Real estate is one of the first asset classes investors think of when they look for ways to diversify their portfolios. It has also traditionally had a very high entry cost. It is still possible to invest in real estate with little money.

Why Invest in Real Estate?

Over the past 30 years, the average price of a family home has gone up by an average of 4.4% a year[1]. The average rate of inflation over the past 62 years has been around 3.5% annually[2]. Real estate appreciation – on average – is just a hair above inflation.

And when you consider that the stock market has averaged around 10% annually for the past 30 years, you realize that stocks have far outperformed the real estate market. So, why should you invest in real estate with little money?

🏡 Learn more: Eager to explore real estate investments? We’ve outlined the top approaches for those just getting their feet wet.

Stability

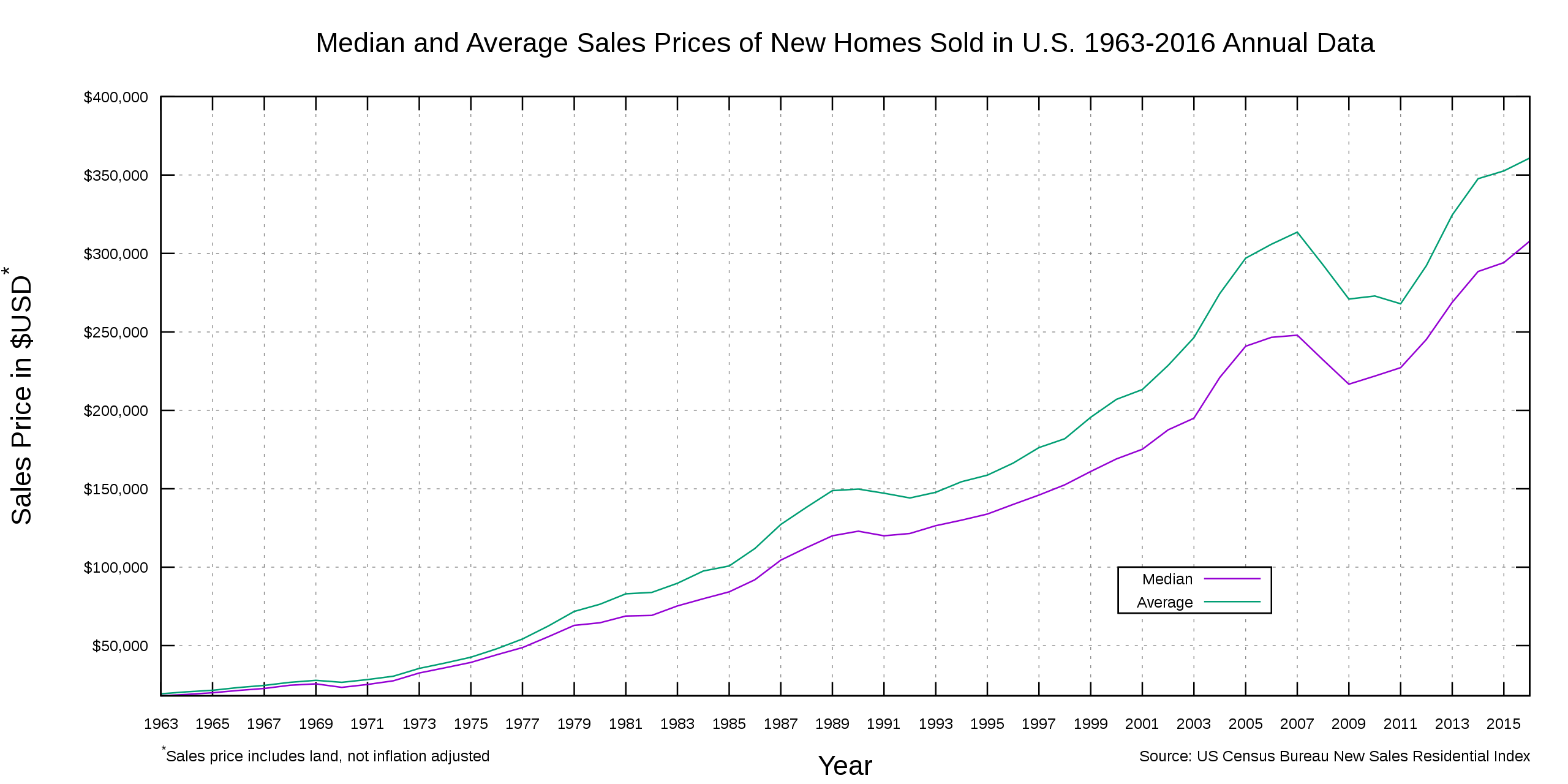

Real estate is typically a stable asset with little volatility. Of course, there will be exceptions (think the 2008 housing crash), but on average, it is very hard to lose all your money in real estate. The stock market is volatile, and if you aren’t prepared for the big ups and downs, it can be nerve-wracking. To see how stable the returns usually are, take a look at the following graph spanning the 53 years between 1963 and 2016.

Real estate investments can provide a source of cash flow in the form of rent. The incoming rent can be high enough to cover a healthy portion of your mortgage payments, reducing the overall cost of your investment.

Tax Advantages

Real estate offers many tax advantages to the investor, many of which aren’t enjoyed by stock market investors. For one thing, thanks to the current tax laws, real estate investors get to retain more of the income generated from their real estate investments. They can also benefit from many deductions as well as capital gains tax deferral strategies.

Security

Aside from stability, real estate provides security. In other words, a stock is a piece of paper that represents part ownership in a company, and if the company goes under, that piece of paper is worthless. A property is a physical, tangible asset that has utility beyond being an investment vehicle.

Even though stocks have a higher overall return than real estate over the long term, real estate has a higher risk-adjusted return. This means that when you account for the risk inherent in each investment vehicle, real estate comes out ahead.

Today, the retail investor has more options than ever before to invest in real estate. Whether you have $10 or $1M, there is an investment vehicle out there that will expose you to the real estate market.

These are sound reasons to put some money into real estate investments. And if you’re short on money, you still have investment options to consider

How to Invest in Real Estate with Little Money

