Investing in income-producing assets is one of the fundamental steps in the wealth-building process. Equities, in particular, form the backbone of many retirement portfolios. Sadly, only about 56% of Americans owned stocks in 2021[1].

Robinhood has tried to encourage greater participation in the stock market by adding game-like features to its trading app. They do so under the premise of furthering their mission to “democratize finance for all.”

That sounds fantastic, but the gamification of investing promotes strategies that benefit brokerages rather than investors. Here’s what you need to know about the process, including how it works, why it’s dangerous, and how to protect yourself.

What Is the Gamification of Investing?

The gamification of investing refers to the addition of features to investment apps that make the user experience more intuitive, exciting, or visually appealing. Their purpose is to make stock trading more fun for the average consumer, like playing a video game.

In contrast, you can imagine a drab, black-and-white screen covered in indecipherable indexes and financial jargon. That kind of user interface is intimidating to the uninitiated and likely to scare away would-be investors.

You might think a friendly and approachable investing app is a positive thing. In theory, it might be, but there are caveats. In practice, it can trivialize the experience, and many gamification features border on manipulative and misleading.

As a result, there’s been widespread criticism about the practice, and regulators are intervening. The Securities and Exchange Commission (SEC) issued a formal request to the public for comments on investing gamification and “digital engagement practices.”

The Financial Industry of Regulatory Authority (FINRA) has expressed interest in doing the same. Both agencies want to assess whether regulatory action is necessary to protect consumers from the risks these practices present.

More drastically, Secretary William Galvin of the Massachusetts Commonwealth charged Robinhood for using “aggressive tactics to attract new, often inexperienced, investors” and employing “strategies such as gamification to encourage and entice continuous and repetitive use of its trading application.” Scathing stuff.

How the Gamification of Investing Works

It’s difficult to properly articulate the dangers of investing gamification as a purely abstract concept. To make things a little more grounded, let’s look at some of the actual practices platforms like Robinhood are implementing.

Reward Animations

One of the red flags that first brought eyes to the gamification issue was Robinhood’s infamous confetti feature. In prior versions of the app, confetti would fall across your screen after every trade, reinforcing the idea that each of them was something to celebrate.

In reality, making more trades is a great way to blow your money. Stock traders almost always lose, and the average investor is often much better off following a less active investing strategy.

There was such widespread criticism for the animation that Robinhood eventually removed it from their app. Somewhat amusingly, they just switched the confetti out for floating geometric patterns, entirely missing the point.

Inadequate Disclaimers and Disclosures

The financial services industry is highly regulated, and for good reasons. The money people use to fund their retirements, put food on the table, and pay for their children’s education is often at risk.

Much of that regulation has to do with the information providers owe their customers. That’s why public companies include disclosures with their financial statements and payday lenders have to disclaim that their prices are unsustainable in the long term.

Unfortunately, light-hearted, game-like interfaces leave little room for these kinds of acknowledgments. That’s dangerous in a world where people barely glance at terms and conditions in the first place. Providers must make critical information readily available for consumers, or they’ll never take it to heart.

Emphasis on Trending Stocks

One of the most dangerous gamification features is the emphasis on trending stocks. Just like you’d see the top ten scorers in a competitive video game, apps often highlight the stocks with the most significant price swings, whether they’re positive or negative.

There is a sea of investments to choose from nowadays, but these lists funnel investors into a volatile few that are far from guaranteed to be profitable. In fact, they’re often the most overbought stocks available.

These lists promote awful investing habits, especially among young investors that are easier to influence. They may end up pouring money into a stock simply because it went up or down more than the others that day, always chasing the latest and greatest.

Learn: The harmful effects of attention-induced training on Robinhood users are well-documented. The average 20-day return for the top stocks purchased each day is a depressing -4.7%.

