August 21st, 2021

Quick Stock Overview

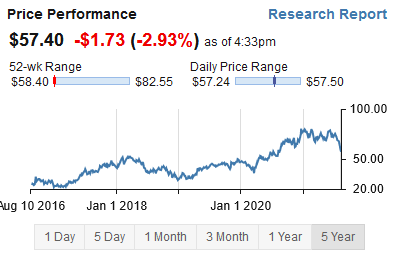

Ticker: NTDOY

Source: www.stockrover.com

Key Data

- Sector: Communication Service

- Sales ($M): 15,962

- Industry: Electronic gaming and multimedia

- Net Cash per share: 16.46

- Market Capitalization ($M): 54,557

- Equity per share: $17.84

- Employees: 6,574

- P/E: 12.5

Investment Thesis

The Hidden (Investment) Gem of The Gaming Industry

Video games have slowly evolved from kids’ entertainment to a large part of the culture. This mostly followed the first generations of gamers getting older and now having families of their own. This was especially visible after a year of lockdowns, with plenty of time to play at home. The gaming industry revenues were up to $159B in 2020, a 9.3% year-to-year growth.

Most of the industry news is dominated by blockbuster AAA games and headlines about the comparative performance of the latest consoles or PC hardware. Deeply rooted in the industry since its inception, the arms race for bigger virtual worlds, better graphics, more complex games is still ongoing.

Gaming is a highly challenging industry, where yesterday’s winners can be outpaced by their competitor’s technical innovations. The sector is littered with the leftover of former industry leaders: Atari, Commodore, Sega, Westwood studio, etc… And were bigger, quicker, and prettier = better.

It is also a field where hardware manufacturers like Sony (PlayStation) and Microsoft (Xbox) subcontract the costly and risky process of game development to third parties. These developers and publishers enjoy the ability to publish their games to all platforms technically able to support them, broadening their market.

But there is one company defying the odds and industry best-practice, betting on cheaper, lower performance hardware. It is also developing almost all its key games internally and outright refusing most third-party developers to use their consoles.

This company is, of course, Nintendo.

Nintendo is one of the most beloved companies by gamers, and also one of the most misunderstood by investors. Recurring comments about the company for almost a decade are things like “highly cyclical”, “archaic management”, “missed the opportunity”, “unable to adapt”.

Due to these widespread misconceptions, this report will be much more focused on a qualitative analysis than the financial numbers or the short-term news. These misconceptions lead investors to miss a great opportunity, as the stock went from its low of $12 in 2015 to its highest ever in February this year, at $81. An x6.75 performance in 6 years is really nothing to be ashamed of.

But is this similar to what the company did in 2008, before going through 7 rough years? I think a lot has changed within the company since 2008, as they are an entirely different company since then.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Chapter 1: Understanding Nintendo

Cyclical? Yes, but Not Only

The console market is notoriously cyclical, especially at the level of individual companies. A new console gets released, a lot of sales happen the first and maybe the same for second Christmas, and then a more or less slow decline happens. It is also common that “a winner” emerges for each console generation, leaving its competitors in the dust.

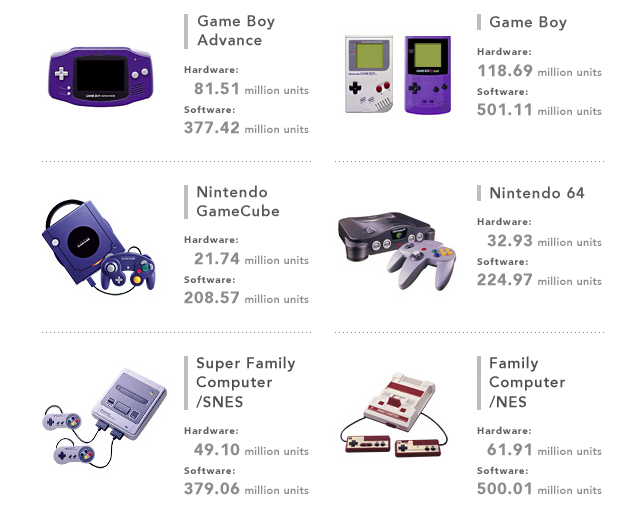

Nintendo is the poster child of this pattern, with an almost perfect track record of a super successful console launch followed by a relative commercial failure for the next model. The GameCube disappointed after the N64, the Wii U was a disaster after the gigantic success of the Wii.