Real estate investing has traditionally been limited to people who can afford to purchase and own property. This takes substantial sums of money or access to large loans at reasonable interest rates. That’s hard for people who don’t have great credit or overflowing bank accounts.

You can invest in real estate with little money (as little as $10). What’s more, you can make money from the purchase and sale of properties without ever having to put in a penny of your money.

Let’s look at different ways you can invest in real estate with little money. We will explore three different cases: You have no money to invest, you have $10-$999 to invest, and you have $1000-$10,000 to invest

📱 Learn more: The right app can simplify real estate investments. Check out our insights from testing the top 5 on the market.

Investing in Real Estate When You Have No Money

Nothing is for free. So, if you don’t have any cash to invest, then you will need to bring something else to the table:

- Time and effort: Any property will either need to be renovated or managed. For instance, if you’re flipping houses, then you need to fix the place up first.

- Special skills: These are skills used to spot a good investment, negotiate a good price, and so on.

- Another asset: If you own a home or another suitable asset, you can use it to secure a loan.

With those ingredients, you have several options to consider when investing in real estate with little money.

1. Wholesaling

Wholesalers are very similar to real estate brokers. They act as intermediaries between buyers and sellers.

Wholesalers will sign a wholesale contract with distressed sellers, promising them to find a buyer for the property within a certain timeframe. Wholesalers may even put down an earnest money deposit. In return, the seller can’t entertain any other buyers during the agreed-upon period.

For wholesalers, having ironclad contracts is key. It ensures that their deposit doesn’t get lost. It is also important to have a solid network of real estate investors to whom these properties can be sold. This is not to mention how wholesalers need strong negotiation and people skills, especially when dealing with a distressed seller whose emotions may be all over the place.

But most important of all is that wholesalers need to be able to assess the value of a property and gauge how attractive it would be to buyers.

2. Bird Dogging

Let’s say that you have the ability to spot good real estate investment opportunities, but you don’t have the other skills required for wholesaling. In this case, bird-dogging is for you.

Simply, bird-dogging is all about finding these golden opportunities and passing them along to investors. You can even pass them to wholesalers in return for a finder’s fee.

The higher the quality of your analysis, the higher the fee you can demand.

3. Leveraging your Primary Residence

Where you live right now can be the gate that introduces you to the world of real estate investing.

