America does a lot of things well. Our military, blockbuster films, and cheeseburgers are second to none. However, our healthcare system leaves a lot to be desired. In 2019, we spent 42% more on healthcare per person than the closest runner-up (Switzerland), yet our average life expectancy is a full five years lower.[1, 2] To make matters worse, we’ve tangled our health insurance systems almost inextricably with our employment system. It’s much more expensive (and complicated) to get health insurance while self-employed or in early retirement.

If you don’t fit into the traditional employment model but aren’t old enough to qualify for Medicare, you’ll have to slog through buying long-term health insurance for yourself. This guide will help you navigate the system effectively and set yourself up for success. Here’s what you need to know to get health insurance while self-employed.

Understanding Health Insurance Plans

There’s a lot of jargon and confusing acronyms involved in selecting a health insurance plan. If you don’t understand what they all mean, the process can get overwhelming. Here are the terms you need to know to interpret what each plan has to offer.

Numbers to Watch Out For

Health insurance is a numbers game. You want to find the plan that will get you the coverage you need and cost you the least amount of money in the long run. To do that, you have to know all the different ways that a plan can cost you. Here are the numbers to pay attention to:

- Premiums: These are the monthly fees you pay to benefit from the coverage. Whether or not you use any services, you’ll have to pay the premium each month you retain the insurance.

- Copays: These are the flat fees you’ll have to pay for covered medical services. For example, you may pay a $25 fee for visits to your primary caregiver.

- Deductibles: This is the maximum amount you’d have to pay for covered health services before the insurance company pitches in. For example, you may have to pay the first $3,000 of service costs yourself before they start helping.

- Coinsurance: This ratio explains how you’ll split with your insurance provider after reaching your deductible. For example, your insurance provider might cover 80% of the subsequent costs while you cover 20% until you hit your out-of-pocket maximum.

- Out-of-pocket maximums: This is the most you’d ever have to pay in a year for healthcare. Once you reach it, you no longer have to open your wallet for further services or copays.

☝️ Make sure to consider all of these terms when comparing various health insurance plans and not just the monthly premium. If you end up requiring services, your deductible will be just as significant for calculating total costs.

👉 A Sample Medical Bill:

To put all of the health insurance terminologies into perspective, let’s take a look at how they’d apply to an example of a medical bill.

Imagine that John goes in for a doctor’s visit because he’s experiencing increasing discomfort in his abdomen. It’s his fourth visit for the year, which isn’t covered by his insurance, so he pays a $30 copay on arrival.

The doctor examines him and gives him the bad news: He has appendicitis, and they’ll have to remove his appendix to fix the problem. All in all, those services cost $5,000. Fortunately, his deductible is $2,500, and his out-of-pocket maximum is $2,800. His coinsurance split is 80% for his insurance company and 20% for him.

John would end up paying the entire first $2,500 of his bill, thereby meeting his deductible. After that, he would owe just 20% of the remaining $2,500, which is $500.

However, his out-of-pocket maximum limit is $2,800, and he’s already paid $2,530 so far for the deductible and the copay. Therefore, he would only have to pay $270 of that $500. The insurance company would cover the remainder and any future expenses for the year.

John’s insurance plan:

Deductible: $2,500

Coinsurance split: 80%/20%

Out-of-pocket maximum: $2,800

John ends up paying:

Copay: $30

Deductible: $2,500

Coinsurance: $270

This is the way things work when everything goes as expected. That doesn’t always happen. Insurance companies will often do all they can to avoid paying some parts of a bill. You need to read the fine print to check on possible non-covered expenses, and you may have to negotiate with your insurance company to get the full coverage you paid for.

Common Types of Health Insurance Plans

There are four common types of health insurance plans. The specific terms will vary between plans and providers, but these are the general characteristics you can expect from each of them.

| General Function | Need Referral to See Specialists? | Size of Monthly Premiums | Coverage for Out-of-Network Care? | |

|---|---|---|---|---|

| Health Maintenance Organization (HMO) | Work with a primary care physician (PCP) who coordinates everything | Yes | Lowest | Only in Emergencies |

| Point of Service (POS) | Similar to an HMO, but with access to out-of-network providers | Yes | Lower | Yes, with slightly higher copays |

| Exclusive Provider Organization (EPO) | No PCP; can only see doctors in-network, but the network is larger | Usually no | Higher | Only in Emergencies |

| Preferred Provider Organization (PPO) | Select any doctor at any time; pay extra for out-of-network care | No | Highest | Yes, with slightly higher copays |

Generally, you’ll probably want an HMO if you’re young, healthy, and need little in the way of healthcare. If you’re already fighting an illness and think you may need help from specialists, you might want to pay higher premiums for the increased flexibility of a PPO. Not all plans of the same type are equal, though, so do your due diligence.