And the successor to the Wii U, the Nintendo Switch is a large success, almost the largest in Nintendo history (for now, the Wii still holds this title, probably not for long). After releasing a Switch lite last year, a Switch OLED is planned for October 2021, with more memory and a better screen for just $50 more than the base model.

There is no hiding from it. After the successful Switch console, a shadow of historical failure looms over Nintendo near future. Here’s the good news:Nintendo is very aware of this fact.

Nintendo has been around since the late 19th century, an it has not survived that long by being careless. When it hits a home run, the company has a habit of stockpiling that cash for leaner years. It is now sitting on no less than $10.7B. While this might look like poor capital allocation to some, this might be highly reassuring for the cautious or worried investor.

Nintendo management is perfectly aware of the risk entailed by this model. If failure would succeed more than 2 or 3 times in a row, the whole company could be toast. I think that the company is now able to break away, at least partially, from this cyclicality, but I will come back to this point later on.

Until recently, the solution was a mix of radial innovation and perfectionism, and it worked. As you can see above, every single one of the new Nintendo consoles was a radical departure from the previous one. Each had a different design, control system, etc… Just compares it to the competition of PlayStation and Xboxes, can you feel the decision-making by corporate committees?

Source: www.gamespot.com/

Source: www.gamasutra.com

The Power of Corporate Culture

With no other company I reviewed, understanding corporate culture was so important. Culture is often a way to pretend things about a company, how caring it is, how sustainable, or whatnot. But with Nintendo, the culture permeates everything, and I will keep coming back to it in this report.

As I see it, it relies on a few pillars, beyond the cult of perfection I already mentioned:

A Family Company

Most other gaming companies are focused on giving their consumers an adrenaline rush. Bigger guns, more explosions, more gore, more intense experiences are always better; and then there is Nintendo.

Nintendo has built its entire branding around being child friendly. This is especially key now that parents know more about video games having been gamers themselves. It will include some games that are more “adult” focused, but mostly, its target audience is 5-14 years old.

Most gamers will have fond memories of their Nintendo games and are now transferring them to their children. Their children might want more action-oriented during their teenage years but are still likely to want to share Mario, Zelda, and Metroid with their own children down the road.

The lower pricing and less high-grade performance make a lot of sense in that light. Nintendo does not need to have the best visuals to impress teenagers and young adults, just the best games for the children. And families are usually on a much tighter video game budget than single young adults.

A Cult of Perfection

The other key element to Nintendo’s culture is a cult of perfection. A central person in Nintendo resumed it perfectly, Shigeru Miyamoto, the creator of both Mario and Legend of Zelda, two of the largest and most enduring Nintendo’s franchises:

“A delayed game is eventually good; a bad game is bad forever”

The important part is not the focus on quality. It is that a delayed game WILL be good. It is simply not an option to cancel it, for example, a very common industry practice.

The product will be perfected until it is good. Period.

Virtually no matter the costs or effort required. Shareholders and gamers waiting for sequels be damned, it will wait until it’s good. Fans of the Metroid franchise might get a new game this fall, after 19 years without any new opus.

The consequence of this obsession for quality is very tight control. Most of the games on a Nintendo console are made by Nintendo. It was not always that way, but a stream of bad games in the 1990s consoles left the company permanently convinced that having ONLY good games means doing the job by themselves.

Third-party developers are rarities and on an invite-only base. And in return, other consoles cannot access Nintendo exclusives. In addition, the latest and fanciest graphics would struggle on the weaker and cheaper Nintendo consoles.

So, Nintendo is not so much part of the industry as an isolated island with its own separate ecosystem.

A Consumer-Friendly Policy

While console and PC gaming has traditionally focused on graphics, virtual world size, and technical performance, another branch of gaming took a different direction. Mobile gaming has used the smartphone revolution, building the industry on the super-fast computers everybody already has in their pockets.

The problem of mobile gaming is attention retention. A PC or console gamer is likely to stay on his game solely focused for hours in a row. But smartphone games compete with all the other apps like news, social media, email, messages, etc.

The logical evolution was to make mobile games as addictive as possible. Most of the techniques used by the mobile gaming industry have been first discovered and used by the gambling industry: dopamine rush from regular mini rewards and “wins”, the randomness of success, unpredictable rewards, and increasing difficulty. So then, it is probably not a surprise that some of the best-selling mobile games look not-so-different from slot machines.

