Dividends are an attractive but somewhat confusing concept for many beginning investors. Getting money regularly from your investment regardless of market price fluctuations is very tempting. There are entire investing strategies and funds focused exclusively on dividend investing.

A juicy dividend yield can also be too good to be true, and it’s important to know when that’s the case. So what is the difference between good and bad dividends, and how do you decide whether to focus on dividend-bearing stocks?

What Are Dividends?

Dividends are money that a company distributes directly to the owners of a company, the shareholders. Dividends and share buybacks are the devices companies use to return money to their investors.

Dividends are paid from the cash available to the company. This is why ultimately, the value of a company is equal to the total amount of its future free cash flow. That cash can be used to grow the value of the company or be distributed in the form of dividends.

A dividend is typically a fixed amount per share, regardless of the share value at the time of the payment. Most companies pay dividends quarterly. Some may pay annually or even issue a special dividend after an unusually profitable period.

What is Dividend Yield?

When a company distributes a dividend, it is possible to calculate the dividend yield. The dividend yield is a ratio, expressed as a percentage, that tells us how much of the company’s share price is paid out in dividends each year.

The dividend yield is calculated by dividing the dividend per share by the stock price.

The dividend yield formula is:

Dividend Yield = Cash Dividend per share / Market Price per share * 100

👉 For example: If a stock is trading at $100 and the dividend is 8$/share, this makes 8/100=0.08, or an 8% dividend yield.

This means that if the dividend stays unchanged, the investment in that example is expected to bring at least 8% yearly from the dividend alone. Any growth of the business and/or stock price rise would come adding to these returns.

The dividend yield will rise if the stock price falls.

👉 To use the example we used above: If the dividend remains at $8 per share but the stock price falls from $100 to $75, the dividend yield will go up to 10.67%.

It’s important to note that your dividend yield is based on the price you paid for the stock, not on the current dividend yield. If you bought our sample stock at $75 and it went up to $100, the dividend you receive is still 10.67% of what you paid. Your yield is still 10.67%.

You can think of the dividend yield as the equivalent of a bond’s interest rate. It’s a defined return on investment that does not change unless the company reduces or eliminates its dividend.

Advantages of Dividends

Dividend payments may cut into a company’s growth, but they still have significant advantages for many investors.

For some other investors, dividends offer a higher level of control. Once the cash is distributed, they can decide by themselves if they want to reinvest it in the company or allocate it to other opportunities. Instead of being somewhat locked in by the decisions of company management, they can decide for themselves where returns are the most promising.

For income-focused investors, like people in retirement, dividends distribution gives a steady income similar to bonds but often with a much higher yield. Dividend stocks are a solid alternative to bonds during periods when bond yields are very low.

Dividend-bearing stocks are also a common defensive play. If stock prices fall across the board, the rising yields of dividend stocks tend to attract new investors seeking that income, assuming that the Company is strong enough to keep paying its dividend. This limits the likelihood of dramatic drops in stock price.

👉 To go back to our earlier example: If our hypothetical stock with a dividend of $8 saw its stock fall from $100 to $50, the dividend yield would jump to 16%. That’s a very high return on invested capital and would quickly draw in new investors, bringing the stock price back up. A reliable dividend puts a floor under how far a stock is likely to drop.

Dividend Bearing Stocks Yield Income and Growth

Dividend-bearing stocks provide income, like a bond. They also have the potential for increased (or decreased) value, as the price of the stock changes.

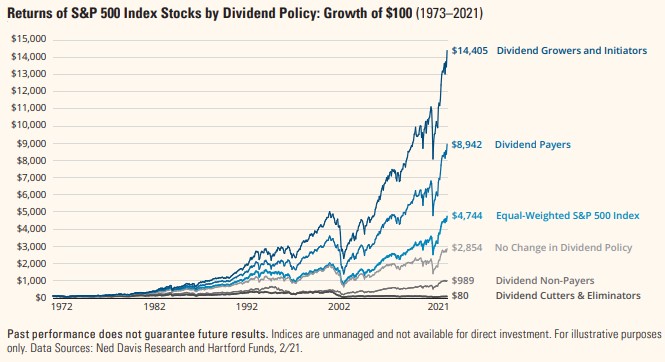

Dividend-bearing stocks have performed very well over time. As you can see from the chart below, companies that initiate, increase, and pay dividends have substantially outperformed the S&P 500 over time. That gives two opportunities for returns: the dividends themselves and the stock price.

☝️ There’s no guarantee that any stock will increase in value, but dividend stocks have traditionally performed well.

Tax Considerations

One reason why investing in compounders tends to outperform other strategies is that it is very tax-efficient. A company like Apple makes money and reinvests it into more R&D for better products. This means lower taxes for the company and no taxes for the investors until they sell the stock.

In comparison, a company distributing dividends will force its investors to declare the dividends as an income. This can cost them a significant part of their returns, and slow down compounding drastically.

This is why when it comes to dividend investing, it is best to do it with a tax-advantaged account like an IRA or 401(k).

