November 1st, 2021

Quick Stock Overview

Ticker: DPSGY

Source: www.tikr.com

Key Data

- Sector: Industrials

- Sales ($M): 85,594

- Industry: Freight and Logistics

- Net Cash per share: $4.93

- Market Capitalization ($M): 76,634

- Equity per share: $15.03

- Price to sales: 0.9

- P/E: 14.5

- Price to Free Cash Flow: 10

- ROIC: 32.7%

Investment Thesis

Boring Means Safe in Turmoil

Investors are by nature thinkers. Pessimists (bears) are thinking about what could go wrong. Optimists (bulls) what could go write. But both agree that some businesses are simply boring.

Some businesses are naturally difficult to hype up. Most firms are altogether implausible to grow 50% year to year for decades and become the next Apple. And they are equally unlikely to go bust. So, it is hard to garner much interest from the investing crowd for such uneventful stocks.

However, boring does not mean unprofitable, or a poor investment. It is just uninteresting, dull, and stable. The thing is, boring can be profitable.

Especially if it is cheap!

Today’s report is about such a company, something as mundane and ordinary as postal services. And more precisely, the German postal service: Deutsche Post Group.

The company has a long history, going back to 1876 or even 1490, depending on how you want to see it. This is rather a strong point, as a structure that lasted centuries is likely to survive a few more centuries.

I will provide greater detail later on about the different segments of the companies, but you already know the general idea well. It’s a postal service. It takes items or paper from point A to point B and charges a fee for it.

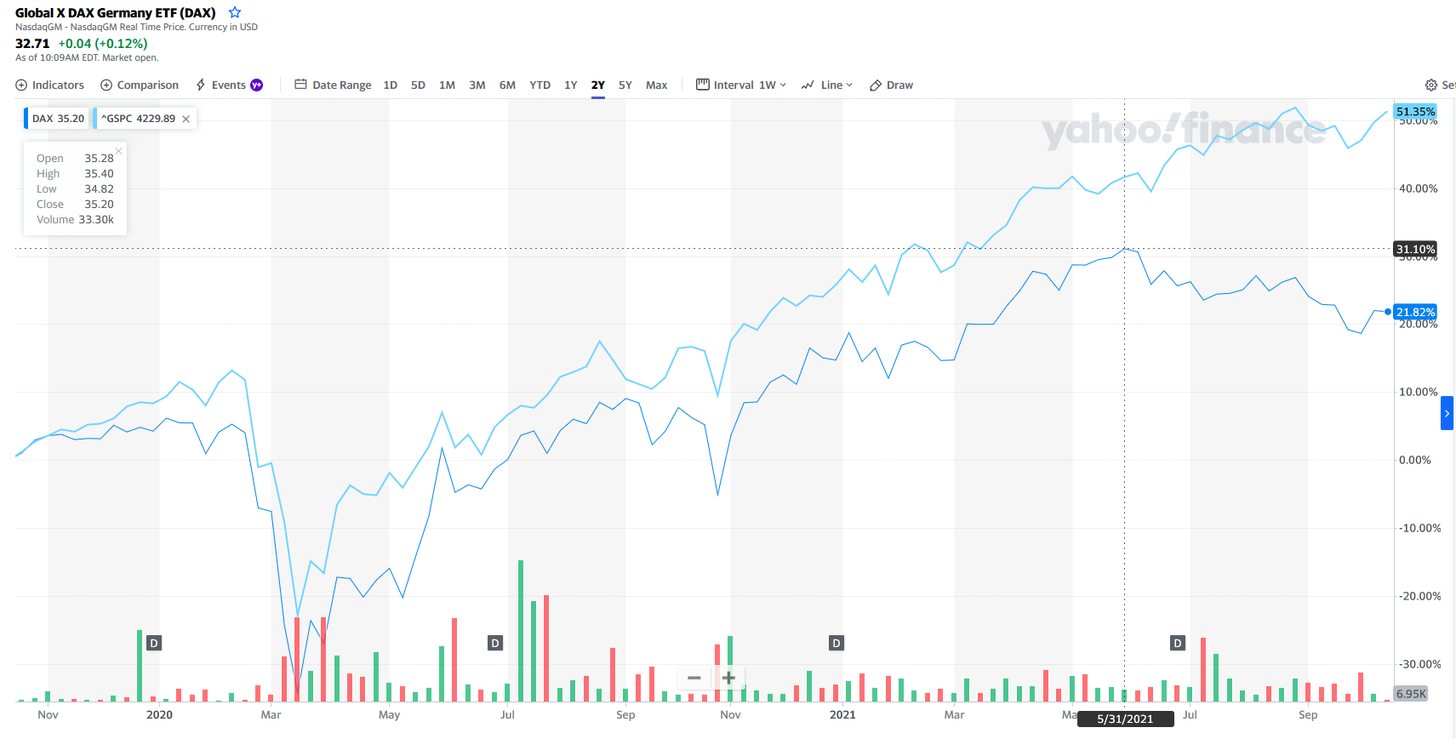

Recently, Germany has not really been at the top of its game. The Eurozone is facing very slow growth/a recession. It is also in the middle of an energy crisis to the point of risking massive blackouts this winter, with the Nord Stream 2 pipeline still in limbo.

Germany is also facing large political uncertainty with the end of the Merkel era, compounding the unknown about economic and energy policy.

So overall, investors are not favoring Germany at the moment. As you can see, while the US markets are still exuberant, the main German index, the DAX, is quite down since July.

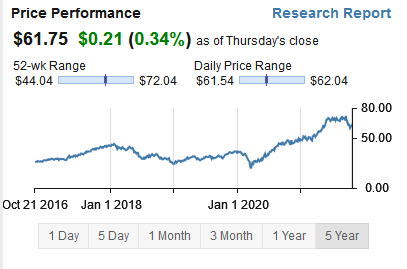

Despite that lack of enthusiasm for Germany, Deutsche Post stock price has handsomely rewarded its shareholders in 2021. The stock was rising strongly, before stumbling at the end of summer with the rest of the DAX.

As we will see at the end of the report, I do not think that, at the current price, the company is overvalued. Rather, simply that it was ridiculously undervalued just before and after the covid crash. I am just sorry for not having thought of it then!