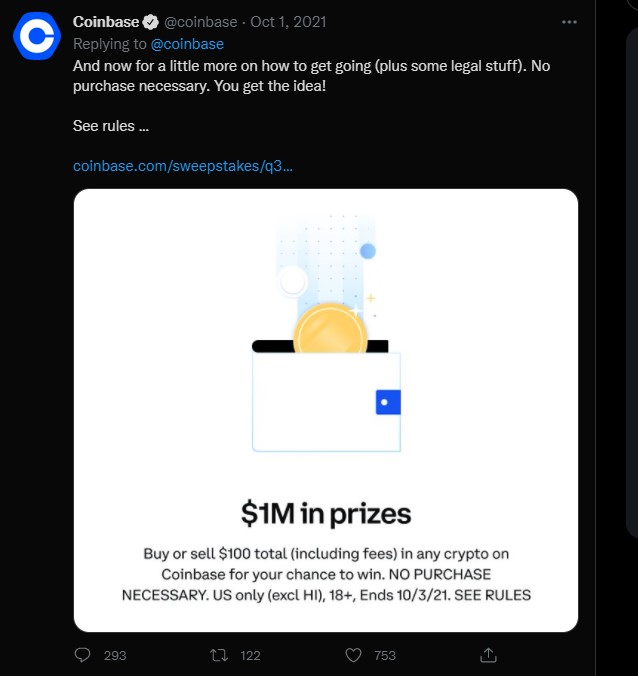

Lottery Incentives

Last but not least, many of these apps include lottery systems to incentivize actions that aren’t necessarily in your best interest. They can also make the experience feel more like gambling than investing, further numbing users to the risks involved.

For example, Coinbase recently sent me an email about their latest sweepstakes. They’re giving away $500,000 in prizes to eight lucky winners. To enter into the sweepstakes, all you have to do is execute a trade worth $100 or more.

Your odds of winning are low, but it’s another way to tempt you into trading more actively, especially if you’re a new investor that’s hesitant to get started. Of course, you’ll incur a pesky fee if you choose to buy or sell, but they don’t talk about that.

Why Is the Gamification of Investing Problematic?

It’s time to get to the heart of the matter. Why are regulators and myself so suspicious that there are less than noble intentions behind these gamification techniques? And what vulnerability do these tactics target that makes them so insidious?

Let’s take a look at these issues in turn.

The Broker-Investor Conflict of Interest

In my past life, I used to audit companies for a living. A significant issue in the auditing world is maintaining independence from your clients to avoid potential conflicts of interest.

The idea is that you can’t issue an unbiased opinion on the accuracy of a company’s financial statements if you own stock in their business or accept a Porsche from their CEO. You have a monetary incentive to give them your stamp of approval.

Managing conflicting interests like that is another major cause for regulation in the financial industry. When money is involved, people tend to promote outcomes that end up with as much of it in their pockets as possible.

That’s never been a more prevalent issue than in the broker-investor relationship. The interests of these two parties almost entirely conflict. The most profitable strategy for the investor is often the least lucrative for the broker and vice versa.

That used to be the case because of commissions. In the past, every time you called your broker to execute a trade, they’d get a pretty sum for the transaction. As a result, they had every reason to encourage you to make as many trades as possible.

But as we touched on early, the more trades you make, the more likely you are to lose money. It’s hard to trade stocks and make money in the short term and almost impossible in the long term. A study of eToro users found that roughly 80% of active traders on the platform lose money, with an average return of -36.3% over 12 months[2].

The Payment for Order Flow Model

Trade commissions aren’t a concern on most modern free trading platforms. However, the broker-investor conflict of interest remains, thanks to the controversial payment for order flow model. Here’s how it works, as simply as I can put it.

When you initiate an order through Robinhood, they send your request to a third-party “market maker.” The market maker facilitates the transaction, profiting from a difference between the price Party A pays for the shares and the price at which Party B sells them. The market maker then pays a portion of those profits to Robinhood.

👉 For Example

Say you want to sell one of your shares of Stock A. You execute the order through Robinhood, and they send your order to a market maker. The market maker buys your share for $100 and simultaneously sells one to someone else for $100.10. They pocket $0.10, then pay $0.03 to Robinhood for sending them your order.

That’s how Robinhood generates roughly 80% of its profits[3]. It’s what allows them to offer commission-free trading, but it’s received criticism for the many conflicts of interest it causes between brokers and investors. Most relevant to this discussion is that it again incentivizes brokers to maximize trading volume.

