July 6th, 2021

Quick Stock Overview

Ticker: OTCM

Source: www.stockrover.com

Key Data

- Sector: Financial Services

- Sales ($M): $78

- Industry: Financial Data & Stock Exchanges

- Net Cash per share: $1.47

- Market Capitalization ($M): $550

- Equity per share: $2.02

- Employees: 102

- Debt / Equity: 0.7

Summary

The OTC Market Group (OTCM) is a stock exchange operator managing Over-The-Counter (OTC) trades. Instead of investing with its own or its client money, like a bank or a fund, it is one of the key elements in the machine making all selling and buying of stocks possible. It do not hold stock itself, nor take money from client or investors.

So, it is more a cog in the financial market and stock trading, with a risk profile completely different from most financial companies. In fact, it is a surprisingly easy to understand business for a financial company.

Stock exchange companies like OTCM, NYSE or the NASDAQ are managing the listing, selling, and buying of shares, but do not own them. So, they are financial companies, but without the opacity and complexity that come usually with financial stocks like banks or investment funds. You can find a more detailed overview on how stock exchanges operate and what the term OTC means here.

So, what exactly are stock exchanges doing? Simply said, they allow buyers and sellers of financial products to meet. Most investors pass by a broker when they are buying or selling stocks and other financial products. Then, this broker goes on an exchange, and finds what he needs to satisfy the request of his client, from another broker.

Stock exchanges, by centralizing data and having thousands of brokers registered at once, allow for markets to function more smoothly, making the job easier for brokers to find a buyer when they want to sell something. The exchanges also usually operate a system giving the last price for a given stock.

You are probably familiar with the fees your broker charges you when you do a trade. Part of these fees are in turn paid to the stock exchange for facilitating the transaction. So, the more trading happens, the more the stock exchanges make money.

Strategic Analysis

The largest stock exchange companies are juggernauts like Intercontinental Exchange, which owns the NYSE, but also another 11 stock exchanges, valued at $63B. In comparison, the OTCM market cap of $550M makes it a small cap actor in a small cap market.

But instead of focusing on the largest parts of the stock markets, where a ferocious competition is waged between the giants like the NYSE and the NASDAQ, OTCM managed to carve itself a small niche.

This niche is OTC trades (Overthe-Counter). In general, the larger stock exchanges require plenty of rules and minimum size for a company to be listed by them. This is fine for the likes of Amazon and Tesla, but that also means that some companies are unable to be publicly traded on the largest exchanges. This can be because the company is too small, or simply does not want to waste the money on complex and frequent regulatory requirements.

For such companies, parallel markets exist where brokers can still trade the shares, what used to be quite literally done in somewhat shady offices away from the main stock exchanges, or “over the counter”. OTC companies are not forced by the SEC to disclose the same amount of information than companies traded on the main exchanges.

Also, the trade volumes are generally lower, create some liquidity problems at times (it can be hard to buy or sell large amounts at once, as there are not so many buyers or sellers active at a given time). Due to lower liquidity and less regulatory oversight, OTC markets are usually perceived as riskier.

Overall, OTC markets are smaller, but also more lucrative for brokers and the stock exchanges that manage them. Investors in OTC markets have generally to pay higher fees, which helps rise the profitability of the involved stock exchanges.

The 3 Types of OTC Markets

OTC markets controlled by OTCM in the US are actually divided in 3, with each segment offering a different level of control:

Source: www.otcmarkets.com

OTCQX: The highest levels of regulation and reporting standards in the OTC market, the QX section, is something of an in-between from fully unregulated OTC markets and well-established larger NYSE or NASDAQ.

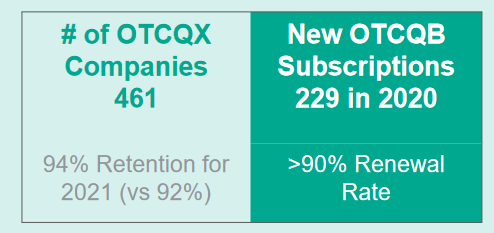

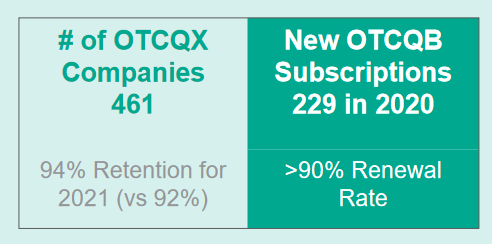

It is worth noting that the retention rate among the 461 companies listed in the QX market is very high, above 90%. I imagine that most of the removals are due to the companies in question growing sufficiently to join the larger stock exchanges instead. But overall, companies here are happy to deal with lighter regulations and less reporting hassle, while still enjoying a listing on a “reputable” exchange.

Source: www.otcmarkets.com

OTCQB: Also called the venture market, this is a place for growing startups. These companies have to submit their financials and follow some regulations, but they are less stringent than for the QX exchange. This is usually the place for growing companies before they can “graduate” to the OTCQX exchange.

Pink Sheet: Pink sheet companies take their names from the original documents about them, which was printed on an easy to recognize pink paper. These companies do not have to report their financials. They might do it, but they do not have to. Such reporting is also a lot less controlled.

This makes it a pretty wild area of financial markets, with many dishonest or even scammy companies bundled together with new and thriving businesses. Finding which is which is an exciting, but also very risky task for the investors. Think about the fraudulent schemes that occured from Wolf of Wall Street.This can give you an idea of the risk involved.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

OTCM activities and profits are derived from 3 separate activities, done throughout their 3 main OTC exchanges described above.

Source: www.otcmarkets.com

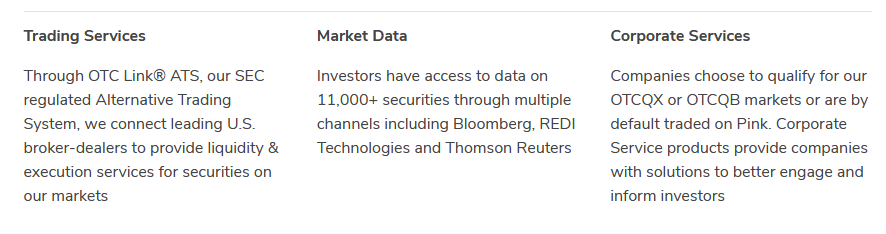

Trading Services: The trading service is the main stock exchange service. They provide connection between brokers and price quotations to make the exchange of OTC companies’ stocks possible at a low transaction cost.

Market Data: By being the middleman for the trading of 11,000+ OTC stocks, OTCM gathers tremendous amount of information about market condition, price, etc… Such information is extremely valuable for investment firms, analysts, banks, venture capitalist investors, etc… They also sell these data to other financial data firms, like Bloomberg or Reuters.

