What is a market bubble? The simple answer is that a market bubble happens when the price of an asset rises to a level high above its fundamental value.

That simple answer is not satisfactory, because the “fundamental value” of an asset isn’t always clear. It’s hard to find two investors who agree on what a “high” asset value is.

It may be hard to define exactly what a bubble is, but most investors know we had two of them quite recently: the dot-com bubble of the late 90s and the real estate bubble of the mid-00s. In both cases, values soared and many investors made money. Then they crashed, many investors lost money, and the economy sank into recession.

The Anatomy of a Bubble

Asset prices rise because people buy the asset. That’s true whether we’re talking about real estate, stocks, cryptocurrency, or tulip bulbs. Of course, people buy assets all the time. To inflate a bubble you need a sudden and sustained surge of buying.

That requires three things.

- Liquidity. People can’t buy assets unless they have liquid cash. Periods of low interest rates and relatively easy access to credit often help to kick off a bubble.

- Confidence. Bubbles typically begin during periods when people perceive the economy to be healthy and their prospects to be good.

- Excitement. The perception of a revolutionary change or an emerging “new paradigm” often drives high-risk investing behavior.

These ingredients are not some explosive recipe that instantly expands into a bubble. Even when conditions are right, a bubble grows in stages. This chart shows a typical bubble pattern.

The peak of the bubble is often called a “Minsky Moment”, after economist Hyman Minsky, whose theories on the movement of an economy from stability to instability to crisis are central to our understanding of bubbles.

A Minsky Moment can be a relatively minor event. If asset prices are stretched far beyond any rational construct of value and valuations are supported largely by borrowed money, any trigger can burst the bubble.

Opportunities and Risks

A bubble produces both risks and opportunities. People who were holding assets at the start of the bubble or purchased them relatively early in the upswing can earn huge profits if they sell before the peak.

Many people are sucked into the frenzy late, often driven by FOMO: the fear of missing out. They take the worst hit, as they often buy at high prices and cling to their assets as the values plunge.

Cashing in on a bubble requires discipline and a cool head. It’s not easy to sell assets when the value is soaring every day and everyone around you is scraping together money and even borrowing to put more into the market. That’s still the best time to sell, and wise and wealthy investors have known through the ages.

“Buy on the sound of the cannons, sell on the sound of the trumpets”

Attributed to Nathan Rothschild (1777-1836)

“Be fearful when others are greedy, be greedy when others are fearful.”

Warren Buffet

Both quotes deliver the same message: buy in the “despair” phase and sell in the “mania” phase.

Bubbles Aren’t Universal

Most bubbles are focused on one asset or asset type. Other assets may languish ignored, or even fall in value as investors liquidate other holdings to raise cash to put into the fashionable investment of the moment.

For example, look at this chart of three stock indices during the late 90s dot-com boom. The tech-heavy NASDAQ soared to the heavens and then dove into the pit, while the broader S&P 500 and the Blue Chip Dow Jones Industrial Average showed relatively minor fluctuations.

This happens because bubbles are essentially psychological phenomena, not economic phenomena. From an economic perspective, there is no reason to buy an asset if the price exceeds the value.

People buy into a bubble because of belief. Investors set valuation aside, and buy simply because they are convinced that someone else will always be willing to pay more. Even professional money managers get sucked into the frenzy as clients demand the “exponential returns” they are hearing about in the media.

🧐

Great Bubbles Through History

Market bubbles are as old as asset markets. Here’s a look at some classic examples.

Tulipmania

The first recorded bubble occurred in the Netherlands in 1636 and early 1637. The Netherlands was the trading capital of the world at the time, with the world’s highest per-capita income and well-developed financial markets. Speculation in tulip bulbs reached such a fevered pitch that a single bulb had the same price as 5 hectares of land. Traders embraced futures contracts and other forms of derivatives. Prices collapsed, and many speculators were left holding bulbs and contracts that were effectively worthless.

The South Sea and Mississippi Bubbles

These speculative surges peaked in 1720. Both were driven by fevered and often wildly exaggerated stories of the riches that state-sponsored trading companies would reap from explorations in North and South America. Investors piled in and shares soared to extraordinary values until the bubbles burst.

The Roaring 20s

The emergence of new technologies dominated the 1920s: automobiles, aviation, railroads, refrigerators, and many others were becoming popular. Consumer credit, available for the first time to many people, drove demand for goods and poured borrowed money into the stock market. Stock prices plummeted in 1929, kicking off the Great Depression.