But ultimately, Deutsche Post is the type of company to invest in for the long run, so it is fine to pick it once the storm clouds of the pandemic are clearing.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: A Simple and Well-Run Business

From National Dinosaur to International Leader

A postal service is a remarkably simple business. It is so simple that it more or less falls into everybody’s circle of competence. Everybody in the world knows how their post-service works.

However, in many (most?) countries, this is not an endorsement of quality. I remember a comic strip describing how the author imagined Hell: a noisy, crowded, and endless waiting line in a post office.

For others, it means a company on the permanent edge of bankruptcy, always looking for more support from taxpayers, all while delivering letters and packages haphazardly. Adjectives like inefficient, unreliable, costly, archaic, lazy, abound to describe most postal services in the world.

Deutsche Post itself was suffering from this dreadful reputation of postal services. I find it very interesting and funny that the company itself acknowledges it in its “The company at a glance” communication. How often does corporate communication describe the company as formerly “government-controlled, deficit-ridden”? Germans’ reputation for brutal honesty seems at play here:

Truly, the description seems adequate. The Deutsche Post had a terrible reputation and was losing tons of money. But privatization and reforms changed the company in the 2000s. And it paid off, even if slowly, as can be expected for such a large institution.

This is a company more akin to a cruise ship than a speedboat. It will take a while to change its course, but once done, it is likely to stay steady. Since 2013-2014, all measures of profitability are pointing upward for the last 10 years, with a net inflection point after 2018.

A big part of this transformation was turning the government-run Deutsche Bundespost into a modern international logistics company. The company did this by raising private capital and changing management. This led to the key moment that was the acquisition in 2002 of DHL.

While Deutsche Post was formally gaining DHL, DHL turned into the dominant actor of the fusion. What had strategy and practices made DHL a global leader in logistics ultimately took over throughout the rest of the group, bringing its competitive, private-sector way of management to the bureaucratic postal services.

Notably, DHL was bundled with the express and logistics part of Deutsche Post, now one of the most profitable parts of the group.

One other milestone was that Deutsche Post shares have been listed on the public markets since 2005. The same year, Deutsche Post was also acquiring the British Exel group (111,000 employees).

After that, the company would withdraw from banking activities, an extension that many postal companies tried at the time, generally unsuccessfully. Instead, it refocused purely on logistics. It would also expand its logistic network abroad, notably with new planes and giant distribution centers in Asia. More recently, the company has used its experience in modernizing and turning profitable postal service by acquiring UK Mail in 2015 and bringing up to speed the rest of the Deutsche Post divisions.

So, as you can see, what seemed on the surface boring, the “German Post”, is a leading and global logistical company. But you need to go beyond the first glance to realize it.

A Diversified and Global Business

The company business is divided into 5 segments.

The Post & Parcel Germany is pretty self-explanatory. This is the purely domestic part of Deutsche Post’s activity. It transfers 49 million letters and 5.9 million parcels every day. The sheer size of just this department is the kind you usually hear only from companies like Amazon. The company controls most of the German market. Especially the largest and most profitable market, advertising:

Deutsche PostCompetitionMarket volumeMail63%37%EUR 4.3BAdvertising93%7%EUR 23.8B

The competition exists, and it is good, so it keeps Deutsche Post from turning back into an inefficient bureaucracy. Still, the company is the dominant player in Germany and has a stable market share. This is akin to all the advantages of a monopoly, without the inefficiencies that come with it.

The express division is what you probably know better as DHL and never associated with the Deutsche Post (I sure did not before doing the research for this report). This is the express, worldwide delivery of parcels that absolutely need to arrive as quickly as possible, and in perfect shape, at their destination.

These are mostly just documents and small boxes. Most customers are B2B, and the service is relatively expensive compared to normal posts. The company operates a mix of its own airplane fleet and also rents empty space in regular airlines’ planes, accessing this way a “virtual fleet”.

The division recently acquired cheap planes from desperate-for-cash airlines companies and is converting them into freighters. Excellent use of a once-in-a-lifetime opportunity to save capex!

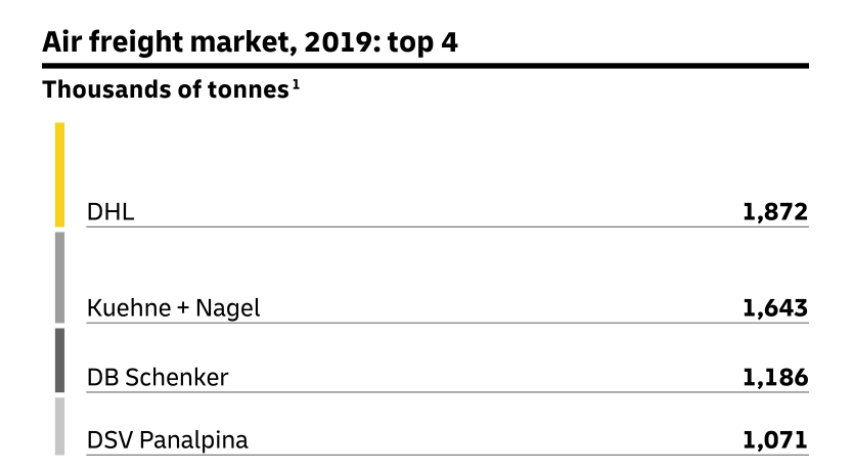

The freight division includes air, land, and sea transport. It is dedicated to the larger, bulkier cargo. I was pretty surprised to discover that DHL is not only the leader in Air Freight but also the top two for Ocean Freight. Again, not something I expected when I looked into the Deutsche Post.

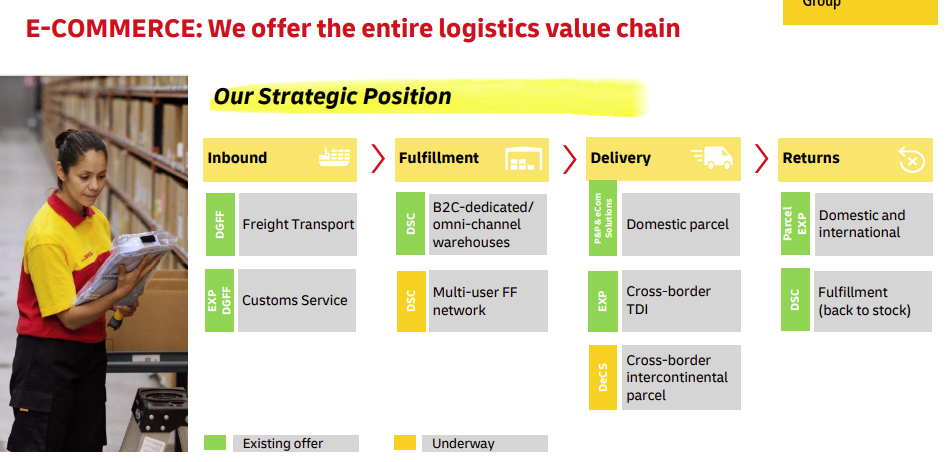

Supply chain is the division sub-renting or managing warehouses for other companies. In that activity, Deutsche Post/DHL can use its scale and experience to deliver best-in-class supply chain management. Including dedicated software, warehouse designers, semi-automatic trailers, custom-made devices, etc.…

This level of quality would be very difficult and expensive to replicate for smaller companies, at worst impossible. Especially for very extensive automation and complex robotic tools.

