Table of contents:

Quick Stock Overview

Applied Materials by the numbers.

1. Executive Summary

A brief discussion of Applied Materials and its potential appeal to value investors.

2. Extended Summary

A more detailed explanation of Applied Material’s business and competitive position.

3. Semiconductors are the new oil

The vital role of semiconductor supply in modern economies.

4. Reshoring the semiconductor industry

Semiconductors are now a strategic resource, and one under threat.

5. Applied Materials Business

The strength of the business model and the company’s outlook.

6. Applied Materials Financial Results

AMAT profitability and growth.

7. Conclusion

Quick Stock Overview

Ticker: AMAT

Source: Yahoo Finance

Key Data

| Industry | Semiconductor equipment |

| Market Capitalization ($M) | 79,475 |

| Price to sales | 3.3 |

| Price to Free Cash Flow | 16.7 |

| Dividend yield | 1.08% |

| Sales ($M) | 25,159 |

| Free cash flow/share | $5.53 |

| P/E | 12.4 |

1. Executive Summary

Semiconductors are turning from a key industry to a potential geopolitical flashpoint. Semiconductor manufacturing is concentrated in a small, politically volatile area of northeast Asia. The pandemic-driven chip shortage has turned this key vulnerability into a policy concern.

This has led to a move to rebuild Western chip production capability. This is parallel to an increasing number of applications and inventory rebuilding which will keep chip demand high for years.

Geopolitical incentives and chip demand are driving a massive build-up in new semiconductor foundries. Each of these new foundries will rely on Applied Materials (NASDAQ: AMAT) for state-of-the-art machinery and systems.

As the leader of the upstream segment of the supply chain, Applied Materials is ideally positioned to benefit from this trend. It provides an opportunity for investors to bet on the industry without having to understand all the intricacy of leading-edge chip technology and decide which chipmaking specialist will prevail.

AMAT is also fairly valued, despite a very strong growth profile and a solid balance sheet.

2. Extended Summary: Why Applied Materials?

Semiconductors Are the New Oil

Semiconductors are now a vital commodity, powering every aspect of modern economies. Their production is highly concentrated in Northeast Asia and vulnerable to geopolitical conflict. This could become a major issue in the case of China looking to force a “reunification” with Taiwan, especially now that Russia has demonstrated the power of weaponized commodity supply.

Reshoring Semiconductor Manufacturing

The geopolitical importance of semiconductors is driving the West to rebuild its production capacity at any cost. This is true for all semiconductor production, not just the most advanced chips. One way to invest in this trend is to buy a company producing the equipment needed in new semiconductor foundries.

Applied Materials: The Business

Applied Materials supplies manufacturing equipment, software, and services to the semiconductor, display, and other industries.

Their primary business is in supplying semiconductor makers with highly sophisticated production equipment, with a few other segments active as well. The company has very strong moats and is the undisputed leader in its segment. The Company is well positioned to benefit from the move to reinvigorate US semiconductor manufacturing and the business outlook seems strong.

Applied Materials’ Financial Results.

Applied Materials’ financial results have shown solid growth for the last decade. Margin and ROIC are very high. Valuation ratios are relatively cheap, especially considering the growth, but the dividend yield is rather low.

This report first appeared on Stock Spotlight, our value investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 like-minded investors!

3. Semiconductors Are the New Oil

Semiconductors as a Commodity

Almost every single item we use nowadays relies on semiconductors to work properly. Chips and digital systems are not just for computers and phones. They are part of our cars, light appliances, watches, ovens, refrigerators, and much more. For example, a modern car uses no less than 1200 different chips. Modern life would grind to a halt without a steady supply of chips and other semiconductors.

That almost happened during the pandemic. Chip shortages crippled multiple industries, from car to computer manufacturing.

Still, the shortages were still relatively moderate. Production slowed down but didn’t stop. Nevertheless, the chip shortage showed how modern economies rely on a steady supply of cheap semiconductors, not only super-advanced chips for computers and smartphones but small digital displays for home appliances, controls for car systems, light switches, etc.

