Interest rates have become big news, even outside the financial community. Speculation over interest rate movements is intense, and markets hang on every word from the Federal Reserve’s Open Market Committee.

How do interest rates affect the economy, and why are they suddenly so important?

Let’s answer some common questions.

What Interest Rate Does the Federal Reserve Set?

The Federal Reserve’s Open Markets Committee sets the federal funds rate, sometimes called the federal funds target rate or fed funds rate. This is the rate banks charge when they lend to each other, often on overnight loans.

The federal funds rate is usually expressed in a range from 3.75% to 4%, for example.

☝️ Commercial interest rates are always higher than the fed funds rate.

How Does the Fed Funds Rate Affect the Rate on My Loans and Credit Cards?

The fed funds rate is a benchmark interest rate. Many loans and credit cards base their interest rates on this rate.

👉 For example, a mortgage lender may use a base rate of the fed funds rate plus three percent, or a credit card issuer may charge the fed funds rate plus 15%.

If you have a variable-rate loan or credit card, your interest rate will rise every time the fed funds rate rises.

If you have a fixed-rate loan, your rate on existing loans will stay the same even if the fed funds rate rises. If you apply for a new fixed-rate loan, you’ll pay the new, higher rate.

What Other Benchmark Interest Rates Are There?

The fed funds rate is not the only benchmark rate. Here are some others that you may hear of.

- The prime rate is the rate that banks charge their best and most creditworthy customers, usually large corporations. This is the lowest rate banks will lend at.

- LIBOR, or the London Interbank Offered Rate, is the average rate used between banks in London’s interbank market and is often used as a reference rate for currency transactions and international loans.

- The 10-Year US Bond rate is the rate paid by the benchmark 10-year treasury bond. It’s often used as a reference for bond market transactions.

These rates, especially the prime rate and the US bond rate, tend to move with the fed funds rate. If the fed funds rate increases, the prime rate, and the US bond rate will also increase. LIBOR tends to respond to rates set by the Bank of England, the UK’s central bank.

☝️ Commercial lenders may base their rates on the prime rate rather than the fed funds rate.

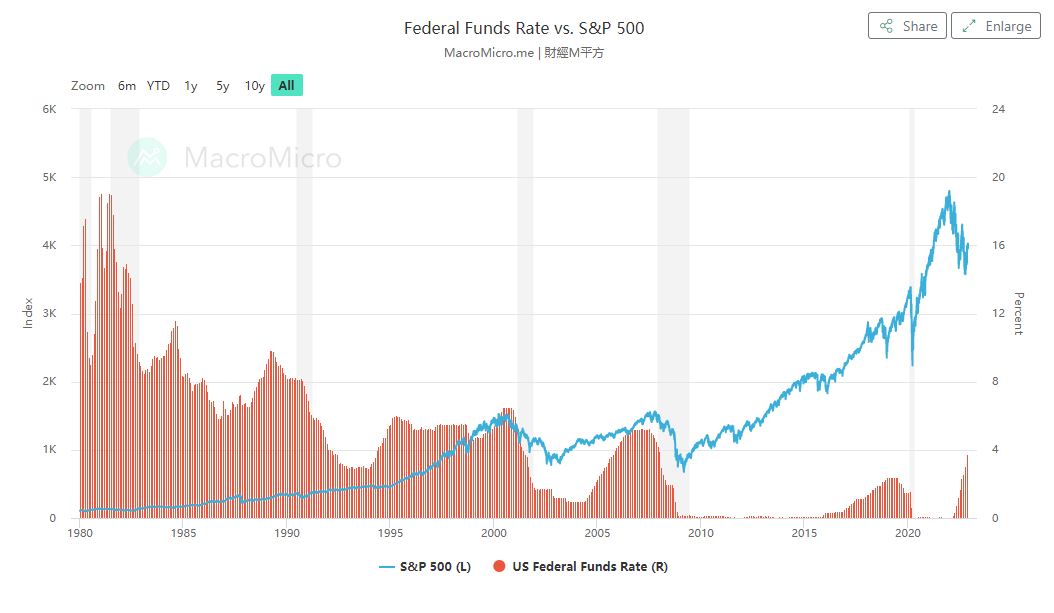

Are Today’s Interest Rates the Highest Ever?

As of Nov. 1, 2022, the fed funds rate is 3.83%. This is the highest rate the US has seen since 2008. During the 2008-2009 recession, the Fed dropped rates to historic lows to stimulate the economy. From June 2009 to May 2017, the fed funds rate was less than 1%.

As this chart shows, today’s rates are higher than they’ve been for many years, but they are still relatively low by historical standards. In the early 1980s, the last time the US saw serious inflation, the fed funds rate peaked at over 20%.

How Do Low Interest Rates Stimulate the Economy?

Low interest rates act on the economy in several ways.

- They encourage purchasing. Low interest rates make buying on credit cheaper and particularly encourage purchases of large items like homes and cars. This raises the demand for goods and services.

