Biotechnology is on the cutting edge of healthcare, leveraging technological and scientific advancement to treat diseases once thought incurable. That technological level carries excitement, but often leaves investors confused about their options.

Let’s take a closer look at this up and coming sector and some ways to assess companies in it.

One of the things that launched the strength in biotech is when the pharmaceutical industry itself got a little slow.

Louis Navellier, Chairman and Founder of Navellier & Associates

Key Takeaways

- Understand the difference between biotech and pharmaceuticals. The biotech industry uses biological processes rather than chemical processes.

- The clinical trial process is key. Clinical trials are expensive and success is not assured. Biotech investors often have to assess the probability of approval for a new therapy.

- Intellectual property affects profitability. Biotech companies, like pharmaceutical companies, have to make their profits before patents expire.

- Biotech also has non-medical uses. From biofuels to agriculture and materials, biotech processes have applications across multiple industries.

Biotech vs Pharmaceutical

Pharmaceutical companies are an offshoot of the chemical industry. They use chemical molecules to address health issues.

Biotechnology companies use biological compounds and processes to achieve their goal. This means that biotech products are much more complex than pharmaceutical drugs. When the average drug might be made of a few dozen atoms, a protein or a DNS strand will be made of tens of thousands, sometimes millions of atoms. Cell therapies even use entire cells, several billion times more complex than pharmaceutical products.

Because biotechnology is defined by its method first, it extends beyond healthcare applications. It can include the production of biofuels, bioplastics, fermentation, pollution control or remediation methods, farming technologies, etc. Still, the largest part of the sector is dominated by human health applications, as this is a very large and high-margin sector.

Because of the difference in its products, biotech can address problems that pharmaceutical companies could not. Notably, the industry went beyond industrial applications like fermentation when Genentech first produced artificial insulin. This invention would go on to save millions of lives.

Regulation and Clinical Trials

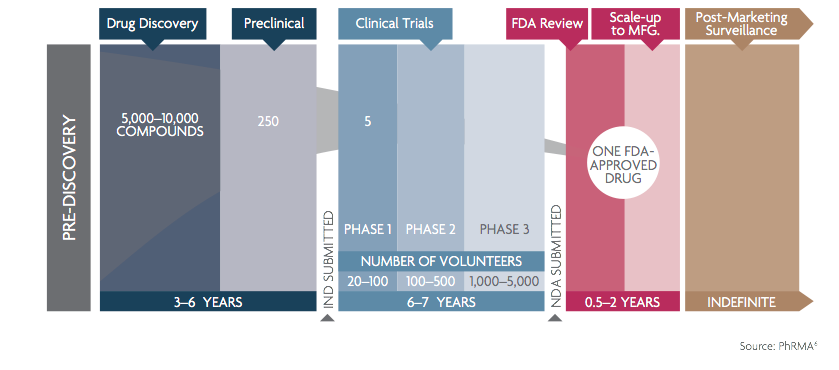

When it comes to human health, the process for biotech companies is very similar to the one followed by the pharmaceutical industry. Before reaching a patient, a new treatment goes through an extensive clinical trial. If the trials are successful, the FDA (Food and Drug Administration) may approve the new treatment.

I described each stage in more detail in the pharmaceutical industry primer, but here is a quick reminder:

Clinical Trials 101

To limit the risk of potentially lethal surprises, all new drugs must pass through a strict sequence of clinical trials. They go through the following successive phases:

- Preclinical: Tested on cells or animals only, to avoid a lethal error in human trials.

- Phase 0: Tested on just a few healthy humans, low concentration if possible, to check if animal and lab safety profiles apply to people as well.

- Phase I: Tested in a medically relevant concentration on a larger number of healthy people.

- Phase II & III: This is when actual patients suffering from a medical condition join the trials to determine the effectiveness of the product. The results of these tests determine whether the FDA will approve the product.

- Phase IV: Also called surveillance, this happens after the drug is approved. Ongoing surveillance aims at detecting any issues that were not detected in the clinical trials.

Intellectual Property and R&D

Both pharmaceutical and biotech companies rely heavily on patents to defend their innovations, acquired through prolonged and very expensive R&D.