In practice, almost all factories require an input of chips the same way they require power, steel, or water. Most of these chips are standardized and relatively simple semiconductors. So outside of specific applications (computing, AI, etc…), semiconductors are akin to a commodity.

Semiconductors as a Strategic Resource

In theory, semiconductors should not be a highly strategic resource. Unlike oil or gas, they can be produced almost anywhere. At first glance, we could expect most countries to produce their own semiconductors, the way they produce their own steel, aluminum, or fertilizer.

Semiconductors and chips are much more technical products. Their production requires very advanced and expensive facilities, a highly specialized set of machinery and skills, and a very intricate and connected supply chain.

It also benefits from an economy of scale, encouraging the concentration of production in a few companies instead of a more decentralized structure.

Western countries are still central in designing and inventing new chip technology, especially the US which has been the leader since the 1950s.

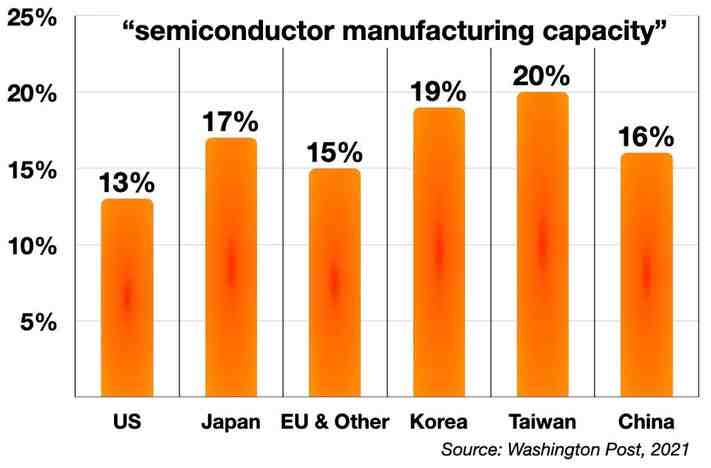

When it comes to actual manufacturing (the chip “foundry”), the semiconductors industry is now heavily dominated by East Asian producers. The US and EU together provide barely 27% of total production, with the rest being done in Taiwan, China, South Korea, and Japan.

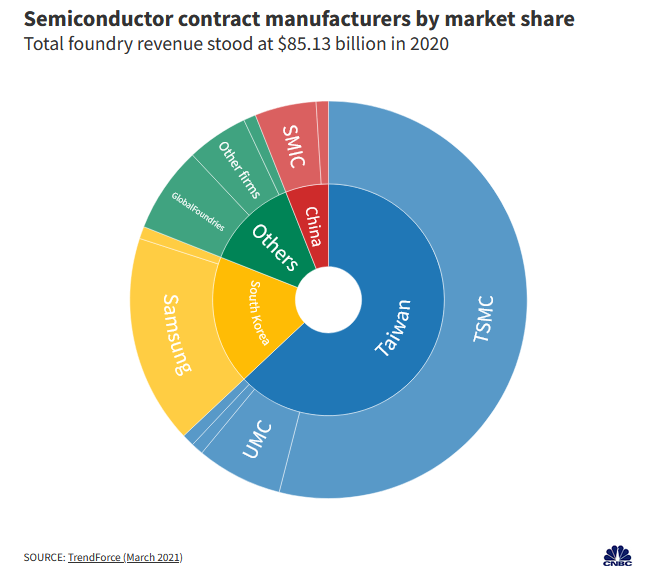

The chart above does not even give the whole picture. This is because while the Western countries produce some semiconductors, this is usually of the simpler type. The most advanced chips (with transistors smaller than 10nm) are ALL produced in Asia. Actually, 92% of them are produced by ONE company, Taiwan Semiconductor Manufacturing Corporation (TSMC).

These types of chips are vital for advanced applications, like computing, and AI, but also for weapon manufacturing. Without these chips, there are no satellites, anti-tank missiles, cyber defense, F-35s, and much, much more… And they are essentially all made in Taiwan.

This reflects in the revenue share of the industry. Taiwan is taking more than half of the world’s semiconductor revenue. Add South Korea and China and you have over 3/4 of global semiconductor revenue.

