Aging populations and health crises like the COVID-19 pandemic have kept attention on the pharmaceutical industry. Pharmaceutical products are at the core of modern healthcare and save lives daily, creating sustained and growing demand and high levels of profitability.

The greatest wealth is health.

Virgil

This is often a sector avoided by retail investors, as it feels overly complex. It also shows some attributes of a hated sector: “Big Pharma” is right up there with oil companies and banks as one of the most disliked industries in the country.

This industry primer will explain the basics of investing in the pharmaceutical industry.

Key Takeaways

- Know what the pharmaceutical industry does. This is a separate sector from related industries like medical devices or biotech. Understand the distinctions before investing.

- Understand the clinical trial process. Clinical trials are expensive and many products are not approved. Understanding the process and its risks is essential to successful investing.

- Patents matter. Once a drug is off-patent its profitability declines immensely. Knowing when a company’s major products come off patent is critical.

- The pharmaceutical industry is non-cyclical. Demand for medicines remains constant despite economic conditions.

What Are Pharmaceutical Companies

Pharmaceutical companies produce drugs for the benefit of human health. Pharmaceuticals are usually considered separate from other health-related industries, like manufacturers of medical items, referred to as “medical devices” (pacemakers, prostheses, diagnostic tools, surgery equipment, etc…), or veterinary medicines.

The biotechnology sector is also usually considered a separate sector. The difference is that the pharmaceutical is an outshoot of the chemical industry. It synthesizes or purifies artificially different drugs/molecules to solve medical problems. Biotech uses biological processes.

So drugs and pills will be considered pharmaceuticals, but gene therapy, antibodies, and stem cell treatments will be biotech. Of course, the line between the two can be blurred, like with mRNA vaccines for example, and there will inevitably be some overlap.

Regulation and Clinical Trials

The pharmaceutical industry evolved progressively with medical science. From often ill-conceived primitive remedies, the sector progressively became more scientific in its approach. This also means the industry has a long history of mistakes or treatments that were discovered to be dangerous in retrospect. To add to this, the difference between helpful and harmful treatment can be pretty thin, depending on the patient and dosage.

The dose makes the poison.

Paracelsus

The history of medical errors has led to an extremely high level of regulation. In the US, these regulations are under the control of the Food and Drug Administration (FDA). Pharmaceutical companies sell their products all over the world, so they also have to pass the scrutiny of regulators in other markets, who often have different standards.

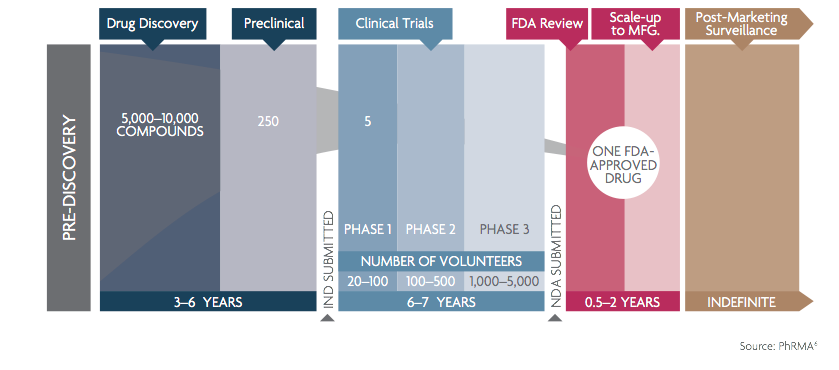

Clinical Trials 101

To limit the risk of potentially lethal surprises, all new drugs must pass through a strict sequence of clinical trials. They go through the following successive phases:

- Preclinical: This is the phase where the potential drug is tested on cells or animals only. This is done to detect problems early and assess the potential for medical treatment. It comes after the drug discovery, which tests thousands of molecules for possible medical effects.

- Phase 0: The drug is given in small doses to a few (less than 10-15) healthy people to see how humans react to it. This is to test the potential toxicity of the compound.

