clients are frustrated by a clogged supply chain.

At the current valuation, the future returns from an investment in ZIM will depend on the state of the world economy.

If the current supply chain issues, energy and commodity prices, and war in Europe trigger a worldwide recession, demand for shipping will decline. In that case, ZIM’s profit margin might decline dramatically. This scenario would hurt such investment, even if the strong balance sheet and flexible fleet composition would avoid a disaster.

If the current trend lasts for a few 2 or 3 more years, ZIM will be a cash machine. 2022 free cash flow could be used for paying off all the debt and still give a 25% dividend yield. 2023 would see even more free cash flow available for a rising dividend. I could imagine in that case the entire current price given back in dividends by 2024, not counting on a stock price rise.

If everything goes well, thanks to the asset-light business model, ZIM will avoid the temptation to overpay for more ships at the end of the business cycle, favoring shareholders’ returns instead. In an industry known to miscalculate the business cycle and waste the money of bountiful years on “vanity growth”, this makes ZIM special.

The dividends are massive, but the cyclicality of the industry implies some risks to the capital invested. So from a portfolio management perspective, ZIM should be in my opinion a relatively small position.

In any case, this is not a buy-and-hold type of investment. At some point, either the economy will cool down or the shipyards will have built enough new ships to depress rates again. It seems this point is at least 3 years in the future, but this is not an investment where we want to overstay our welcome. So a cautious look at the number of ships available and the health of global trade will be useful to know when to take the chips off the table.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in ZIM or plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation from, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.