Brazil is the world’s 12th-largest economy and the third-largest outside the US, Europe, and East Asia. Brazil’s abundant resources, youthful population, and insulation from geopolitical conflict have drawn the attention of emerging market investors, but serious questions remain.

Let’s take a closer look at Brazil and its position in the emerging market investment landscape.

Brazil Overview

Brazil is the largest country in South America, more than half of the continent by surface area. It is split into 3 general regions:

- The Amazon basin: flat, sparsely populated, and mostly jungle.

- The Brazilian highlands: A rough mountainous terrain, mostly consisting of savannah. This is where most of the farming is being done. Poorly connected to the coastal cities.

- The coast: a narrow band of land between the sea and the highlands, where most of the large cities and population are located.

The country spent over three centuries as a colony of Portugal, relying heavily on the export of cash crops grown with slave labor. This left a pattern of underdeveloped infrastructure, poor access to inner regions, high inequality between the rich and poor, and a dependence on global commodity prices.

You can read a detailed explanation of Brazil’s geography and development challenges in this excellent article by Thomas Pueyo.

Source: Free World Maps

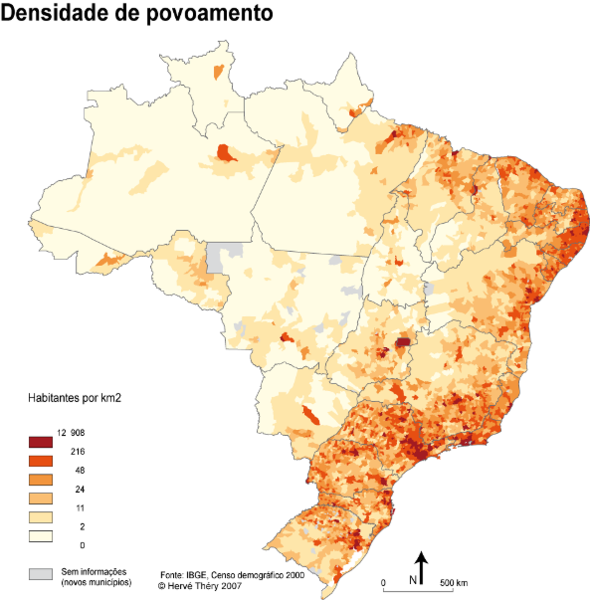

Brazil Population Density – Source: Wikipedia

Despite some struggle, Brazil is emerging as an important actor on the world stage. It is part of the extending BRICS (Brazil, Russia, India, China, South Africa) cluster, which is often cited as a representation of the economic emergence of the global south.

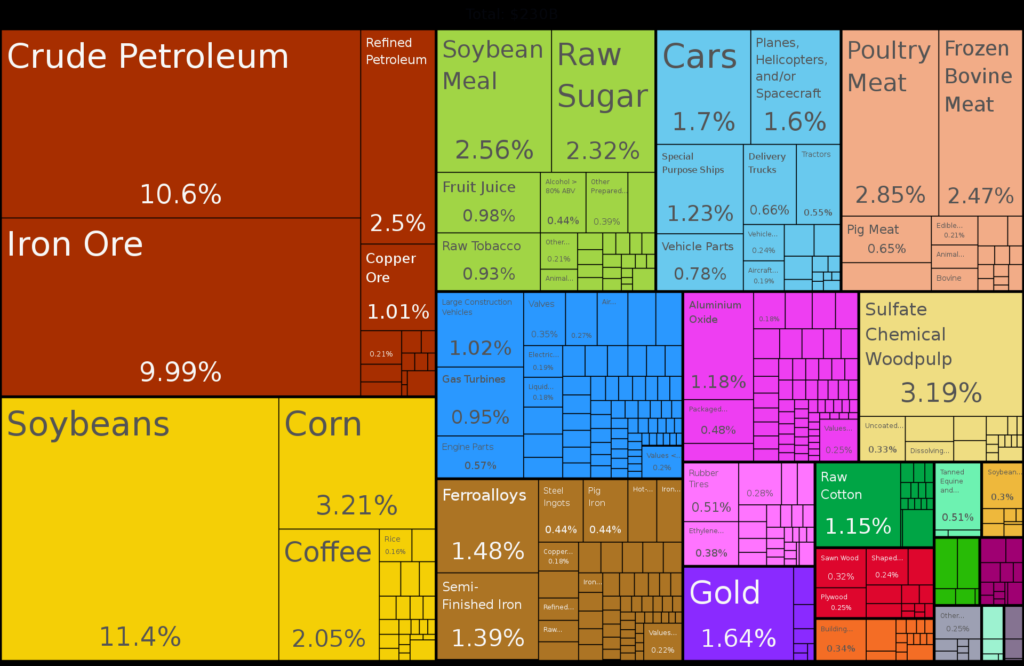

With the exception of China and India, these are mostly commodity-driven economies. The Brazilian economy is a good example of this, with its exports being almost exclusively crops, meat, wood, metal, and oil.

