March 6th, 2021

Quick Stock Overview

Ticker: CO

Source: www.stockrover.com

Key Data

- Sector: Healthcare

- Sales ($M): 179

- Industry: Diagnostic and research

- Net Cash per share: $7.47

- Market Capitalization ($M): 583

- Equity per share: $5.40

- Employees: 1,260

Summary

Global Cord Blood, or CO, is a surprisingly attractive business. I will explain more in detail below, but frankly I was wondering what I am missing when I found it. The price is really low, its growth potential is enormous, net margin is very high, debt is nonexistent, and so on.

So, what’s the catch? I have spent most of my time researching data for this report trying to answer this question. I actually failed to find anything solid like seemingly shady accounting, dishonest management or so on.

So again, what’s the catch? The main issue with this stock is that while it is listed in America, it is a purely Chinese company. And to some extent, this means we have to take at face value the numbers we are given regarding their Chinese operation. A series of accounting malpractices, deceptions and outright frauds have come out of popular publicly traded Chinese companies, so it is a risk you will need to remember while reading this report.

But some bad apples does not mean that all Chinese companies are dishonest or shady. No more than Enron meant that all US companies were dishonest. We just to be reasonably cautious and careful when dealing with overseas operations.

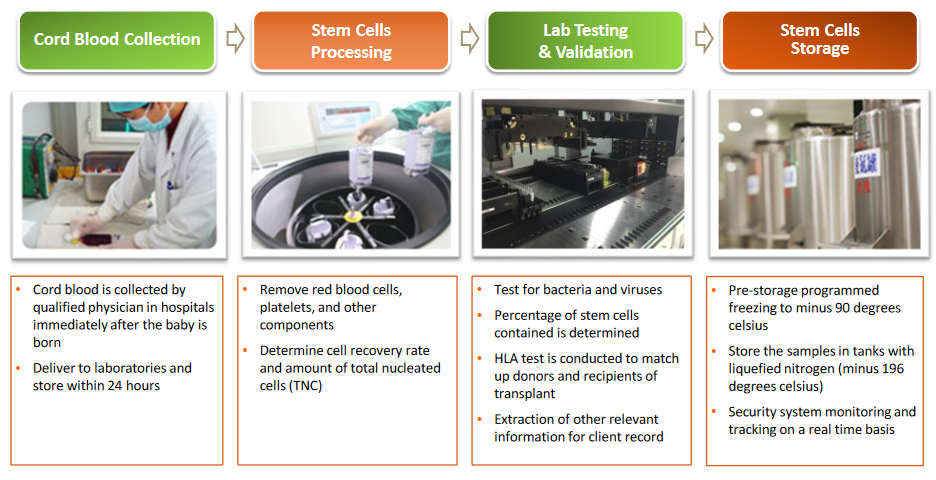

But let’s leave out the China question for a minute and look at what CO does. It collects, prepares, and stores stem cell from umbilical blood, collected at the moment when a baby is born. While the cell preparing might seem complex, this is a standard and well-established procedure in medical labs, so nothing overly complicated.

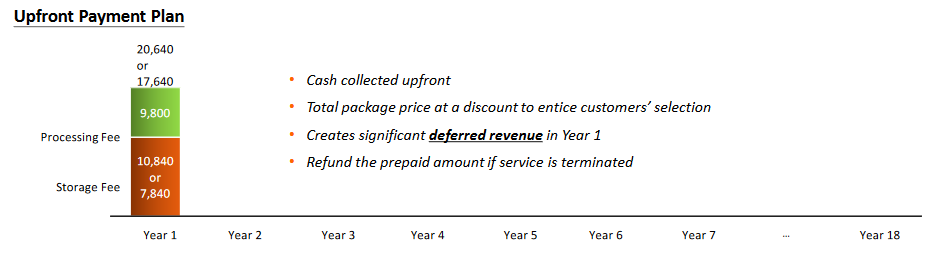

The happy parents pay upfront to have the cells preserved and stored away, and then pay a yearly fee to have it kept frozen and safe. In that respect, the blood cord bank acts as an insurance company, keeping potentially lifesaving samples stored away in case the child might need it in the next years. The samples are stored for 18 years, until the child gets ownership of the biological samples.

Source: ir.globalcordbloodcorp.com

Source: ir.globalcordbloodcorp.com

This is a really simple operation, and CO does not have other activities, so it is pretty straightforward to understand how the company makes its money. If the salary of nurses and doctors and administrative staff + cost of keeping the samples + cost of client acquisition is lower than their revenues, the company is profitable. And you will see, it is indeed very profitable.