The Dot Com Bubble

The tech bubble of the late 90s was driven by the emergence of the baby boom generation into their peak years of earning and spending the end of the cold war, and the emergence of a new generation of technologies. Investors poured money into tech stocks, and by the late 90s, it was common to see IPOs of companies with no products or revenues, just an exciting story. Conventional stocks languished as investors focused almost exclusively on tech and internet-related stocks

The Real Estate Bubble

The recession following the dot com bubble was relatively mild, as the Federal Reserve lowered interest rates to near zero and flooded the economy with liquidity. Much of that liquidity poured back into asset markets, and speculation in real estate, in particular, pushed prices rapidly higher. By the peak of the bubble, lenders were making “NINJA” mortgages – no income, no job – purely on the belief that property values would rise even more, and financial institutions were packaging arcane forms of mortgage-backed securities. When prices crashed many property owners were left holding loans that far exceeded the value of their properties, and defaults and foreclosures peaked.

Each of these bubbles was different from its predecessors in some way. Variety is a key driver of bubbles. Because every bubble is different, speculators, politicians, and regulators can tell themselves that this time will be different, that this really is a new paradigm.

People like bubbles, and that makes them hard to spot. Investors make money. Small investors make large gains and feel smug, satisfied, and superior. Jobs multiply, tax revenues soar, and politicians are happy. Anyone who questions the prevailing euphoria is accused of spreading “FUD”: fear, uncertainty, and doubt.

Can You Spot a Bubble?

If you could identify a bubble, you’d be in a great position to make money. Looking back at the stock charts of past bubbles is an exercise in “woulda coulda shoulda”: buying at the right time and selling at the right time could have made anyone rich.

Unfortunately, nobody can reliably say what stage a bubble is in or when a bubble will burst. There is no certainty, but there are signs.

Prices Exceed Value

The definition of a bubble is an excess of price over value. That’s often difficult to determine, because “value” isn’t always clear. It is fair to say that a stock or market sector is in bubble territory when prices exceed any rationally supportable construct of value.

One of the simplest guides to stock value is the price/earnings or P/E ratio. It is normal for fast-growing companies to have higher than average P/E ratios: people are paying for future expected earnings, not current earnings.

👉 P/E ratios soaring to extreme levels is a sign that investors are setting rational valuation aside. People are no longer paying for assumed earnings, they are simply assuming that because the stock is popular and has a high profile, somebody will be willing to pay more for it.

Hype is Everywhere

Hype is a defining characteristic of a bubble. Stories of instant millionaires and incredible gains proliferate. Newly successful investors will proudly share their infallible recipes for instant success. Investing is a sure thing, you just put your money in and watch your gains roll out.

💡 I used to refer to what I called “the barbershop theory of investing”: when your barber starts talking about an asset class, sell it at once. When literally everyone is putting all their spare money into an asset class, there’s no room left for growth because there’s no new buying power left.

Bubble hype often features claims that “everything is different this time”. It’s a “new paradigm”; investing has been “democratized” and the secret to making money is no longer limited to the rich. It’s easy to believe when you want to believe. Media, politicians, and even some investment professionals join in the chorus until it becomes a collective delusion.

Asset Prices Exceed User Capacity

Not all bubbles involve stocks. A stock market is inherently speculative: everyone is buying with the expectation of selling at a profit. When that speculative approach extends to asset classes like real estate, assets may be priced out of reach of people or businesses who need them.

Real estate prices may rise to the point where people who need a place to live can no longer afford them without going into excessive debt. That’s a good sign that prices are being driven by speculative demand, not user demand.

☝️ When people are willing to take on excessive debt (relative to their income) because they are sure the asset will keep gaining value, you’re probably in a bubble.

When “flipping” becomes a household word, and people are borrowing money to buy “off plan” units in buildings still under construction or in planning, you’re certainly in a bubble.

Borrowed Money Flows into Markets

Debt is both the fuel and the downfall of many bubbles. You can’t pump up a bubble without money: people need money to buy assets.

When market returns are high and interest rates are low, it seems logical to borrow money and put it in the markets. If you’re paying 4% a year on your debt and gaining 15% a year – or more – on your investments, the difference is pure profit.

The problem is that debts come due. Sooner or later, an investor has to pay off debt for a losing investment. They do that by selling other investment holdings. Those sales drive prices down, and other investors have to do the same.

You can’t “HODL” (hold on for dear life) if you need the money to avoid default on a debt. As more investors are forced to sell to meet obligations prices can plummet, leaving some investors unable to cover debts even by selling other holdings.