For starters, you can rent a portion of it. For instance, if you live in a 2-bedroom apartment, you can rent out the spare bedroom. As a landlord, you will have to go through all of the required steps, from finding and vetting tenants to getting insurance and ensuring the comfort of whoever is staying at your home.

If you want to buy a new place and you own your current residence, you can use your current home’s equity and borrow cash secured against it. This cash can come in the form of a home equity loan or a Home Equity Line of Credit (HELOC), and it can pay for your downpayment on a new investment property.

On the subject of loans against a primary residence that you own, you can also look into a cash-out refinance, which is a type of mortgage. You can pay the downpayment on a new investment property by refinancing the mortgage on your current home and taking out up to 80% of the equity built up in the real estate property so far.

💵 Learn more: Turn your spare space into potential income: our in-depth review of Neighbor.com offers insights and takeaways.

Invest in Real Estate With Little Money: $10-$999

Most investments in this category will involve working with a group. You’ll pool your resources with those of others.

So, while you gain some things, you will lose others. Most importantly, you will lose control over what happens with the real estate investment. Instead, a specialized entity will manage the asset, and you will have to trust them to do a good job.

In some cases, you might even lose control over which properties are bought, and you will only enjoy the rewards (or losses) reaped by the entire real estate portfolio as a whole. Add to that, you will have to pay a management fee, lowering your overall returns.

Bearing that in mind, your biggest gain is that you will enjoy access to properties and investments that would have been unaffordable had you been on your own. These investments typically don’t require large inputs of time or effort.

Here are some of your best options to invest in real estate with little money ($10-$999)

📖 Learn more: Real estate wisdom is just a book away. Dive into our recommended reads to elevate your investing game.

1. REITs

A Real Estate Investment Trust or REIT is a liquid way for the average investor to get into real estate.

REITs are shares in companies that invest in real estate. So, your shares will appreciate or depreciate depending on the performance of the company and its portfolio of real estate investments.

REITs combine the relative stability of the real estate market and the liquidity of the stock market. You can buy REITs for as little as $10, if not less, making it a great way to invest in real estate with little money.

For any company to qualify for REIT status, it needs to pay out 90% of its profits as dividends to its investors. Otherwise, the company would have to pay corporate income tax. So, REITs pay plenty of dividends but have a hard time growing their portfolios.

If you really want to diversify your portfolio, you should consider investing in an ETF consisting of different REITs. This would expand your exposure and make sure that your investment’s performance is more related to the real estate market as a whole rather than to any single REIT.

2. Crowdfunding Platforms

Even though crowdfunding platforms can be used to finance your real estate investment, we are going to look at things from the perspective of the person actually putting up the money (after all, you want to invest in real estate with little money, right?)

Online crowdfunding platforms let you combine your money with other investors to fund real estate developers and enable them to take on large projects.

One of the nice things about crowdfunding platforms is that, like REITs, you can invest as little as $10. For instance, companies like Fundrise and Groundfloor enable you to put your money into short-term loans.

There are a few caveats. For starters, when participating in crowdfunding, you need to do your own due diligence, especially as real estate developers don’t have to follow the same stringent disclosure requirements enforced on public companies in the stock market. The other thing to look out for is that some crowdfunding opportunities are only open to accredited investors, which applies to people whose income or net worth exceeds a certain limit.

👉 Learn more: The first step to entrepreneurial success? Securing the right funding. Check out these five tried-and-true methods.

Investing in Real Estate With $1,000-$10,000

At this stage, you can actually buy your own real estate property if you can get the right loan for it. You would use your own money, the $1,000 to $10,000 sum, for the downpayment, and the mortgage will cover the rest for you. If you play your cards right, your investment property can help pay off the loan by generating a steady cash flow for you.

And while this option gives you the most control over the property, it is usually the most risky because regardless of whether your investment succeeds or fails, you will have to pay your loan off.

💵 Learn more: Personal loans for home buying? It’s a topic of discussion in our article. See what we found out.

1. The General Requirements

The first and most important requirement is your credit score. With the right credit score, you can qualify for most loans out there and get favorable interest ratesA bad credit score can mean either a rejected application or an exorbitant interest rate that would eat at your potential returns.