Because biotech companies are usually built on scientific discoveries, the sector tends to be more startup-heavy than pharmaceuticals, which are dominated by huge corporations. This also results in the sector spending even more of its money on R&D than the pharmaceutical industry, with R&D spending typically in the 40%-60% range.

Most biotech startups will have one idea or technology they try to develop. The success of the company will therefore heavily rely on how solid the science is.

Because of this, this may be a field even more technical than classical pharmaceuticals. It also means that production can be a lot more complicated and expensive, unlike chemical drugs where the cost per unit excluding sales and R&D is very small. Because of the inherent complexity of the processes, biotech patents are also granted for a longer period than pharmaceutical patents.

On the good side, this reliance on unique technology has the advantage of making the competition a lot less intense than for classical drugs. Replicating the effect of a drug can be done with slightly different compounds, or even the same one once the patent expires. But a very complex protein or a proprietary cell line can be almost impossible to replicate or imitate.

Sales of chemical drugs are always at the mercy of generic drug manufacturers as soon as their patents expire. But biotech products are generally safer from patent expiration, even if the analog to generic drugs, biosimilars, exists.

Investing in Biotech

The key metric for most biotech companies will be their expected burn rate. Because most will be pre-revenue and spending on unproven treatments, they are far from making any money. The sector is usually first supported by VC (Venture Capitalist) money, and then by public capital after an IPO. A proper calculation of future costs and dilution of shareholders will also be important.

Due to this, the sector is also sometimes criticized for harboring too many “scam” companies, perpetually raising money before publishing disappointing results. I would not call this criticism completely unfounded, but it is often blown out of proportion. Incertitude is simply the price we pay for investing in such a speculative sector. Even the most honest companies and the most promising ideas can hit unexpected issues.

Another metric should be the size of the total addressable market (TAM). A treatment that may be used by 10,000 people per year has radically different profit potential from a treatment that could be used by 10,000,000 people a year. Of course, unrealistic TAMs are often the target of critics of the biotech industry.

For investors, an extra difficulty is that clinical trial results will often be binary:

Good = next phase can be launched or even better, treatment should be approved by the FDA soon.

Bad = this is a scientific dead end, and most of the money invested is lost.

Such binary outcome result in extreme volatility, with individual stock often going up or down by 30%-70% in a day, depending on how good or bad the latest published news are. This is definitely not a sector for the faint of heart or beginner investors.

Biotech companies are often very specialized on the scientific side. Most will prefer to keep advancing the science rather than handle the difficult task of commercializing the treatment themselves, which requires dedicated salespeople, contacts with doctors and hospitals, negotiation with health insurance companies, etc.

So it is quite common for successful biotech companies to follow one of these paths:

- Get acquired by a large pharmaceutical company.

- Sell the intellectual property for a specific discovery to a large pharmaceutical company.

- Sign a licensing agreement for the discovery, sharing future revenues in exchange for support on finishing trials and commercialization.

Many biotechs will search for such a partner just before phase III clinical trials, as this is the most expensive stage, but also the least likely to lead to failure. This reduces the risk for the pharma partner while avoiding dilution for the biotech’s shareholders.

Promising Sectors and Technologies

When looking for promising biotech, I feel there are a few fields more promising than others.

Orphan Diseases

Some diseases affect just a few people and have been so far impossible to treat well with conventional medicine. Treatments for such diseases are offered preferential pricing, or sometimes research grants and patent exclusivity by the FDA. Because they are not concerning a large population, it might also be a less competitive segment.

The main thing here is to look for truly innovative, life-saving treatment, usually leveraging a technology that did not even exist 5 years ago. If older technology could have solved the problem, it would have likely been done already. Still, stay aware that by definition, unproven new ideas will also have outcomes that are very hard to predict.

Very Common Unsolved Problem

I said the same for pharmaceutical companies, and it holds as well for biotech. Some sicknesses might be treatable with biotech, which can mimic, enhance or fully replace faulty biological mechanisms, instead of just chemically activating the body’s cells.

