The defense industry is a major center of innovation and industrial capacity. It is also controversial, and some investors prefer to avoid the sector. Others see the continuous rise in global military spending and focus on the industry’s profit potential.

If you are considering defense industry investments, this primer will introduce the basic structure and subsectors of the industry and look at some issues and concerns that are unique to it.

Only the dead have seen the end of war.

Plato

Key Takeaways

- Global defense spending is growing fast. Global instability and regional rivalries have both large and small countries investing more in their military forces.

- The defense industry is highly consolidated. In most countries, the industry is dominated by a small number of major players.

- The defense industry is highly resilient. Defense companies often flourish and see their best investment performance during unstable periods when other companies are performing poorly.

- Defense companies are closely linked to governments. Because their customers are governments, defense contractors must navigate complex bidding and procurement rules, and may not be able to sell to some potential customers.

The Case for Defense Investing

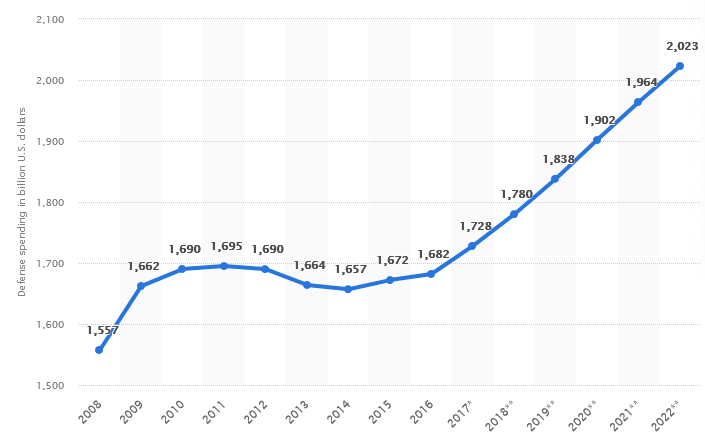

Global defense spending is on a continuous and seemingly unstoppable growth curve.

One simple for this growth is geopolitics. Conflict and the potential for conflict are simmering around the world and occasionally – as in Ukraine – boiling over. An arms race has started between the US and China and looks set to last for a while. Just to give you some perspective, here is some of the most recent news about increases in military spending:

- Germany commits an additional €100 billion to defense spending.[1]

- China boosts defense budget again, exceeding $208 billion.[2]

- Senate panel approves record US military budget for 2022-2023 ($858B).[3]

- Poland to increase defense spending to 3% of GDP from 2023 ($23B).[4]

- France to request multibillion-dollar defense budget boost in 2023 ($44B).[5]

- Japan Begins Defense Upgrade With 26% Spending Increase for 2023 (51B).[6]

None of these budget increases have yet translated into increased earnings for defense firms, but stock prices are already reflecting some of these expectations.

Si vis pacem, para bellum

Vegetius

(If you want peace, prepare for war)

Industry Structure

Over the last three decades, we have seen a consolidation trend in the industry, especially in the US defense industry. You can read more in this article about how many of the US suppliers to the military are now merged into just 5-6 megacorporations:

- Lockheed Martin

- Boeing

- Northrop Grumman

- Raytheon

- Huntington Ingalls Industries

- General Dynamics (we covered the General Dynamics investment case in this report in April 2021 report, with the stock up 32% since).

Most non-Western manufacturers are state-owned companies that are closed to investors. Beyond the US, other NATO countries and US allies have publicly listed defense companies, for example:

- France: Dassault, Airbus, and Thales

- Germany: Reinhmetall, Thyssenkrupp and MBDA

- UK: BAE Systems

- Italy: Leonardo

- Sweden: Saab.

The defense industry actually covers a multitude of subsectors, often categorized by technology:

- Aerospace (planes, satellites, missiles,…)

- Cyberdefense, Telecom, and AI

- Weapons (ammunition, artillery, guns, …)

- Vehicles (armored carriers, tanks, …)

- Maritime (ships, submarines, …)

- Logistics & Software

- Personal equipment (body armor, shoes, …)

- Sensors (optics, radars, etc…)

Because of consolidation, some products in these subsegments are either the monopoly of one company or a small oligopoly with 2-4 companies controlling the market, The more expensive the equipment, the smaller the number of suppliers usually is.

This gives the primary suppliers strong pricing power and a powerful moat, especially in times of crisis when governments rush to increase defense spending.

Defense Industry Advantages

The other reason for investing in this sector is the actual business case.

This is an industry with a strong focus on innovation, including technologies that can later be licensed to the civilian industry and find more peaceful applications. It is also focused on the long term and is known to be a great capital compounder.

The sector also has multiple strong moats relying on different forces:

- Substitution costs: armies often use the same basic design for several decades, upgrading it as new technology emerges: for example, the Abrams US main battle tank from General Dynamics was first designed in the 1970s.