☝️ Note: Dividends from foreign countries might be subjected to extra or special taxes.

Dividends vs. Growth

Dividends are a way for a company to return profits directly to shareholders. Any profits that are returned to shareholders cannot be invested to generate growth for the company.

Growth-oriented investors often search for quality companies able to grow year after year, often called “compounders”. Companies like Visa, Alphabet (Google), Mastercard, Costco, Sherwin-Williams, Brown & Brown, Nvidia, and Microsoft are good examples. They are generally high-quality businesses with very solid business models.

These companies often pay a small dividend or no dividend at all. This makes sense, as they are better off reinvesting cash into the business and generating growth. As the company grows the share value grows with it. Investors get their return from increased share value, not dividends. Investors who prioritize the appreciation of share value generally don’t look for high dividends.

Dividend distribution makes sense for stable and non-growing businesses, with utilities the classic example. Many power generation companies grow very slowly, at best in line with general GDP. They might be profitable, but have limited possibilities to reinvest for growth. In that context, a generous dividend policy makes more sense than squandering cash on growth at all costs.

Mature companies with limited room for growth often use a dividend to attract investors.

Good Dividend Policies

Looking for low/no dividend high-quality compounders is still a very solid strategy for long-term investing. Dividends can also make sense in the following cases.

1. Businesses With Low or No Growth

Not all businesses can or should grow at all costs. I mentioned utilities, but this is also true for businesses operating in a declining sector or extractive industries like fossil fuel or mining. If additional growth would bring a low yield or negative returns on the capital used, growth should be avoided.

Instead, shareholders’ interests are best protected by “milking” the company and distributing the cash through dividends. The money can then be reinvested in other activities more promising in the long term. This is also good for the whole economy, as this means capital is allocated to productive activities.

2. Highly Cyclical Businesses

Some sectors are inherently cyclical and go through regular booms and busts. We can think of mining or the energy sector for example. In these cases, investing in growth at the top of the cycle is a sure way to waste money. Generous dividends distribution during the boom will bring great returns to investors and limit losses even if the sector crashes again.

For example, we have today companies like Petrobras, distributing cash to reach up to 17.5% dividend yield. Once the cash is distributed, it is “safe” from a crash in oil prices, Brazilian politics, corruption, and other factors.

3. Dividend Aristocrats

One last type of dividend investing strategy is to focus on the so-called “dividend aristocrats”. These are companies that have increased their dividend payout every year for at least 25 years in a row. These are companies like Home Depot or Altria (tobacco). The profile of these companies is usually a “boring” but steady business with plenty of possibilities for reinvestment and growth.

Investing in these companies is a mix of compounder and dividend investing. Yields are rarely very high but they are consistent and may rise when the stock is unpopular.

Bad Dividend Policies

While attractive at first glance, dividends can also lure unsuspecting investors into a trap. It is easy to get greedy when dividend yields reach extremely high levels.

1. Hiding Risk

A company may have a very high dividend yield not so much because of high profits but because of a very low stock price. This low stock price is often justified by very real high risks, for example, the geopolitical risk or the risk of expropriation by the government.

Please note that the example of Petrobras I gave above could as well be such a case. Brazilian politics are notoriously unstable and have almost destroyed the company in the past. Gazprom before the Ukraine invasion was such a case of high dividends leading to ruin. Very high dividend yield should probably always be looked at with a grain of skepticism.

2. Uncovered Dividends

A characteristic of dividends is that it is difficult for companies that started to give dividends to reduce the amount of money distributed. A dividend reduction generally creates a strong backlash from shareholders that expected their dividend yield to be “safe”. This can lead to management teams trying to maintain dividends even when cash flow is insufficient to pay for them. In this case, the dividend digs into the cash the company needs to maintain its activity and survive.

In the short term, this might be okay, but this might put the company’s survival at risk if the dividend payout doesn’t leave enough cash to fund operations.

👉 As a rule of thumb, the payout ratio – the percentage of net income that a company spends on its dividend – should not be higher than 40-70%.

Some companies deliberately take the risk of showing very high payout ratios. ExxonMobil is raising its annual dividend for the 42nd consecutive year in 2025. ExxonMobil maintains its dividend even when oil prices and profits are low, sometimes running a payout ratio over 100%, meaning they are paying more in dividends than they earn in profits. They can get away with this because they are a very large company with deep cash reserves, and because investors believe that oil prices will cycle back up and drive higher profits.

☝️ A high payout ratio may not always be a danger sign, but it’s certainly a red flag that a potential investor needs to examine closely.

Conclusion

Dividends can provide great returns to investors if the business can sustain them in the long run. Growing dividends for a long time can also indicate a great profitable business able to grow over time. Generous dividends in stable or cyclical businesses probably indicate shareholder-focused management and can be profitable as well.

Still, very high dividend yields compared to cash flows or high dividends in companies facing high risks should be a red flag to warn of possible danger. Dividend-focused investing is typically seen as a conservative strategy, but a stock with a very high dividend yield is not always a safe buy.