- Companies expand. Many companies rely on borrowing to fund expansion. Cheap loans are an incentive to expand production, which increases supply and creates employment.

- Investment increases. When interest rates are low, there’s an incentive to invest borrowed money in asset markets, especially for large institutional investors that have access to the lowest interest rates. Stock markets tend to rise.

Low rates stimulate economic growth, but they don’t bring equal benefits to everyone. People with poor credit will still face low access to credit and high interest rates when they can get credit.

People with poor credit and low incomes (they often go together) may benefit indirectly from greater access to jobs – if they are qualified for those jobs – but they also suffer most when increased demand pushes prices up.

If Low Interest Rates Drive Economic Growth, Why Does the Fed Raise Rates?

Low interest rates stimulate economic growth. Economic growth is a good thing. So why doesn’t the Fed keep interest rates low all the time?

That has actually been the Fed’s policy since 2009: interest rates have been extremely low by historic standards almost continuously since that time. Low interest rates still bring problems:

- Inflation. In theory, low rates should stimulate both consumer demand and added production. In practice, demand often increases faster than supply: expanding production takes time. If companies can’t get enough workers or raw materials, demand outstrips supply and prices rise.

- Asset bubbles. If interest rates stay very low for a long time, the borrowed money flowing into assets can push prices far beyond any reasonable value. These asset bubbles eventually burst, often with large losses.

- Reduced incentive to save. When interest rates are low, savings earn less. Fixed-income investments like bonds, savings accounts, CDs, and money market accounts have lower yields, and people tend to avoid them.

- Lack of latitude for response to problems. The Fed cuts rates to stimulate the economy during cyclic recessions or black swan events (like a pandemic). If interest rates are already minimal, they have nothing left to cut.

Politicians and voters both love a “red hot economy,” but that is still rarely desirable or sustainable. Raising rates to slow the economy down is often an unpopular policy, so it’s often delayed for too long.

How Do Interest Rates Affect Stock Markets?

Low interest rates tend to be associated with rising stock markets. We see that clearly in 2020-2021 and from 2010 to 2016.

The influence also goes the other way. The Fed often sees booming stock markets as a sign that the economy is heating up and rates need to rise.

One exception to this rule was the “jobless recovery” of 2010-2014. The Fed kept rates low despite rising markets because unemployment remained high, and they hoped to stimulate job growth.

Low interest rates stimulate markets in three main ways:

- Rising demand drives higher revenues and profits, drawing more money into stocks.

- Yields on fixed-income investments fall, so investors move money to stocks instead.

- Higher profits and incomes mean more cash for investors to place in stocks.

- Borrowing becomes cheap, encouraging speculation with borrowed money.

All of these factors work in reverse as well, higher interest rates tend to drive markets down.

How Do High Interest Rates Affect the Housing Market?

Interest rates have a dramatic impact on the cost of buying a home. Almost all homes are bought with large long-term loans. Even a 1% increase in a mortgage increase rate can add tens of thousands of dollars to the cost of a home.

Rising interest rates tend to reduce demand for new homes, which usually translates to fewer sales and lower prices.

How Long Will Rates Stay High?

It’s impossible to know for sure. Comments from St. Louis Fed President James Bullard indicate that rates will get higher and may remain at elevated levels through 2024.

This could change. If inflation slows or the economy sinks into recession, the Fed is likely to cut rates sooner. If inflation stays high, rates could stay elevated for a longer time.

How High Will Rates Go?

This is another thing that nobody knows for sure. The Fed will push rates as high as they think is necessary to get inflation under control. In 1981 the fed funds rate pushed up to 20%. That’s extremely unlikely to happen again.

St. Louis Fed President James Bullard, in the interview stated above, stated that he believes rates will need to reach 5% to 5.25% to get inflation under control.

Will High Interest Rates Control Inflation?

The classic description of inflation is “too much money chasing too few goods.” That typically occurs when the amount of money in circulation is high, driving the demand for goods above the supply of goods and pushing prices up.

The current round of inflation is a bit different. It’s driven less by a surge in available money than by a reduction in the goods available: pandemic-driven supply chain issues and the Ukraine war have created extensive shortages.

Those shortages have been exacerbated by continuing COVID-related restrictions in global manufacturing powerhouse China, cutting not only the supply of goods but also cutting the flow of key components for many US-made products.

It’s not clear how effective higher interest rates will be at controlling inflation that’s driven by the supply side rather than the demand side. It could even be counterproductive, as rising rates could constrain investment in new manufacturing capacity.

Why Does the Fed Use Interest Rates to Control Inflation?

The Federal Reserve’s default response to inflation is higher interest rates. That is not necessarily because higher rates are the most effective response.

Interest rates are the only effective lever that the Fed controls, so they are the first and last resort as a response to inflation. Any other policy change would have to come from Congress, which is typically paralyzed by partisan political concerns.

That leaves interest rate increases as not necessarily the most effective response to inflation but the only response that the Fed can implement immediately without having to move through a politically controlled process.