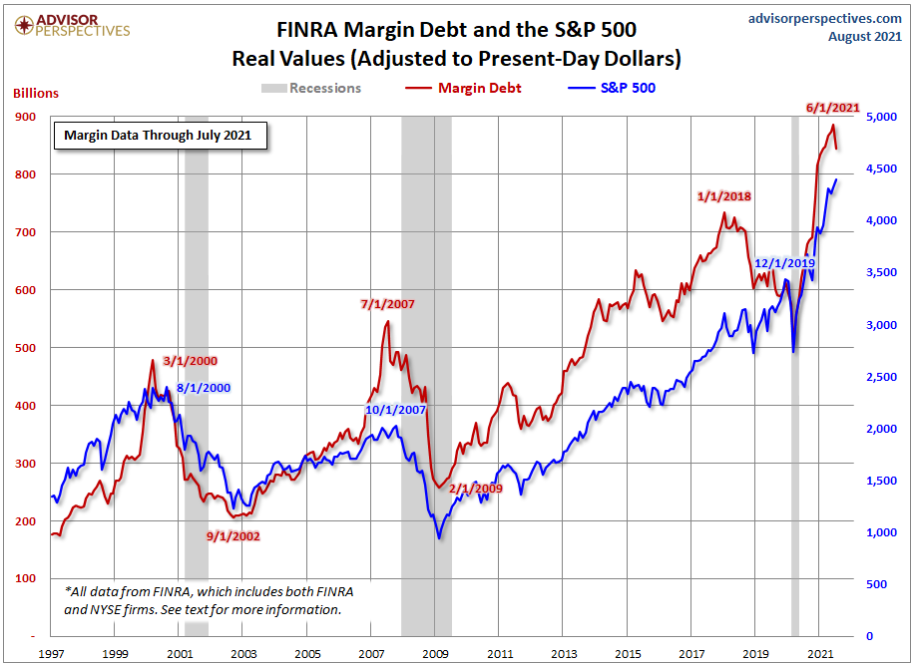

One indicator to watch is margin debt: credit extended by brokers to customers who want to buy stocks.

As you can see, margin debt peaked before both the 2000 and 2008 market crashes.

Margin debt isn’t the only way investors borrow money to buy stocks, but if margin debt is peaking it’s a good indication that borrowed money is pouring into the markets. Because margin debt is callable – the lender can demand repayment in full – it is a type of debt that’s uniquely able to kick off a downward spiral.

Don’t Get Caught

Nobody wants to stay on the sidelines during a bubble: there’s too much money to be made. Nobody wants to be the one left without a chair when the music stops. We don’t know when the music will stop, which makes bubble investing a gamble.

Here are some ways to put the odds in your favor.

- Keep your head. A bubble is first and foremost a psychological phenomenon. When everyone else is going crazy, stay grounded and remember that it will end.

- Never swim after a ship that’s already sailed. Investors flock to high-performing stocks: FOMO is real. Remember that the goal is to buy low and sell high, and you can’t do that if you buy high. No investor gets them all. Look for another ship.

- Don’t be afraid to take money off the table. If you have a tidy profit on an investment, there’s nothing wrong with selling some or all of a position. You may forego some gains if it keeps rising, but a bird in hand is worth two in the bush.

- Profit isn’t profit until it’s realized. It feels great to say that your portfolio is up xyz%, but until those gains are locked in, they aren’t real.

- Consider defensive strategies. Defensive investment strategies won’t gain as much as aggressive strategies, but they will protect you in a downturn. If you feel that markets are approaching bubble territory, putting part of your portfolio in defense mode makes sense. Methods like stop-loss orders can help protect an aggressive portfolio.

⚠️ None of these methods will guarantee that you won’t take losses if a bubble bursts. Stock markets don’t offer guarantees. They do offer ways to improve your chances of emerging intact or with minimal losses.

You Can Beat the Bubble

Hyman Minsky, who we mentioned earlier, wrote one of the defining statements about bubbles:

“Stability leads to instability. The more stable things become and the longer things are stable, the more unstable they will be when the crisis hits.”

Hyman Minsky

Stability breeds both confidence and capacity. When people feel secure they take risks, and when they are financially stable they have the means to take risks.

Minsky understood what many investors and politicians don’t want to accept: the danger phase is not the collapse of a bubble, but the expansionary phase that comes before the bubble.

That’s hard for many people to accept because bubbles are fun. Everybody makes money and everyone feels smart. Tax revenues soar, the populace is content, and political leaders are popular. That euphoria makes it almost impossible to implement policies to constrain a bubble.

Government agencies and the mass of investors may not be able to recognize a bubble or act to constrain it. You can still recognize one yourself and act to maximize your gains and control your losses. If you succeed, you can turn the bubble to your advantage.