Source: www.theguardian.com

This led mobile gaming to be, exactly like casinos, highly dependent on “whales”, the rare players that spend more than all other players combined. Commonly, 1-5% of all players make up for 90-95% of revenues in this industry. While 0.1-0.5% players representing half of a game’s revenues. Considering very high acquisition costs for a mobile game, this makes squeezing as much money from whales an absolute necessity.

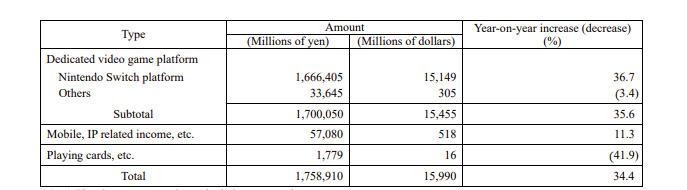

Nintendo has notoriously “failed” at mobile gaming. It is not even displaying mobile separately from its other IP-related income in its annual report.

Source: www.nintendo.co.jp

And the reason for this failure is obvious. The company literally said, “It does not want its users to spend too much on mobile games.” Can you imagine the head of gaming at Sony or Microsoft worrying about users spending too much?

But this makes perfect sense for Nintendo. Mobile gaming is using highly predatory and manipulative practices. So much that the leader, Tencent, is now getting threatened by the Chinese government to rein in such practices.

Adopting such methods would contradict everything the Nintendo brand stands for. High-quality games, affordable fun that family can trust to build a multi-generational bond. Not just a corporation, but a friend.

Just one child spending once $7,500 on a Nintendo mobile game would be a PR disaster.

For the same reason, Nintendo does not make pay-to-win games, where your credit card determines your in-game success. It also does not chop games into parts, selling the core first, and then all the rest in expensive DLCs. A practice so common and so hated by gamers that it is now integral to the brand of the largest video game companies, first of them EA (Electronic Arts).

The internet is full of memes mocking the practice.

Chapter 2: The Iceberg Company

The Richest Untapped IP Resource in The World

Nintendo’s most visible section is the console business. But a lot more of it stays immersed and invisible to the casual observer. Having been the center of so many childhoods, Nintendo is sitting on a stash of beloved IP like few other companies. In that respect, the comparison should be done more with Disney than with Sony or Microsoft.

And so far, this resource has essentially been unused. Video game IP has been used to make … more video games. And not even that many of them. One Zelda game every 3-5 years (just 18 games in 3 decades+). A Mario or Pokémon every 2-3 years. And sometimes, beloved IP either went for a 19-year hiatus, like Metroid, or simply got left behind, like Starfox, Kirby, and many more.

Switch users are the first ones to see a change in that behavior, with Nintendo now using long-time gamer’s nostalgia. Nintendo has notably successfully released a remake of Link’s Awakening, a legendary title initially released on Gameboy decades ago. A 5-game pack for Mario’s 35th-anniversary campaign, plus a few other beloved and never forgotten titles from the 1990s and early 2000s.

This is exactly the demographic matching 35-40 years old buyers, looking for a console for their kids.

So, an improvement on the games front, but still, no movie, no TV series, no cartoons, no licensed games, and not much merchandising. You need to understand that Nintendo has not always been hostile to letting other parties use its IP. But it usually went horribly wrong.

There was the disastrous 1993 Mario movie. Or the hideous Zelda cartoon, that people are still making fun of these days, together with some terrible games by third-party developers.

These failures have left a mark on the company culture, and it took a while for anyone to convince management to try it again.

And this is finally happening. A new Mario movie is planned for 2022, after the success of Detective Pikachu. Finally, the company is opening more than one retail shop for merchandise. And more importantly, a series of theme parks is being created and managed by Universal. Now people can go to a section of the Universal park that is very much like the Disney World parks, but all Nintendo themed.

Another one is planned to open in Orlando, but with Covid delaying everything, it might takes a few years to open. Other opening are also planned for Hollywood Universal park and Universal park in Singapore.

It is very hard to overstate how much potential Nintendo has unused so far. Markets have realized the potential after Disney went on a purchasing spree with Marvel and Lucasfilm (Star Wars) and turned relatively dormant IP into cash machines. The success of Detective Pikachu or the Witcher and the Castlevania Netflix series prove that video game adaption to big and small screens is not anymore “cursed”.