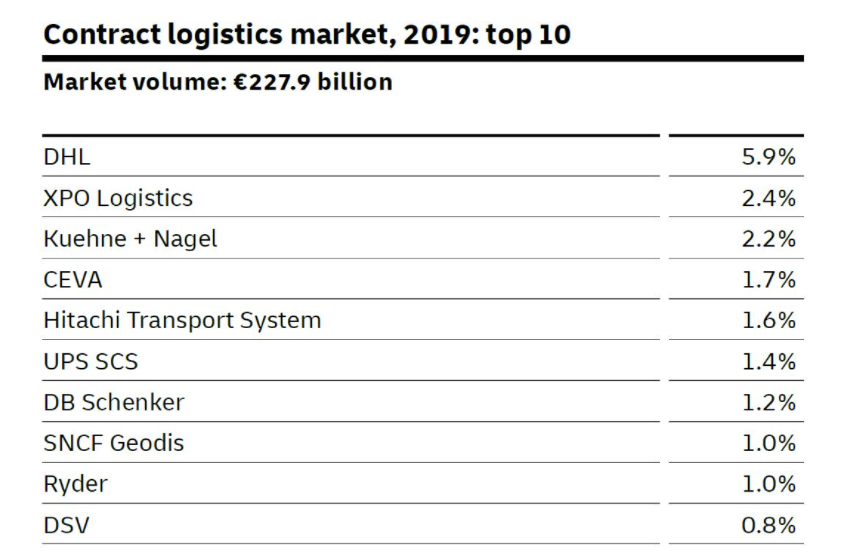

Here too, the company is simply the world leader, with as large a market share as the next top 2, 3, and 4 combined. This is for a market worth no less than $228 BILLION. It is also a constantly growing market, with more and more companies needing top-notch logistics to keep up with Amazon and Walmart.

The market is, however, VERY fragmented, and this should leave plenty of growth and consolidation potential. It would not surprise me to see Deutsche Post controlling 10% + of this market in 10 years, through a mix of acquisitions and organic growth.

Source: www.dpdhl.com/

E-commerce and international trade drives both directly and indirectly, much of the company’s activities. Like companies operating more internationally and needing express delivery and freight, or assistance for their own warehouse and supply chain.

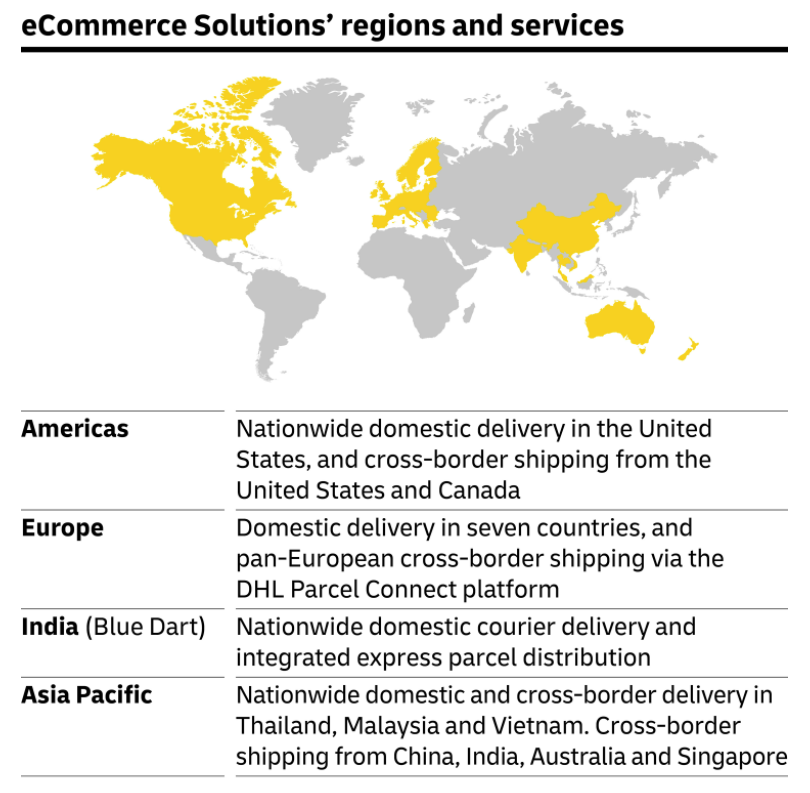

The dedicated e-commerce segment of Deutsche Post employs 37,000 people and delivers 1.1 billion parcels per year. Or 29,730 parcels / employee / year. Or 120+ parcels per employee / day. This is some incredible volume and efficiency, considering one parcel will be handled by many people on its journey.

They mostly focused on the so-called last-mile deliveries for 7 European countries, and international cross-border delivery in other regions.

Deutsche Post operations are focused potential needs on the heart of world economic activity: North America, Europe, Asia, and Oceania. Its e-commerce division covers almost all the potential needs for e-commerce distribution. It levels the field for every company forced to match the offer like same-day delivery from Amazon, without forcing them to build themselves hundreds of warehouses on all continents.

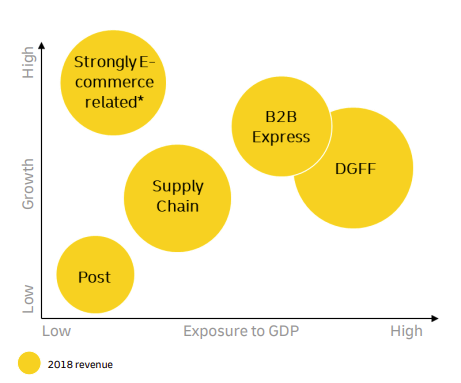

Overview: The several business lines allow for diversifying risk. Some activities are strongly linked to GPD fluctuations, while others are likely to be more robust. In addition, each is growing at different rates.