Don’t forget to take into account whether a plan offers a Health Savings Account (HSA). These are uniquely powerful tax-advantaged accounts that give threefold tax savings. You get a deduction for contributions, the growth within them is tax-free, and you’ll pay no tax on distributions for health-related expenses.

Even if your health insurance plan doesn’t offer an HSA, you can open one through a separate financial institution, as long as your plan qualifies as a High Deductible Health Plan (HDHP). That just means that their deductibles and out-of-pocket maximums fall within certain thresholds.

💡 Using an HDHP and an HSA together is a powerful option for young people with few healthcare needs that want to put away money for use later in life.

Levels of Coverage

The type of health insurance plan isn’t the only choice that will affect your total healthcare costs. There are different levels of coverage available for each type of plan. They are:

- Bronze: These come with the lowest monthly premiums, highest deductibles, and the least favorable coinsurance splits. They’re best for people who don’t think they’ll need much care but want to protect themselves from worst-case scenarios.

- Silver: These are the most balanced health insurance plans. They have moderate monthly premiums, moderate deductibles, and reasonable coinsurance splits.

- Gold: These are for people who are willing to pay high monthly premiums in exchange for much lower costs when they need healthcare services.

- Platinum: These are the plans with the most expensive monthly premiums and the lowest costs when you need care. If you know you’re going to be using a lot of expensive services during a year, you may want a platinum plan.

Catastrophic plans are another option, but they’re only available to people under 30 or those who meet certain hardship exceptions. They’re comparable to Bronze plans with low premiums and high deductibles, but you can’t apply tax credits to reduce their premiums like you can with the “metal” plans. Speaking of taxes, let’s take a look at how that works.

💁♂️ Need help getting started in your search? Read our list of some of the best insurance providers for self-employed individuals.

How to Reduce the Cost of Health Insurance

Health insurance costs are daunting at first glance, but they don’t have to break the bank. For starters, as a self-employed individual, you can take a tax deduction for the monthly premiums you pay. That automatically discounts the cost of your monthly premium by your marginal tax rate.

👉 For example:

If you earn $50,000 as a single filer in 2021, your marginal tax rate would be 22%.

If you were to pay $5,000 in health insurance premiums for the year, it would reduce your adjusted gross income (AGI) by the same amount.

So while you’d lose $5,000, you would also save $1,100 in taxes.

Because of the Affordable Care Act (ACA), you can take a credit against your monthly premium for certain plans if your AGI is below 400% of the federal poverty level. The lower your income is (all the way down to the poverty level), the cheaper your premiums can be.

In 2021, the poverty level is $12,880 for a single person. If your AGI is below that threshold, you’ll pay no premiums for governmental health insurance. If it falls between that and $51,520 (400% of the poverty level), you can receive a partial discount. Visit the Marketplace’s tool to see if you’ll qualify based on your household and income.

📘 Learn More: Still a little unsure of how the tax system works? You have to understand the fundamentals if you’re self-employed. Take a look at our introduction: Taxation 101: How Do Taxes Work For Individuals?

How to Get Health Insurance While Self-Employed

1. Visit the Marketplace and Private Exchanges

To get health insurance while self-employed or working as a freelancer, you can purchase a plan from one of two places:

- Healthcare.gov: This is the national exchange sponsored by the government. You can visit it to purchase a plan through the federal or a state marketplace.

- Private exchanges: If you’d rather get coverage from a private exchange like eHealth or directly from an insurance company like Aetna, you can. Their plans are still up to the Affordable Care Act’s standards.

Generally, if you qualify for a subsidy due to your income levels, you’re probably going to want to go through Healthcare.gov. All the plans there are available for premium reductions, while those that are on private exchanges or from private insurance companies might not be.

I’ll use the Healthcare.gov site as an example for this walkthrough.