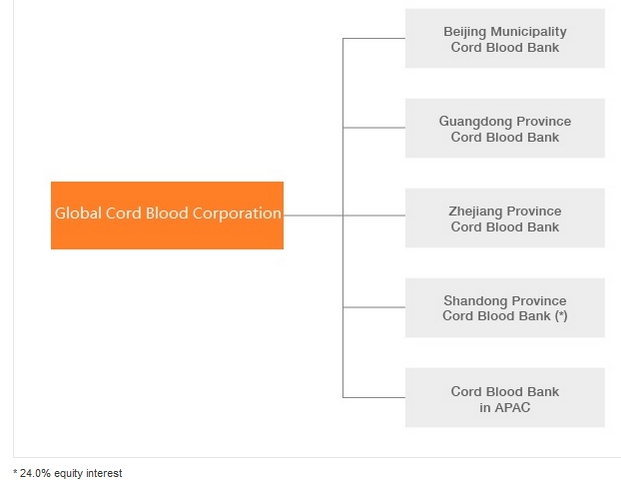

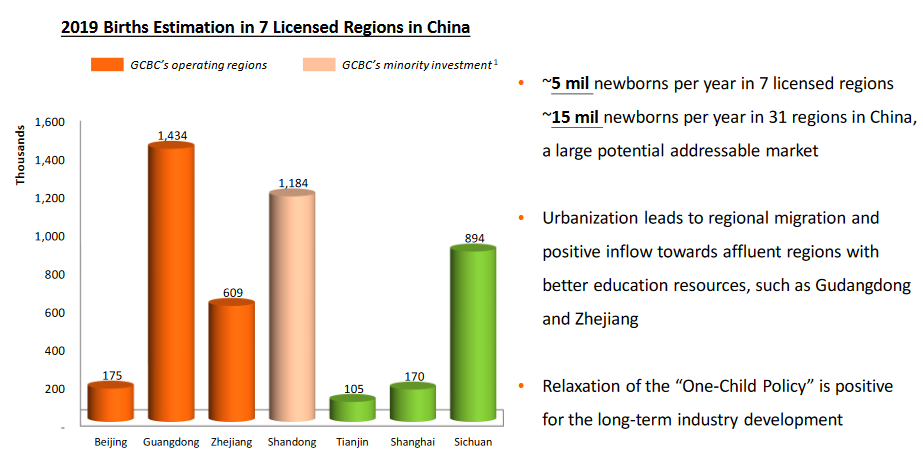

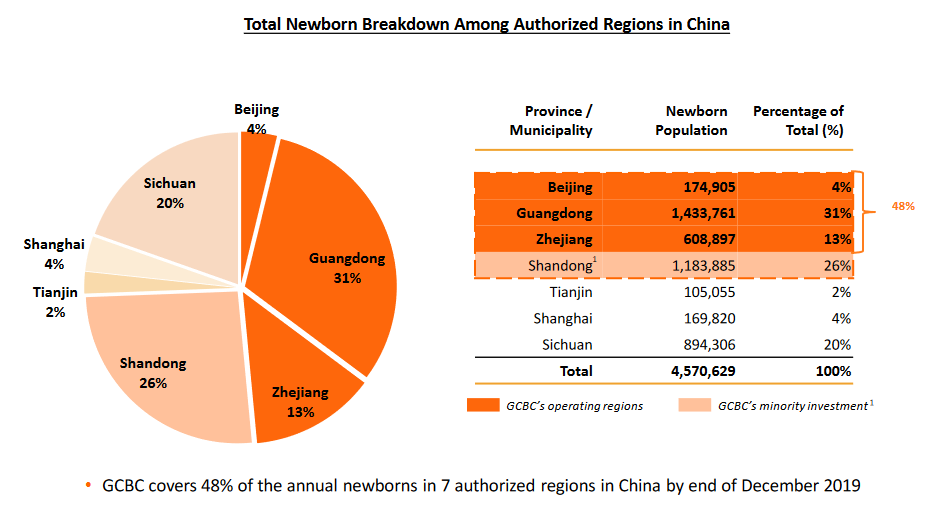

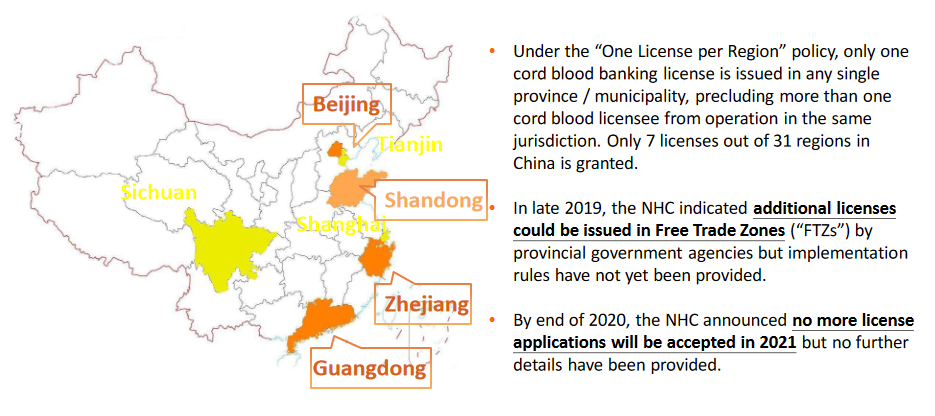

CO is the first and largest operator of cord blood bank in China, and the only operator with licenses in multiples provinces, holding 3 out 7 of the licenses available in China.

Source:ir.globalcordbloodcorp.com

Strategic Analysis

CO has been growing steadily in this new healthcare sector, and is the market leader in China, but still has a lot of room to grow.

A Growing Medical Potential

Cells found in the umbilical cord, or cord blood, are unique in their ability to evolve into all blood cell types. Such cells are also called stem cells. This makes cord blood a potentially powerful treatment for a large variety of blood diseases, from cancer like leukemia to many genetic diseases. By being from the baby’s body itself, it also has very low risk of allergic rejection compared to transplants from donors.

Blood cord treatment is at the very edge of modern medicine and medical research and is considered as a potential cure for many debilitating or deadly afflictions. In 2019, 50,000 cord blood units have been used for actual treatment, and progress in treatments is likely to increase that number several fold over the next decades. At the moment up to 75 diseases can be treated with cord blood stem cell / hematopoietic stem cell transplants.

The company itself provides more information about the medical potential of cord blood and a useful FAQ.

A Large Addressable Market

At the moment, CO has 882,982 subscribers to its services, up from 833,094 at the end of the 2020 fiscal year. It is worth noting that despite COVID, 84,000 new subscribers registered in the company in 2020, showing the resilience of the business in a very troubled year.

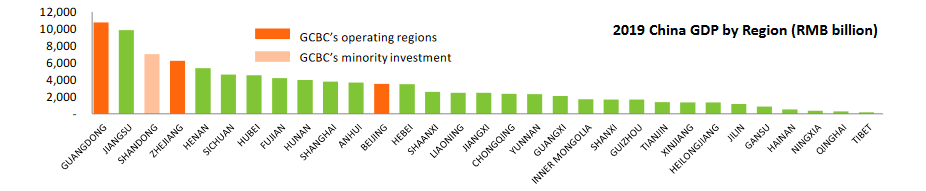

The markets they operate in see no less than 2 million newborns every year in Beijing, Guangdong, and Zhejiang. These regions are among the richest in China and also the ones with the most births.

Source: ir.globalcordbloodcorp.com

So only 4% of prospective parents have used CO services so far, a number that could easily double or triple over the year. This is due to both rising standard of living among the Chinese middle class, but also changes in social structure.

The one-child policy has made families increasingly focus on the well-being and health of the only child of the family. The progressive elimination of the one-child policy is likely to increase natality in the long run (a positive for CO) but the deep changes to culture it induced will likely be long lasting.

Source: ir.globalcordbloodcorp.com

Source: ir.globalcordbloodcorp.com

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

CO is an extremely predictable and stable business. Advances in medicine and increasing disposable income ensure a growing interest in the services and capacity to pay for it.

The retention rate for such services are extremely high worldwide, as worried parents are unlikely to give up the relatively cheap subscription once they paid a large sum upfront and have been convinced their child health might depends on keeping the cord blood stem cells frozen.

Economic Moats

In value investing terms, Global Cord Blood has several economic moats:

Official Licenses

We will discuss it more in detail in the competition part, but any competitor would need to get a license to operate to even be authorized by the Chinese government to compete with CO. It is possible that more licenses are one day attributed to newcomers in the market, but this does not seem likely in the foreseeable future.

Substitution cost

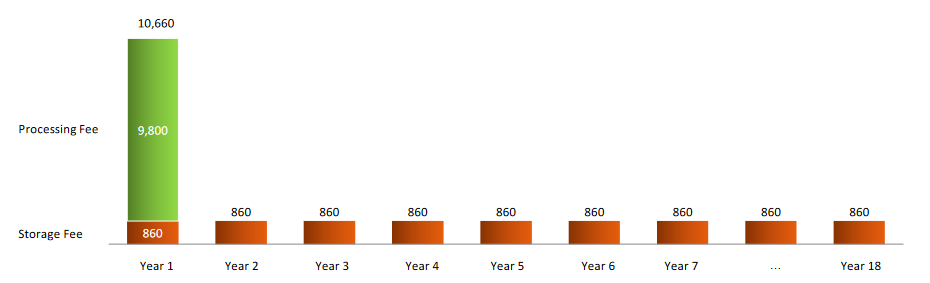

Put yourselves in the shoes of parents who have purchased CO services. You now know that your baby cord blood has been processed and safely stored away in case some truly scary diseases strike. Even if a new company would offer you a cheaper yearly subscription, would you be sure you can trust it? Would you really change operator to save a ¥100 per year? The yearly subscription cost ¥860 yuan, or $132/year, just $13/month.