This system worked as long as the current world order was stable. Chips were made efficiently and cheaply in Taiwan and sent to assembly lines all over the world. In a very similar way, Russian gas & oil was efficiently and cheaply sent to the EU, powering German industry.

The war in Ukraine has shattered the assumption that such a state of affairs can go on forever. The EU energy crisis has made it obvious that relying on only one supplier for a vital commodity is a dubious strategy at best, and a catastrophe at worst.

This is directly relevant to the exponentially rising tension between the USA and China, which was exacerbated by Trump’s trade wars and is still ongoing under the Biden administration.

Finally, let’s not forget that China considers Taiwan not as a country, but as a separatist province that will be reunited with the mainland, peacefully or not, in the next decades at most.

Chinese President Xi Jinping pledged on Thursday to complete “reunification” with self-ruled Taiwan and vowed to “smash” any attempts at formal independence, drawing a stern rebuke from Taipei, which lambasted the Communist Party as a dictatorship.

Reuters

In that context, depending on Taiwan for chips seems very dangerous. Defending Taiwan would require a steady supply of the same weapons that could not be produced if Taiwan was under attack. All this while the Pentagon is warning that the war in Ukraine has massively depleted ammunition stockpiles.

A hot war would not even be needed to cause problems. Just a blockade of Taiwanese trade could be enough, the same type of blockade the Chinese navy just practiced in August, entirely surrounding the island of Taiwan in the process.

The US leadership is getting understandably nervous about the semiconductor industry. From now on, new semi factories need to be set on safer shores, irrespective of the costs such plans will entail.

4. Reshoring Semiconductor Manufacturing

Picks and Shovels

The semiconductor industry is extremely competitive and innovating constantly. Many major semiconductor makers don’t actually make semiconductors: they design them and outsource production to giants like TSMC. So it is hard to pick the right company without being an expert in the industry, and even experts might be hard-pressed to pick the companies that will do best from a transition to domestic manufacturing.

In addition, if the new US-based factories are owned by companies like TSMC, this makes hardly a good investing case. Yes, TSMC might survive in case of an invasion of Taiwan thanks to these factories, but its shareholders would still suffer dramatic losses.

Intel is a “safer” company, but it might be losing its edge regarding advanced (and profitable) technology. We come back to the difficulty of picking the winner in a highly competitive and R&D-driven industry.

This is why I propose to take a step back. In every gold rush, there are two ways to make money. One way is to go into the wilderness and look for gold yourself. It might work, or it might be an abysmal failure. You need to know where to find the gold, and luck will play a big role in your eventual success or failure.

The other way is to sell the picks and shovels to the gold prospectors. There is no need to pick the best mining spot or get lucky. You just need to be at the right place and sell the right equipment.

This is what I am proposing to do regarding the reshoring of the semiconductor industry. Instead of trying to find which foundry will be a winner, why not invest in the companies selling the equipment that goes into all of the new foundries?

One such company is Applied Materials.

The Semiconductor Industry

AMAT produces and sells the machinery, sensors, tools, and other equipment needed to produce semiconductors. This is an extremely complex and technical industry and I am frankly not an expert in that field.

To get my knowledge up to date, I read material from multiple sources. If you are interested to do so yourself, I can recommend the Youtube channel of Asianometry as a good start. Here are a few takeaways:

- Theoretical progress in semiconductor design is not that hard (both China and the Soviets were keeping up with the US for decades). Production at scale with a high yield (not many faulty chips) is extremely difficult.

- The key shortages are not really about below 10nm state-of-the-art chips, but for more mundane, “old” designs, massively used by the auto and defense industries, among others.

- The most advanced chips require unique tech like Extreme Ultraviolet Lithography (EUV). The US forced an embargo on shipping such technology to China under the Trump administration. Even more regulations/sanctions are in discussion for less advanced equipment.

- The industry is very complex, with each step essentially an oligopoly dominated by a few companies. No one controls the whole value chain (theoretical research -> machinery -> design -> foundry), not even giant like TSMC. Specialization is the key to success.

Building New Foundries

As I said before Asian dominance of the semiconductor industry was fine in a time with no serious risk to international trade. Covid and the Ukraine war shattered these assumptions.