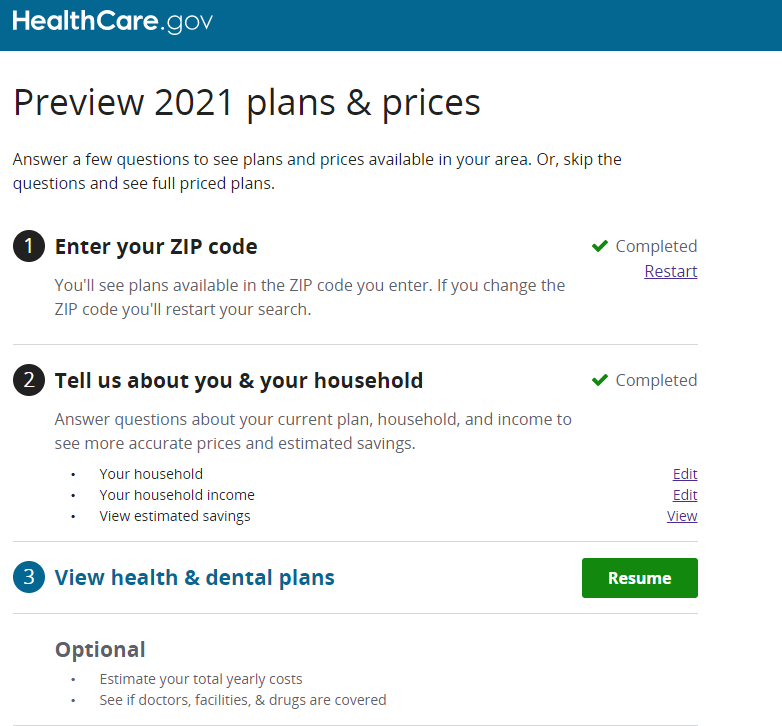

2. Search for Local Plans

Coverage options and regulations vary significantly from state to state, and you’ll need to purchase one with a network near you. If you’d like to browse the plans available without committing just yet, visit Healthcare.gov’s preview page and enter your zip code.

3. Provide Your Personal Details

Whether you use Healthcare.gov or a private exchange, you’ll have to share your age, the number of people in your household, whether or not you use tobacco, and your estimated annual income.

The exchanges will use that information to estimate your premiums for each available plan. Note that it will be cheaper to cover multiple household members than just one.

4. Calculate Your Premium Reduction

If you can estimate your AGI for the coming year, you can get a good idea of whether you’ll qualify for a premium tax credit. If your income is too high, you may want to contribute to a tax-advantaged retirement account like a Solo-401k to get your AGI under the threshold.

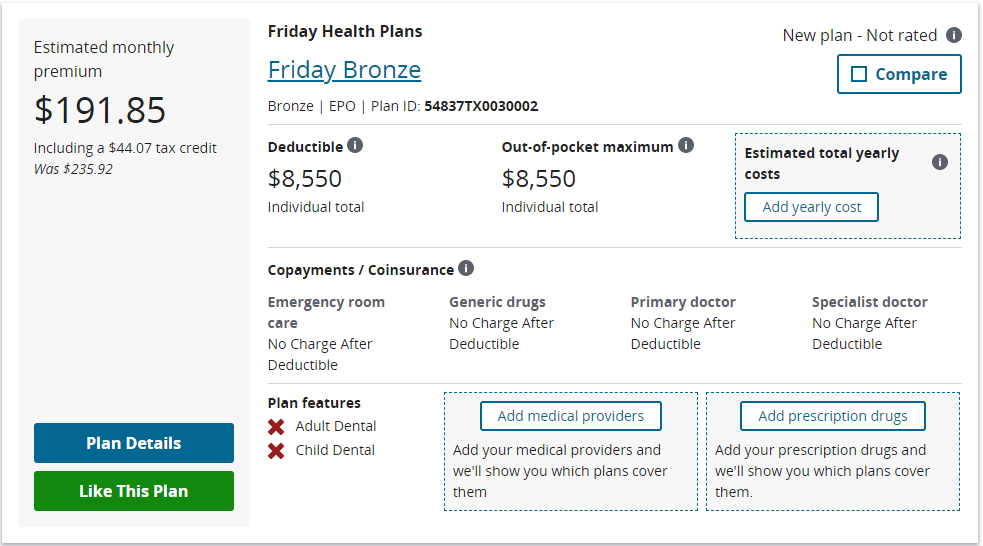

5. Optimize Your Options

Sort through the plans to find the best deal for you. You’ll want to keep the total yearly cost as low as possible, so make sure you estimate that based on what you expect your usage to be. If you have a doctor that you like and want to keep working with, confirm that they’re in a plan’s network before committing to it too.

💡 Pro-tip: On the Healthcare.gov website, you can estimate the total annual cost of a plan based on your expected level of healthcare use. Make sure to enable that feature to help compare plans.

6. Register During an Open Enrollment Period

You can only register for a health insurance plan during specific windows. An extension due to COVID-19 allows you to enroll through August 15th, 2021, for the current year. If you miss the deadline, you can’t get coverage unless a qualifying event triggers a Special Enrollment Period for you.

Don’t Be Afraid to Get Help

Frankly, our health insurance process is unnecessarily complicated. It’s all too easy to miss a discount, pay more than you need, or buy the wrong type of coverage. You don’t know what you don’t know, and there’s a lot that can go wrong with health insurance.

Given the high stakes involved, it’s not an area that you can afford to make mistakes. If you need to get health insurance while self-employed, don’t try to figure it all out on your own. Reach out to a health plan advisor or two and get their opinions. Let them walk you through the process so you know you’re getting the best deal and the coverage you need.