Freight and Express highly depend on economic conditions and have quite a good growth profile. E-commerce is growing no matter what. And traditional Post services are slow gorwing, but a solid cash cow even during recessions.

Chapter 2: Embracing the Future

The 2025 Strategy

I am generally skeptical when large corporations come with a well-crafted narrative with a catchy name for their strategy. It is often hard to find what is purely PR and what is going to impact the company’s future. Or even understand it all sometimes.

It was a bit the case with Deutsche Post’s 2025 strategy. Things like the logo below look nice, and give work to the communication department designers, but contain very little useful information.

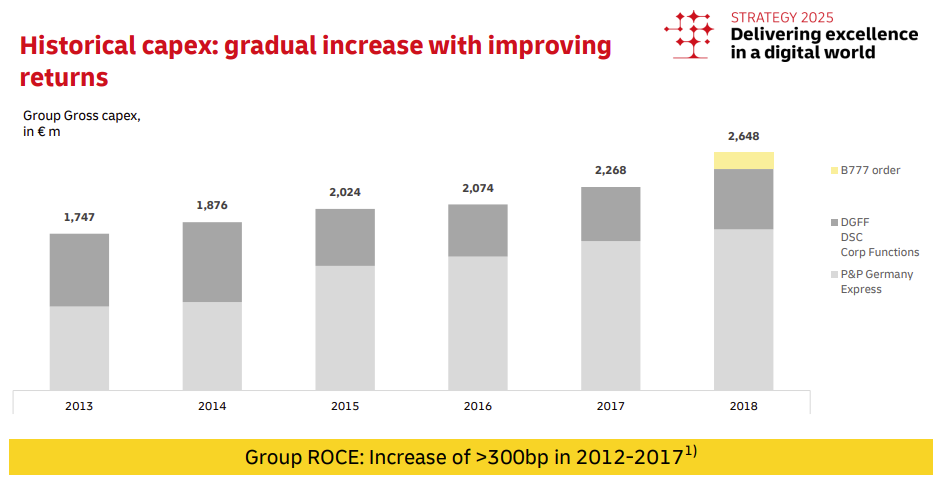

Beyond the corporate-speak, we can find a few interesting pieces of information in that strategy declaration. First, the company will invest EUR 2B in further digitalization. The EBIT is “expected to grow to at least EUR 5.3B” and the company to “generate a total EUR 5B of free cash flow by 2025”.

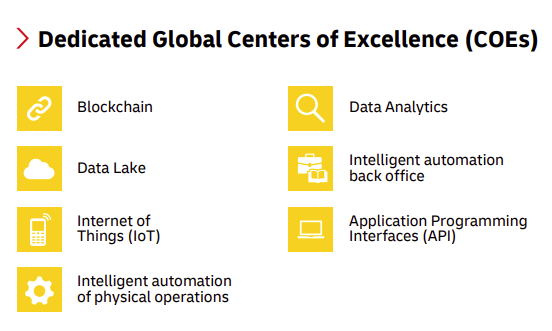

The second part is to create “Centers of Excellence”. These are essentially teams that will be in charge of integrating new technologies into the company.

The first part, the investment strategy, seems solid and will allow for more efficiency and maintain growth. The second part is a little harder to judge.

Throwing around catchphrases like IoT and blockchain does not really mean anything in terms of operational results. However, I believe things like blockchain could create a more accessible and persistent tracking system for packages. And warehouses are likely to become almost fully robotic in the future, with each captor talking to a network and workers using fully wearable digital tools.

It is nice to see the company embracing change instead of resisting it. But I am not convinced it will impact the company’s results for the next 5 years. It might, however, have some on the stock price if the re-branding of Deutsche Post as a technology company catches on with investors.

A Unique Strategic Position

More importantly, I think the position of Deutsche Post in the global trade network is worth a premium in itself. We saw the last 2 years the complexity of global supply chains, and we might have again problems with empty shelves this Christmas. “Just in time” is suddenly not that great, and reliable deliveries will command a premium.

Deutsche Post has tremendous advantages to ride the ongoing storm in logistics compared to its competition:

- Dominant position in the largest European economies.

- World leader in airfreight AND ocean freight.

- World leader in contract logistics.

- Strong position on e-commerce deliveries.

Altogether, this provides the company with a wealth of data, scale, and network effects that no one except maybe Amazon and Alibaba can rival.

We are likely to keep seeing trouble in supply chains, created by energy crises, inflation, shortages, trade wars, re-shoring industries, and the China-USA tensions. This will be a major headache for most logistics companies. For the like of Deutsche Post, this will instead be the occasion to shine and steal contracts from its competitors.

If you are an industrial company or a retailer expecting troubles, you want your supply chain to work well, and you need simply the best and largest provider to help you achieve it. Each time you read about clogged ports, missing parts, and exploding shipping costs in the next months and years, you can bet Deutsche Post is going to turn it into an opportunity.

The Technologies to Come

Postal services and delivery is a very labor-intensive, low-tech process. This is why Deutsche Post employs almost 570,000 people, making it one of the largest private employers on the planet (apparently the 5th largest).

But this is about to change. There is already existing and deployed technology to automate much of the business: automated parcel machines. They are very common in the Baltic countries, and they are likely to spread in all Europe, as well as the USA/Canada soon.

How does it work?

You receive an email/SMS telling you your parcel has arrived. You go to the automat 500m-1km from your home and go pick it up by entering the unique code in the SMS. One delivery postman can handle a lot more packages than a traditional postman.

And no more packages left on the porch, undelivered. This works well in the dense urban area, but also in the rural area where post offices are far apart. Do you want your package in the nearby town manned post office 15km away (costing fuel and time), or in the unmanned automat 2km away?

The same automats can easily be used to send parcels nearby. You enter the address, pay, leave the parcel in a compartment, and viola! No more queue and fully contact-less (especially important if Covid stays with us).

You might remember from a previous report on iRobot I talked about robotic deliveries (at the time for food and local shopping). But startups are also looking at autonomous driving and realizing that delivery is a much simpler solution that can be achieved right now.