So I think, it is unlikely that deals as “low” as the $4B sales each for Lucasfilm and Marvel would happen today. In the long run, I would not be surprised that a large, diversified, and all-public IP like Nintendo’s could be worth anywhere between $10B-$20B alone. This would include the tens of games and evergreen success franchises of Legend of Zelda as well as Mario. Or the frequently updated and ever popular Pokémon. But also, a lot other well known by gamers, like the sci-fi action shooter Metroid, the kid-friendly Kirby, the futuristic high speed licenses of F-Zero and Star Fox.

Truly, Nintendo has nothing to envy to the endless pool of Marvel superheroes.

Licensing IP is very likely to become a steadily growing part of Nintendo in the future. It is likely to be a lot slower than investors would expect with the Disney template. But it is also certain to not risking killing the entire license like the last three Star Wars movies almost did.

If Disney is the hare, Nintendo is the turtle; and we know who wins at the end.

The Countless Growth Potentials

Beyond IP licensing, there are so many possibilities for Nintendo to grow revenues and profitability that it was rather difficult to organize. Among them are some many analysts mention, but that I personally think unlikely to the company’s culture. I will review each and give a synthesis at the end.

AR/VR gaming

This is likely the largest near-term new segment for Nintendo to expand into. One of the most successful AR games to this day is still 2016’s Pokémon Go. The game was developed by Niantic and the Pokémon company. The actual ownership of this by Nintendo is frankly a tangled mess, so let me explain as briefly as possible.

Nintendo owns fully the Pokémon trademark, giving a lot of control over it. However, from a financial point of view, the license is managed by the “Pokémon Company”, owned 33% by Nintendo. The other owners also have a third each and are “Creature” and “Game Freak”. But in practice, Nintendo is likely to own part of these companies, rising the actual ownership of the Pokémon company higher. As these two others are private companies, Nintendo does not disclose the exact numbers of its ownership, thanks to Japanese markets rules. My guesstimate places Nintendo’s real ownership of the Pokémon Company around 50-60%.

Now back to Pokémon Go. The game itself was actually developed by Niantic. Niantic is a spin-off from Google, focused on developing tools to develop Augmented Reality (AR) solutions. It is also largely owned by Nintendo, for a number anywhere between 20-40%.

Pokémon Go is owned equally by Nintendo, Niantic, and the Pokémon company. So that should make something in the range of 33%+11%+16%=60% of Pokémon Go belonging to Nintendo in total.

Where game developers for PC use massively Unity 3D, AR developers rely on Niantic’s tool, the Niantic Real World. So, Niantic and Pokémon Go are really to be compared to Epic Game and Fortnite. Epic Games is a $29B company and Niantic was valued at $4B two years ago.

Considering the extensive portability of the Switch, something that Nintendo seems to plan to keep for future consoles, a fusion of future games and Niantic technology is likely on the horizon. It might take a little bit longer but would solve the problem of poor controls on smartphones that have hindered the progress of AR so far.

So, I assume that Pokémon Go is the first in a long series of games exploiting the potential of Nintendo in AR.

New Consoles

It should be obvious, but one way for Nintendo to keep going strong is a successful new console after the Switch. It is now releasing the Switch OLED in October (an upgraded version of the Switch, following the Switch Lite some time ago).

Will the successor of the Switch be a victim of the historical hit-and-miss pattern? It is entirely possible, as Nintendo never stopped taking risks in new control and console design, with unequal results. But I believe the ability of the Switch to replace both the failed Wii U and the successful Nintendo DS shows that Nintendo got better at understanding its user’s expectations. And if the next one fails, the one after should correct the mistake (hopefully).

Retail Stores and Collectibles

Nintendo communicates remarkably poorly on its dedicated stores. After some research, I think I managed to find a grand total of four Nintendo stores, one in Japan, one in Israel, and two in the USA (In New York and Redmont).

For a license with so much potential in the sale of an infinite variety of collectibles, mugs, apparel, and other goodies, this is astonishing.

Source: www.tokyoweekender.com

Of course, Nintendo branded merchandising is available in other places. But the fact that so many avid fans cannot visit a dedicated shop without traveling thousands of kilometers show how neglected this opportunity is. I think the company could easily open 10-50 more shops, basically one per large metropolis, and still be far from saturating the market.

