It seems like an obvious move. We’re in a bull market and stocks are soaring. Interest rates are still near historic lows. If you can borrow money at a single-digit annual interest rate, you should be able to earn enough in the market to pay off the loan and earn a substantial profit. But how does that work in practice? Can you borrow money to buy stocks? And more importantly, should you?

Let’s take a closer look.

Yes, You Can Borrow Money to Buy Stocks

The simple answer to the question is yes: you can invest borrowed money in stocks. It’s a risky strategy. It’s also quite popular, especially during bull markets. Some people have used it very effectively and made money. Others have lost, sometimes badly.

That’s the simple answer, but how do you go about doing it?

The decision to invest with borrowed money comes down to comparing the cost of borrowing versus the expected investment returns… If the returns exceed the cost, then the transaction makes economic sense.

S. Michael Sury, Lecturer of Finance, University of Texas at Austin.

How Can You Invest in Stocks With Borrowed Money?

There are several ways to invest in stocks with borrowed money. Here are the most important ones.

1. Margin Accounts

Many brokers will lend you money to buy stocks. This is called buying on margin, and you’ll need to open a margin account to do it. A margin account is different from a basic cash account, in which you can only purchase securities with the cash in your account.

You’ll have to apply for a margin account with your broker. You’ll need a minimum investment of $2000. When you buy stocks, you can borrow up to 50% of the purchase from the broker. You will have to pay the balance yourself. This enables you to make larger purchases than you otherwise could.

The money or securities in your account are collateral for the money you have borrowed. This collateral is called your margin. When you sell the securities bought on margin the broker will deduct the loaned amount, along with interest and any fees involved.

Know the Terms of Your Agreement

This process sounds straightforward, but it’s important to know the exact terms of your margin account. Here are some particular things to watch for.

- Restrictions. You won’t be able to buy penny stocks, OTCBB securities, or IPOs on margin.

- Interest. Margin loans carry interest, which may be substantial. If you hold stocks bought on margin for some time you will have to make periodic interest payments. For this reason, margin purchases are usually intended to be short term holdings.

- Fees. Many brokers impose fees for margin transactions. You’ll have to factor the fees into your calculations of cost and benefit.

- Maintenance Margins. This is the minimum balance you must keep in your account. If your balance is below this level you may have to deposit funds or sell stocks. You’ll need a maintenance margin of 25% of the account value or $2000, whichever is greater.

- Margin calls. If you fall below the maintenance margin (for example, if your stocks fall in value) your broker can issue a margin call, requiring you to deposit funds. If you don’t, the broker can sell securities at their discretion without your consent. Many margin agreements allow brokers to sell without warning you first.

Buying on margin can be profitable if your investment appreciates significantly in a short time period. If you have to hold the stocks for an extended period the interest charges may outweigh your profits. If the stocks that serve as your collateral drop in value, you may have to put up cash or sell your stocks at a loss.

A margin call is an issue that demands immediate attention. If you don’t deposit cash or sell stocks of your choosing your broker can sell whatever they like to cover the call. Because margin loans are callable, they are considered a high-risk method of investing.

The rules governing margin accounts are complex, and it’s important to understand margin accounts before you consider using one.

2. Other Loans

Any loan that generates disposable cash can be used to buy stocks. Your broker won’t ask where you got the money you deposit in your account. You can use a personal loan, as long as the lender does not place any restriction on the use of the loan proceeds. You could use a home equity loan or any form of loan that does not require the proceeds to be used for a specific purpose.

These loans have one advantage over a margin loan: they are generally not callable. You will still have to pay the loan back, and unlike a margin loan, you’ll have to make regular payments.

⚠️ If your investments don’t appreciate as fast as you expected, you could miss payments. That could trash your credit, and if your loan is secured you may lose your collateral. Remember that you will be paying interest on the loan, and often fees as well.

3. Loans From Friends or Family

Many young investors borrow money from friends or family to start investing. This is the least financially risky form of loan: your relatives won’t report missed payments to a credit bureau, and unless you have a formal promissory note you won’t face legal action.

⚠️ You could still face serious damage to valued relationships.

If you do intend to borrow money from friends or family to invest in the stock market, be upfront with what you’re doing. Make sure the lender knows what you’re doing and understands the risk.

4. Indirect Loans

Many people borrow money to buy stocks without even knowing it. If you have an active loan and you choose to invest money rather than make extra loan payments, you are effectively using borrowed money to buy stocks.

👉 If you could afford to pay cash for a car but instead take out a loan and invest the rest of your money, you are indirectly using a loan to buy stocks.

Of course, this isn’t always a risky idea. The risk level depends on the type of loan you hold and the type of investment you’re making

👇If you’re making 401(k) contributions while you still hold a mortgage, you’re taking a very low risk.

👆 If you choose to put money into meme stocks or cryptocurrency instead of paying off high-interest credit card debt, your risk is a lot higher.

Do People Borrow Money to Invest in Stocks?

Borrowing money to invest in stocks is popular and common. A study from MagnifyMoney revealed that 4 out of 10 surveyed investors had taken on debt to buy stocks. Some key points from the survey:

- Younger investors were more likely to take on debt. 80% of Gen Z investors, 60% of Millennials, 28% of Gen Xers and 9% of Boomers bought stocks with borrowed money.

- Personal loans were popular. 38% had taken personal loans to invest. 23% borrowed from friends or family. Others used credit card debt (14%), borrowed from a retirement plan (13%), or used home equity (11%).

- Many investors borrowed to fund retirement. 37% of those surveyed borrowed money to use in their retirement plan. 32% wanted to buy a particular stock, 31% were day trading. 10% bought cryptocurrency.