In July 2022 the US Congress passed the $280B CHIPS act to rebuild the domestic semiconductor industry. It will include $50B in subsidies to boost the domestic chip manufacturing business.

This is not all the money that will be spent on US-based foundry. Even before the CHIPS act, many projects were already on the way. This includes a $12B factory from TSMC, with maybe 5 other plants as well. Also, the $20B factory in new facilities by Intel, making it “the largest on the planet”, and the $17B investment by Samsung in Texas, next to the $5B Texas plant by GlobalWafer, and the $5B plant by Wolfspeed in North Carolina.

This trend is not exclusive to the US. For example, Italy will receive a $5B new factory from Intel as well, and there’s €5.7B of local investment in France.

All in all, there is a rush of activity for new facilities able to churn out more semiconductors. Each of these new foundries will need tons of equipment, from the bleeding edge tech like EUV to the simpler and mundane factory lines, captors, software, filters, ventilation systems, etc…

It is certain that TSMC or Intel will not be looking for the cheapest supplier. Even the smallest subpar component in a semiconductor factory can lead to poor yield or problems for the whole factory. They are likely to stick to tried and trusted suppliers, and that leads them straight to AMAT.

5. AMAT’s Business

Overview

AMAT is working in the upper part of the semiconductor value chain. It provides the semiconductor industry with the machinery it needs to produce chips. The company employs 31,900 people and generates a total of $25B in annual revenue. AMAT manages most of its sales directly, not relying on distributors.

The company specializes in equipment for the semiconductor industry, but also for a few other sectors. This includes Display (screens), Solar, Roll-to-Roll coating (electronic printing on flexible film), and Automation software/Smart Factory.

Almost 3/4 of revenues come from the semiconductors segment. AMAT experienced explosive growth in the 2020-2021 period, before coming back to the previous growth trend:

| TTM | 2021 | 2020 | 2019 | |

|---|---|---|---|---|

| Semiconductors | – | $16.2B | $11.4B | $9B |

| Solar and others | – | $5.2B | $4.2B | $3.9B |

| Display | – | $1.6B | $1.6B | $1.7B |

| Total | $25.2B | $23B | $17.2B | $14.6B |

Most of the sales (86%) are to customers in Asia, notably China (33%), Korea (22%), Taiwan (20%), Japan (8%), and South-East Asia (3%).

AMAT’s headquarters is in Santa Clara, California. Its semiconductor-related products are manufactured in California, Texas, Montana, Israel, and Singapore.

So while the company’s clients might be in Taiwan, China, or Korea its production facilities are in much safer locations. This makes AMAT a rare haven of safety regarding geopolitical risk in the semiconductor industry.

If anything happened to AMAT’s clients in East Asia (like a China-Taiwan war), the loss of revenue would be offset by a massive and panicked build-up of capacity in other regions.

AMAT’s Moats

Besides its safety from a geopolitical point of view, AMAT is a high-quality company.

It is a leading supplier in the industry and sells directly to the most prominent companies in the sector. 20% of its business is done with Samsung, 15% with TSMC, and a bit below 10% with Intel.

The industry is inherently “moaty”, as good products lead to a dominance of the market, leading to more revenue, giving more money to keep innovating, and leading to more dominance. The same dynamic that has led TSMC to control half of the industry revenue is at play with AMAT.

The industry demands extremely high levels of capital and expertise, making it difficult for competitors to enter.

On top of this “general” moat, you can add the substitution cost. Any competitors need to prove an outstanding superiority to an existing user of AMAT’s tools. Anything less than that would make the risks of substitution too high.

The only risk for AMAT’s market position would be a technological shift away from its current and future offerings.

If we are to believe the company’s management, this is not a threat but an opportunity. The company seems to be the leader in the yet-to-be-implemented next technological progress.

The major technology roadmap inflections—including Gate All Around transistors, Backside Power Distribution Networks, new materials for interconnect and contact, and Heterogeneous Integration of chips and chiplets—are enabled by materials engineering where Applied Materials is the leader, and this shifts more dollars to our available market over time.