The robot can be tiny, confined to sidewalks, with no danger from a collision with cars or passersby. This is the promise of Estonia’s Starship Technology robots.

Source: www.medium.com

In the same country, another company, Cleveron, already has a driverless prototype for an autonomous parcel delivery robot. The company started doing the parcel automation I mentioned before in 2009! You can see more about the model here, where the specs are more detailed. And this promotional video, by the way.

Anyway, the point is not to praise the progress of robotics in the Baltics. But to emphasize that the “boring” business of postal services and parcel delivery is going to twist into a tech industry. This is for now limited to test markets and small countries where it is easy to deploy, but will soon expand everywhere in Europe, the Americas, and Asia.

This will be a period of explosive growth for e-commerce, as lower prices and even better convenience of delivery will overcharge the already quickly growing sector. Only logistic companies with a specific profile will manage this turn well:

- Profit-oriented instead of bureaucratic and archaic postal services.

- Existing high level of digitalization.

- Profitable with ability and plan to spend enough capex.

- International with experience of adapting to local customs and culture.

- Critical mass (at minimum dominant in 1 major country) to cover the extra overhead and R&D.

- Already using robotics in warehouses.

- Having experience in integrating new processes and recent acquisitions into the existing operations.

Or simply put, Deutsche Post / DHL is the poster child of the logistical company that will be primed to capitalize on the postal industry transformation into autonomous robotic delivery.

We hear a lot about jobs that self-driving vehicles will destroy. But really, the first industry to see job destruction will certainly be the post and food/parcel delivery. In a decade, a human delivering pizza or parcel might join phone books and dumb phones into technological obsolescence.

These technologies are already there, on actual streets with real customers and making real income. The same cannot be said of autonomous cars…yet. Besides, regulatory agencies will be a lot less picky with slow-moving, silent, small robots on sidewalks than with 2-3 ton cars or 20-30 ton semi-trucks.

So, watch out for the next big story in IA, robotic and autonomous driving, where the “boring” companies will rule the new narrative.

Chapter 3: Not Your Ordinary Postal Service

Growth Expectations

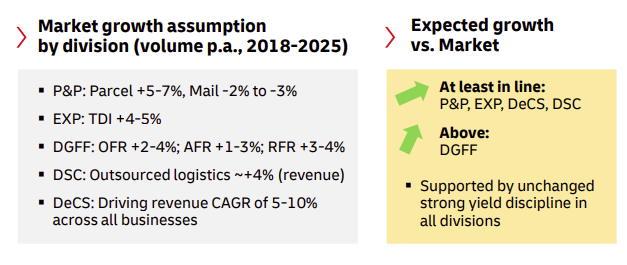

Deutsche Post’s management is expecting relatively solid growth, considering its business line. Most of the activities are expected to grow yearly by 4-5%, with e-commerce expected at 5-10%.

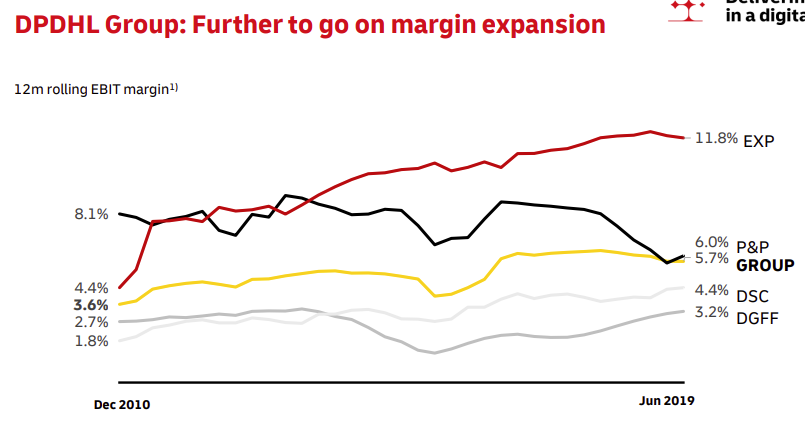

On top of that, margins have consistently improved over the last 10 years. This directly results from economies of scale and digitalization. The same is likely to still be true for the next 5 years. So, we can easily expect profits to grow from both revenue growth and margin growth.

Outstanding Results

Deutsche Post is this business completely misunderstood by most of the market. The name hid a much more global business, and I think almost no one has realized how different delivery services will be in 10 years. A few more self-driving robots around your street and this will change.

In that respect, I suspect the company is even conservative with its growth target for 2025, or maybe the real acceleration will only start then? It is possible that 2025-2030 will surprise us in a good way.

But how is business now? What if none of these lofty projections ever happen? Is the business as it is today solid?