- Phase I: The drug is now given to more healthy people in the expected concentration needed to treat patients. Here too, the goal is to assess the toxicity risks first.

- Phase II & III: This is when actual patients suffering from a medical condition join the trials. Phase II has generally a few hundred participants. If phase II is promising enough, the product moves to Phase III, with several thousand participants. This is also when the ideal concentration and treatment method are determined. Approval of the drug by the FDA will depend on Phase III results. In general, the company needs to prove that the new drug offers superior benefits compared to existing treatments.

- Phase IV: Also called surveillance, this happens after the drug is approved. It involves tracking over several years, or even decades, thousands of patients, to detect any problems that could have not been found during the previous phases.

Trials and Investing

Because each clinical trial phase can spell the difference between marketability and doom for a new drug, investors tend to follow them very closely. They are also extremely expensive.

The success rate of trials can vary greatly depending on the specialty. In any case, a failure rate (as defined as “not being approved by the FDA”) of 70-90% is the norm. It can be as high as a 96.6% failure rate for oncology drugs (treating cancer).

Probability Of Success2 by Clinical Trial Phase and Therapeutic Area

| P1 to P2 | P2 to P3 | P3 to Approval | Overall | |

|---|---|---|---|---|

| Oncology | 57.6 | 32.7 | 35.5 | 3.4 |

| Metabolic/Endocrinology | 76.2 | 59.7 | 51.6 | 19.6 |

| Cardiovascular | 73.3 | 65.7 | 62.2 | 25.5 |

| Central Nervous System | 73.2 | 51.9 | 51.1 | 15.0 |

| Autoimmune/Inflammation | 69.8 | 45.7 | 63.7 | 15.1 |

| Genitourinary | 68.7 | 57.1 | 66.5 | 21.6 |

| Infectious Disease | 70.1 | 58.3 | 75.3 | 25.2 |

| Ophthalmology | 87.1 | 60.7 | 74.9 | 32.6 |

| Vaccines (Infectious Disease) | 76.8 | 58.2 | 85.4 | 33.4 |

| Overall | 66.4 | 48.6 | 59.0 | 13.8 |

| Overall (Excluding Oncology) | 73.0 | 55.7 | 63.6 | 20.9 |

With such high failure rates, most investors will be better off investing only in one of the largest pharmaceutical companies (nicknamed “Big Pharma), which have dozens of commercialized molecules and hundreds in trials.

Small companies with only a few compounds in the trial process run the risk of ending up with no marketable product or not having the resources to complete their trials.

Even the scientists directly designing the clinical trials are unable to forecast the outcomes with any degree of certitude. So I would not recommend relying on predictions of clinical trial results, even though this is common among pharma and biotech analysts. People with a stake in a company want a positive clinical trial result, and that desire can easily cloud judgment.

Intellectual Property and R&D

One key difference between pharmaceutical companies and other sectors is their reliance on intellectual property. Patents for drugs have their own rules, which can be rather complicated.

Normally, pharmaceutical companies will communicate clearly when their patents for each commercialized drug are expiring. After that, competitors can start producing “generic” drugs, using the same molecule but without incurring all the R&D and clinical trial costs. The selling price approved by the FDA might also change once the patent expires.

A pharmaceutical patent lasts for 20 years, but must often be registered during clinical trials, so 5-10 years can be “lost” before commercialization. The registration date of the patent can also vary depending on the region, for example being 2 years later for EU markets than in the US.

It should be noted that in most cases, the patent can be prolonged by a few years, using some of the drug-specific rules of intellectual property law. This is especially true if the drug is saving lives, targets a small number of patients, or is especially innovative and unique. You can learn more about patent expansion strategies here.

As a rule of thumb, profits drop 60%-80% as soon as a drug loses patent protection. This is less true for drugs addressing a very small niche or chemically very complex, as competitors might not bother to set up an entire production facility for a small market.

A company that depends on a few “blockbuster drugs” (drugs that generate $1 billion or more in annual sales) may see its valuation drop steeply as the patents on those drugs near expiration, especially if they don’t have new potential blockbusters in the pipeline.