Corporate Services: The companies traded in OTC markets are often former private equity startups or private companies now publicly traded. This transition requires expertise regarding regulatory demands, management of investors’ expectations and new financials to disclose. OTCM, being the center of the OTC trading world, has an obviously strong brand and seems like a natural choice for many companies when they are looking to hire some consulting advisors on these matters.

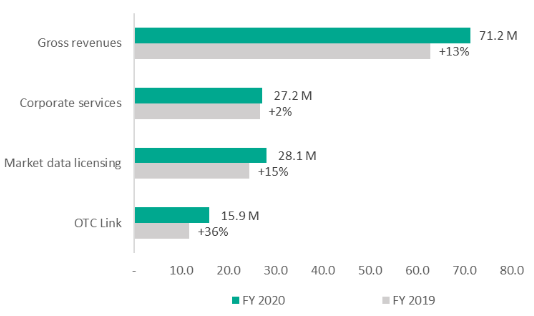

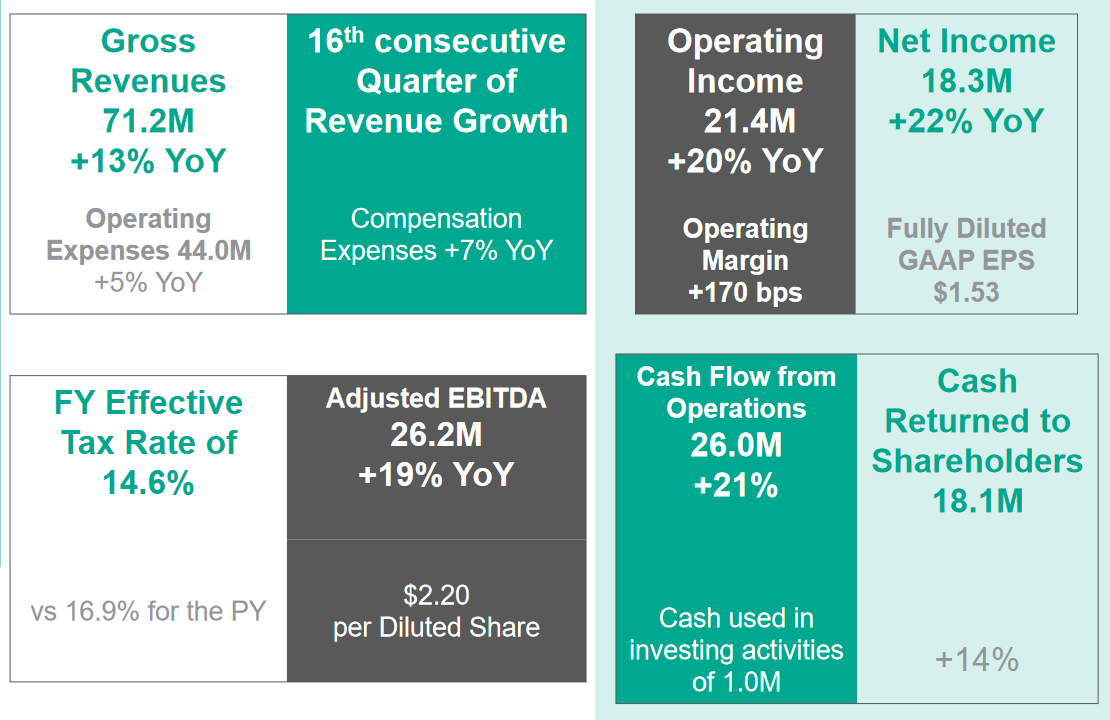

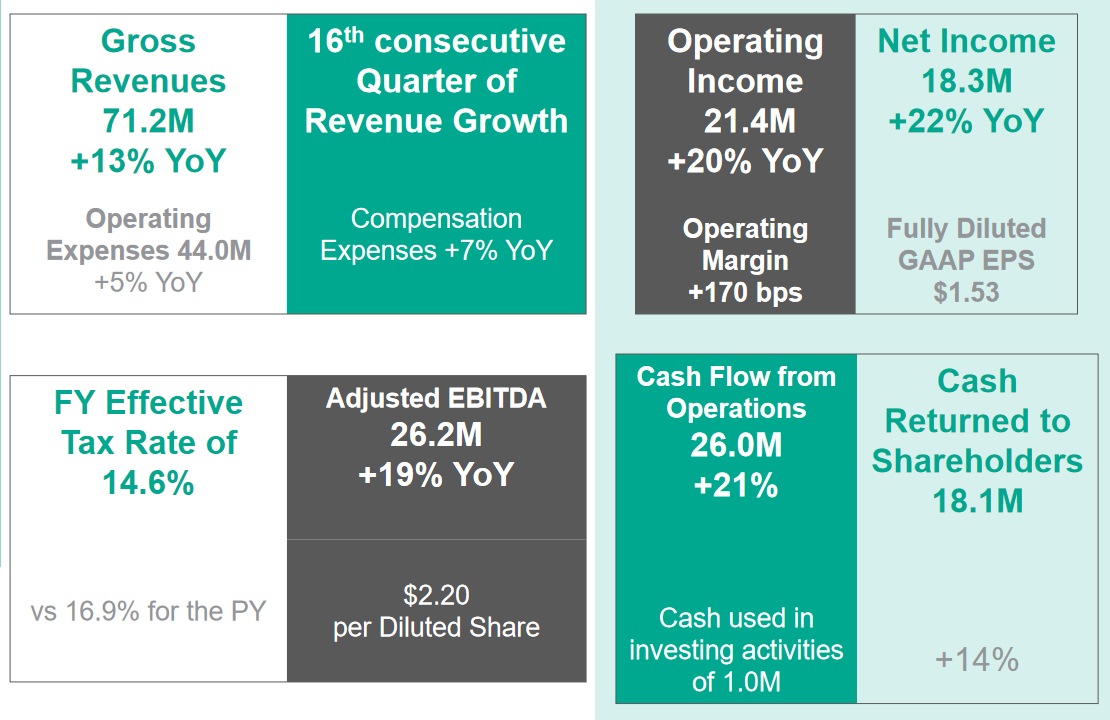

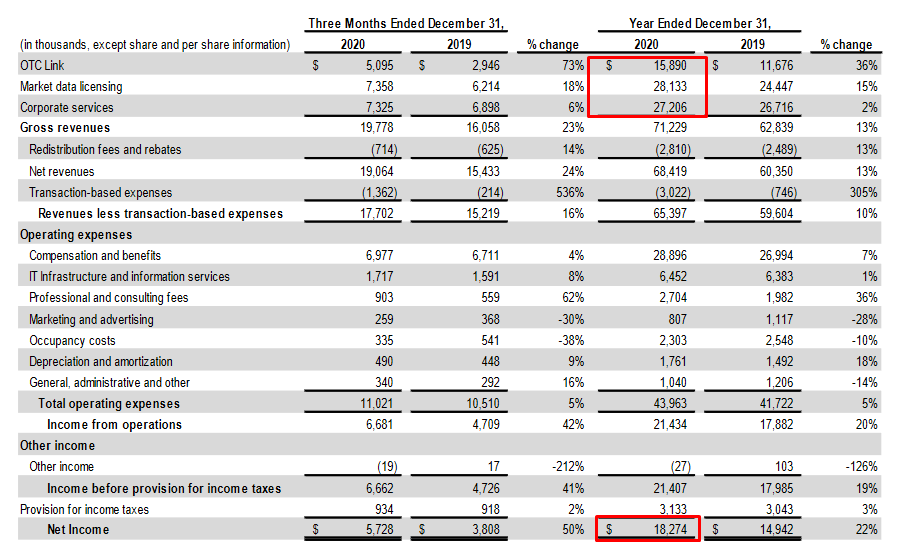

Surprisingly, the trading part of the business is actually the smallest source of revenue for OTCM, only $15.9Min 2020. The main value of the trading department is to generate data and expertise more than directly profit. This data is then monetized to generate $28M from both the corporate services and market data licensing.

So, in many ways, a proper analysis of OTCM is not so much to see it as an OTC stock exchange, but as a data company using its OTC trading branch as the source of the unique proprietary data. In turn, this data is what actually creates most of its income ($55M out of $71M).

Source: www.otcmarkets.com

Growth

OTCM have a long history of growth, from a small operator named “Pink OTC Market” in 2008, to the larger company of today operating beyond just pink sheet stocks.

In almost 10 years, revenues doubled, free cash flow quadrupled, and stock price went from a low of $5 to almost $50 (not even counting dividends on the way). So, this is already a 10-bagger for its early investors. I put the graph of these below so you can see it briefly before we look at numbers more in details in the quantitative analysis section.

Source: wwwfinbox.com

2020 was a strong year for OTCM, most likely due to the increase in interest for trading and investing among the general public in the midst of COVID-19 related lockdowns. On top of that, new companies that might not have fit the narrow requirements of larger exchanges still look to be publicly listed and did so through OTCM. This can be seen in the high number of new companies listed in the OTCQB (Venture) market, which was 229.

Source: www.otcmarkets.com

This resulted in strong growth in virtually all metrics, from revenue to income to cash flow.

Source: www.otcmarkets.com

Will the company be able to keep this growth rate? It mostly depends on general market conditions and if the speculative mood of the investing public stays so elevated. This is especially true for more riskier parts of the financial markets, like the OTC trades. So far in 2021, speculation is getting even more intense, but I would stay wary, as such exuberance is usually more a sign of an end of cycle and riskier period.

OTC trades have been rising in volume and value constantly over the last 10 years. But this is still not a full market cycle, so it is hard to predict how hard they would be hit by a financial crisis.

We will discuss these different growth scenarios in the valuation section.

Economic Moats

In value investing terms, moats are what allows a company to keep a hedge against it competition for a longer time.

Regulatory Situation

Even if less heavily regulated, OTC markets are still under strict supervision of financial authorities like the SEC. This is not a field were an upstart newcomer can come and disrupt the market with better offers or technology. At least not without first getting approval from the regulatory bodies.