Relaunch & Remaster

The exceptional success of Link’s awakening remake and the Mario pack on the Switchshows the strength of nostalgia. And Nintendo is now acting upon it with notably a release in 2017 of an NES console, back from the 90s.

Not much R&D involves, just repacking old games with new cheap hardware. 4 million copies sold in a year. Not bad…

For people in my generation, a re-release of a Nintendo 64 could be worth forking $100-150, just to remember times with friends, or sharing it with their own kids.

Remasters of games is also an option. Basically, it means taking an old and now ugly game, keep the beloved level design and the gameplay, but upgrade the graphics and improve little details. On PC, the large successes of Age of Empires 2 multiple remasters, or the C&C series prove the existence of a large market. The larger the catalog of such title, the larger chance to turn nostalgic gamers into buyers of the Switch.

IP Purchases and Console Opening

As I said before, Nintendo has a long history of closing its console to outside developers, to preserve quality. But since the 90s, the industry quality standards have evolved for the best. And the tens of millions of consoles sold are a solid argument for developers to look for Nintendo’s approval to publish on the Switch.

In parallel, some PC games have become a must-have for a children-focused console and have been incorporated into the Switch catalog, like for example, Minecraft. I expect an increasing presence of selected third-party games in the Nintendo catalog, especially coming from the PC gaming world. This will increase the sales of new games, but also make more attractive the purchase of a Switch in the first place.

Could the company acquire directly more licenses or game developers? Possible, but as it has not been done in the past and considering Nintendo conservatism, I would not wait for it.

Digitalization

Almost a decade late, Nintendo has finally adopted the method to have user accounts for people to register their games and their consoles. This allows users to keep ownership of what they bought even if the initial machine or disks are lost or damaged. It also encourages people to directly purchase online, a much more seamless experience than having to physically go to the shop to buy a physical game.

Console gaming has always been a bit late at that, but the example of PC gaming, where virtually every game is available for download on Steam or the Epic Game store show this is the way forward.

Now many investors seem to think this will open the way for Nintendo to start selling more DLCs, more unique in-game items, and so on. Personally, I think hopes of digital sales boosting revenues per user is a pipe dream. It might improve things a little at the margin, but remember, Nintendo does NOT want people to spend too much on a game. The company is focused on keeping people coming back in 5, 10, and 20 years, not squeezing money, as much as possible and right now. And it’s a good thing.

Other Ownership

Nintendo also has partial ownership in other companies. The first one is DeNa, a mobile game developer, the 10% Nintendo ownership is worth $217M.

The second is Bandai Namco, with a 1.75% ownership by Nintendo. Bandai is a private company, but it is estimated that Nintendo holdings are worth around $171M.

More surprising, Nintendo also owns 10% of the Seattle Mariners. Hard to tell again the real value, it is likely to be something around $140M-$300M.

Conclusion About Growth Venues

It is easy to lose track of all the extra things Nintendo does or could do on top of gaming consoles. As I see it, the three most important are the AR gaming potential, the theme parks, and cinematic adaptation.

The first one via Niantic gives Nintendo a lot of control over the leader of the most promising sector in video games. I can totally imagine one day seeing Nintendo smart glasses, powered by Niantic, allowing to play games in the real world seamlessly.

The theme parks have another role in Nintendo strategy, in providing a reliable steady stream of income in an otherwise very cyclical business. Reinforced fans’ loyalty and extra venues for selling merchandising will not hurt either. Letting Universal manage them is probably a good choice, or else it could become a distraction for the company’s management.

Finally, the incoming Mario movie, the potential for a Metroid sci-fi series or an action-adventure Zelda movie cinematic universe is simply unparalleled except by a handful of corporations like Amazon (now owning MGM as well as Lord of the Rings and the Wheel of Time IP) and Disney (including Star Wars and Marvel). I think this growth project could if properly managed, single-handily be worth as much as half of the current Nintendo.

Contrary to Disney’s frenetic and uncoordinated stream of releases, causing quality issues, I will be worried that Nintendo will be too cautious instead. I suspect it will take much longer for it to fully realized its full potential, but also will have a much more enduring impact, instead of risking to alienate long-time fans and damage the IP value.