- Regulations and compliance: procurement procedures from ministries of defense are notoriously complex and give large, established firms an advantage. It is also a factor of why lobbying and long-term relations with decision-makers (politicians and generals) can make a difference.

- Intellectual Property: trade secrets and patents are hard-to-replicate advantages favoring the incumbents.

- Unique manufacturing infrastructures. If a company has built nuclear submarines for decades, it will be almost unbeatable at this activity and might be the only one with the right shipyard and certifications to do so.

All of these factors protect established defense firms from competition.

Assessing Defense Companies

Here are some key points to consider when assessing defense companies:

National Profile

The first thing to consider when looking at a defense company is its nationality. As it will mostly depend on public spending, we must accurately assess the country’s finances and politics.

The ideal country for investors in defense would have a profile like this:

- Spends at least 1.5% to 2% of its GDP on its military budget and plans to increase it.

- Has a society-wide consensus on the necessity of military spending.

- A healthy economy and low or no deficit, with a reasonable debt load (meaning the current spending can be sustained).

- The 10-year geopolitical horizon with neighboring or competing powers is tense, implying no reduction in the military budget soon (sadly, this might be less relevant today, as it might be true for almost all countries).

Exports can be important contributors to a defense company’s bottom line. Export contracts often go on for years and include lucrative spare parts and service contracts. Still, considering how politically and diplomatically sensitive defense contracts tend to be, excessive reliance on exports might be tricky and unpredictable.

A large and healthy national economy supporting its defense champions makes for a safer investing case, with export contracts as a welcome bonus.

Business Profile

While the industry as a whole can be attractive, individual companies are a different matter. Competitive position is very important here. A good defense company should have several successful designs that have been adopted by multiple countries.

It should also be recognized as an innovator, and its new designs to be both cost-efficient and reliable. For example, recent issues with the development of (too?) complex and expensive weapons like the F-35 fighter jet or the Puma tank should be red flags, in my opinion.

Lastly, the company should be active in “trendy” sectors that reflect a growing military need (and spending). For example, sectors like space, cyber defense & AI, drones & air defense, and hypersonic missiles.

Valuation

Because the defense industry is relying on relatively constant military spending, we should not base valuation by counting on explosive growth. This means that even in the context of expected increasing militarization, valuation should still incorporate a margin of safety.

This is especially true as part of the past 2-3 decades’ growth has come from consolidation and cost optimization. With fewer targets for M&A, this might not be true in the future.

In addition, some supply problems for Ukraine might indicate that cost rationalization has been pushed too far, for example, too little spare capacity in ammunition manufacturing or the production of older designs interrupted and hard to restart from scratch.

In my opinion, this indicates that the peacetime era of ever-increasing ROIC is probably over.

So P/E ratio should be ideally in the single digits or the 10-15 range at most, not higher. Similarly, conservative ratios for price-to-free cash flow or price-to-sales should be preferred as well.

Portfolio Construction

It can be difficult for investors with no deep knowledge of the military to decide which stock to pick. Is this new tank plane a technological marvel or a breaking-down mess?

For this reason, I would suggest that amateur defense investors should stick to a panel of large, established companies. The inconvenient truth is almost regardless of the performance of individual equipment, and the largest firms will continue to win contracts with the military. Dedicated ETFs are also an option, like the iShares U.S. Aerospace & Defense ETF or the SPDR S&P Kensho Future Security ETF.

Some geographical diversification might be good as well, as European defense spending is likely to stay way above its historical average for the foreseeable future. Their stock prices might also be lower than the more well-known US giant defense suppliers.

More knowledgeable investors might want to focus on specific subsectors or designs. If you think that the future of naval warfare will be submarines, it will make sense to focus on shipbuilders with unique experiences and shipyards in that field. The same can be applied to air, space, or drone warfare.

Conclusion

The defense industry is a stable and steady sector, likely to compound over time and give some dividend income. It is also an antifragile investment and will likely perform best when world tensions are rising, and globalization is stalling. It could provide some help in keeping portfolio volatility down.

Is it ethical to invest in defense companies? This is mostly a philosophical question better left to each person. Your opinion will depend on how you see war: as a sometimes necessary task to defend freedom or as an inherently evil thing.

From a purely investing perspective, I consider the defense industry a viable option IF the price is right. National budgets and economies have limits, and forever-growing budgets for weapons should not be the sole reason to justify an investment in the sector. Innovative and efficient defense companies trading at reasonable prices are the best bets for steady returns over the long term.

Industry Primers

The process of analyzing a company varies considerably from industry to industry. Many industries have their own vocabularies and specific concerns that investors need to consider. This series of articles looks at specific industries and at industry-specific factors that affect investments. The goals are to highlight specific risks, clarify confusing terminology and explain industry-specific metrics for valuation. These methods complement the usual evaluation process, they don’t replace it.