I have considered in this report to go into details about every regulatory rule that OTCM must follow, as well as the recent updated rules, and soon-to-be changed rules. But frankly, these byzantine regulations are, in the long run, a strong moat for OTCM. Every new regulation and complexity will actually be a barrier to entry for eventual new competitors. And their costs are already reflected in OTCM margins.

It should also be noted that increased regulation on other exchanges might make OTC markets more attractive, helping OTCM to poach some clients from the NYSE and the Nasdaq.

So instead of trying to make sense and writing 25 pages about every possible regulation OTCM is submitted to, and their possible future evolution, I decided to just look for large incoming risks to its business.

So far, all new regulations in discussion might cause some extra costs, but nothing that could cause serious damage to OTCM profits. On the other hand, it will continuously make the position of the established players more defensible. I expect this moat to become almost indestructible over time, one additional page of extra regulations at a time. You can see more about the regulatory landscape and incoming changes on their annual report, page 12 to 15 (a rather technical discussion, but not impossible to grasp for a non-lawyer either).

Branding and Switching Costs

By being the OTC market of reference, OTCM’s exchanges carry a lot of weight among investors. They might be wary of stocks listed on a less well-known OTC exchange instead. OTC’s already do not have the best reputation, but a second grade OTC market sounds like looking for trouble. If you are curious to understand more about OTC and penny stocks, I recently wrote an article about it.

Similarly, companies looking for more liquidity and exposure to new investors have no interest to take the risk of going to a place that might make people suspicious of them. Cutting on costs or going to a new exchange just for slightly lower fees is simply not worth it.

Together, these two elements mean that brokers, who follow their clients’ preferences, will also stick with OTCM. OTCM profits from a strong dominant position that is self-reinforcing, making this moat durable and very hard to dent for a new competitor.

Management

Management is overall first grade and have a lot of experience and clout in the financial industry. I will only give details about a few of them and discuss how these high-quality profiles are both a good and a bad thing.

Cromwell Coulson, President and CEO

Director of OTCM since 1997, Mr. Coulson is a pillar of the company. He was the driving force behind the growth and success OTCM has experienced over the last two decades. A Harvard graduate, he is now 54 years old, and should be able to lead the company for quite a while longer.

Antonia Georgieva, CFO

A newcomer to OTCM since January 2021, her profile is rather impressive. She was partner at Drake Star Partners, and before that, a managing director at BMO Capital Markets Corp ($760Bin assets under management, or 8th largest bank in the US by asset size). There is no doubt about her professional abilities.

Bruce Ostrover, CTO

With a firm relying so much on its IT infrastructure, I want to see the CTO profile to tick off a major risk factor. With a diploma in mathematics and computer sciences, he has worked all his career in IT development for financial firms, especially Convergex, involved into broker orders management software solutions. So, if you need someone who knows the ins and outs of trades at stock exchanges, Bruce Ostrover seems the right person for the job.

The Others: Vice Presidents for Each Market Segments

Matthew Fuchs, Lisabeth Heese, Michael Modeski are all 45 to 51 years old. They each have long experience in large financial data handling and passed by prestigious financial firms and institutions. Here too, OTCM seems to be led by some of the best in the industry.