Source: Wikipedia

As a result, the investing sentiment about Brazil follows commodities prices, as illustrated by the covers of The Economist, first in 2009 (at a commodity price peak) and 2015 (at a low point for commodities). (The Economist covers are notorious for being artfully made and hilariously wrong in their timing, indicating the end of a trend).

Brazil has the largest economy in Latin America and the country is slowly taking up a leadership role in the region. With the recent tentative discussion of a common currency, the “Sur”, which could one day become a Euro-style common currency for South America.

Brazil’s Strengths

Brazil is attractive to investors for a number of macroeconomic reasons. They are all pretty self-explanatory:

- Global underinvestment in commodities has led to a short supply of key materials like copper and oil. Meanwhile, Brazil is one of the only countries to have massively invested in production growth and is poised to reap the benefit of this strategy.

- Neutrality in a world of rising geopolitical risks. Brazil is both geographically and politically separated from the current Russia-China vs US-EU-NATO tensions.

- Large, young, and growing population: Brazil has 217 million people, with 20% below 14 years old.

- Abundant energy: The country produces 88% of its electricity from hydropower. It also has the 15th largest oil reserves, behind Qatar. It also has a large and untapped potential for developing solar and wind power.

- Undervalued markets: many leading Brazilian companies are trading at single-digit P/E ratios despite giving double-digit dividends. This is mainly due to perceived political risks (see below).

Those points of attraction are offset by disadvantages, and we have to consider those as well.

Brazil’s Weaknesses

At the surface level, Brazil seems like a great place for investors. Young, growing, energy-rich, and undervalued. But those low valuations come from somewhere. There are also reasons to be wary of investing in Brazil.

Political Risk, Corruption & Instability

This is THE big negative point everyone will bring up about Brazil. The rule of law is elusive and the political culture is rife with corruption. The recent storming by protestors of the Congress, the Supreme Court, and the presidential palace is just one example of instability, though it must be said that the same thing happened in the USA!

The return of Luis Ignacio Lula da Silva into power has also been viewed as a potential negative by investors. His previous administration is regarded as marked by widespread corruption, even if some will claim these accusations were bogus and politically motivated. In any case, this further illustrates the political risk and division of the country.

Inflation and History of Poor Management

Recent Brazilian inflation rates have been mostly in the 3%-8% range, but the country also experienced out-of-control inflation of 2,000% in the 1990s. Overall, the country has historically had problems with poor economic management.

Brazil has suffered from a common issue in South America: the toxic mix of powerful vested interests of a small elite of landowners and rich families, which invariably provokes a socialist backlash among the poor.

This deep-rooted economic structure is the real cause of corruption and political instability. The wealthy can buy politicians and protect their interests, the left wants to loot national companies, and the rest of the population is forced to pick a side, even if it is a lose-lose situation for them.

Consequently, while improving, the country is still widely perceived as always at risk of falling to a Pinochet-style right-wing dictatorship or a Venezuela-style socialist takeover.

Middle-Income Trap & Commodity Exposure

So far, Brazil has been a textbook case of the middle-income trap. This is where an economy develops up to a point, but then hits the ceiling and is unable to go up in the value chain.

“a country in the middle-income trap has lost its competitive edge in the export of manufactured goods due to rising wages, but is unable to keep up with more developed economies in the high-value-added market.“

Poor education, dysfunctional institutions, and corruption are the main causes.

This leaves the country massively exposed to the global commodity cycle. When commodities do well, Brazil booms and produces a budget surplus, like the record $62B trade surplus in 2022. And the opposite happens when commodities prices slump.

This repeating cycle damages the long-term prospect of the economy, reinforcing the middle-income trap. It also exposes the country to risk from fluctuating currency values, as exports are typically priced in US dollars.

Risk Management

Investing in Brazil can be a high-stress venture. This is a market renowned for its volatility. It is also a market that has been essentially going sideways for the last 20 years. So from a trading point of view, managing a good entry point and knowing when to exit is crucial.