Gary Dickerson, AMAT CEO

As I said, I am not a semiconductor engineer, so I am honestly not qualified to judge if AMAT is truly the leader in “Backside Power Distribution Networks” or “Heterogenous Integration”. But considering Samsung, TSMC and Intel are currently trusting AMAT to deliver high performance, I think we can expect them to stay the same in the next 3-5 years at least.

AMAT’s Operations

The company is offering tools and software for virtually every step of the chip manufacturing process. It is spending a large $2.5B/year in R&D, up from $2.2B in 2020 and $2B in 2019.

As AMAT products encompass all of the activities of a foundry, they can also offer integrated solutions. Each of its machinery lines can be integrated with each other, using AMAT’s software. That creates an incentive for buyers to add more AMAT products.

This level of synergy makes the substitution costs an especially strong moat. Replacing an AMAT tool or software can mean redesigning a whole part of the foundry operation, retraining technicians, ironing out bugs, needing extra checks to detect faults in the chips produced, etc.

Marketing & sales operations are remarkably lean, with a total cost of only $0.6B in 2021, compared to the $23B in sales. Or a sales cost-to-revenues ratio of just 2.6%. It seems to me that at this point, sales are more based on established relationships, reputation, and innovation rather than on the sale process itself. Because the industry is dominated by a relatively small number of established manufacturers, existing relationships matter more than developing new customers.

Similarly, overhead is just $0.6B. This means that the company could scale up sales up to its maximum production capacity without much increase in sales or administrative costs.

Overall, AMAT operation seems very efficient, with a very lean sales and administrative side, and most of the money going to innovation and maintaining high margins (more on that in the valuation chapter).

AMAT Investments

Relying on its expertise with silicon and manufacturing at the nanometer scale, AMAT is also investing in promising companies. The company invests around $100M per year in startups through its Venture Investment Branch.

AMAT has currently invested in a venture portfolio of 90 different companies. A complete analysis of this portfolio would turn into a report in itself, so I will have to keep it short.

What I find interesting is the presence of next-generation computing technology, like printed electronics, silicon photonics, and optical communication (via lasers). It is also touching new fields, like 3D printing/additive manufacturing, lithium-ion batteries, and electric motors.

It might seem like a very diverse portfolio, but every single one of these ventures relies on precise, atomic-level re-arranging of matter. That exact same field has been the center of AMAT’s expertise since the 1960s. So while applications might diverge, this is actually right at the core competency of the company. AMAT is uniquely qualified to evaluate startups in these industries.

Quite a few of these startups have been acquired, offering AMAT successful exits.

While this is surely profitable, I think it could be interesting for shareholders to maybe see the company going all in for at least one new application, adding a new segment to the current solar+display+semiconductors. 3D printing equipment has the most potential in my opinion.

AMAT is also partnering with multiple universities, research institutes, and companies. These partnerships seem to work together with venture investment in fields like battery technology, 3D printing, and medical treatments using nanotechnology.

AMAT Outlook

AMAT’s moat from a supply chain and technology point of view looks secure. So how is the business outlook?

While I assume new foundries built up all over the world should be good news, I preferred to check it up. I mentioned AMAT revenues jumped in 2021, and so did its backlog:

| 2021 | 2020 | |

|---|---|---|

| Semiconductor | $6.7B | $2.9B |

| Solar and others | $4.3B | $2.6B |

| Display | $0.7B | $1.1B |

| Total | $11.7B | $6.6B |

Despite the generally cooling global economy, the backlog has only grown. At this point, it is beyond 12 months, with AMAT clients providing longer than usual visibility about future demand. And that was before the USA decided to provide an additional $50B in subsidies for new foundries.

We expect Applied to remain supply constrained for the next several quarters, we are working through our very substantial backlog of orders which provides a buffer to in-year demand fluctuations and, in addition, customers are providing us with longer-term visibility and commitments in response to their own customers’ actions to lock in the strategic capacity they need.

Gary Dickerson, AMAT CEO

The Twelve-Trailing-Months (TTM) revenues also seem to indicate that demand is not slowing down. The only sector slowing down is Display, which makes sense as people are buying fewer TVs and computers.

I think the need to improve the efficiency of current foundries was a big reason for the jump in sales in 2021, along with AMAT’s clients being flush with cash and overwhelmed by demand.