Are you going to go through the trouble to get your baby stem cells transferred and potentially endangered for the cost of a few coffee cups per month? I doubt it.

Between the emotional incertitude and mental cost, the overwhelming majority of parents will not change supplier and will stick to their contract with CO, even if they moved to another province.

Scale

Overall, CO operations are simple. It needs some standard equipment for most medical labs, and the prepared samples are kept frozen in large freezers that need monitoring systems and multiples back-up generators, surveillance personnel, etc.

The costs for such labs and storage facilities with extensive backups are rather fixed. Costs for 100,000 samples are not 10x the cost for 10,000 samples. CO does not breakdown its cost structures, but I assume that for the example above, 10x more clients would only increase cost by 2-3x.

Management

For overseas companies, management is a key component to judge if you should trust the company. Unknown or unqualified board members and chief officers are a big red flag for a company that would not operate legitimately. Frequently changing management, multiple members of the same family without the company being a family business can also alert the savvy investor of nepotism or skeletons hiding in the closet.

CO offers detailed information about its management. The key members are:

Ms. Ting Zheng, CEO: In charge since 2003. She was before involved in the IPO of Golden Meditech and before that she worked in an accounting firm.

Mr. Bing Chuen Chen, CFO: Former Vice president of Golden Meditech and before that an analyst in the biotech sector. He has a degree in commerce from Queen’s University, Canada.

Ms. Xin Xu, Chief Technology Officer: Lecturer in cryobiology at Beijing Medical university and research in cryobiology for 20 years before joining CO.

Diplomas and experience wise, the management is maybe not really stellar, but there are no red flags either. The results achieved by CO seem to indicate that if they are not as flamboyant as Elon Musk, they know how to run the company’s operations efficiently.

Ms. Xu’s background in cryobiology (biology of extreme cold and freezing of biological samples) is reassuring to know that the samples are properly processed and stored.

At first, I was suspicious of the recurrence of Golden Meditech in the background of the management. It might have meant conflict of interests or back dealing we would not be aware off. But upon further research, I discovered that CO is actually a spin-off company of Golden Meditech.

So, it does make sense that CO management is simply composed of the former Golden Meditech branch management for its cord blood division.

The connection to Golden Meditech is however not really severed. As far as I know, Golden Meditech is still a major shareholder in CO, but I could not find the exact number. The relation to Golden Meditech will also have an impact on the future strategy of CO, as I will explain more below regarding a possible fusion with Cordlife.

Competition

The Chinese market is rather concentrated compared to North America or the EU.

This is due to the need of special licenses, and that the Chinese government prefers to have a handful of companies operating and becoming market leaders. Actually, the government has decided to have only one license per region and such policies are likely to change only very slowly, if at all, considering China’s political functioning.

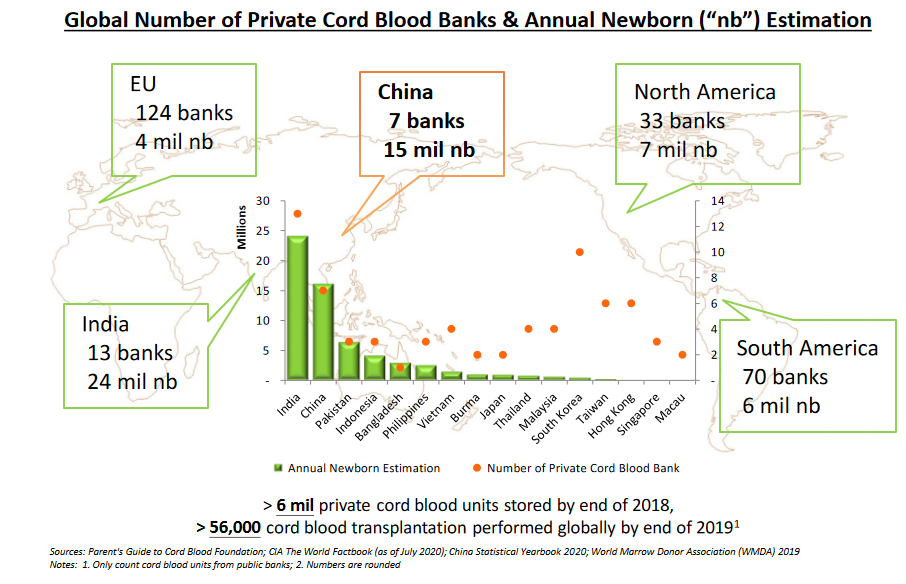

It is worth to notice that 10 million babies are born in the 24 regions without licenses for cord blood sampling at the moment. CO having obviously good relations with Chinese health authorities, extra licenses would allow it to grab some of these markets too in the near future.

Future Fusion with Cordlife?

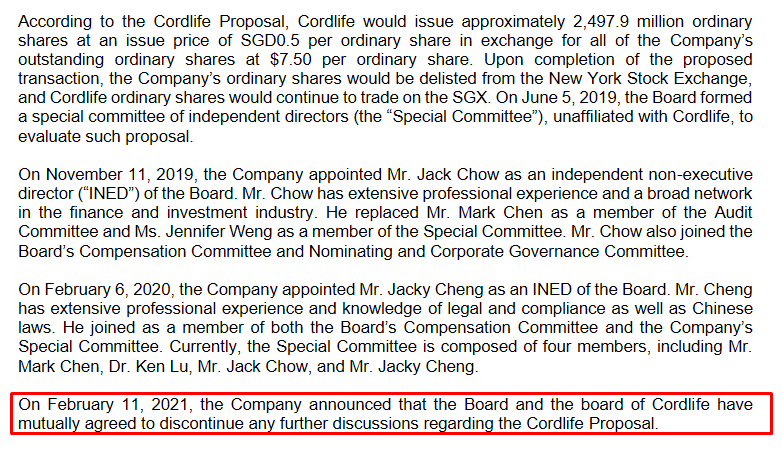

Since mid-2019, CO is in discussion with Cordlife for a merger of the two companies. Cordlife is a company very similar to CO, offering cord blood bank in Hong-Kong and multiple South-East Asian countries. Its largest shareholder is Golden Meditech (owning at least 18.9%). So, I was a little wary of conflicts of interest and undisclosed conflicts of interest between CO’s managers (former Golden Meditech) and Cordlife (owned partially by Golden Meditech).

The discussion was initiated by Cordlife, which looked to expand its operations by enter the largest Asian market. Due to the limited license number, the only way for Cordlife was through acquisition/merger, and CO as the largest Chinese operator was the logical target.

But good news, it seems that CO will stay independent after all. An independent committee was formed and on 11th February 2021, the respective boards of the two companies have decided to give up the merger talk.

