If you have debts that you cannot pay, debt settlement is a way to reduce them. Your debt settlement letter will offer a proposal to settle your debt in full for less than the amount you owe. A well-prepared letter has a better chance of success.

Key Takeaways

- Consider Debt Settlement Only When Necessary: Only opt for debt settlement if you truly cannot pay your debts. A settlement can reduce your debt, but your credit score will suffer.

- Be Realistic: Your creditor doesn’t have to agree to a settlement, and a very low offer may be refused. Offering as much as you can afford to pay will improve your chances of success.

- Require Written Acknowledgment: Get a written acceptance of your proposal before sending any payment so your payment being won’t be treated as partial fulfillment of the debt.

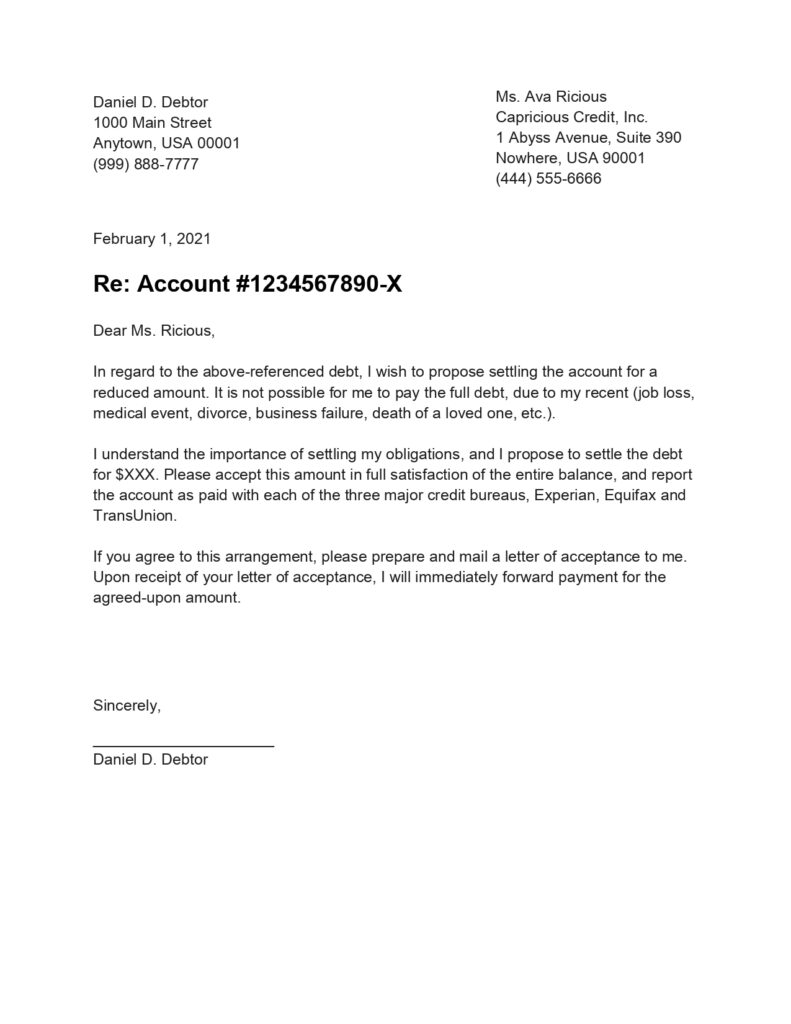

Sample Debt Settlement Letter

You can use the sample debt letter below as a template for your own debt settlement effort. Customize it to fit your individual circumstances.

Review the sample letter, then we’ll break it down with some items to consider for each section.

Daniel D. Debtor

1000 Main Street

Anytown, USA 00001

(999) 888-7777

February 1, 2021

Ms. Ava Ricious

Capricious Credit, Inc.

1 Abyss Avenue, Suite 390

Nowhere, USA 90001

(444) 555-6666

Re: Account #1234567890-X

Dear Ms. Ricious,

In regard to the above-referenced debt, I wish to propose settling the account for a reduced amount. It is not possible for me to pay the full debt, due to my recent (job loss, medical event, divorce, business failure, death of a loved one, etc.).

I understand the importance of settling my obligations, and I propose to settle the debt for $XXX. Please accept this amount in full satisfaction of the entire balance, and report the account as paid with each of the three major credit bureaus, Experian, Equifax and TransUnion.

If you agree to this arrangement, please prepare and mail a letter of acceptance to me. Upon receipt of your letter of acceptance, I will immediately forward payment for the agreed-upon amount.

Sincerely,

(YOUR SIGNATURE)

Daniel D. DebtorDownload debt settlement letter templates:

⏬ Debt settlement letter template for Microsoft Word

⏬ Debt settlement letter template for Google Docs

⏬ Debt settlement letter template in PDF

⚠️ Please Read Before Using This Template!

This template must be customized to fit your circumstances. You will see instructions for the information that you will need to insert. These instructions are indicated by ____ text.

Be sure that you fill in all required information and delete the ____ text before you send the letter.

Your letter will be less effective if our instructions are still visible!

