Changes in currency value can have a durable impact on an economy’s performance. For example, changes in the dollar value are among the major root causes of regional crises like the 1997 Asian financial crisis or the 1980s Latin American debt crisis.

Changing currency parity is also something investors in foreign markets need to keep in mind. It is worth paying attention to when a major currency loses value very quickly, it is worth paying attention.

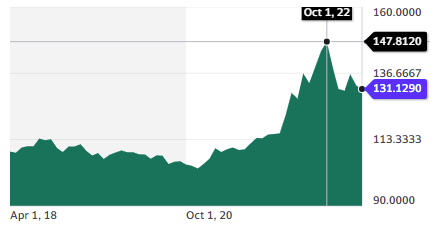

The Japanese Yen has recently experienced such an episode, going from almost ¥103/USD in December 2020 to a low of ¥147/USD in October 2022. The Yen has recovered a little since but is still at a 20-year low point. 20%-50% moves between major world currencies are very rare events.

Why Did The Yen Fall?

Part of what shocked the financial market was the speed of the currency’s movement. In less than 6 weeks, the yen’s value against the USD lost more than 10% from ¥115 to ¥125 and kept falling.

So what triggered it?

It was a perfect storm of factors:

- The Fed raised rates quicker than the Japanese central bank.

- The US economy grew faster than the Japanese economy.

- Rising energy prices eroded the Japanese trade balance end competitiveness.

- The dollar gained strength against almost all the world’s currencies.

Some of these causes have since weakened, explaining the partial recovery of the Yen. Energy prices, in particular, have moderated. But this is unlikely to be over.

The unfolding banking crisis stems largely from older government bonds losing value as interest rates rise. It’s difficult to sell older bonds with low interest rates when newer bonds with high interest rates are easily available. That means that the immediate value of older bond portfolios drops rapidly.

This hurt banks that were holding large parts of their reserves in longer-term bonds. Japan has held rates low for much longer than any other country, and the ongoing rise in interest rates by the central bank of Japan is likely to cause similar effects.

Without going into a deep macroeconomic discussion, we can say that, in general, inflation with a high debt level is generally negative, especially if the central banks have to raise rates to fight inflation. And Japanese inflation finally picked up: “Japan CPI inflation hits 41-year high in Jan as BOJ changes loom“

So if this setup can cause bank failures in the US or Switzerland, Japan might be at risk as well.

Overall, while certainly not spelling total doom for the yen, the current trends are likely to keep the yen weakened against the dollar for a long time.

Economic Consequences

For the rest of this article, we will consider a Yen that stays weaker than in 2020 or 2021. This is not a “doomsday” scenario. just a weaker Yen staying at the current levels or a little lower.

The primary effect of a weaker currency is that imports become more expensive and exports become more competitive. This is because if a product is priced in yen, but sold in dollars, its export price suddenly goes down 20%-30%.

This is more than the average margin of most industries, making Japanese products suddenly more competitive.

The same phenomenon affects tourism. Hotels, restaurants, and entertainment in Japan, if measured in euros or dollars, are suddenly a lot cheaper.

Or, as the Hokkaido Backcountry Club put it:

Attention guests, we are confident that the borders will be open by next winter. This is the time to book your trip. The yen has never been weaker, and your dollar will never go further.

Hokkaido Backcountry Club

Investing Takeaways

Because the change was so sudden, the business models and supply chains have not adjusted to it yet. This means shareholders in Japanese companies and investors need to prepare for a few changes.

The Risks

- Japanese companies relying on imported goods or services: If a local company sees all its suppliers’ prices in Yen increase overnight by 20%-40%, this can devastate their margins.

- Energy-intensive business models: Japan is very dependent on imports for its energy supply. While the country is looking at restarting nuclear power plants, this will still hurt a lot of power-hungry manufacturing businesses.

- Heavy dollar-denominated debt: Any Japanese business with a lot of dollar debt will struggle, as the yen cost of the debt suddenly went up 30%-50%. This is probably not a common case, but it’s something to keep in mind.

Opportunities

There are also beneficiaries of the yen’s decrease in value.

Japanese Exporters

With exports cheaper, Japan’s robust export economy should be able to capture more market share abroad. But this is true only for a limited set of Japanese exporters with the perfect trifecta:

- Producing in Japan: they will benefit only if the costs are in yen.