Some of the most promising sectors that are both unsolved and affecting millions of people are for example:

- Diabetes

- Alzheimer’s

- Parkinson’s

- Cardiovascular diseases

- Cirrhosis (liver damage)

- Dementia

- Paralysis

Successful therapies of any of these would be enormously profitable.

Non-Medical Biotech

Biotech is larger than medical applications. Other fields can offer very large potential markets with far less regulation.

Here is a list of sectors I think can be completely disrupted by biotech innovation:

- Biofuel production (notably from algae or cyanobacteria)

- Farming and Forestry (vertical indoor farming, biocontrol for crops diseases, soil biology, etc…)

- Material sciences (vegan alternative to leather, bioplastics, factory-made silk, recycling process, etc…)

Because they seem more “mundane” or “boring” compared to solving cancer or Alzheimer’s, these efforts could be more likely to provide undervalued stocks.

Specific Technologies

Lastly, a way to invest in biotech could be to focus on the promises of a specific technology instead of an application. For example:

- Genomics (a topic we covered extensively in our last Illumina report)

- RNA technologies: this includes mRNA vaccine and other RNA technology, but also RNAi.

- Cell therapy: using healthy or modified cells to replace deficient ones.

- Bioprinting: the artificial assembly of cells, tissues, or even full organs.

- Gene editing: this includes “trendy” tech like CRISP, and other methods to modify the genome of living cells as well.

- Synthetic biology: the creation of biomaterial or compounds not found in nature.

This is a strategy that lends investors who are quite well-versed in the science part of the equation, which might help them pick a winner in the sector.

Possible Investment Strategies

There are a few large independent biotechnology companies, notably Amgen, that have a diversified portfolio of new products in the R&D pipeline. The list can include also other companies we previously covered in our reports, notably Regeneron and Vertex.

Still, as most biotech investments will be for pre-revenue startups, diversification is crucial to building any biotech portfolio, especially when considering the very high failure rate of clinical trials. Untested technologies, new materials, biofuels, and other biotech products are equally risky.

In that respect, the biotech sector is very similar to VC investing. The idea is to spread the portfolio over dozens of different companies and aim for a few to do a 10x or x100 return.

The good news is that in 2022, biotech is rather out of favor, after a period of feverish speculation. This means that valuations are probably more reasonable than they used to be.

Another way to bet on biotech is to invest in pharmaceutical companies with a large biotech portfolio. For example, the first large biotech company, Genentech, is now part of Roche.

Or you could also bet on equipment manufacturers and suppliers to the industry. This can even be narrowed down to specific technologies, like genomics or cell therapy.

In any case, because of the highly technical nature of the industry, it will be best to either diversify massively (directly or through a fund or an ETF) or learn enough about the science to make more enlightened choices. Accredited investors might also back VC funds specialized in early-stage biotech startups.

Conclusion

The biotech industry is a highly profitable one as a whole. It is also growing very quickly and providing tremendous improvement to millions if not billions of lives. It also benefits greatly from the digital revolution, which provides access to cheap genome data, imagery, and computing power.

The difficulty for investors is that this profitability comes from extremely variable and hard-to-predict individual outcomes. So maybe more than finding the right individual idea or making a good analysis, biotech investors will need to sharpen their risk management skills.

Nevertheless, this can be a highly rewarding sector. Biotech companies are also not particularly sensitive to overall economic conditions, as most of the sector income is from health insurance payments or niche industries.

Valuation and enthusiasm for the sector are known to ebb and flow over long 5-10 year cycles, so a degree of market timing can help as well. If biotech valuations are reaching an all-time high across the board, better stay away for a bit.

Currently, biotech valuations remain in a slump, so this might be the time to pay attention again to the sector, especially considering a generally gloomy macro outlook.

Industry Primers

The process of analyzing a company varies considerably from industry to industry. Many industries have their own vocabularies and specific concerns that investors need to consider. This series of articles looks at specific industries and at industry-specific factors that affect investments. The goals are to highlight specific risks, clarify confusing terminology and explain industry-specific metrics for valuation. These methods complement the usual evaluation process, they don’t replace it.