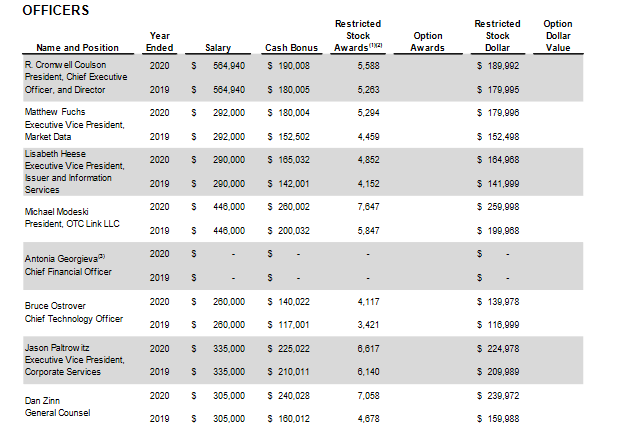

Compensation

With such a large selection of top-level talent, I was a bit worried of their compensation levels. This is a team that could easily choose to work at Goldman Sachs or join the top level of government regulators if they wanted to.

And frankly, my fears were quite justified. Together, officers’ salaries in 2020 are a total of almost $2.5M, to which a $1.4M of cash bonuses.On top of that comes a total in stock options worth almost $1.4M.. The total comes to a staggering $5.3M.

For perspective, the net income of the company was $18 million in the same year. Management’s compensation is more than a quarter as high as the company’s net income… or said another way, if management’s salary was halved, the company’s net income would got up by 10% overnight.

I am aware that such a highly regulated field needs top talent, but this frankly feels a bit steep.

Source: backend.otcmarkets.com

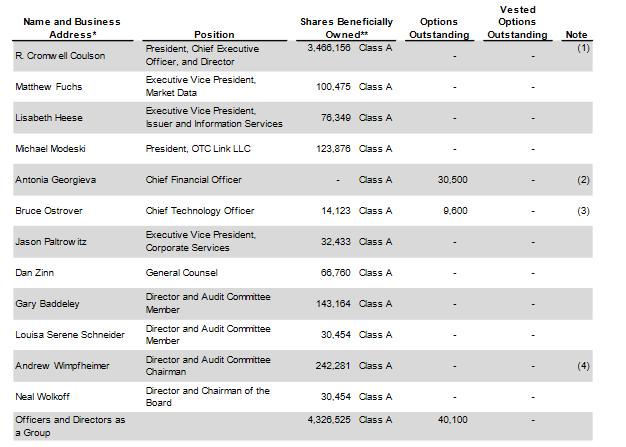

On the other hand, management not only a direct interest in their salary, but each has a significant wealth in the shape of OTCM shares, with an ownership increasing yearly with stock options. So, while I dislike the very onerous compensation, I think management’s interests are still mostly in-line with shareholders.

Source: backend.otcmarkets.com

Overall, stock options do not seem to cause a large dilution of shareholders overtime. But share count seems to be pretty stable, despite a sizeable stock repurchase program.

So, this needs to be remembered when management mentions share repurchases, that it is mostly a compensation for stock options, and should not be seen as cash redistributed to shareholders by other ways than dividends.

Source: www.finbox.com

Competition

Competition for OTCM is most likely to come from the bigger stock exchanges in USA. At the moment, the competition is limited to the very narrow set of companies that could list on the NYSE or NASDAQ and chose to do it on the OTCQX.

NASDAQ

NASDAQ has pushed for being authorized to manage thinly traded securities (low volume of trade). This would give it legal authorization to enter the market for some companies now traded only on OTC markets. In general, this seems to indicate that the NASDAQ group is somewhat willing to expand in the sector, but mostly through influencing the regulators than direct competition.

NYSE

A subsidiary of the NYSE Group Inc, Global OTC, it manages some automatic orders for specific OTC securities. While for now, the NYSE group seems fine to not compete too aggressively with OTCM, this is maybe the main risk for future competition for OTCM.

How much of a risk it is, is hard to quantify, and ultimately, the OTC market is likely to stay a side-project for the NYSE group, instead of a strategic target.

Quantitative Analysis

Financials

Revenues

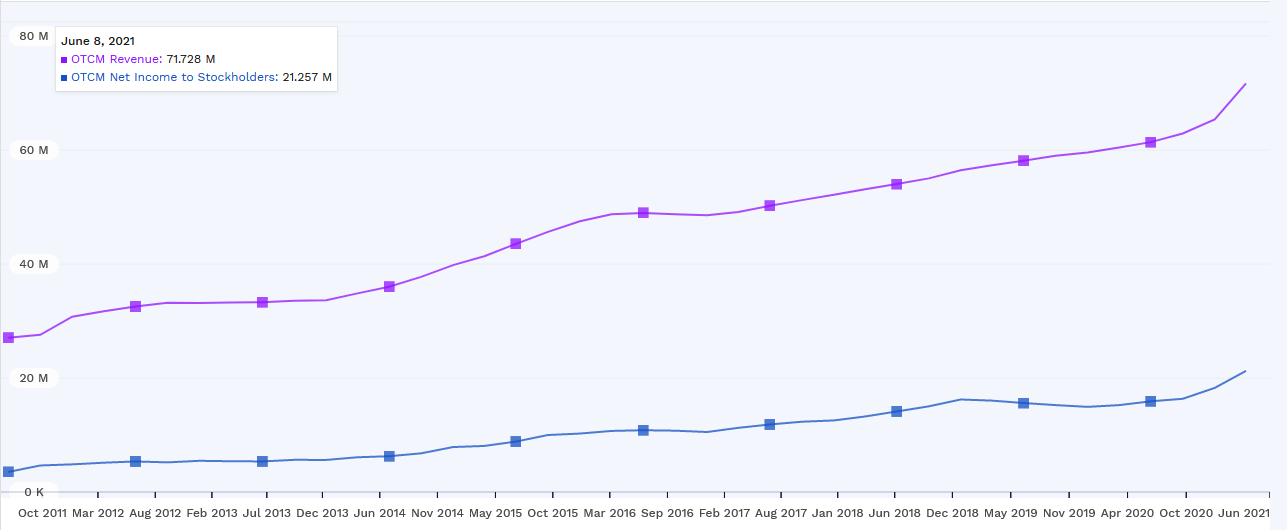

OTCM revenues have strongly grown in 2020, confirming a steady four years of continuous growth every quarter.

Source: www.otcmarkets.com

In fact, as you can see on this graph below, net income has been steadily growing over time. The growth was the result of the increasing size of the OTC market, a growth in which OTCM itself has been instrumental.