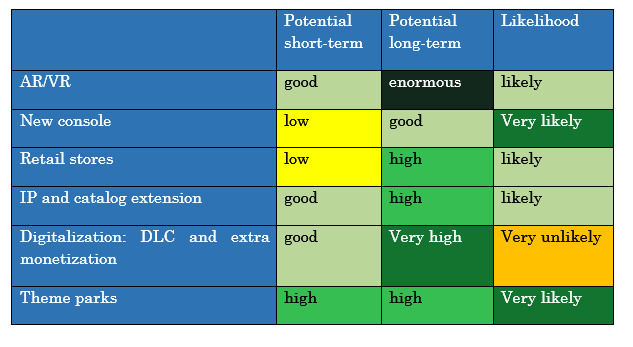

There are many value creation opportunities here for Nintendo. In order to visualize this, I have created the chart below.

Overall, I like what I see here. I think that all the things that Nintendo is attempting to do with their IP can be incredibly valuable for the company, and its shareholders. The likelihoods of the outcomes are also high, in my opinion.

The biggest risk for Nintendo will be management’s mindset shift. They are very fiscally responsible, so risk of severe loss is limited.

Chapter 3: The Future

Competition

In this report, I mostly glossed over Nintendo’s quality and potential. It is however not without competition. I think that other consoles, namely PlayStation and Xbox are not actually much of direct competitors. Their price range, their offer, and their consumer target are simply too different. Similarly, Apple and Android phone gaming is a completely parallel universe, to the antipodes of Nintendo’s value and positioning.

Much has been discussed lately about the “Switch-like” console planned by Valve for this December. Will it manage to threaten Nintendo’s dominance on the low-price portable consoles?

Maybe, but I doubt it. The main advantage of Valve here is too also owns Steam, the central point for 95% of PC games publishing.

I also think this is the main disadvantage. Most PC games are not designed for a console system, either because of performance or controls issues. Shooters are better with a keyboard, and strategy games without a mouse is a stupid idea.

I struggle to understand what this console will do that a separate controller and an HDMI cable between the PC and the TV cannot do.

If anything, I see this device possibly competing with Xbox and PlayStation for its portability, but that’s all. Add to that the abysmal track record and reputation of Valve with hardware, and I would not worry too much.

In the longer run, the entry of Amazon or Google, with a full streaming offer might be a bigger threat to all the existing actors in the industry. With faster bandwidth, it might become possible to simply let these cloud servers run your game calculation and simply connect online, without buying any console or high-end PC.

Google tried it unsuccessfully with Stadia, but over time, I suspect this will be the future of gaming. Then, the extreme conservatism of Nintendo and its insistence on making its own hardware might hurt.

But by then, I think the proper usage of the IP will have completely changed the company.

The Financials

As I said, I will not look too deep into the quantitative aspect here. But is still good to have in mind the key numbers of the company.

The company made $16B in revenues in 2020, most of it overseas. This resulted in a profit after taxes of $4.3B.

Debt is at $417M, almost non-existent compared to a cash cushion of $10.7B.

The P/E ratio is at 13.3, and price to free cash flow is at 9.9. The dividend yield is at 4.5%. Overall, the market is not pricing Nintendo for future growth and cling to the idea of an outdated, cyclical, and capital inefficient company.

The last quarter has just let some believe these fears were founded, with disappointing results in Q1. I think this is a mix of several factors: a post-Covid cooldown in sales, plus some supply issues with the semi-conductor shortage, combined with no major game release in the quarter. The October release of the Switch OLED should help alleviate any short-term weakness and ensure a good Christmas season.

Nevertheless, Nintendo seems to consider its share price undervalued, with a repurchase of 1.5% of the total shares planned in September. Together with the comfortable dividend, it does not seem like a company unwilling to give cash back to shareholders once the cash cushion for lean years got big enough.

With cyclicality likely to decrease in the future, I consider that a part of the very negative net debt (-$15B on a $54B market cap) should be removed from the company market cap to get the “real price”, probably $5B to $10B.