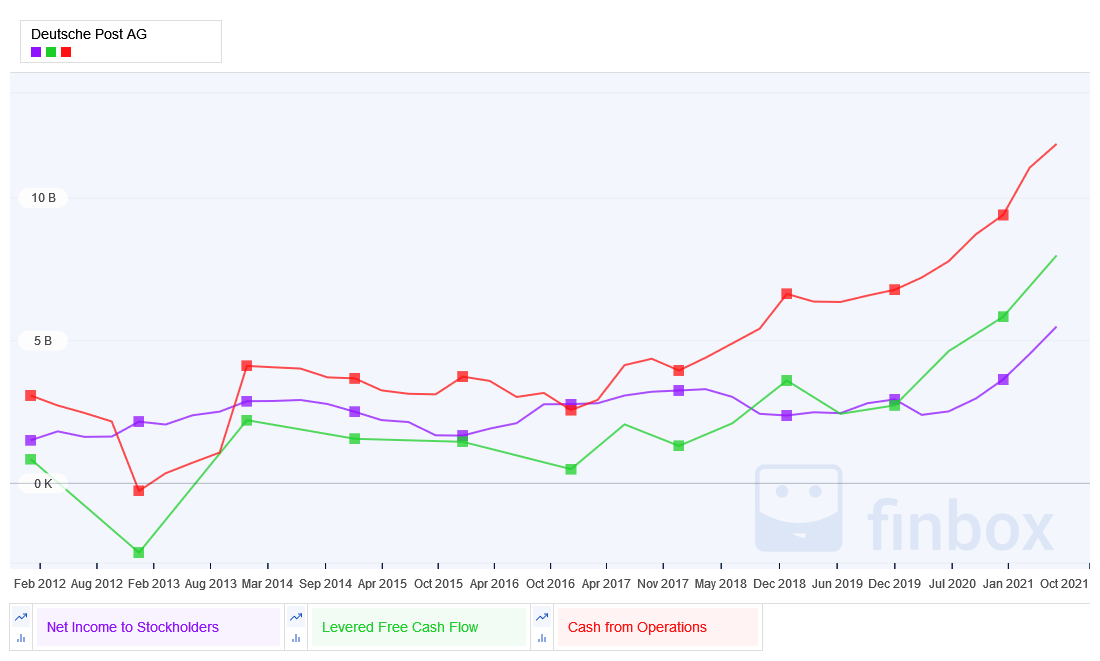

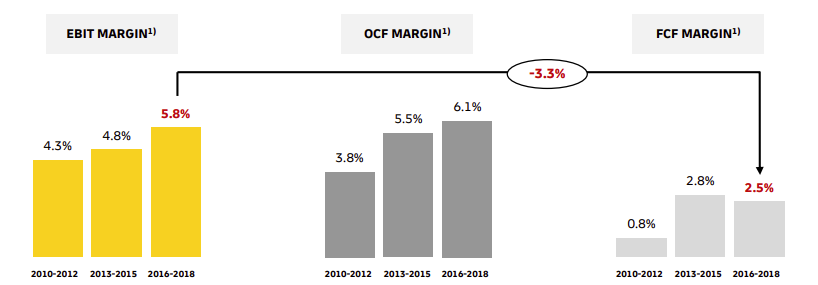

To start, the company has dramatically improved its margins, no matter what metric is used. I really like that management shows multiple margin calculations. This reduces the chance it is a mere accounting trick.

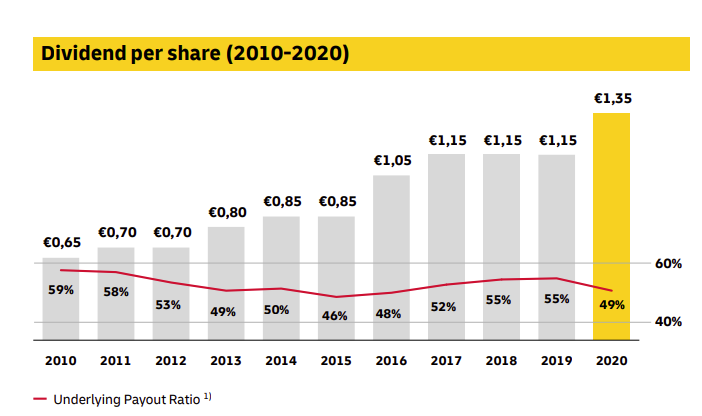

This translated into slowly but steadily growing dividends. They postponed the 2020 dividends when Covid made everything uncertain. But they finally paid it, just with a delay. Conservative approach, but not overly risk-averse either.

The payout ratio is maybe a little high to my taste, but it did not hinder a parallel growth in capex. So, it does not seem the company is giving back too much to shareholders and risking future profit.

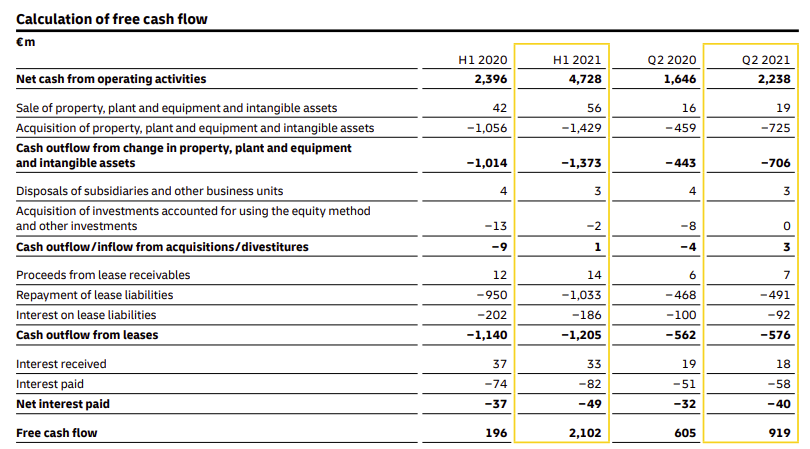

Covid was a period of a sudden drop in activity before a surge because of more online purchases and lockdowns. This means the recent revenue and profit numbers are a little chaotic. Overall, I am happy to see that even in H1 2020 free cash flow stayed positive and has since spectacularly recovered, reaching all-time highs.

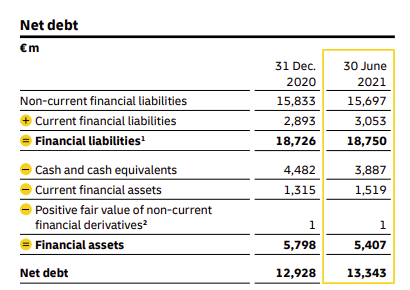

The balance sheet is not pristine, but solid enough. Debt is quite stable and well covered by income and cash flows. You can see below the current net assets and the net debt.

I must also point out that the company is really rich in assets. We are talking here about real things like valuable real estate, planes, cargo ships, warehouses, trucks, forklifts, and everything in between. A grand total of EUR 57.7B in assets.

When compared to the EUR 18.7B of total liabilities, this makes the company’s total assets worth EUR 49B. With a market cap of EUR 65B, this means the market is valuing the enterprise at only EUR 16B! Hard to believe for a company with good cash flow and steady 5%+ growth for the foreseeable future.