Beyond the possible accounting malpractice from the location in China, the relation to Cordlife and Golden Meditech was my main concern about CO. I was doubtful that a merger would benefit CO, as it would dilute its Chinese focus and maybe even potentially damage its relation to the Chinese regulatory agencies.

Making its headquarter move to Hong-Kong could also have increased the geopolitical risks. And the past connections of the CO management team was a risk that shareholders’ interests might not have been the priority.

It was making perfect sense for Cordlife to want to acquire/merge with CO, as they are the major actor of the cord blood sector in south-east Asia and would have benefited from expanding to China. However, CO would have only diluted its unique advantages of being China-centric, and I am glad its management realized it.

With the merger out of the way, CO can now focus on growth inside China and become a quasi-monopoly in the provinces it operates in. So, the situation has drastically cleared and looks better.

Quantitative Analysis

Financials

Revenues

CO revenues have steadily grown over the last 10 years, reflecting its steady enrollment of new subscribers and high retention rate. For some reason, the stock price completely failed to reflect the company’s growth and have spiked in 2017 before declining steadily up to the end of 2020. I could not find a compelling reason for the stock decline, beyond a possible general worry of the market regarding Chinese companies in the midst of Trump’s trade war.

Source:www.finbox.com

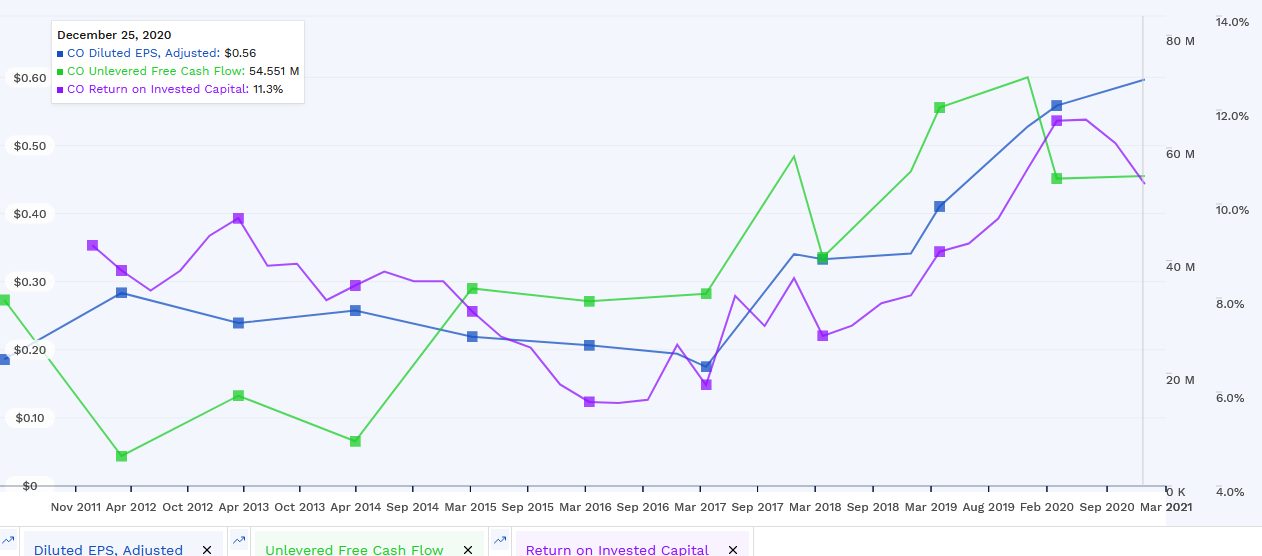

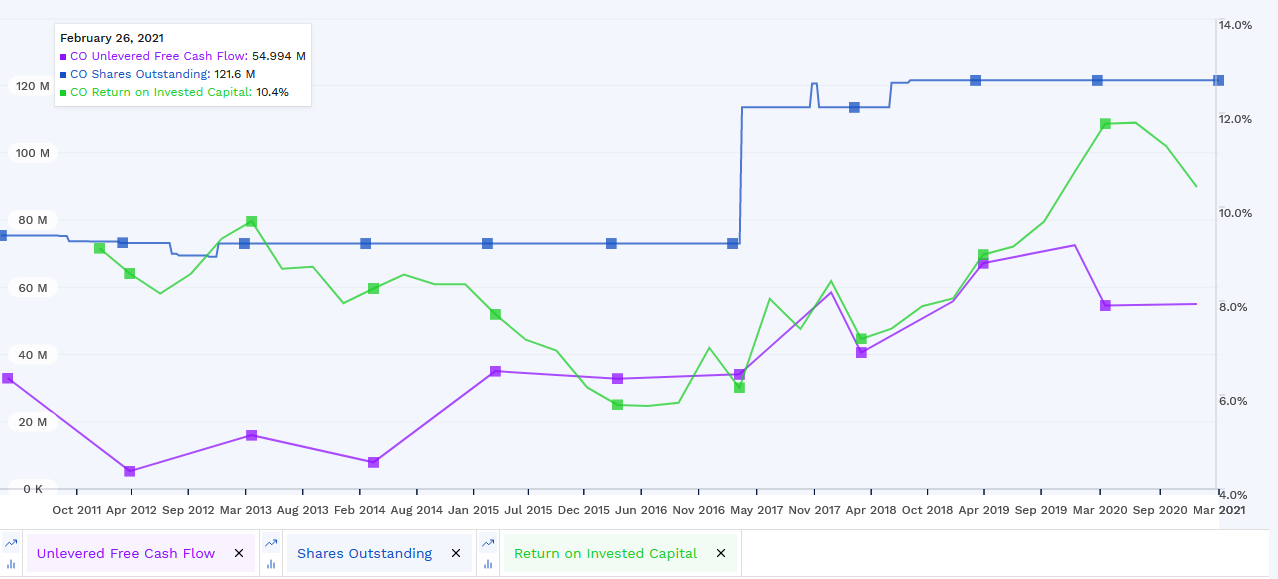

To also add to the confusion, CO is running a solid business, with growing revenues and earnings, unlike so many biotech and tech stocks these days. You can look at earnings per share, free cash flow, or ROIC, all point out an upward trend since 2016.

So, the company growth profile is rather spotless, and the market seems simply to not have recognized or is worried about it being Chinese and ignored CO results.

Source: www.finbox.com

Dividends and Stock Buybacks

At the moment, CO is not distributing any dividends. It might change in the future, at least in the long term, but no mention is made of it in the annual reports. I however do not dismiss it might happen considering the staggering amount of cash the company has on its balance sheet (more on that directly below).