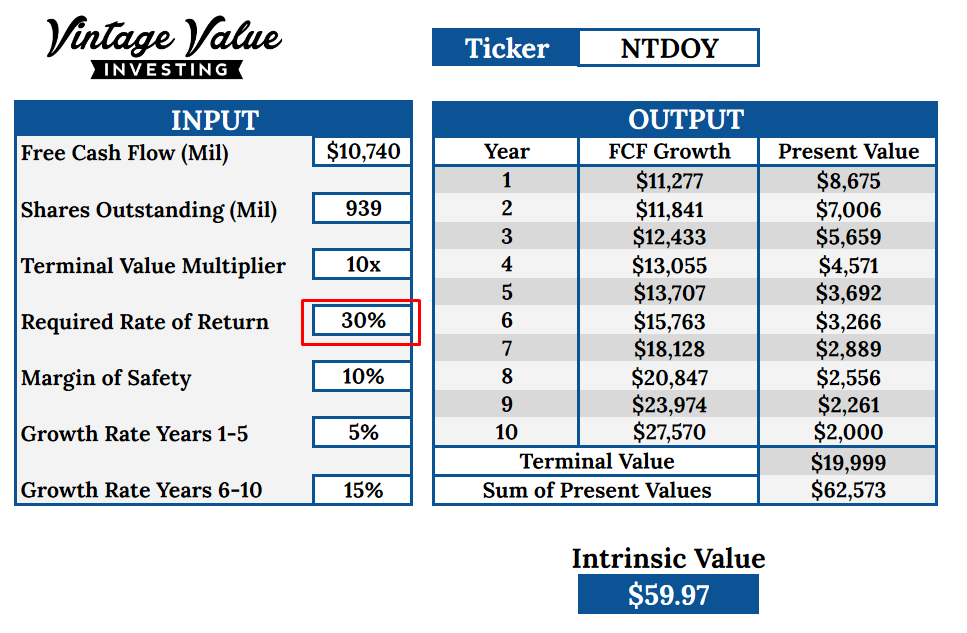

Chapter 4: Valuation

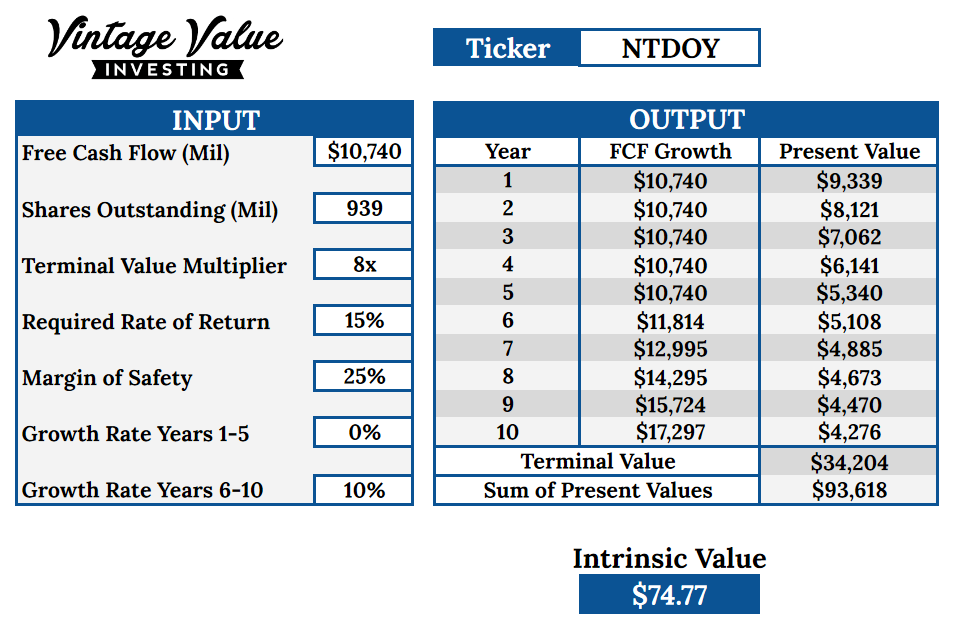

I decided to use the Discounted Free Cash Flow method to value Nintendo. As the company is likely to keep growing for at the very least the next 10 years, I think this method is rather adequate.

Free cash flow grew explosively in 2019 and 2020, so I will be cautious in using the current numbers. We are at a high with the success of the Switch, and some short-term decline is likely. So, I will give a 0% growth for the next 5 years, and a high margin of safety. Same prudence for the value multiplier.

For the farther future, I assume something will work out to generate some growth, either a successful new console, theme parks, retail stores, movies, or augmented reality. I think any of these could produce a moderate 10% at least growth in cash flow.

This would indicate that with the recent pullback in price, Nintendo stock is quite undervalued. It was also probably a little overvalued at its peak. And this does not even include the abundant cash in the balance sheet.