R&D (which includes clinical trial costs) is unavoidable for the continuous operation of a pharmaceutical company. In such an innovative sector, R&D costs should ideally be listed in the income and cash flow statements as a recurring cost, not as an investment or CAPEX.

Promising Sectors and Technologies

In today’s market and regulatory environment, I feel that the highest chance of financial success is at 2 ends of a spectrum.

On one hand, the very niche, rare diseases with no good treatment, or no treatment at all. Because they are usually deadly or generally horrible afflictions, national insurance policies and regulators are ready to effectively subsidize research in the field and give higher selling prices and longer patents. And because they are complex diseases and small markets, competition is often reduced for such “orphan” diseases.

On the other hand, treatment for very common problems with no good treatment yet could become the new generation of blockbuster drugs. For example:

- Diabetes

- Alzheimer’s

- Parkinson’s

- Hypertension

- Cardiovascular diseases

- Cirrhosis (liver damage)

- AIDS

- Dementia

- Paralysis

- Flu (not sure I really need to add this one…)

Any reliable treatment for any of these issues will bring (well-deserved) tens of billions in profits.

Investors pay a lot of attention to oncology (cancer). Cancer drugs can be legally sold at incredibly high prices and curing any type of cancer would be a big money maker. This is also the field with by far the worst trial success rate. This is because cancer is not a single disease: it is more like 1000 different related diseases. So I would warn of caution in investing in this field. Success would be highly rewarded, but it’s also a very low probability.

Possible Investment Strategies

As I said before, diversification is an absolute must in a sector where new products cost billions in R&D and end up at a dead end 70%-95% of the time.

One way to get that diversification is to stick to large companies. They will have a lot of products commercialized and many ongoing clinical trials. Here, buying at a good price will be the most important. You can find here the top 20 largest pharmaceutical companies by revenue.

Another way is to specialize in one pathology or specialty. Even non-doctors or biologists can develop considerable expertise in one narrow field. That knowledge might give you an advantage in judging what method could solve the problem and the best companies in the sector. By betting on several companies all focused on one pathology, you increase your chance to grab a share in the winner that grab this new market.

You could also buy a very large portfolio of multiple smaller pharmaceutical companies. By spreading the risk large and wide, you can capitalize on the success of the pharmaceutical industry at large, while still benefiting from the growth of small caps. Dedicated ETFs can provide help for this method.

Lastly, you can focus on generic producers. These less glamorous than innovative companies are still saving lives and generating profits. They can be cheap at times and are not exposed to patent expiration problems or large R&D costs, and uncertain trial results. If they are well-run and cost-efficient, they can be very good businesses selling somewhat commodified products.

Conclusion

The pharmaceutical industry is a large part of the global economy and should not be ignored by investors. It is also a sector that is relatively defensive, not really in sync with the market cycles. Medicines are an inelastic cost: even if they get more expensive, people still buy them, because health is always a top priority. Even during a recession people still get sick and need treatment.

The pharmaceutical industry benefits from secular trends like aging populations in developed countries (older people use more medicines) and improving access to modern healthcare in developing nations.

Extensive knowledge of medicine or biology can be an advantage but is not required. Experts might also be tempted to overestimate their knowledge and try to forecast clinical trial results. This is a very risky and uncertain endeavor.

A safer approach is to diversify enough, either through major “big pharma” companies or a large selection of smaller companies. If you think one specific medical problem is more likely to be solvable soon or more profitable, you can also specialize your pharma investment in this field.

In any case, I hope this article helped to demystify investing in the pharmaceutical sector and encourage you to give it a second look!

Industry Primers

The process of analyzing a company varies considerably from industry to industry. Many industries have their own vocabularies and specific concerns that investors need to consider. This series of articles looks at specific industries and at industry-specific factors that affect investments. The goals are to highlight specific risks, clarify confusing terminology and explain industry-specific metrics for valuation. These methods complement the usual evaluation process, they don’t replace it.