Payment for order flow is so problematic that the SEC might ban it entirely. I’d be remiss if I didn’t tell you that Bernie Madoff, the infamous Ponzi schemer, was one of its earliest and most significant proponents.

The Targeting of Younger Investors

One hallmark of predatory financial tactics is the targeting of vulnerable groups. Internet scammers prey on the elderly, payday lenders set up shop in lower-income communities, and gamification techniques target young investors.

As you can probably guess, video game enthusiasts usually aren’t homeowners flush with cash in their 50s and 60s. Roughly 38% of video game players are between ages 18 and 34, with another 21% under 18 years old[4].

Gamification techniques are particularly effective on that audience, who feels the most familiar with those kinds of interfaces. As a result, it probably won’t surprise you to learn that roughly 40% of Robinhood users are between the ages of 19 and 34, with a median of 31 years old[5, 6]. Those are some eerily familiar numbers.

Unfortunately, young people have less experience with investing, almost by definition. When you combine their lack of knowledge with the higher risk tolerance that comes from a long time horizon and the brashness of youth, you get perfect targets for brokers who want to encourage active trading.

📘 Read More: If you’re interested in reading anecdotes documenting this phenomenon, take a look at some of the links below:

How to Protect Yourself from Manipulation

Even if regulators take steps to prevent the gamification of investing, there will always be people and businesses using manipulative tactics to profit from your need to invest.

Ultimately, only you can be responsible for keeping yourself safe. To that end, here are some of the best steps you can take to protect yourself from their manipulation.

Educate Yourself

As we established earlier, financial predators primarily target the vulnerable, just like a wolf pack going after the slowest deer in the herd.

Vulnerability can take many forms, but ignorance is one of the ripest for exploitation. As a result, learning the most reliable investment strategies and the mechanics of the most popular asset classes is a critical step in protecting yourself against manipulation.

For example, someone armed with the knowledge that active trading is incredibly risky has already immunized themselves to the primary trap that the gamification of investing poses.

The more you expand your understanding of investing, the greater confidence you can have in your ability to make good decisions, and the harder it is for predators to trick you into giving them your money.

📘 Learn More: If you’re in need of resources to help further your education, check out our favorite guides and tips for investing: Start Investing – FinMasters

Follow a Long-Term Strategy

In the world of finance, you’ll often hear people say, “It’s a marathon, not a sprint.” That applies to many things, but none more so than investing, where patience, consistency, and discipline are critical.

For instance, consider the stock market. If you look at the returns of the S&P 500 Index in any given year, you’ll find terrifying volatility. It went down 8.78% in 1974, then up 37% in 1975. It went down 36.55% in 2008, then back up 25.94% in 2009.

Your odds of picking a winning year aren’t fantastic. Your odds of picking a winning month, week, or day are even worse. However, if you take a longer-term perspective, the risk diminishes. Take a look at the best and worst returns over the following time horizons[7]:

| Time Horizon | Best Returns | Worst Returns |

|---|---|---|

| 5 Years | 30% | -6.6% |

| 10 Years | 20% | -3% |

| 15 Years | 20% | 3.7% |

| 20 Years | 18% | 6.4% |

As you can see, the longer you’re willing to stay the course, the more likely you are to come out ahead. Keep that in mind as you pick an investment strategy and be skeptical of anybody selling something else.

Stay Away from Temptation

Once you thoroughly understand investing and devise an intelligent long-term plan, rash decisions are the thing most likely to ruin you. Typically, that means getting greedy or getting scared. For example:

- The hype around the latest and greatest cryptocurrency is too enticing. You can’t resist dumping money into it, but you do so right before the bubble bursts.

- The stock market plummets, and you get scared, so you sell everything right before the market bottoms, then miss the ride back to the top.

These are tales as old as time. We’re all susceptible to the fear of missing out or losing what we’ve built. I’ve found that the best way to prevent myself from falling for these traps is to avoid them entirely.

Don’t watch your asset balances go down when the stock market is tanking because it’ll only upset you. And be careful who you let sell things to you because you might find they’re too good to resist.