Source: www.finbox.com

Source: www.otcmarkets.com

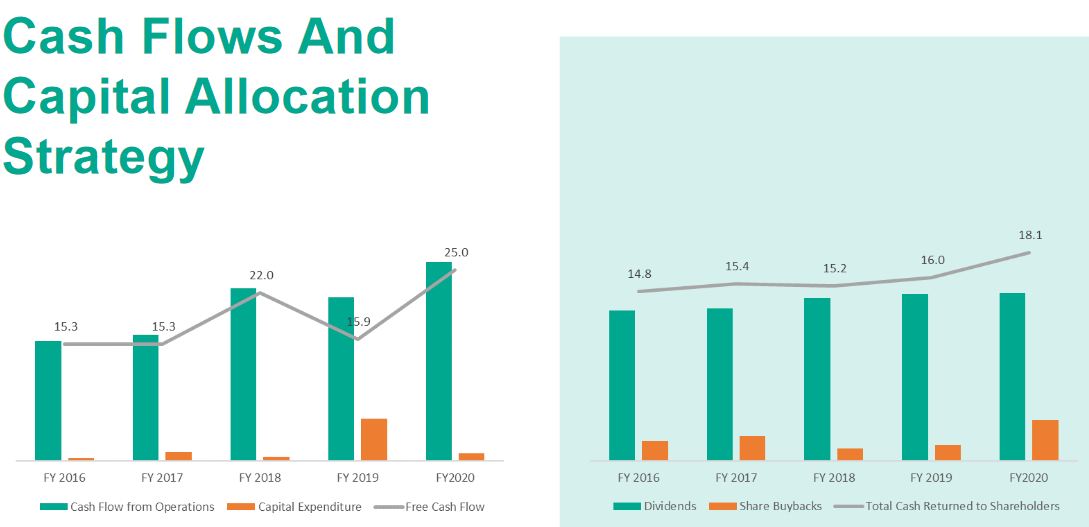

Dividends

Dividends have grown steadily from 2012 to 2015 and have stagnated since. As stock prices have gone up in the meanwhile, this has steadily decreased the dividend yield. This came at a time when free cash flow was growing, so I think dividends could soon start growing again.

Source: www.finbox.com

Debt and Balance Sheet

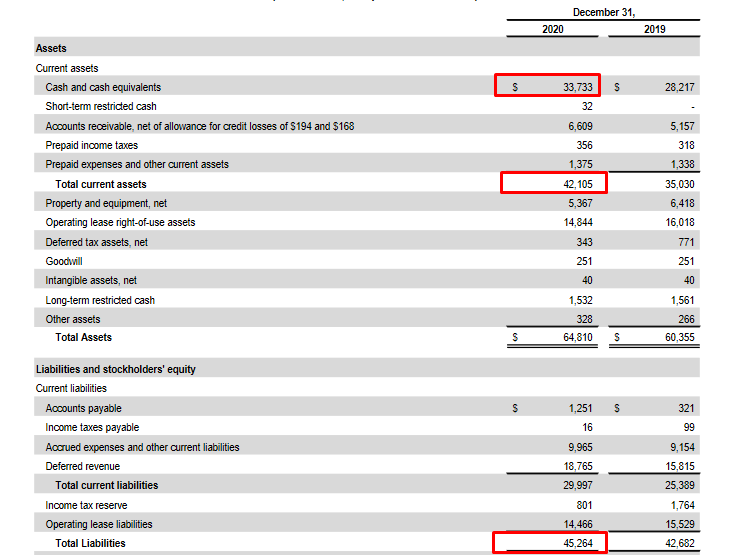

OTCM’s balance sheet is very solid, with current assets covering almost all liabilities. In addition, almost all liabilities are current liabilities occurred while running the business or a lease liability, instead of debt. The company is at no risk of bankruptcy and probably should be considered as a little cheaper due to its rather large cash cushion (8% of total market cap).

In addition, I would add that contrary to a bank or other financial institutions like hedge funds, stock exchanges do not carry a lot of counter-party risk, or complex, hard to value assets on their balance sheet. I do not expect hidden liabilities that could occur with the derivative book of a large bank, like for example the very large one of Deutsche Bank.

Cash Flow

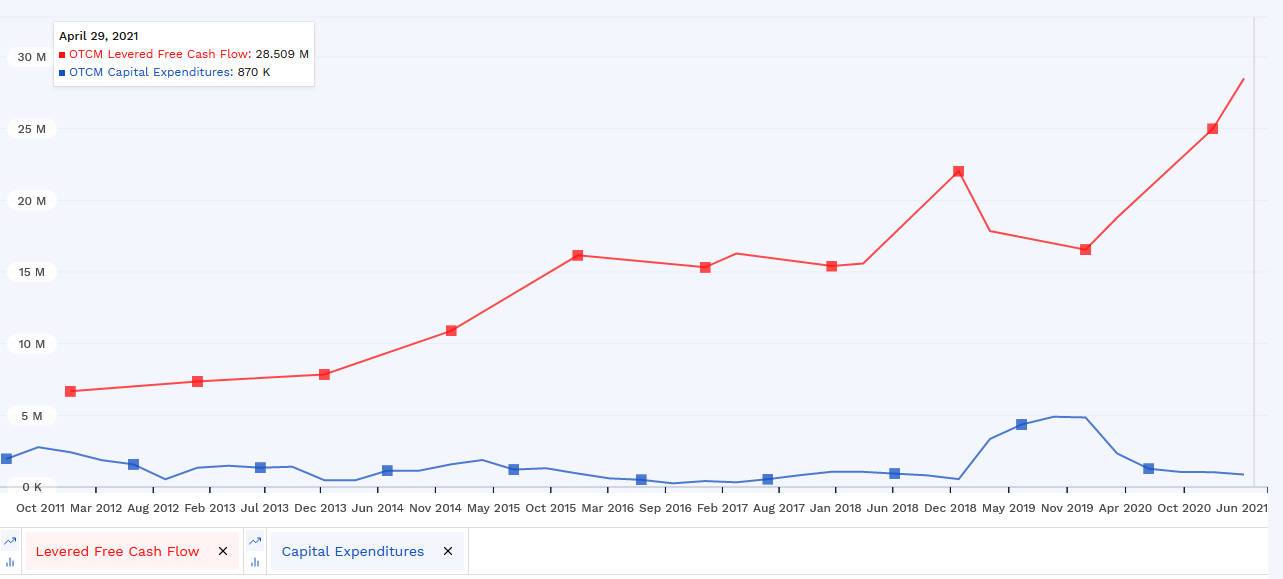

OTCM free cash flow has been very steadily on the rise for the last ten years. This is mostly due to the business being exceptionally capital light. Contrary to a bank, it does not need large capital reserves to back loans and other risky assets. And it does not really own anything in the way of buildings, factories, etc…

With the exception of 2019, when OTCM modernized its IT infrastructure, CAPEX can be almost neglected. Therefore, all of the growing revenues and income are almost entirely converted into free cashflow.