There are other factors that any lender will take into consideration:

- Your income and employment status

- Your credit utilization (Ideally, it should be around 30% or less)

- Your co-signer or lack thereof

- Your debt-to-income ratio

- Your derogatory marks (previous bankruptcies, delinquencies, and so on)

A few years ago, when interest rates were near zero thanks to the pandemic, loans were cheap enough to make investing in real estate attractive. In 2025, the average 30-year mortgage rate remains between 6.6% and 6.8%, with forecasts suggesting rates will stay above 6% throughout the year.

Let’s take a look at the different types of loans available to you. There are two broad categories of loans: Government loans and private loans. Government loans often offer lower interest rates and down payments, but there may be additional requirements.

2. Government Loans

The US government provides different types of loans for would-be homeowners and real estate investors. These loans involve some red tape, but if you qualify for one of them, it can make the investment that much more feasible.

These loans are typically made by approved private lenders but guaranteed by the government agency involved.

FHA Loans

The Federal Housing Authority provides these mortgages for people purchasing a primary residence, i.e., a property where they plan to live. That requirement limits their usability for pure investment properties.

While the average mortgage loan (the kind you’d get from a bank) requires a 20% downpayment on the property, an FHA loan may require a downpayment as low as 3.5%. FHA loans typically provide better interest rates than other options.

VA Loans

VA loans are given to veterans and their immediate family members, so you may not qualify for one. For those who do, you can get a mortgage on a house with a 0% downpayment so long as it will be your primary residence.

VA loans ensure great interest rates, lower closing costs, and can be used more than once. The primary residence requirement may still make these loans difficult to use for investment properties unless you plan to treat your residence as an investment or rent part of it out.

USDA Loans

The US Department of Agriculture provides low-interest mortgages through its Rural Development Office.

USDA loans have a set objective of serving underpopulated zones within the US, and they are available in towns that have less than 10,000 inhabitants. This may seem limiting, but almost 97% of towns in the United States satisfy this condition.

To qualify, you must show that your income is low to moderate. In other words, if you can’t get a traditional mortgage, then this might be the loan for you.

🏡 Learn more: The journey to homeownership as a self-employed individual is different; our guide simplifies every step for you.

Fannie Mae & Freddie Mac Loans

Fannie Mae and Freddie Mac are both private companies, they are also government-sponsored as their objectives and operations are endorsed by the government.

Long story short, both these companies fund mortgage lenders to make house financing more accessible. In return for this funding, these two companies set the guidelines surrounding different mortgage loan options.

So, why are these loans so popular?

For starters, they require a downpayment as low as 3%. This is not to mention how they offer fixed-rate mortgages for periods that can last as long as 30 years. Additionally, the other loans on this list are for primary residences, but Fannie Mae and Freddie Mac loans can be used for second homes, vacation homes, and rental properties. They provide loan limits that are higher than what the FHA loan program provides.

3. Private Loans

Government-backed loans usually provide favorable terms, but they can be slow and hard to qualify for. Here are several options to think about if you want to invest in real estate with little money.

Conventional Mortgages

A conventional mortgage is exactly what it sounds like. You borrow directly from a bank or an online lender. You will need good credit and a low debt-to-income ratio to qualify, but there will be no restrictions on your use of the property, making these loans ideal for investment properties if you can get them.

The obstacle, of course, is that you will have to pay a down payment and closing costs. Even if you have good credit and a low debt-to-income ratio, this can be challenging if you are looking for a way to invest in real estate with little money.

First-Time Homebuyer Assistance Programs

Many states and cities have programs designed to help people buy their first homes. If you previously owned a home but have not owned one in several years, you may also qualify.

These programs do not usually offer loans. Instead, they typically focus on helping buyers cover closing costs or a down payment. That assistance can be just what you need if you are creditworthy but don’t have ready cash.

These programs may require that the property be a primary residence.

Seller Financing

Seller financing involves getting a loan from the seller. Rather than demanding the full price of the property upfront, the seller can set up with you a payment schedule that can suit both of you.

This option is ideal when you can’t seem to get a loan through any other means.

A seller who helps you finance the purchase of the property will likely demand a steep interest rate, one that is larger than what a bank would have demanded. You may have to agree to stringent terms that dictate what happens should you default on your obligations.