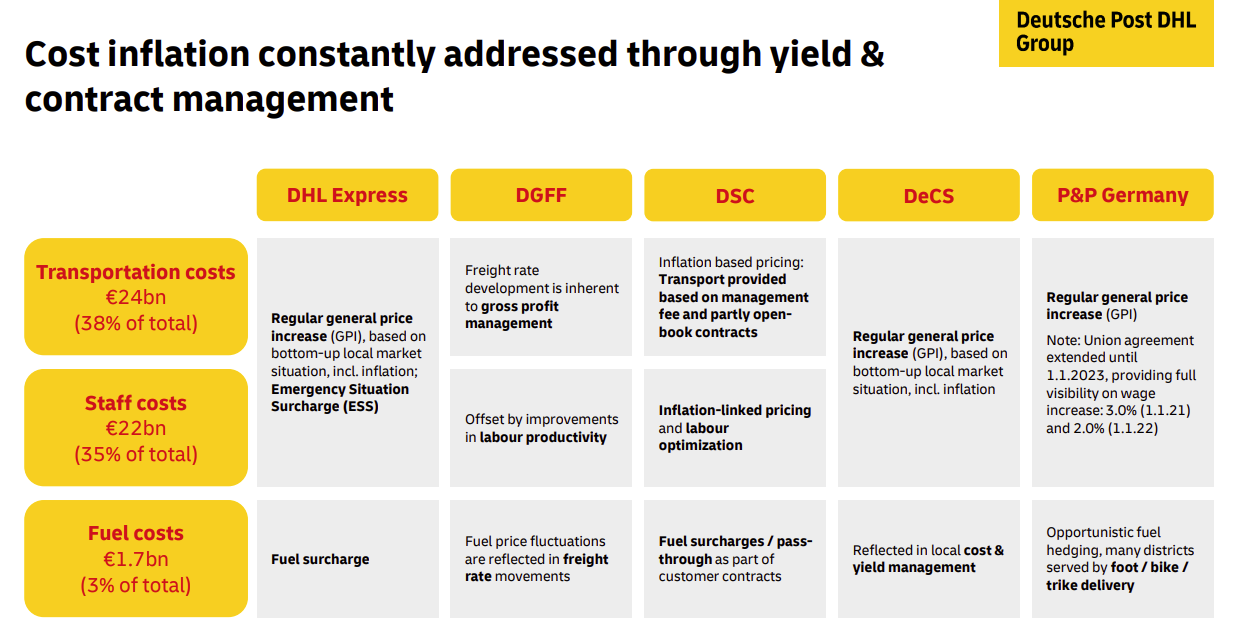

A Note on Inflation

For assets-heavy companies, inflation can be a good or a bad thing, depending how well it’s managed. On one side, already owned planes, ships, real estate and heavy equipment gain in value during inflationary period. On the other side, costs can quickly skyrocket out of control as well.

I appreciate that the long-term part of the company presentation address the issue and breakdown the costs, between fuel, staff, and transportation.

It seems that fuel is actually a rather smaller part of the group’s costs than I expected. Even with the current rise in fuel costs, this should not have a dramatic impact on the company. On top of that, most of fuel costs rise can be passed on to the customers and arbitration for local delivery on foot/bike can help capitalize on growing fuel prices.

For the rest of the activity, a lot of the services are priced with inflation-linked contracts. The problem I can see is that GPI (an equivalent to the American CPI) might not reflect fully the real inflation. But this does provide an okay protection, nevertheless.

Overall, Deutsche Post is likely to suffer a little if our inflation problems are getting worse. The combination of low exposure to fuel costs and inflation-linked pricing should shield it from most of possible damages. And less rich competitors, leasing or renting assets instead of owning them might be a lot more hurt, which will then improve Deutsche Post’s competitive position.

Chapter 4: Valuation

Deutsche Post is such a large, international, and stable company that two valuation methods seem possible.

The first is the classical Discounted Cash Flow.

The other is the equity bond yield, treating the company stock as a perpetual bond due to its safety profile.

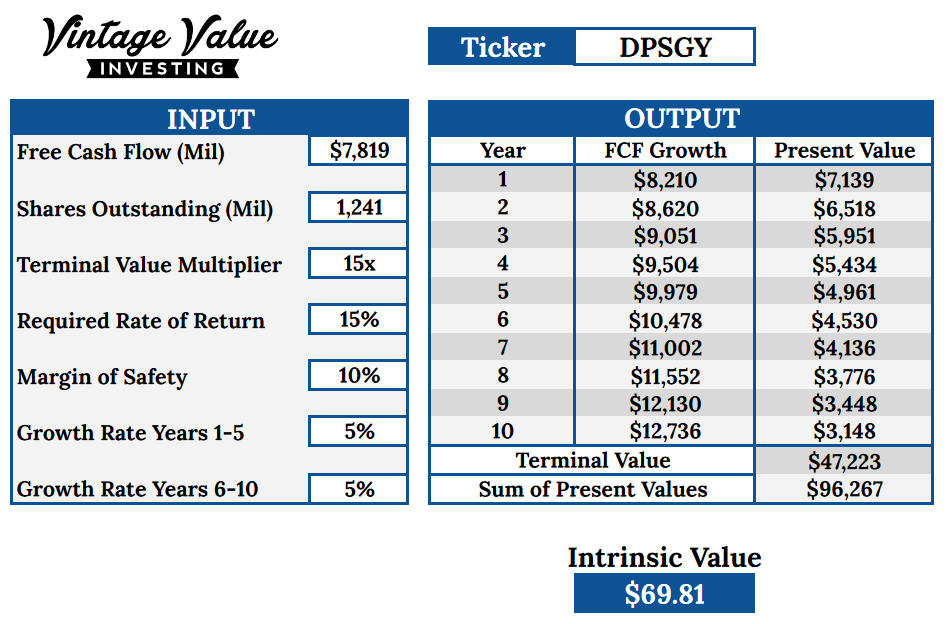

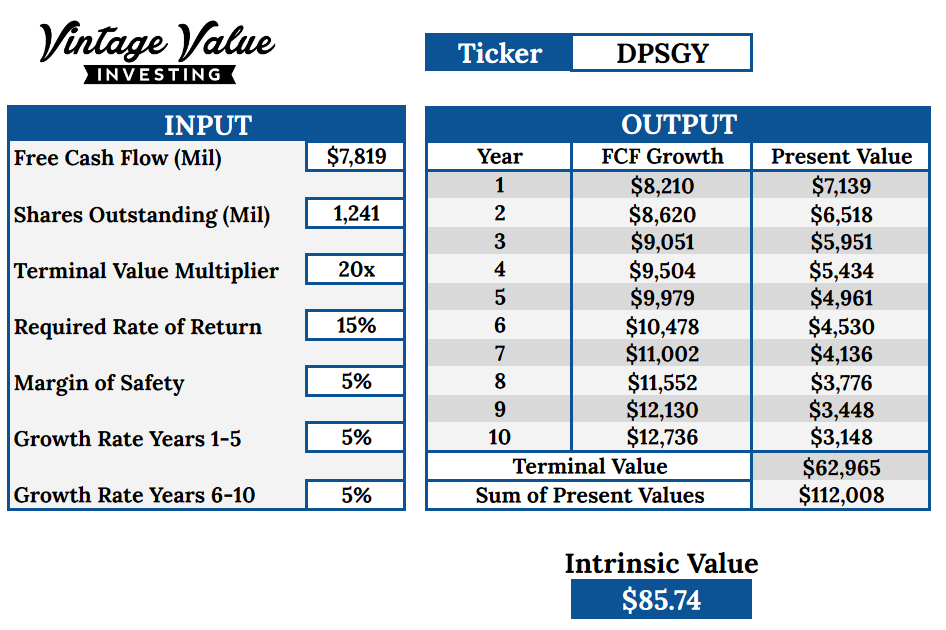

Discounted Cash Flow

Historically, Deutsche Post investors have been ready to pay quite a lot for cash flow, reflecting their confidence in the company’s future. I suspect it is also a good pick for many German and central Europe pension funds.