- Most would borrow again. 61% said they would borrow again to fund investments, 33% said they might consider borrowing again.

- Borrowings were substantial. Almost half of the borrowers took out loans of $5000 or more. 20% took over $10,000.

One notable point: the study did not include margin debt. That may be why Gen X and boomer investors were less likely to report borrowing. Older investors are more likely to qualify for margin accounts.

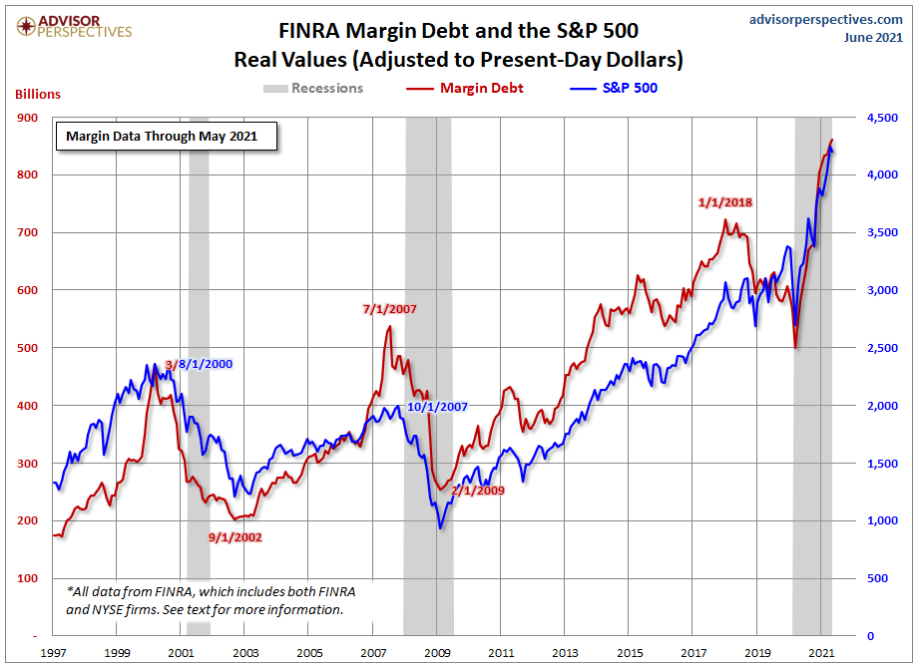

Margin trading is also considerable, and margin debt is currently at all-time highs.

Source: Advisor Perspectives

With margin debt soaring and many investors actively taking on consumer debt to buy stocks, we can conclude that there’s a lot of borrowed money in the market today. If so many others are doing it, does that mean you should also borrow to invest?

Consider the Risks

You can borrow money to buy stocks, but you’ll be taking significant risks, and some of the risks may not be obvious. Let’s take a look at some of those risks.

Systemic Debt Risk

This risk is not specific to you. It applies to anyone using borrowed money to invest in a highly leveraged market. High debt levels mean high risk levels: if you look at the margin debt chart above, you’ll see that margin debt peaked before both the 2001 and 2008 recessions.

If stock values turn down, people who are borrowing to buy stocks don’t just have to sell the stock they borrowed to buy. They may have to sell other stocks to cover a margin call or pay back a loan. That selling pushes prices down further and pushes other investors into the same situation. That makes a highly leveraged market vulnerable to rapid price drops.

You should assess the impact of leverage on the market before making any investment, but it’s particularly critical when you’re investing borrowed money.

Risk of Loan Default Due to Investment Loss

This is the most obvious risk of using borrowed money to buy stock. If your selected investments don’t perform as expected you may lose money. You may then be unable to pay your loans. That could force you to liquidate other investments.

Your credit may suffer and you could be forced into default and even bankruptcy, depending on the amount and type of loans you’ve used to buy stock.

Risk of Leverage Addiction

This is perhaps the most insidious risk of borrowing money to buy stock. If you succeed and make money you’ll get a huge emotional high. You’ll feel smart and accomplished like you beat the system. There’s a very good chance that you’ll do it again. The more you succeed, the more likely you are to borrow more and take more risks. That can leave you in an extremely risky situation, and sooner or later markets do turn down.

When leverage works, it magnifies your gains… but leverage is addictive. Once having profited from its wonders, very few people retreat to more conservative practices.

Warren Buffet

The Experts Advise Against It… But Aren’t They Doing it Too?

Very few investment professionals would advise using borrowed money to buy stocks. Most would advise against it, and those who would approve would probably qualify their approval heavily.

That reluctance to endorse buying stock with borrowed money is often seen as hypocritical. Many of the fund managers and investment professionals that discourage individual investors from buying stock with borrowed money are managing highly leveraged portfolios. Warren Buffet, who has warned about the risks of leverage, used borrowed money to invest early in his career.

The difference, of course, is that individual investors simply can’t borrow on the same terms as large investment institutions. That may not be fair, but it’s still true. If you could borrow on the same terms as Berkshire Hathaway or a major hedge fund, and if you have professional-level risk assessment expertise, borrowing to buy stocks might be a good idea. Very few individual investors are in that position.

Investing with borrowed money could be a reasonable move if the loan terms are good and you’re very sure that you’ve predicted the stock’s movement accurately.

If you plan on borrowing money to buy stock you’ll need to know how to research and choose stocks. In most cases, you’ll want to borrow to fund relatively short-term investments. That reduces your interest expense and makes it less likely that unpredictable market risks will occur while you’re holding that investment.

It’s very tempting to use low-interest loans to invest in a rapidly expanding market. It’s also very risky. You may choose to take that risk, but you’ll want to assess it very carefully and avoid getting carried away if you do succeed. Leverage has made some investors rich. It has also made some rich investors poor.