Lease Options

In a lease option deal, the owner of the piece of real estate will charge you rent to use their property, and their rent will be higher than market value. In return, you will have the right to buy the property at a later date at an already predetermined price.

With a Master Lease Option, you not only have the right to do what you want with the property but can also rent it to other tenants. Of course, you will have to be involved in all the minutiae that plague landlords, including rent collection, property maintenance, and so on.

As appealing as a Master Lease Option may seem (After all, with enough tenants, your rent burden is lightened to non-existent), there are a few issues you need to be careful of. To begin with, you should opt for this type of lease option when dealing with apartment buildings or any other large real estate investment because this enables you to bring in more tenants.

A Master Lease Option can be very risky, especially if you can’t find tenants to occupy the property.

Hard Money Lenders

If you can’t get a conventional mortgage loan, another option to explore is a hard money loan. This is a loan that comes from either a single private individual or a group of individuals pooling their resources together.

Unlike most other lenders, hard money lenders don’t have onerous requirements when it comes to qualifying someone for a loan. In fact, they don’t place too much emphasis on the borrower and their credit score. Instead, they focus on the property itself and its potential for appreciation.

The approval process of hard money lenders tends to be much faster in comparison to other types of lenders. The flip side of that coin is that hard money lenders also charge higher interest rates because they are taking on more risk than the average lender.

💰 Learn more: Whether it’s for business, property, or personal needs, here’s your roadmap to securing a million-dollar loan.

4. Different Strategies For Investing in Real Estate with Little Money

There are several less conventional ways to invest in real estate with little money. They aren’t for everyone, but people do use them effectively, and they might work for you.

House Hacking

Several of the loans on this list only support people buying a primary residence, which is a place they plan to live in. So, how can you generate income from a primary residence?

One way is house hacking: You can buy a large place, such as a multi-family unit, live in one of those units, and rent out the remaining units. And if you have done your due diligence correctly, the rent can cover your mortgage payments.

After you’ve lived in the property for a while, you can leave it and buy a new property as a new residence using an FHA loan yet again.

The BRRRR Method

The letters in BRRRR stand for:

- Buy

- Rehab

- Rent

- Refinance

- Repeat.

Another less conventional method to invest in real estate with little money is to buy a property that needs some work and, hence, is undervalued. The seller may be eager to get rid of the place and willing to make a better deal.

You put in the work and remodel the place, boosting the property value. Once the asset is in good shape, you rent it out to tenants and start generating cash flow. After renting out the property, you can then refinance it, and seeing as it is worth more thanks to your remodeling efforts, you should receive a new loan that covers both the original price of the asset as well as any renovation costs.

Finally, rinse and repeat the above process to build a portfolio of real estate assets.

Obviously, this strategy requires plenty of understanding of the real estate market, along with remodeling skills and a high tolerance for risk.

There are several options out there that can provide loans for home remodeling, including:

- The HUD Title 1 property improvement loan.

- The 203(k) rehabilitation mortgage insurance program.

- The weatherization assistance program.

- Fannie Mae Homestyle Renovation loan

- USDA Section 505 Home Repair Loans and Grants.

The challenge with this strategy is that you have to pay the mortgage as well as the remodeling loan for a while before you start seeing rent income. For some, this can be onerous, which is why it is a costly strategy that can involve high levels of debt.

🏠 Learn more: Deciding between selling your home ‘as is’ or giving it a facelift? Dive into the pros and cons in our latest analysis.

How to Invest in Real Estate With Little Money: Which is the Best Option?

We have gone through several options to invest in real estate with little money, and not all of them will be suitable for you. You need to decide how much money you’re willing to invest and how much time and effort you’re willing to put in. Additionally, you want to be honest with yourself about your ability to spot investment opportunities as well as to manage and renovate properties.

There are external factors you need to consider. Your credit score plays a huge role in deciding which path you end up taking.

There is also good news. You can combine different methods and ideas from here to find the best path for you in order to invest in real estate with little money. For example, you could get a lease option, and when it is time to buy the property, you can use an FHA Loan, or you could take the simple path and invest in a REIT.

The key is to work through the menu of options and choose what works best for you!