- Not exposed to energy prices, so nothing like metallurgy or car-making, for example.

- Not needing to import raw materials and commodities priced in dollars.

Software companies and other asset-light companies that are not energy intensive would be best positioned to gain.

Tourism

The combination of re-opening post-Covid and cheaper prices in a period of global inflation is a powerful one. Tourism companies catering mostly to Westerners would be ideal, to not be exposed to possible geopolitical tensions with China.

Manpower-Intensive Industry

With Japanese workers suddenly cheaper relative to their international counterparts, a business model where human input is crucial will get more profitable. Again, this is true mostly for exporting companies.

Real Estate

Real assets denominated in dollars are on a discount from the yen fall. In addition, Japanese real estate is overall less pricey than most of the developed world markets, after the crazy 1980s bubble. The topic was discussed further by fellow Substack writer Rei Saito at KonichiValue.

“Friend-Shoring”

Tensions between the USA and its allies and the Eurasian powers are not getting better. Just look at the looming TikTok ban in the US and the recent visit of Xi Jinping to Russia. Japan could be a beneficiary of relocating supply chains out of China. Especially for tech segments high on automation and requiring a lot of technical talent, like semiconductors, batteries, renewables, etc.

A Few Companies to Look Into

Nintendo

This is one of the first ones to come to my mind, as this is a company we covered a while ago in the summer of 2021. Nintendo will soon be testing its ability to monetize its abundant and beloved Intellectual Property (IP) beyond video games, with the Super Mario Bros movie coming into cinema in a few weeks.

Nintendo fits the bill of an exporting company, with a large part of its profits made from human intellectual labor in producing software and unique IPs. This does not apply as much to its physical console production, but even these are not highly resource-intensive.

The cherry on the cake? Nintendo should also benefit from international tourists finally being able to visit the Nintendo Theme Park in Japan, which opened during Covid. Two other theme parks will also open, first in Hollywood in 2023, and then in Orlando in 2025.

Japanese Trading Companies

Also known as “Sogo Shosha”, they are some of the key intermediaries between Japanese SMEs and international markets. You can read more about the complex history and evolving business model of Sogo Shoshas in this article by fellow Substacker Value Punk.

Always one step ahead, Warren Buffett invested in these companies in 2020. Buffett’s investments were in Mitsubishi Corp. (MSBHF), Mitsui & Co. (MITSY), Sumitomo Corp. (SSUMY), Itochu Corp. (ITOCY), and Marubeni Corp. (MARUY). Follow the link for a summary description of each company.

These companies are shrouded operators that are likely to find ways to benefit from an export boom. Many of these companies are likely to benefit from the “friend-shoring” trend mentioned above.

If you prefer not picking a winner but putting a bet on Japan exports in general, following Warren Buffett’s footsteps can be a simpler option than stock picking.

Tourism

This is not a sector I’ve explored much in the past, so this is just a suggestion to look into by yourself. By searching the most valuable hotel companies in the world by market cap, one Japanese company stands out:

OLC Group (Oriental Land Company) is apparently the largest hotel company in the world. It mostly manages Disney resorts and theme parks in Japan. It could fit the bill of being focused on Western tourists. Still, a potential red flag could be a very high P/E at 107.

Another option could be Seibu Holding, a group managing a chain of hotels all over Japan, as well as railways and bus lanes. It recently had to sell 1/3 of its hotels to gather cash post-Covid. But the remaining portfolio of 45 hotels and leisure locations and touristic network might still be interesting with a current P/E of 4.5.

Conclusion

Japan has been out of favor with investors for almost 3 decades now, and demographic decline and a stagnant economy have given it a bad reputation.

But it is also a very beautiful, modern, and productive country. And the tides are turning if we are to judge by Warren Buffett finally investing in the country for the first time in a 70-year-long career.

Investors need to distinguish “the Japanese market” from specific opportunities. Currently, Japanese exports have a chance to shine from the yen devaluation. In addition, it also benefits from the rise of automation (negating worries about demographics) and the need to relocate supply chains to “friendly” countries.

The key will be to focus on well-capitalized and profitable companies to buffer any banking crisis risk. And to find the right mix of exposure to cheaper exports, but little exposure to rising import costs.