Source: www.finbox.com

To assess the quality of capital allocation, we can look at various rations, like returns on invested capital, equity, and assets.

This capital-light business model has allowed OTCM to have astonishingly high returns on invested capital and equity. Do not let yourself be worried by the drop in the last year in ROI; this was from the very elevated almost 100% to the still very high 40-50%. This is very good ROE and ROI, even by the standard of the asset-light world of IT or financial industries.

Source: www.finbox.com

Categorization and Valuation

Investment Category

OTCM is a typical quality company. It has a very solid moat, and its competitors are rare enough that the worst-case scenario would be its business turning form a quasi-monopoly to an oligopoly, still a situation where the company could keep earning solid margins.

With an ever-growing burden of regulations, many companies will not be able or choose to forgo listing on the larger stock exchanges and be satisfied with the cheaper listing on the OTC markets.

So overall, continuous growth for OTCM seems like a reasonable prospect, and that growth will require little to no capital. So, a worst case scenario would be the company turning stagnant, while growth in income and free cash flow is more likely to be the future of OTCM.

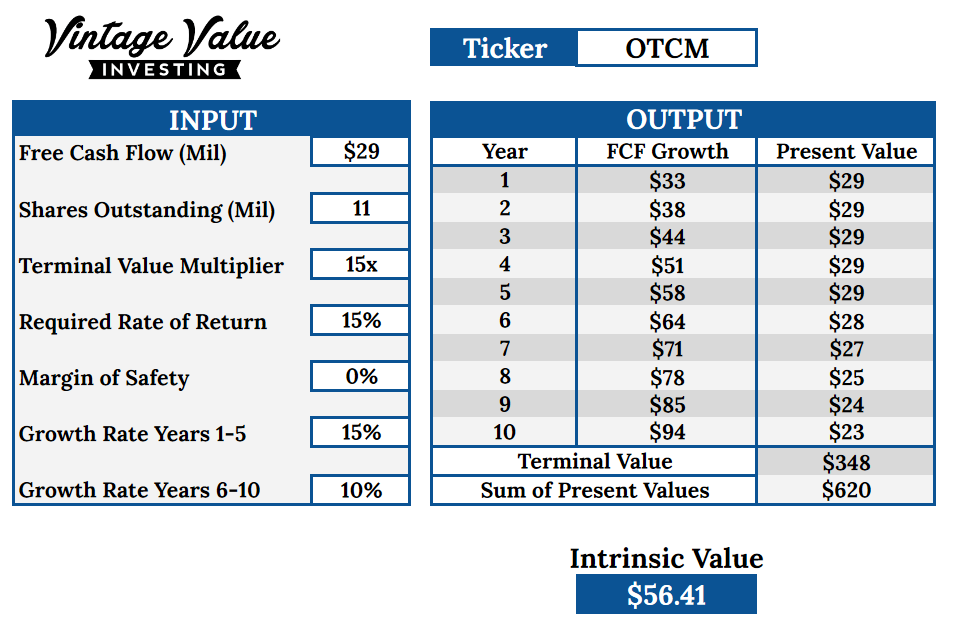

Discounted Cash Flow

Considering the very good and regularly growing free cash flow metric, this is my favorite valuation method for OTCM. Over time, market expectations for the terminal value multiplier of OCTM free cash flow has gotten higher and is around a P/FCF of 18 now.

Even assuming that trading and enthusiasm for investing subdues a bit in the coming years, I think a 15x terminal value multiplier is a safe and conservative enough pick. I also pick “no margin of safety”, considering the size of OTCM’s moat.

Free cash flow has been growing at a rate of 15% annually, and I think this can be sustained in the near future, with a slower 10% expectation for the years 6-10.

Source: www.stockrover.com

This gives us an intrinsic price of $56.41 per share, way above the $46 stock price.

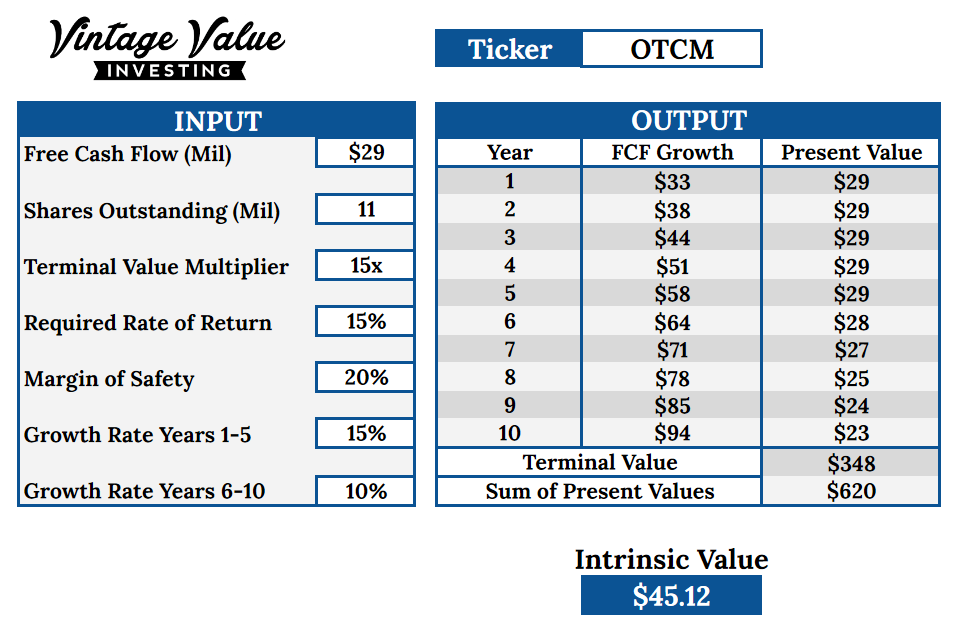

Even with a 20% margin of safety, the company would still be just fairly valued and able to provide a 15% yearly rate of return.

Considering that growth is the largest unknown factor here, I want to see what lower growth would justify the current stock price. If growth crashes from its 15% average to only 10%, the company would still be fairly valued.