Price to free cash flow used to hover around 20, with periodic spikes at very high ratios like 60+. At the moment, the ratio is a meager 10, reflecting the markets’ disaffection for boring companies, and the preference for flashier growth stocks like the FANGs or Tesla, or even crypto.

Using a conservative ratio and growth rate, we end up with an intrinsic value of $69, below the current $62. I picked a 5% growth rate (the expected growth of revenues) which does not include any improvement in margins.

Considering the stability of the company, I could also have used less margin of safety and also the historical ratio of cash flow. This would give us a slightly better intrinsic value.

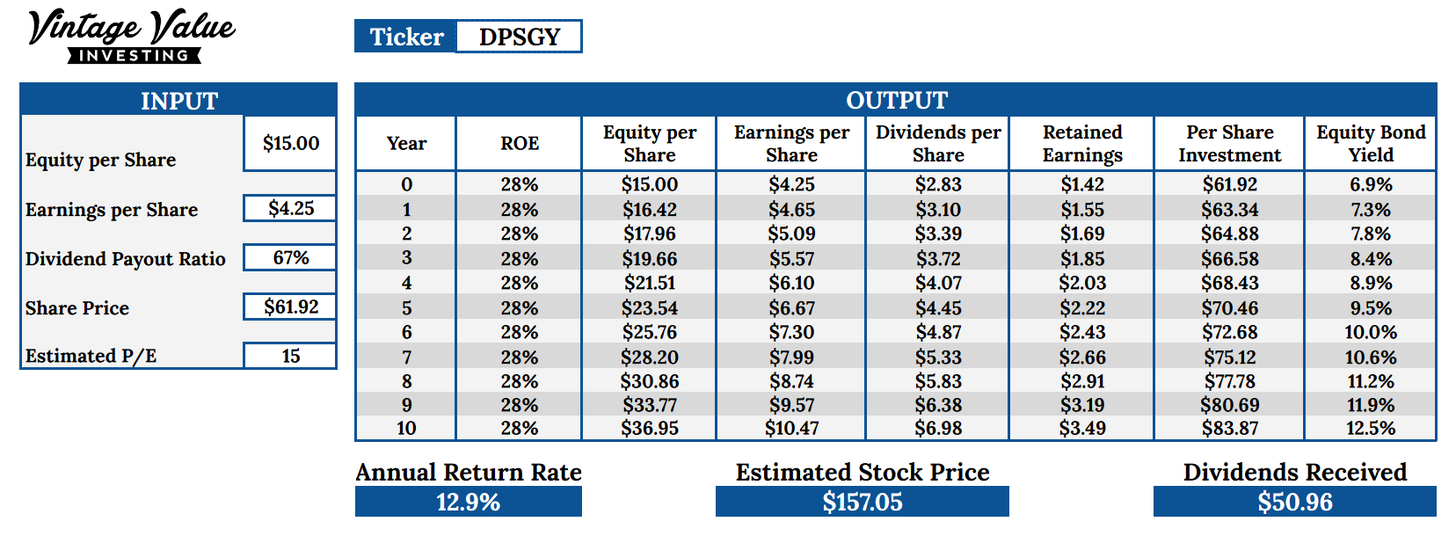

Equity bond

The equity bond yield looks at the company from a long-term perspective and works well for companies with a stable outlook, growth, and dividend growth. So Deutsche Post seems a good match, and this way, I can compare it to the DCF calculation.

DCF gave me a return rate of 15-17%, Equity bond gave me 13%. The second is a little low to my taste, but I must admit that the long-term safety and perspective of the company might be worth it.

Conclusion

I first looked at Deutsche Post because of good financial metrics and to study a blue-chip company for a change. It pleasantly surprised me by what hid in plain sight. Like the very international profile and the ownership of DHL, which I am sure experts in the sector are well aware of, but I did not know about.

The more I studied Deutsche Post, the more I liked what I saw. One way to see the company is to look at it as this large, global, well-managed, low growth company. Profitability is good, return on capital too, and some growth in the 3-5% range is likely. Downturns could temporarily damage quarterly profits but are unlikely to damage seriously the business.

So, in that respect, this would make Deutsche Post a very good buy-and-forget stock, especially for a retirement account with tax advantages.

But after studying more about the business organization, the competitive situation, and the technological potential, I realize Deutsche Post also offers something more. It is BOTH, a steady, profitable blue-chip company AND an unrecognized potential growth stock. The growth is not there yet, but the technology is right now reaching the maturity level to make it happen.

So, the plan with Deutsche Post would be to go for a buy-and-forget strategy. But also, to look out for the switch of the company to a tech profile and keep that as an added option in the future. I derided a little the IoT and blockchain “Global Center of Excellence” as corporate speech, but actually, this might be the most important part of the company.

Notably, the “Intelligent Automation of Physical Operation”. The language seems voluntarily obscure and obfuscating. Autonomous delivery is indeed one focus of the company’s R&D efforts, except that they are waiting for a little before being too loud about it. Better let the market and the competition realize too late than too soon what is going on.

With the current undervaluation compared to the current profitability and growth, the worst-case scenario is likely okay returns. But if things go well, and automation becomes a big theme, this might put Deutsche Post / DHL in a whole new category.

In that case, repricing the stock at a higher ratio TOGETHER with increased profit could send the stock to new highs.

And if nothing of the kind happens, boring but profitable is still pretty nice after all.

Limited downside but large upside, with lower than usual volatility, seems a pretty delightful combination.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in DPSGY and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.