Because consumers of chips are also likely to start building a much larger inventory, I think chip demand is going to stay somewhat elevated for a while, at least outside of the consumer electronic markets. This should give AMAT’s client the cash and confidence needed to go forward with the plans for new foundries.

So going forward, the demand will be driven by the need to keep current foundries running, along with building new ones.

6. Financial Results

Key Metrics

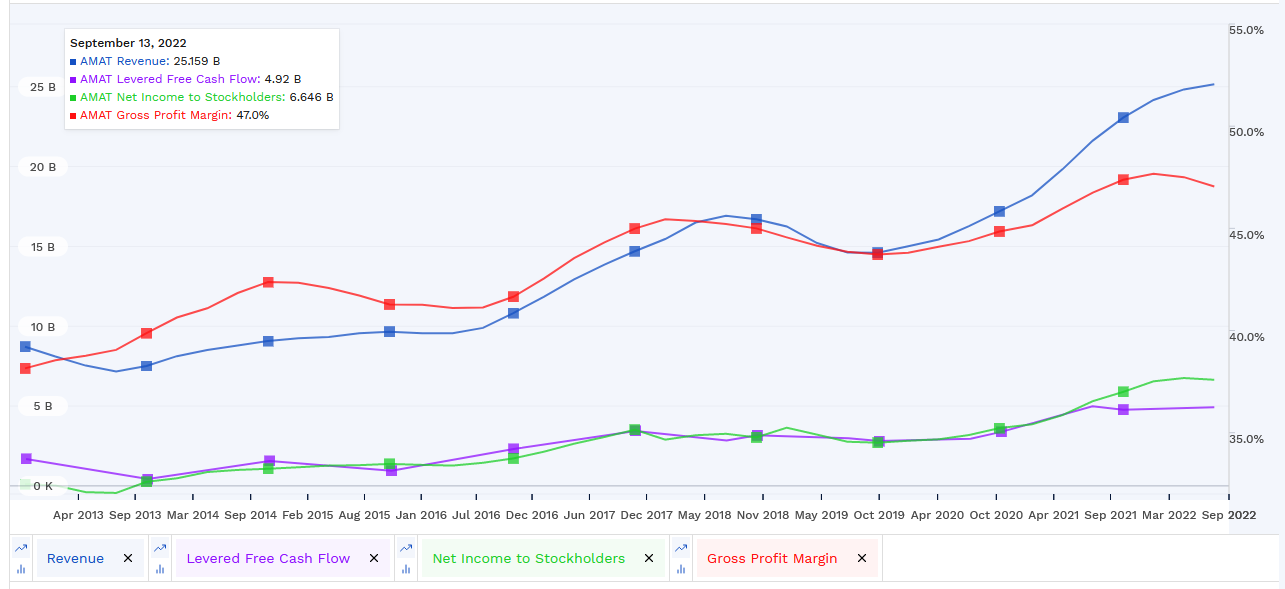

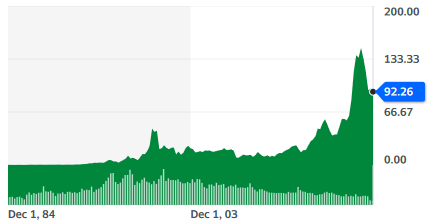

The 10-year trajectory of AMAT is in a steadily upward direction. This was to be expected for a high-quality company, a leader in its market, in a quickly growing sector that become of prime strategic importance.

Free cash flow has yearly grown on average at 11.7%. Free cash flow/share has jumped 15.9%, boosted by a share repurchase program.

The gross profit margin has grown over time and is now at a very impressive 47%. This has supported a very high average yearly growth of net income of 52.8% (starting from a very low point in 2013).

The company has very little net debt compared to its assets (less than half of the yearly free cash flow).

CAPEX is steadily growing, so AMAT is not obtaining these results by cutting on needed investment. At the same time, it is not over-enthusiastic with outsized expansion and new factories, which could damage long-term profitability.

Return on capital has also gone up over time, growing 37.8% yearly on average. It is now at an extremely high level of 37% (for reference, most companies will have an ROIC between 5-15%).