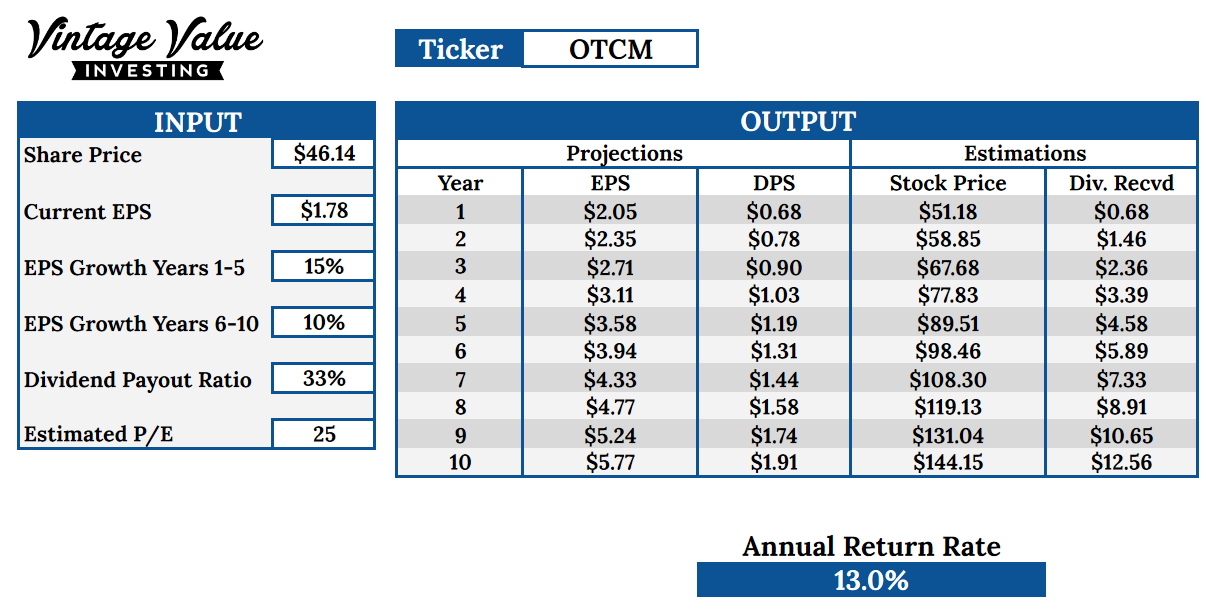

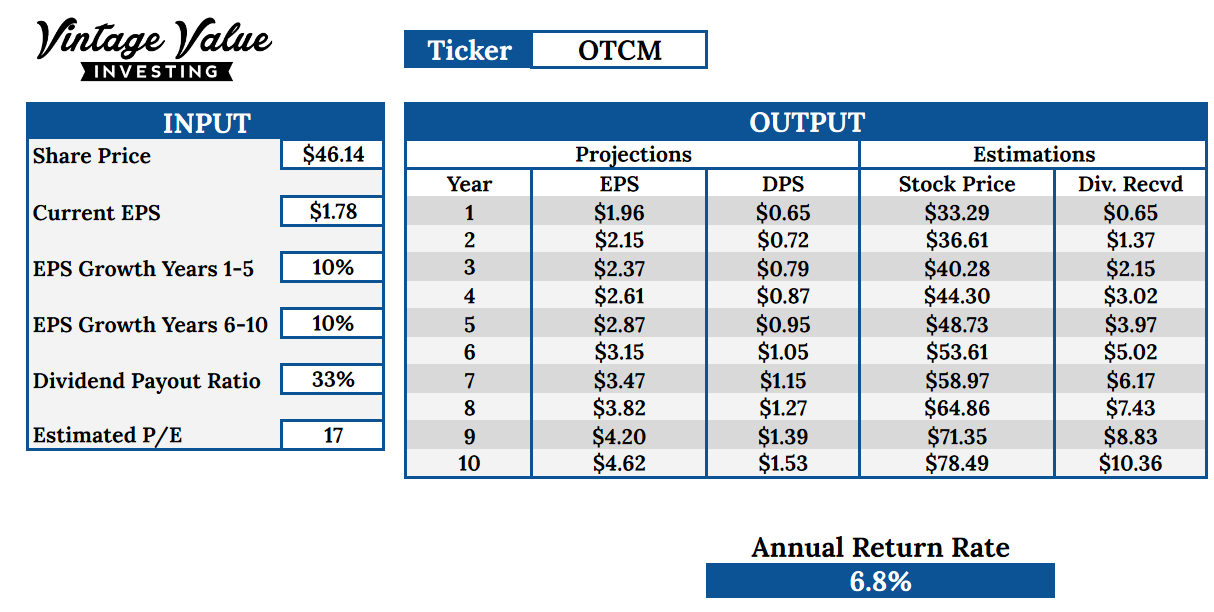

Earnings Growth

Earnings Growth is a method that considers OTCM stock essentially from its ability to grow its earnings over time.

This would give us an expected return rate of 13%, for the previously discussed growth projections and an unchanged current P/E ratio.

It is possible that growth slows down, and this might at the same time affect the multiplier (P/E). In this negative scenario, return rates would fall badly to “just” 7%. Something in line with the broader stock market and indexes, but nothing spectacular either.

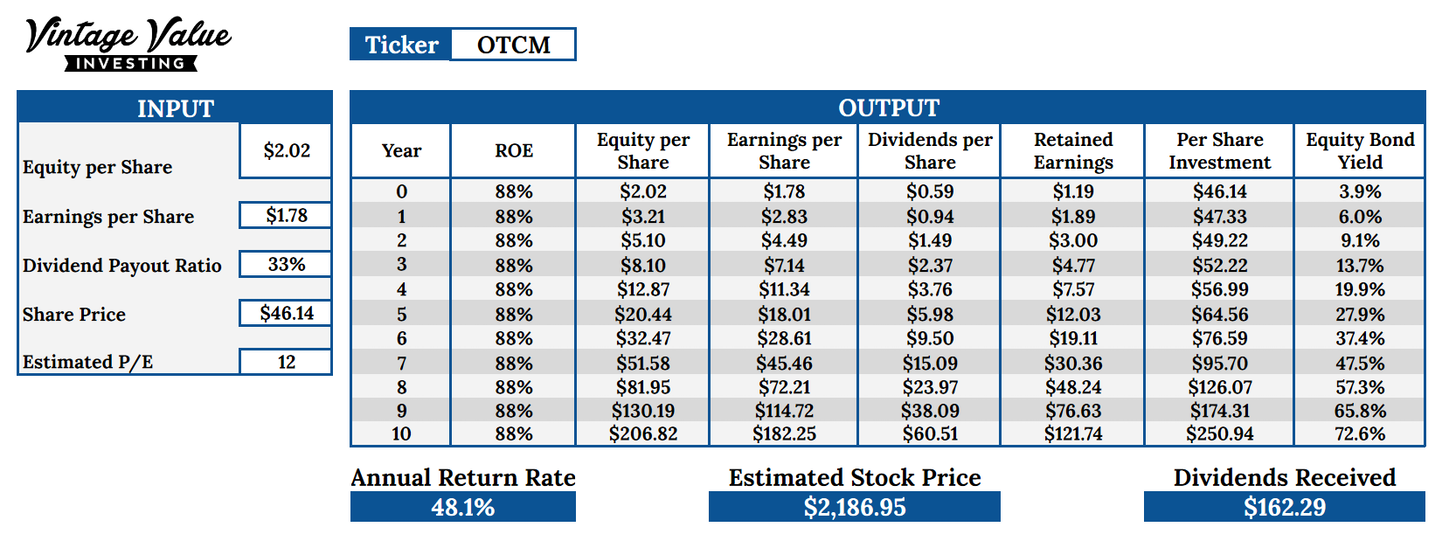

Equity Bond

Equity bond treats the stock like a perpetual bond, and judges it according to its earnings. This is also one method Buffett uses for high quality companies. The criterion to pick a company that fits this method seems fulfilled by OTCM:

Considering the high safety of OTCM, it might be the best way to look at it. The company is unlikely to be pushed into oblivion by competition, and its margins and/or costs are likely to stay rather stable over time.

Due to very high earnings per share compared to the equity per share, potential returns seems very high. The incertitude here is if OTCM can maintain over time this extremely high 88% ROE.

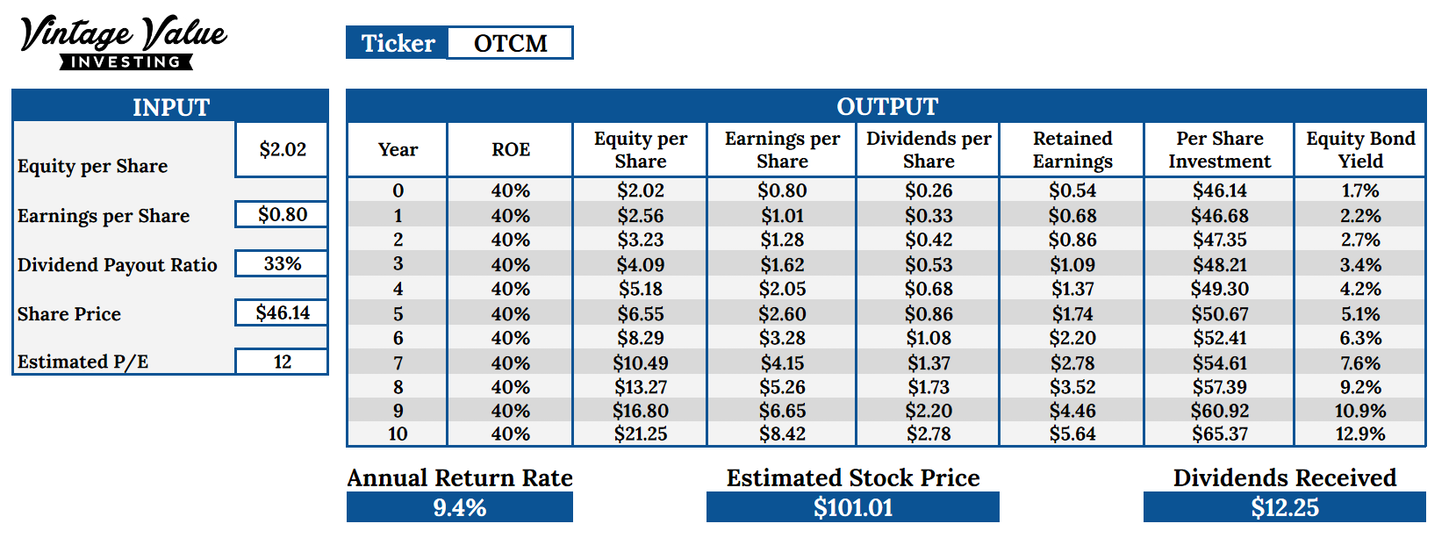

Considering that ROE used above might be too high, I decided to look at the historical value. While OTCM have managed to maintain ROE to 80% or even more the last 3 years, it was a few years ago at the “low” of 40%.

Modifying the earnings to a lower level to get a 40% ROE, the returns should be at 9.4%. Not bad at all to get an almost 10% returns in the negative scenario of earnings being permanently divided by half.

Other Calculation Methods

Considering the incertitude around dividend growth, I decided that the Yield on Cost method would not be useful for OTCM.

Final Assessment

Company Synthesis

As the leader and quasi monopoly of its market segment, OTCM has a large opportunity to be able to keep growing and increase it value, while still distributing some dividends on the way.

The only business risk I really visualize for OTCM would be a market meltdown that would scare off an entire generation from ever trading again, especially “shady/risky” OTCM securities. But frankly, a large historical market meltdown is somewhat of a risk for any stock, so I am not sure if this is something specific to OTCM.

The main actual risk for the long-term shareholders of OTCM is maybe not so many problems with the company but a competitor acquiring it. This would interrupt the company and its investors compounding midway and might be the actual worst that could happen.

How likely is an acquisition to happen? It depends largely on management. I would tend to see OTCM’s management as somewhat greedy, so there is a risk. At the same, would they want to kill the golden goose, instead of steadily collecting $5+Mof paychecks every year?

Maybe when management is 10-15 years older and getting closer to retirement, this might be a risk. But before, I hope they will just stay happy with their oversized compensation and not ruin it for the other shareholders. Now that I come to think of it, this might be the only advantage of management’s large salaries, bonuses, and stock options.

Valuation

Valuation methods gave very different results, indicating how difficult it is to actually value long term compounders. Most of the money is made toward the later years when incertitude is the highest. No one could have precisely calculated the 2021 valuation of Amazon in 2000. But at the same time, staying for the whole time would make most investors not care to have gotten it wrong.

So, you might be reasonably convinced that a minimum of 7-8% long-term return is safe, but how high can it go on the upside? Is it 13%, 20% or 48%? No one really knows.

Due to the necessity to have patience and wait for quality companies like OTCM to slowly compound over time, the stock should be a true Buy-and-Forget investment. One virtually never sold as long as the moats are solid, no matter what the short-term fluctuation in share prices are. Easier said than done.

The graph above is just a reminder, the historical prices have known some serious draw-down periods, and the recently aggressive rise might be followed by a slump. Or not.

It is really impossible to say. Any buyer of OTCM will need to prepare himself to hold on for the long run, and maybe not even look at the share price, and just enjoy the effect of strong return on capital and equity over time. This also means investing only money you would be absolutely sure to never need in the next 5-10 years.

If history is any indication, OTCM could be a 10-bagger (again), or even bigger than that if increasing regulation push more companies to list on the OTC markets.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in OTCM and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.