Debt and Balance Sheet

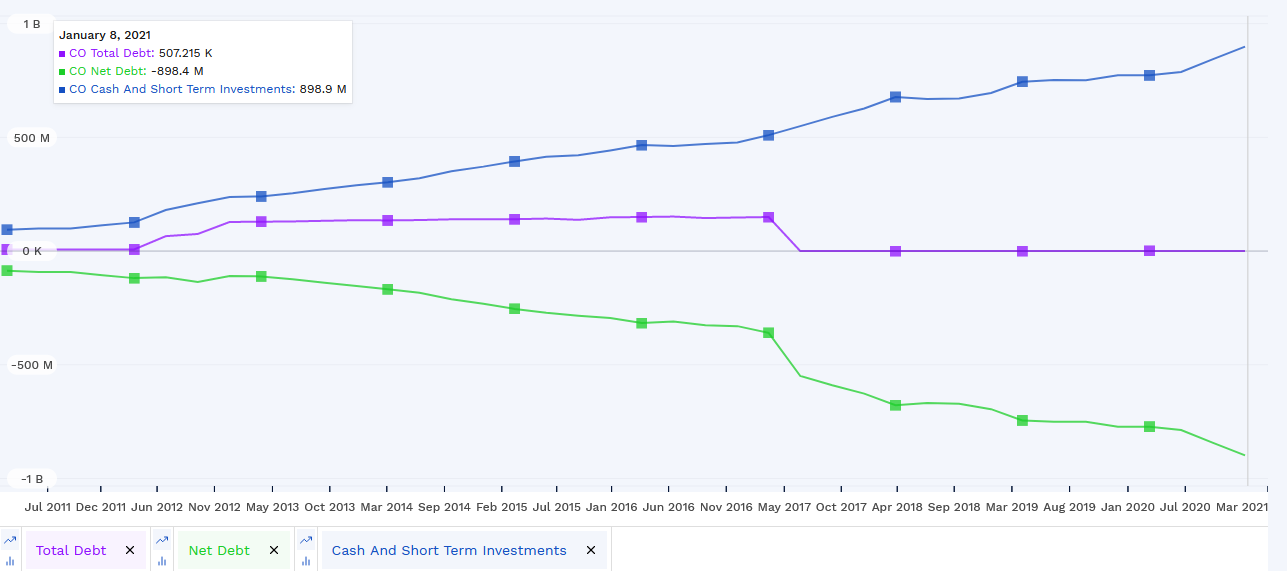

I have mentioned before how flush with cash CO is, but you will see, the numbers are truly astounding. The company has absolutely no long-term debt and almost $900 million in cash. Remember, we are talking of a company with a market cap of $583 million… truly astounding, as I said before.

Source: www.finbox.com

Frankly, it is so abnormal to find such market mispricing that I kept looking for a problem.

So, is it possible that the company is not spending enough in CAPEX, and will have to spend this cash down the road for its operations? Remember that CO operations are rather simple. The company had a large CAPEX spending in 2012 of $40 million, likely to buy the lab equipment, freezers, backup generators and so on it needed to store the cord blood samples.

But this equipment is not that expensive that building new facilities would significantly dent CO’s cash pile. Even a $100 million of extra CAPEX to triple the company’s capacity would only use two years of free cash flow or 11% of the cash available.

Source: www.finbox.com

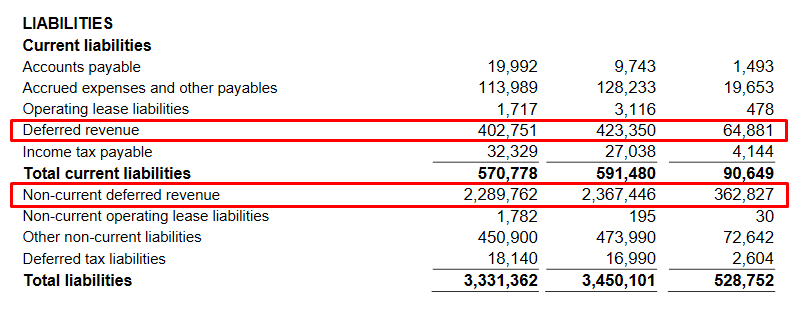

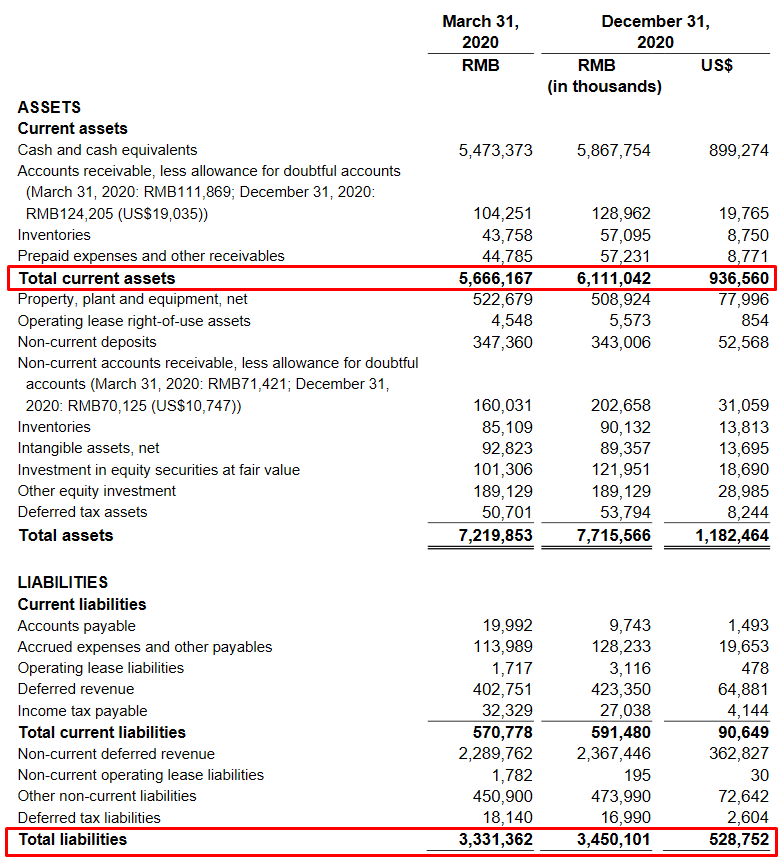

So, are there other liabilities that could be dangerous to the company’s future profitability? The bulk of liabilities are current and non-current deferred revenues. I can let you read more about deferred revenue here, but to put it simply, this is an accounting item current in business with a subscription model.

It means that the company already got paid but will need to spend the money at a later date to deliver the service promised.

Source:ir.globalcordbloodcorp.com

So, this represents the future cord blood storage promised, for which CO got paid upfront. I really like this business model, where the payment comes way ahead of the moment the corresponding spending needs to be done.

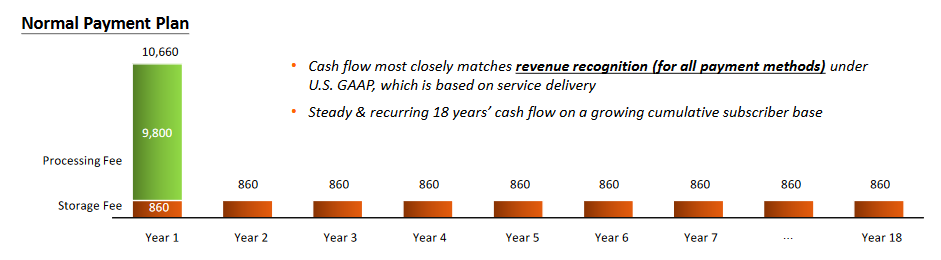

Deferred Revenues

CO deserves a special section on this topic. The current deferred revenue corresponds to the storage paid with the annual subscription model (prices are in yuan).