Source: iShares.com

At the same time, the price tag of a Brazil ETF does not tell the whole story. The persistent undervaluation means that dividend yields can be high, sometimes absurdly high, as we will see with Petrobras’ stock below. So good returns from Brazil are entirely possible even if stock prices are stagnant.

It is also likely that the political risk is a little overblown. If anything, the recent right-wing protests show that the country is unlikely to be easily turned into Venezuela by Lula.

So overall, success in Brazil investing will mostly come to astute cyclical investors, able to ignore the regular panic gripping the Brazilian stock market and be careful in their risk management.

Company Spotlights

Petrobras (PBR)

Petrobras may be the most discussed Brazilian company internationally. This is a giant among oil companies, and one of the only ones to have steadily growing production. Petrobras also increased reserves by 11% in 2021. Its reputation has also never fully recovered from a scandal of money laundering and corruption in the 2000s, which keeps its valuation depressed.

It is majority-owned by the Brazilian state, and if the dividends from the previous administration hold, it might yield an absurdly high 68% dividend yield in 2023. Critics will say it is equally likely to be looted by Lula and be worth zero. At a P/E of 2.17, it can nevertheless be attractive to daring deep-value investors.

In a move to appease investors’ fears, the new Lula-appointed CEO is promising to both embrace renewables (A Lula electoral promise) and also keep the oil & gas production growth on track.

Copel (ELP)

This is a stock we covered in a report in May 2021 report. It has gone up a little since and distributed a generous double-digit dividend. The company produces power from one of the world’s largest hydropower dams in the world.

It can make an attractive income-focused investment, especially for investors looking for carbon-neutral energy producers.

(Please note most stock data aggregators like Yahoo Finance or Stock Rover do not do a good job of compiling Copel data. I would recommend calculating its financial metrics manually).

Vale (VALE)

Vale is the world’s largest iron ore producer and the world’s largest nickel producer. It also produces copper, fertilizers, manganese, and coal. It is trading at a P/E of 4.37 and distributes a dividend of 4.38%. This is a rather simple business: Vale digs resources from the ground and sells them abroad, mostly to China.

The current valuation makes it look cheap, but investors will need to be able to properly assess where they are positioned in the commodities cycle to profit from it.

Vale has been also involved in 2 catastrophic tailing dam failures, killing 270 people and causing major pollution. This tarnished its reputation, or as the BBC put it “The pride of Brazil becomes its most hated company“. The case is still being judged in criminal court.

Ambev (ABEV)

Ambev is a beer and soft drink company selling all over South America and even in Canada, producing and selling brands like Budweiser, Corona, Pepsi, Lipton Ice Tea, Gatorade or Stella Artois, for a total of annual 270 million hectoliters. The company is controlled at 68% by AB-InBev (BUD), the biggest brewer in the world.

The company has been growing revenues, but profits are rather stagnant. Even then, its valuation seems reasonable, it offers a dividend yield of 5.77% and trades a P/E of 15.6.

Brasil Agro (LND)

Brasil Agro is a farming company controlling 18 large farms with a total of 275,000 hectares (680,000 acres) in Brazil, Paraguay, and Bolivia. It produces diverse crops (soy, corn, cotton, sugarcane, beans, cattle) in a range of climates. Soybeans represent the single largest product, at 39% of revenue.

The company trades at a P/E of 6.12 and distributes a dividend of 18.8%. This is a rather similar business to Vale, with dividends and profit tightly linked to the price of global commodities, in this case, food products rather than metals.

ETFs

If you want to invest in Brazil as a whole, an ETF might be a better option.

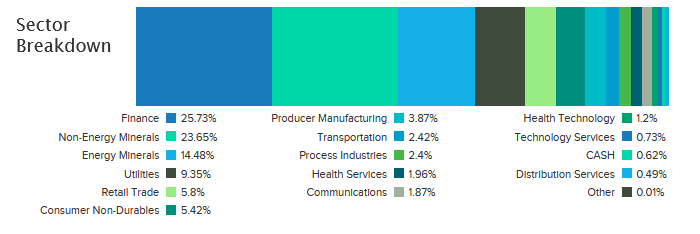

By very far, the most liquid and traded ETF is the iShares MSCI Brazil (EWZ). In addition to minerals and energy, it contains quite a bit of exposure to the country’s financial sector (25% of the ETF holdings), utilities, and 1/3 covering the rest of the economy.

