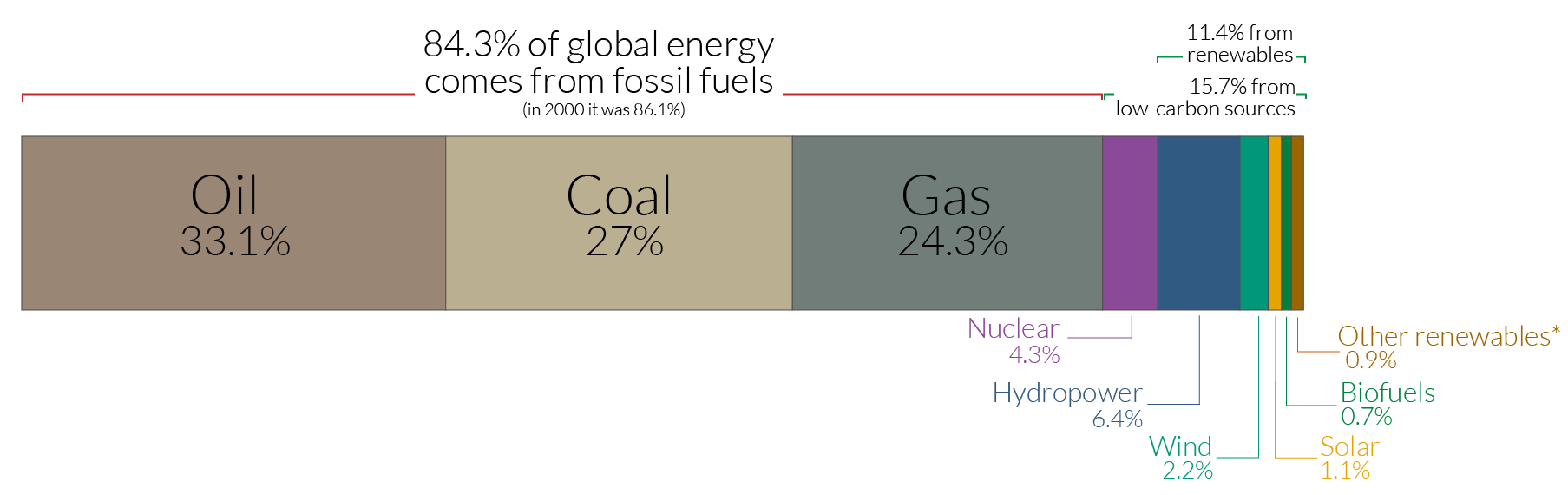

Not long ago, when the financial world talked of energy it meant oil, gas, and maybe coal. Lately, the discussion has added renewables, especially solar and wind. Nuclear energy is rarely mentioned, despite producing 4.3% of the world’s energy consumption, above the combined 2.2% of wind and 1.1% of solar.

Interest in nuclear power is currently surging. The imminent threat of climate change and the volatile prices and geopolitical threats affecting traditional energy sources are driving a search for alternatives, and renewables are still limited by non-continuous production and limited storage capacity.

That opens a window for nuclear power, but what does that mean from an investment perspective?

Let’s look.

How Does Nuclear Energy Work?

Uranium is an abundant resource, with reserves estimated at double the entire production since 1945. It is also extremely dense, with the energy in 1g equivalent to 16,000g of coal. This very high level of energy allows the use of uranium to turn water into steam, which is then used to turn a turbine, producing electricity.

Due to the nature of its fuel, nuclear energy is considered a low-carbon energy source. The only carbon emitted is during the mining of uranium and the construction of nuclear plants.

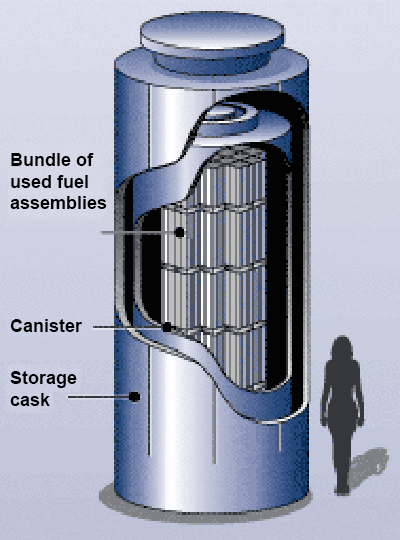

Nuclear energy produces nuclear waste, which can be dangerous for a very long period of time. How to treat nuclear waste is debated, with the majority of them calling for waste to be rendered inactive in vitrified form, as in the schematic below. Thanks to these solutions, the nuclear waste problem is increasingly seen as manageable.

The Case for Nuclear

The reason for the recent lack of enthusiasm about nuclear is its relative stagnation. In the 70s nuclear technology was expected to power the future, and massive building efforts were undertaken in the most powerful nations. The 1986 Chernobyl disaster dampened this enthusiasm dramatically. Just when global warming concerns could have helped nuclear to restart, Fukushima happened.

After several unpredictable crashes, investors became justifiably wary of nuclear. The sector stopped growing and stringent regulations slowed down innovation as well.

Still, a look back at the world energy mix shows how hard it will be to replace fossil fuels. To this day, 84% of the world’s energy still comes from fossil sources. Solar and wind are by nature intermittent and should be supplemented by more steady power sources, which keep producing when the wind does not blow and the sun does not shine.

High energy prices and the ongoing issues with Russia’s supply are creating a very tense situation in energy markets. Short of an end to the Ukraine war AND an unlikely return to the status quo, this is a situation here to stay. Even if the Russian situation resolves, conflict potential in the critical Arabian Gulf remains high.