Source: ir.globalcordbloodcorp.com

The non-current deferred revenue corresponds to the offer when all is paid upfront the first year.

Source: ir.globalcordbloodcorp.com

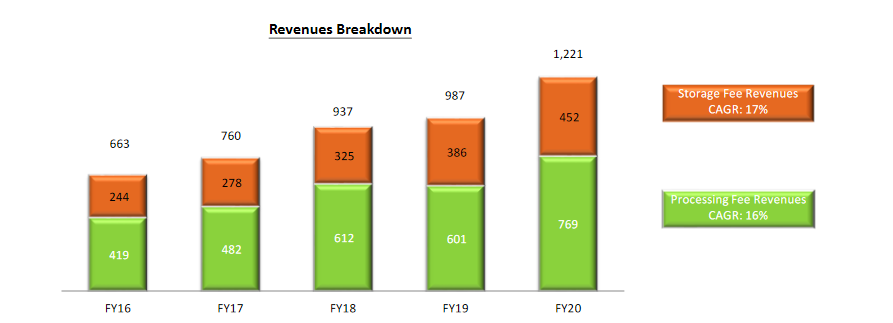

CO provides to investors a revenue breakdown between the two sources of income, storage and upfront processing fees. At the moment, the constant enrollment of new subscribers means that upfront fees are the bulk of CO revenues.

When the market will mature or saturate (although probably not until another 5-10 years), the company will start deriving most of its profit from storage fees and just roll over the inventory of cord blood samples with newborns.

Source: ir.globalcordbloodcorp.com

While I like in general subscription business, especially with very high retention rate, I am a little skeptical of an annual fixed price for 18 years. This is a long time, and Chinese inflation used to be around 2-4% before COVID-19.

Source: tradingeconomics.com

Therefore, I am not entirely sure CO will not lose money on some subscription at some point. It is possible that economy of scale compensate for that, but it is hard to not factor this into the business plan. It is also possible that some fine line in the contract indexes the subscription to baseline inflation, but I could find no mention of it.

Overall, it might be better if CO slowly switches to an only upfront payment only before the volume of subscribers with too low contracts become a drag on profitability.

These liabilities are indeed real, they represent some actual spending CO will need to do down the road. And it is good to see that the balance sheet takes them into account.

But it also means that even taking all liabilities into account, the cash left after covering liabilities is around $407 million, so almost entirely covering the market cap.

Source: ir.globalcordbloodcorp.com

When considering the real balance sheet situation, you actually get so much “free cash” that the real market capitalization is not $583 million but 583-407=$176 million. For a net income of $74 million. Again, astoundingly cheap by almost all metrics.

Cash Flow

One last check on the company financials is cash flow. Free cash flow is around $55 million. It is also worth noting that the number of shares have not significantly increased since 2017, when it seems the company had used the spike in share price to get come extra cash.

Return-On-Invested-Capital, or ROIC is also growing at 8-12% over the last years.

Source: www.finbox.com

The only negative thing I could find regarding cash and cash flow is that the cash seems to just sit in the company accounting and generate very little returns. Such a huge pile of cash should be reinvested. Ideally, I would like to see CO get more aggressive on its sales and marketing efforts.

Source: ir.globalcordbloodcorp.com

Or if it is not possible somehow, just use that cash to invest it and generate some income from it. Real returns of just 3%, not a very aggressive target, would generate $27 million extra, instead of just sitting on $900 million like a dragon on a pile of gold.

Overall, I am really impressed by CO’s balance sheet, cash pile and profitability, as well as growth prospects. I am a lot less impressed by their financial director who should be putting the company cash to better use or start distributing dividends to the shareholders.

Categorization and Valuation

Investment Category

CO is definitely a classic value type of investment, with its stock being so grossly undervalued compared to its earnings, cash flow, zero debt situation and cash on balance sheet.

But with state-granted monopoly as a lucrative and growing niche in the most populous and prosperous provinces of China, it is also a growth play. This does not even consider the possibilities to acquire similar companies in other regions or acquire more licenses for new provinces.

We will discuss it further in the conclusion, but CO seems to be a wonderful company at a dirt-cheap price, a true oddity. The only caveat is that it is a purely Chinese company. You will have to take a leap of faith and accept the accounting at face value and accept the exposure to the Chinese government whims.

It is also likely to either go spectacularly well (if the data are honest) or spectacularly wrong (if the data are fraudulent). This is not a stock without risk due to its location, but a high-risk, high-reward type of situation.

Discounted Cash Flow

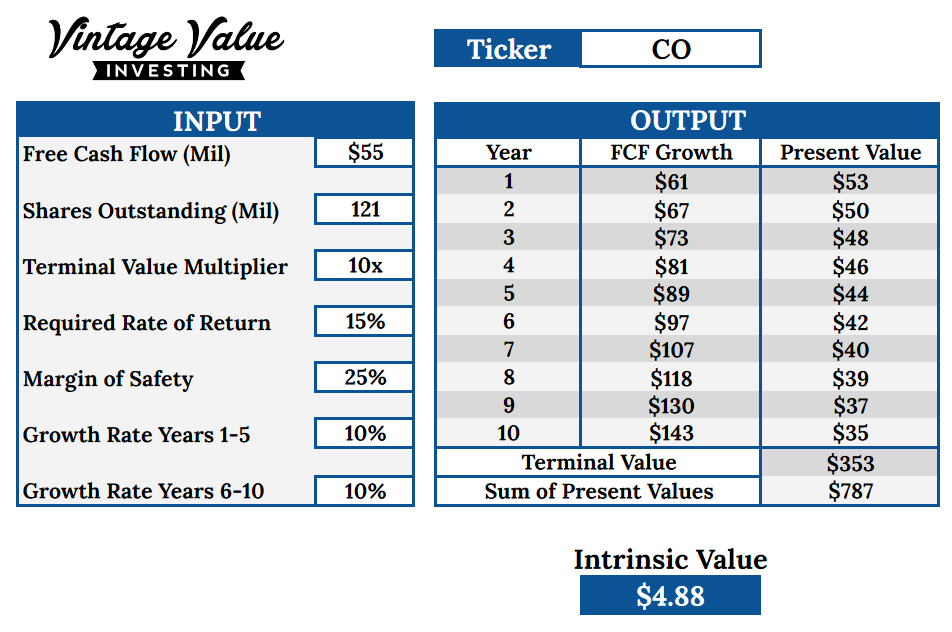

One way to calculate CO valuation is using the discounted cashflow model. You can see what it means and how it works here.

I used a very modest terminal value multiplier of 10x, assuming that markets will keep being skeptical of Chinese companies. I also took a growth rate of only 10%, something probably a little conservative. Even with a very aggressive margin of safety of 25%, I end up with a buying price of $4.88 dollars, so roughly at today’s price.