What’s in a Debt Settlement Letter?

Now that you have a basic idea of what a debt settlement letter looks like, we can get into the details of each section, and why you need to convey the specific information shown.

Address Section

Though the address section may seem like more of a formality than anything else, it includes information critical to a debt settlement proposal.

Your Address

As the sample letter shows, you’ll enter your name, home address, and phone number at the top.

Using a post office box is not recommended, since time may be of the essence. If you visit your PO Box only infrequently, you may miss a deadline included in the creditor’s letter of acceptance.

The Creditor’s Address

Notice that the name of a contact person in the organization is included in the creditor’s address? This is a critical point.

If you simply address the letter to the company, it may never find its way to an individual who will act on your proposal. In a very large organization, correspondence not directed to a specific individual can easily end up in the dead letter file. If that happens, your proposal will never be read, let alone acted upon.

You should send a letter to the person you’ve been dealing with at the company. If there’s no specific individual, make a phone call and get the name of a person likely to be in a capacity to work with your proposal.

The Reference Line

The “reference” line should include the relevant account number. This must be included so the creditor will know exactly which debt you’re proposing to settle.

⚠️ The account number you’ll include on the reference line should be the one provided directly by the creditor. Account numbers listed on credit reports are sometimes scrambled, which makes them invalid.

The Body of the Letter

The body of your letter should be brief, two or three paragraphs at most. It should spell out the main points of your proposal. Anything more is unnecessary and could be misinterpreted.

Let’s look at each paragraph individually to explain what it should convey and why it’s necessary.

First Paragraph

Your opening paragraph should quickly state the purpose of your letter, which is a proposal to settle the account for less than the full amount.

In the next sentence, you’ll explain why you can’t pay the full amount. This revelation may convince the creditor that settling the debt is in their best interest.

In the last sentence, you should provide a reason why you won’t be able to pay the full amount. It should be a circumstance beyond your control. I’ve listed several within the parentheses, but feel free to include whatever situation may be preventing you from making full payment.

✍ You don’t need to be long-winded here. The creditor will either consider your proposal, reject it, or request additional information.

Second Paragraph

You’ll use this paragraph to present the details of your settlement offer. This will include the dollar amount you’re proposing to pay.

Note that we’ve also added the terms of the settlement. This paragraph should specifically state that your proposed payment will serve as full satisfaction for the entire debt.

If the account has gone into collection and is appearing on your credit report, you’ll also include a request that the creditor report the account as paid with all three major credit bureaus.

This won’t eliminate the collection account from your credit report, but a paid collection is better for your credit score than an open one.

Final Paragraph

In this paragraph, you’re making the assumption that the creditor is accepting your settlement proposal.

As such, you’re also making two important requirements:

- That the creditor acknowledges your settlement proposal in writing, and

- that you won’t send payment until that written acknowledgment is received.

⚠️ The second point is especially important. If you send a reduced payment without having written confirmation of your settlement proposal from the creditor, they may accept your payment as a partial payment on the full amount owed, then continue efforts to collect the balance.

Your Signature

Your letter will require your signature because you’ll be offering the creditor a contract, which is settlement of the debt.

If you fail to sign your letter, the creditor may interpret that as an indication you’re not completely serious.

What Should You Offer?

One of the most important components of your debt settlement letter is a single number: the amount you decide to offer. You’ll base that number on your assessment of two considerations.

- Affordability. Never offer more than you can afford to pay. If your creditor agrees to your proposal and you fail to make the payment, the agreement will be void and your creditor will probably not consider another proposal.

- Acceptability. You want to make an offer that your creditor will accept. You won’t know exactly what a creditor would settle for, so you’ll have to guess. If you go too low the proposal may be refused.

Remember that the average price that a collection agency pays for debts is 4 cents for each dollar of debt[1]✓

✓ Trusted source

Federal Trade Commission

FTC is an independent agency of the United States government responsible for preventing fraudulent, deceptive, and unfair business practices.. If you’re dealing with an original creditor, that’s about what they’ll get if they send your account to collections. If you’re dealing with a collection agency, that’s about what they paid for your debt.

⚠️ It’s not a good idea to exaggerate your financial hardships. Creditors and collection agencies can get your credit report and they have access to the information you submitted when you applied for credit, so they will have a picture of what you can afford to pay.

The Bottom Line

As you can see, writing a debt settlement letter is a fairly simple process. The letter itself is brief, primarily spelling out the details of your proposal, which is all it needs to do.

If the creditor is open to your settlement offer, they’ll either provide written acknowledgment or come back with a counter-offer for a higher amount. Either way, your letter will have accomplished its intended purpose of getting the creditor to accept less than the full amount to get the debt out of your life. Your credit score will take a hit – the creditor may be willing to forget the debt, but the credit reporting bureaus won’t – but you will no longer have to deal with collection efforts or the threat of lawsuits. That’s a start, and you can use that start to begin building a better financial record.

More Letter Templates

Our collection of free, fully-customizable letter templates is there to help you write effective letters when you need to set up, cancel or complain about something.