Higher energy prices in Europe and Asia, increasing public awareness of climate change, and the limitations of renewables make fixed-cost nuclear a lot more attractive than before, and new technologies promise a higher level of safety. Those factors are driving a nuclear comeback.

Nuclear Companies

The sector can be separated along the nuclear value chain, from fuel production to electricity generation.

Uranium Miners

While it is technically possible to use other fuels, almost all current nuclear technology runs on uranium. The sector is dominated by 2 companies, Kazatoprom and Cameco.

Kazatomprom operates in Kazakhstan and is by far the larger miner of uranium in the world, producing 45% of the world’s supply. Cameco produces 18% of the world’s supply. The rest of the production is at the hands of state companies or smaller actors, notably in Australia, Russia, China, Niger, and Namibia.

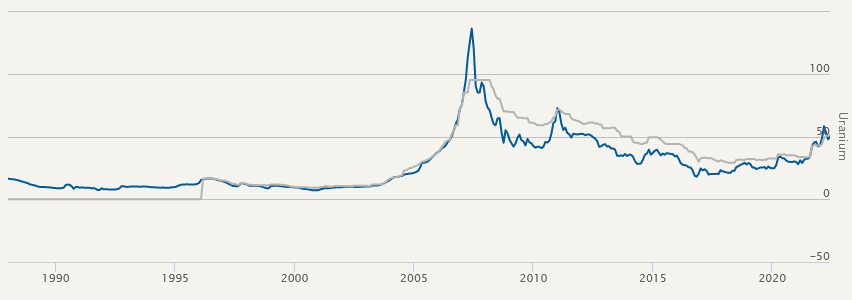

Uranium experienced a price spike in 2008, in the midst of a commodities boom. The sector has since been marked by years of overproduction and low prices, close to or below production costs. This led both Cameca and Kazatoprom to suspend operations at several mines they still own today.

Nuclear energy is not fuel-intensive and even a surge in new plant construction is not likely to result in a uranium mining boom.

Manufacturers

These companies make components for nuclear reactors, whole reactors, or complete power plants. Here, too, we find a lot of state-owned companies and a few private and publicly traded.

Companies making components for nuclear power (like for example, only turbines) or whole reactors tend to be part of larger industrial conglomerates (for example, GE, Westinghouse, or Rolls Royce). So there are relatively few stocks in the market that are established pure players in the nuclear industry.

👉 One of these pure players will be covered in our next premium report, analyzing the nuclear industry prospects and 3 different stocks in the sector (a pure player, a startup, and a dividend stock). Sign up for Stock Spotlight if you’d like to read it as soon as it’s published.

Utilities

Utilities are the electric companies operating the nuclear power plants They are often partially owned or heavily regulated by the local or national government, with only a small portion of the company publicly listed.

Utilities using nuclear power tend to have a similar profile to other utilities. This includes a focus on large CAPEX on long-duration assets, conservative financial management, and distributing a large part of their free cash flow to shareholders as dividends.

In the US, utilities typically serve defined areas, giving them limited growth potential. Investors treat them primarily as dividend generators.

The main risk for nuclear-operating utilities is political interference. Several countries, notably Germany, have aggressively phased out power plants that could have been still running for decades.

Nuclear’s Future

Nuclear manufacturers are aware of the limitations of traditional nuclear power plants:

- They are very expensive to build, with billions in upfront costs.

- They are very large, complicating their integration into an existing power grid.

- There is a significant risk of accident, with large-scale plants creating risks of a reactor meltdown.

In response, a new concept has emerged in the form of Small Modular Reactors (SMRs).

SMRs have a passive cooling design, allowing the reactor to automatically shut down safely even without human intervention or after a catastrophe like an earthquake or a tsunami.

This is now the center of development for the nuclear industry. Most established actors have either a partnership with a startup or their own SMR program ongoing.

SMRs don’t have to be built on-site. They are built in a factory and shipped as complete modules to the location where they’ll be installed, dramatically cutting design and construction costs. They are flexible: a power user can install as few or as many modules as they need.

Thanks to their smaller size, SMRs are also expected to be more widely used for industrial applications requiring a lot of power, as demonstrated by the project of KGHM, a large copper producer in Poland, to power its factories with its own nuclear reactor.

Conclusion

Fossil fuels are now expensive, both in absolute price and environmental effects. They are also highly vulnerable to supply disruption. This increases the need for a reliable low-carbon alternative. With its predictable and reliable power output, nuclear will have to be part of the energy mix of a low-carbon economy.

In addition to this renewed support, new designs are coming to help power a new nuclear boom. SMRs reactors offer a previously unreachable safety profile, while also permitting lower costs and quicker projects. Their flexible power plant design can also help decarbonize multiple industries: power-intensive industries can install their own power plants using SMRs.

Nuclear power is clearly back in the energy mix: there is currently no other way to significantly reduce oil and gas use as a source of stable, reliable electric power generation.

The implications of that fact for investors are still emerging. Accident risk is still significant, and even an accident in an older reactor could affect the entire industry: public perception does not differentiate among reactor designs. The potential of the business still deserves attention as new technologies and companies emerge.

Industry Primers

The process of analyzing a company varies considerably from industry to industry. Many industries have their own vocabularies and specific concerns that investors need to consider. This series of articles looks at specific industries and at industry-specific factors that affect investments. The goals are to highlight specific risks, clarify confusing terminology and explain industry-specific metrics for valuation. These methods complement the usual evaluation process, they don’t replace it.