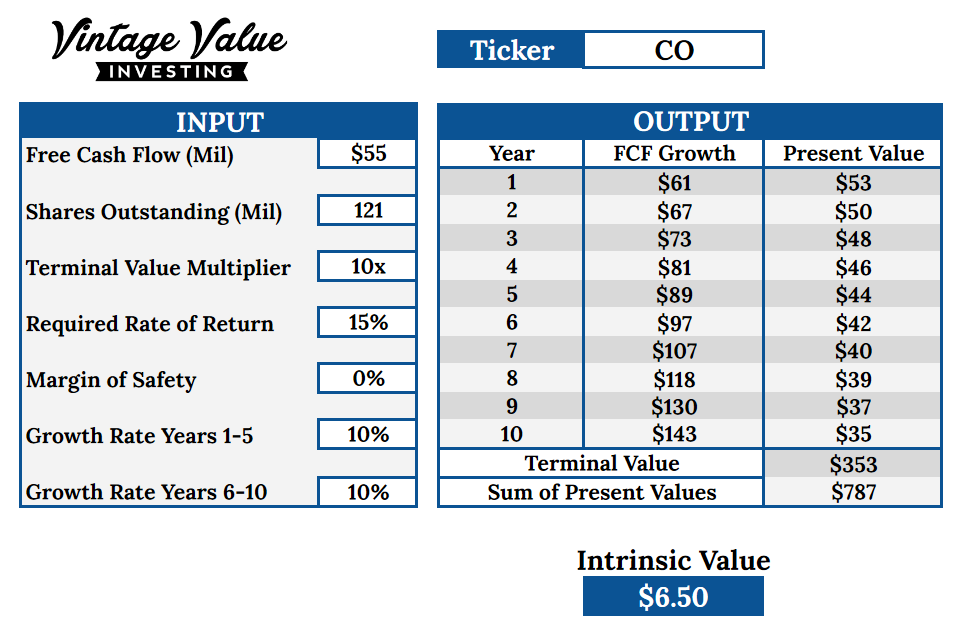

By removing the margin of safety, we find the estimated value of the company $6.50, so really by cash flow estimation, the company is grossly undervalued.

Now remember the $400 million or so of net cash after covering all liabilities. You basically get that for free, as the future free cash flow should be enough to bring a 15% return of investment.

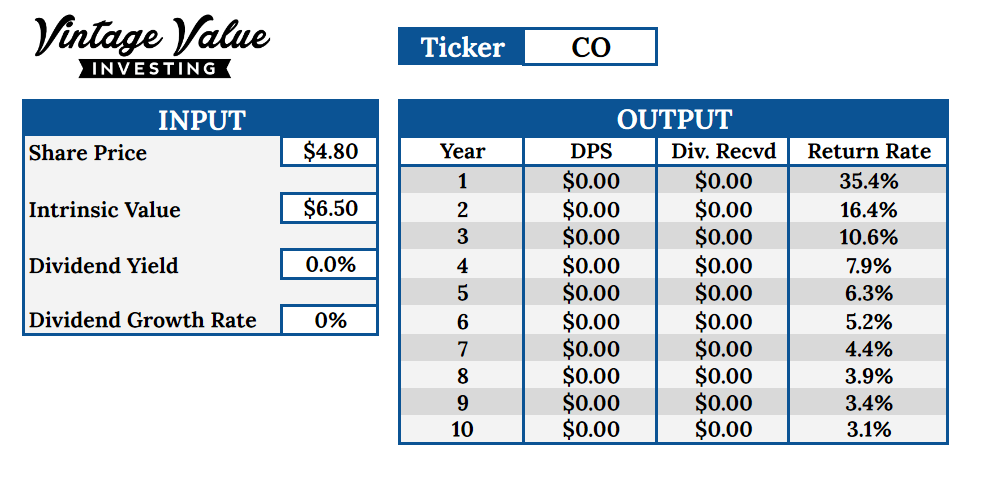

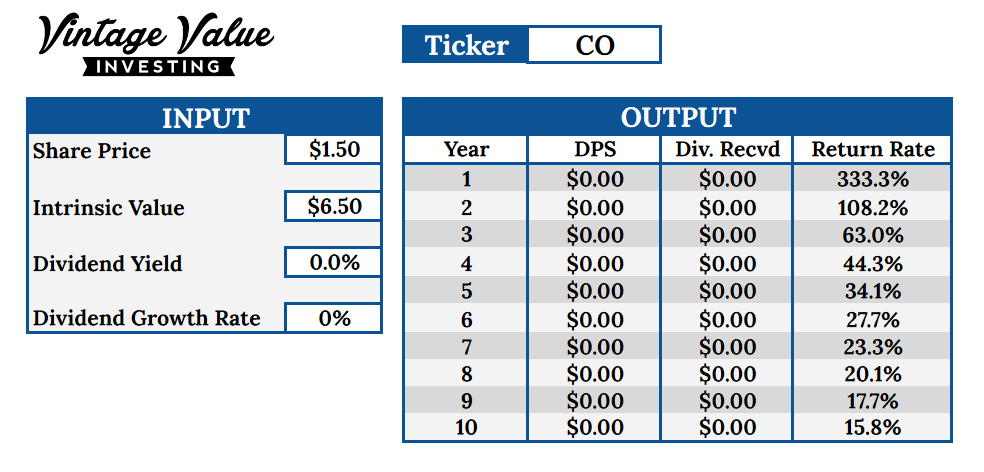

Deep Value Model

The undervaluation made me use the Deep Value model to see how cheap the company really is. So, if the company gets re-priced at its intrinsic value, it could generate a very nice yearly return. Of course, such return will be better the less waiting you have to do.

Here, I again did not take the cash sitting idle into account. If I consider that $400 million of the market cap are covered by it, it will mean the current share price is actually lower.

Instead of a $583 million market capitalization, the “real” market cap would be only $182 million. This would mean a “real” share price of 1.50$ once considered the cash balance and the absence of debt.

Of course, the cash on the balance sheet needs to be properly used for such calculations to make sense. And the passivity of CO in that regard is maybe a little bit worrying.

What is truly amazing in this calculation, is that even if the market takes 10 years to re-price CO, the annualized return rate could still be in the 15% range. Again, high risk (China) but also potential high rewards.