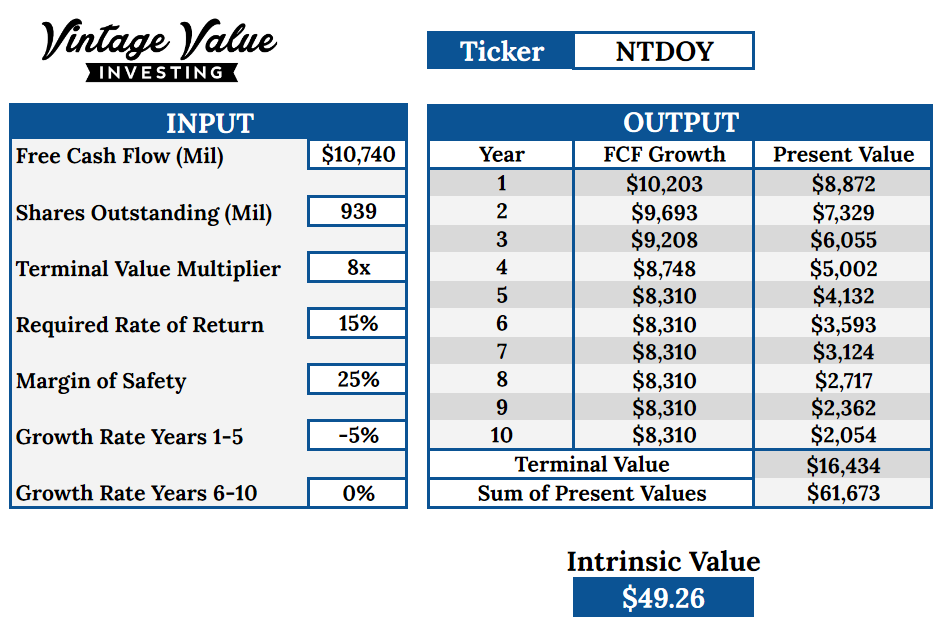

Now, the worst-case scenario would be no growth in cash flow at all. What if the skeptics are right? What if free cash flow goes down for 5 years and never recovers after? Even then, the current price would almost be enough to ensure a 15% return, and certainly a 10%. Currently, a somewhat disappointing last quarter have depressed the stock price. But the long-term prospects of the company are unchanged.

And last, what if things go really well with some growth in the near term and explosive growth later? Then obviously, the current price is ridiculously low, enough to ensure a 30% rate of annualized returns.

Conclusion

Nintendo is one of these companies that fit very well the Warren Buffett style of investing. A lot of people know its products and business model. It is simple to understand, it is well established and has large moats (IP and market positioning). In addition, the experience of Disney has shown the way on how to monetize dormant IP to both management and investors.

Interestingly enough, Buffett bought 5% of Disney for $4M (yes, million!) in 1966. He then sold it again the year after for a quick 50% profit. Would he have kept it like he did with Coca-Cola, the 5% stack would now be worth $6B, or a 1500-bagger!! Selling Disney is apparently something he regrets dearly to these days.

I think the future for Nintendo is somewhat similar, even if I would be fine getting “just” a 100-bagger from it by the time I retire. A lot of patience will be required. This is the kind of stock to keep forever, and watch grow, will mostly ignoring the market fluctuations, except to buy some more in a period of weakness.

Right now, a prejudice against the Japanese market and Japanese corporate culture block most investors to realize Nintendo’s potential. The perception of Nintendo being “just” a cyclical console company contributes as well.

But really, is a super conservative, cash-savvy, and careful approach such a bad thing in a highly cyclical and unstable industry? Or is it the recipe for long-term success? I think Nintendo culture is in fact its greatest asset, despite being nowhere to be seen on the balance sheet.

It is the super-high quality of its product that keeps gamers coming back for generations. And it is its cautious, borderline obsessive management that will ensure the proper growth of its IP in new carefully crafted masterpieces.

We might never see three or four Nintendo movies hitting the box office every year as we got used to with Marvel movies. But I am confident that most if not all will be what the fans want to see. More in line with the original Star Wars trilogy or Lord of the Ring than Avengers.

And while we wait for the next one, we will be able to visit a theme park, buy some merchandising or download the latest remaster of a classic from the NES, Gameboy, or N64 consoles. On a Nintendo console of course.

Holdings Disclosure

I have a beneficial long position in the shares of NTDOY either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.