Source: ETFdb.com

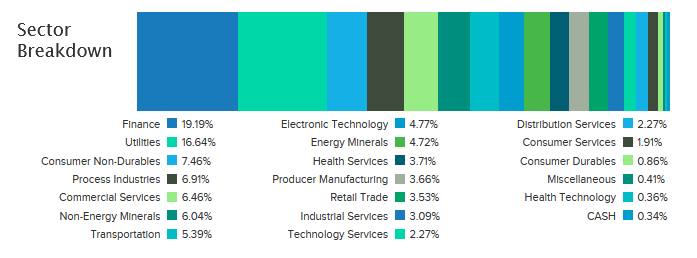

If you are looking for more diversified exposure to utilities (16.64%) and the economy as a whole, the iShares MSCI Brazil Small-Cap ETF (EWZS) is an option as well. It is also offering higher exposure to consumer non-durable products (7.46%), electronics, and transportation.

Source: ETFdb.com

An ETF will let you diversify your holdings, avoid concentration risk, and gain access to companies that don’t trade on US markets.

Conclusion

Brazil is a country with a lot of potential but also numerous risk factors.

It has a large population, plenty of natural resources, cheap energy, and growing oil production. When adding a geographical and geopolitical distance from the world trouble, it might seem like a safe haven in troubled times. High dividend yields contribute to the attractiveness of the country for investors. Long-term potential for growth beyond the middle trap income is something definitely not priced in either.

Still, these advantages are seemingly always at risk of dysfunctional political institutions and social instability. Currently, the country as a whole is essentially a bet on the commodity markets, and its largest companies reflect this status. If the world’s economy slows down, Brazil could find itself in the same trouble it was in 2015 in the last commodity slump.

The recent political contest between far-right Bolsonaro and far-left Lula has brought a lot of skepticism about Brazil. So it might be a good entry point, at peak pessimism. In any case, extreme volatility is almost a given.

As with most emerging markets, an investment in Brazil requires a keen sense of timing, a fairly high risk tolerance, and a modest portfolio allocation.

Finding Value in Emerging Markets

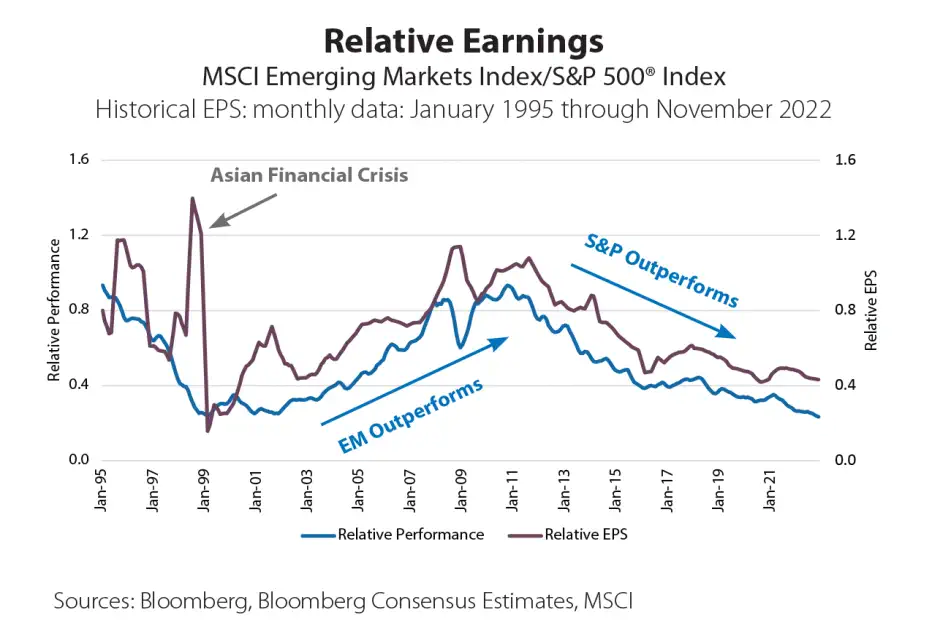

Stock Spotlight has regularly covered stocks in emerging markets, which can offer great companies at discounted prices. After a decade of outperformance for the US stock market, it might be time for emerging markets to shine. This cycle between emerging market (EM) vs the US tends to be roughly 10-15y long, as you can see below. With the S&P500 outperformance stated in 2010, we are due for a reversal in trend.

Source: Western Southern

Past patterns may not be repeated, but the investing world still extends beyond the US, and increasing numbers of investors are considering exposure in non-US markets!

Emerging Value

This is a series focused on opportunities in emerging markets. The goal is not to discuss breaking news. Instead, we will focus on long-term trends and lasting phenomena that will impact investing in a country or region. It will also look at a selection of companies that might be worth a deeper look.