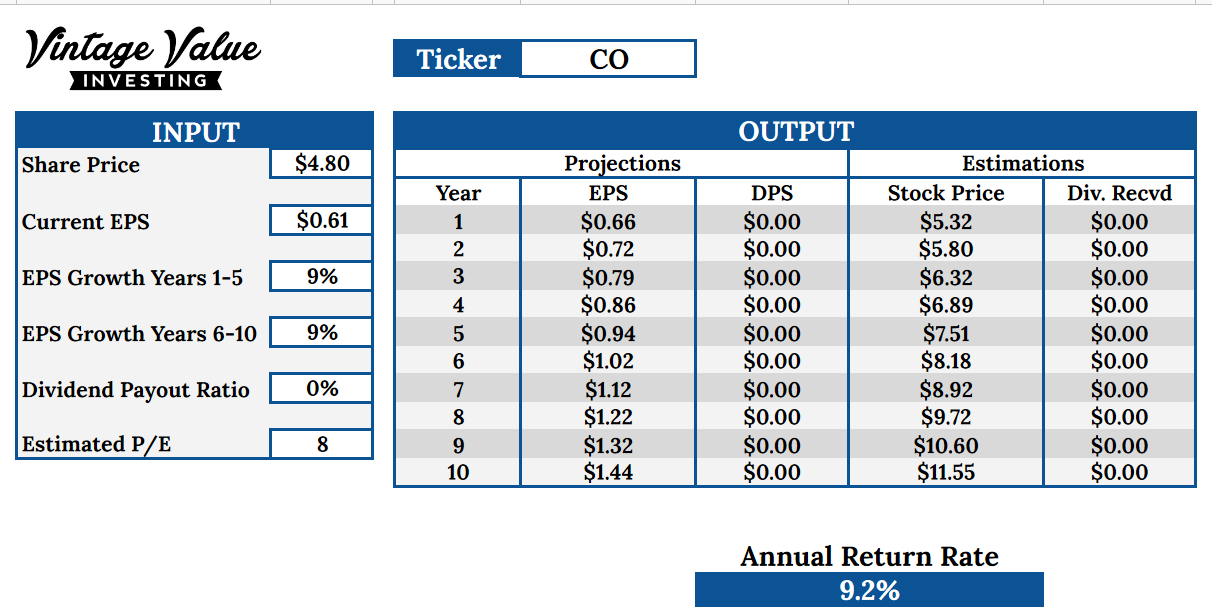

Earnings Growth Model

I expect CO to keep growing, so another way to guess its future returns is to look at earning growth. Over the last 10 years, earnings have grown at the rate of 9%. To keep a margin of safety, I took an expected growth of 9% in the next 10 years, as the monopoly situation of operating licenses and the Chinese market size leaves CO a lot of room to grow.

The annualized return rate is then of “only” 9%. A decent performance, but far from the extraordinary opportunity the other valuations indicate.

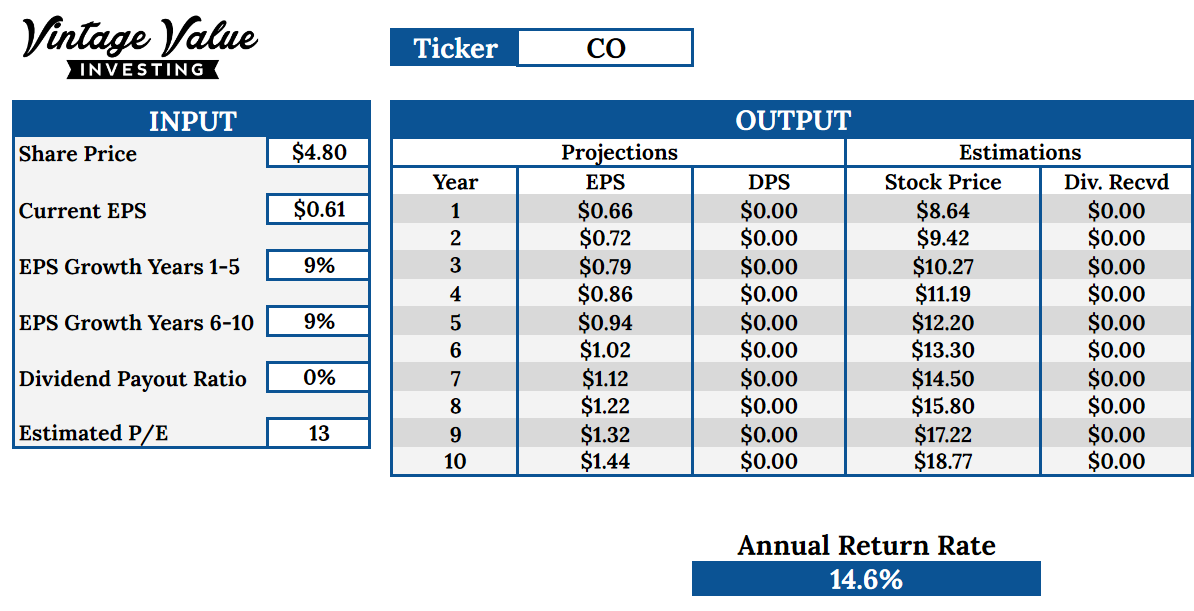

This rather “low” outcome might be due to the fact I picker a pretty low P/E of 8. CO’s P/E have changed a lot over time, so I prefer to keep a rather low one to get a conservative estimate.

Source: www.stockrover.com

If the general pessimism over everything China related does not persist with investor, I could see the P/E to get back to the range of 12-15, with would then warrant a much better return of 14% or more, more in line with the results from the other valuations methods.

Final Assessment

Company Synthesis

CO is a strange stock to analyze because it is impossible to come with a firm conclusion. Either it is the bargain of the century, or something is afoot. However, with all my due diligence on the company, I was unable to detect anything overtly suspicious.

I think that ultimately, an investor has to decide if he wants to take the risk to invest in a purely Chinese company.

As I said before, there are really just two possibilities for investment in this stock. If the numbers are not to be trusted, like it seems to be the case with Chinese companies like Luckin Coffee, then no amount of extra financial analysis will help, as the numbers are fake.

While I could not find any evidence of fraud, it does not mean it is not there. Very important here to remember is that the absence of proof is not the proof of absence. CO could be lying about its customer number or cash balance. It is hard to be 100% sure of what is going on in China. Then, you likely lose almost all your investment in CO.

Or the numbers are truthful, and CO is an outstanding opportunity, going to make 15% returns at the very least.

There is really not much middle ground to expect between these two options. So, a careful decision making is crucial here to make the best of this situation.

Strategic Options

Instead of discussing further valuation and/or long-term and short-term outlooks, I will present a few alternative strategies you could pick depending on your risk profile and time preference. Be aware this is NOT investment advice, but a good way for me to illustrate different portfolio strategies. Please be aware of the risks inherent to such investments.

Strategy 1: Buy, Hope, and Wait

You give a significant portion of your portfolio (5% maybe, no more than 10% for sure) and hope this turns out well. If the deal turns sour, you are likely to lose all of that money. If CO was honest about its books, it will bring up the return of your portfolio drastically.

This is a high risk, high reward angle, not for the faint of heart. Expect high volatility and a potential long wait before seeing any positive return.

Strategy 2: Splice Up the Portfolio Carefully

Put 2-3% of your portfolio on CO, with the goal of making your portfolio a little more aggressive. If CO turns into a solid compounder and cash machine, it will help build up stable returns. If it does not go well, the limited exposure will limit the damage.

This is good for a long-term portfolio and if you have for now low exposure to risky stock and emerging markets and biotech.

Strategy 3: Limited Long Exposure

Put 1-2% of your portfolio in CO and forget about it. Let the company grow its market, get new licenses, do not sell before at least 5 years. If it goes wrong, the loss is marginal. If it goes well, it will pump up your overall annual returns by maybe a few percent yearly, which is not that bad for such a small investment.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in CO and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.