Financial Outlook

I would expect some of this growth to slow down, especially on the gross margin and ROIC. These metrics can only go up so much.

Revenues, net income, and free cash flow are more likely to keep the current direction going. This is supported by the geopolitical shifts I mentioned before, but also by the background growth of the semiconductor industry in general, with the world economy still digitalizing quickly.

The Internet of Things (IoT), wearable devices, the electrification trend (including EV), advanced AI, cloud, automatization, drones, and e-commerce, all are growing quickly. Each of these innovations will require more chips, from simpler old designs to ultra-advanced 10nm or smaller chips.

Similarly, we still spend most of our life working and living with screens. So the temporary weakness in display sales should not be worrying.

For the solar segment, the outlook is even better. Fossil fuels are at high prices or outright impossible to source right now in Europe and emerging countries. The push for decarbonization is ever stronger. So more solar cell factories, needing AMAT’s machinery, are almost a guarantee.

Valuation

With very solid financials and market position, it is safe to consider AMAT a quality company. Nevertheless, I still think that valuation matters for long-term returns. Excessively high multiples could hurt investors even if the company delivers perfectly on growth and business performance.

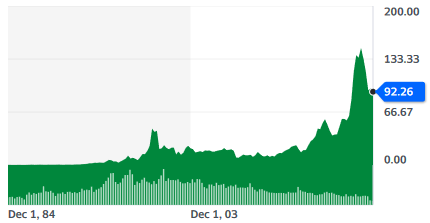

AMAT is not especially expensive at the moment. P/E is at 12.4, price to sales at 3.3, and price to free cash flow at 16.7.

These ratios are nowhere near deep value territory. But they are also far from overvaluation territory. Considering the growth profile of the company, this makes it at least fairly valued, or even undervalued.

Ratios are at these levels partly due to the stock’s drop from its 2021 highs of $147. The whole semiconductor industry has temporarily suffered from the post-pandemic cooling of demand. But considering the build-up of new foundries all over the world, this seems overblown in the case of AMAT.

The main risk for the company would be a brutal global recession, depressing the demand for all items like electronics, cars, etc.

Paradoxically, such a recession would be almost a guarantee of even worse international tensions. This would boost the trend of reshoring semiconductors in the USA and Europe, increasing demand for AMAT equipment to equip the new foundries.

So I think the semiconductor industry as a whole could be vulnerable to a recession, but AMAT will be a lot less sensitive to the macro environment than the rest of the industry.

In the very long term (5-15 years), we can imagine a bear case scenario where the current build-up of foundries turns into a slump. This would be especially the case in a prolongated downturn in demand from a persistently weak economy (maybe driven by persistently high inflation).

7. Conclusion

AMAT / Applied Materials is a very high-quality company, well positioned in a key sector of an increasingly important industry. The company benefits from the strong moats of substitution costs, valuable IP, and industry structure favoring oligopolies or monopolies.

Leading a key segment of the semiconductor supply chain is a great spot to be in right now. Growing demand for AMAT equipment is driven in part by the trends of digitalization, electrification, and other innovation like cloud computing, drones, IoT, etc. It is also driven by rising geopolitical tension, the re-shoring trend, and the need for redundancy in semiconductor production capabilities.

The company has shown stellar financial performance over the past decade. Its margins and ROIC are very high. Revenues, free cash flow per share, and net income are growing, while the debt is very low.

If I had to complain about something, it might be a somewhat low dividend yield and a too conservative strategy. AMAT could distribute a bit more profit and leverage its expertise in new applications like 3D printing more aggressively. For that matter, a little more leverage would hardly endanger the company.

The company is a good investment for a conservative and long-term growth portfolio. Its cautious financial management and technological leadership in its highly-specialized segment make it inherently safer than other companies in the semiconductor industry. Its current valuation also seems to provide some margin of safety.

Still, it should be remembered that while the company should benefit from the current foundry build-up, it might run into a slump in demand in 5-10 years, in case the chip production capacity turns excessive compared to demand.

So this is more of a long-term investment to sell at some point in the future, but not a buy-and-forget stock.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in AMAT or plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation from, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.