The dollar is the world’s dominant currency. It accounts for a large majority share of foreign exchange transactions, loans, and foreign exchange reserves. When the world trades, it trades in dollars.

That dominance has prevailed for many years. But how was that dominance established? What effect has it had on the US and on the rest of the trading world? How long will it last?

Just How Dominant Is the Dollar?

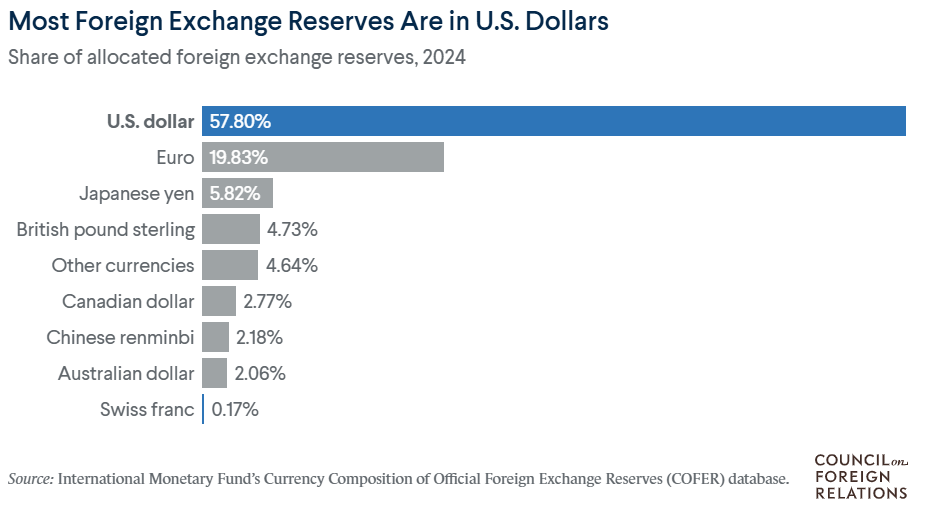

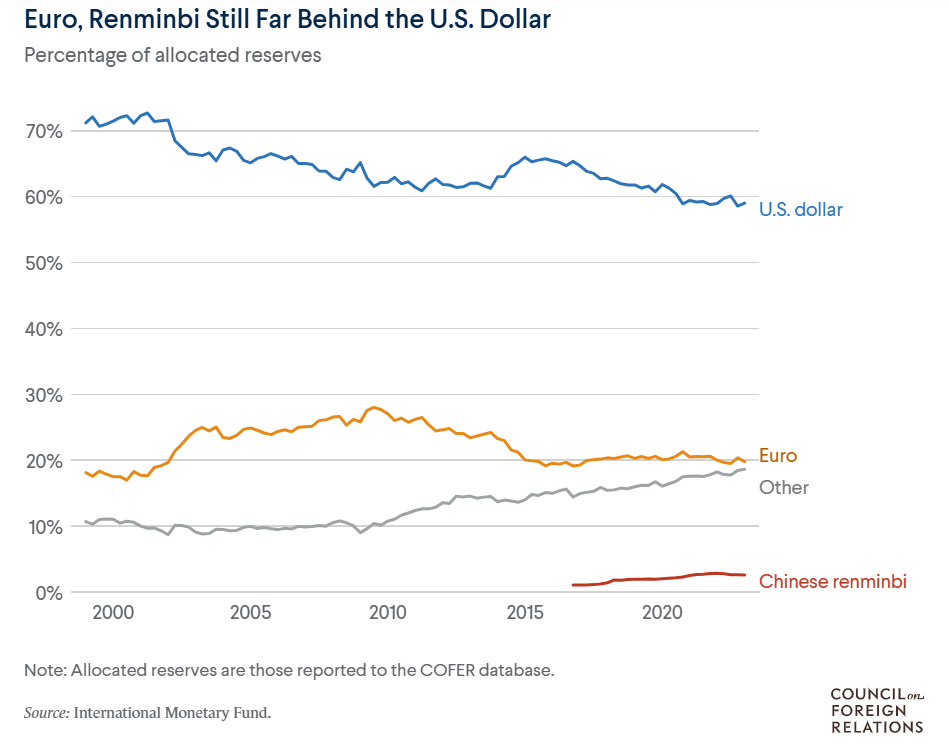

The dollar’s dominance in global trade and among global reserves is hard to overstate. Dollars account for a large majority of global foreign exchange reserves.

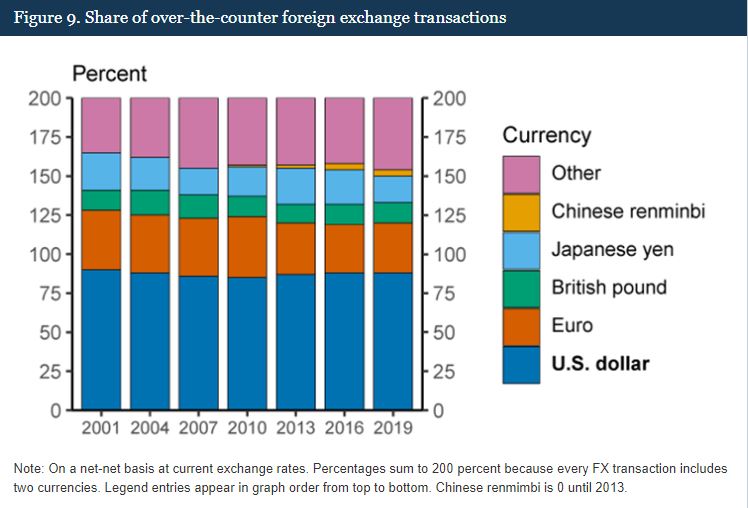

The dollar is also the currency most often included in foreign exchange transactions by a wide margin.

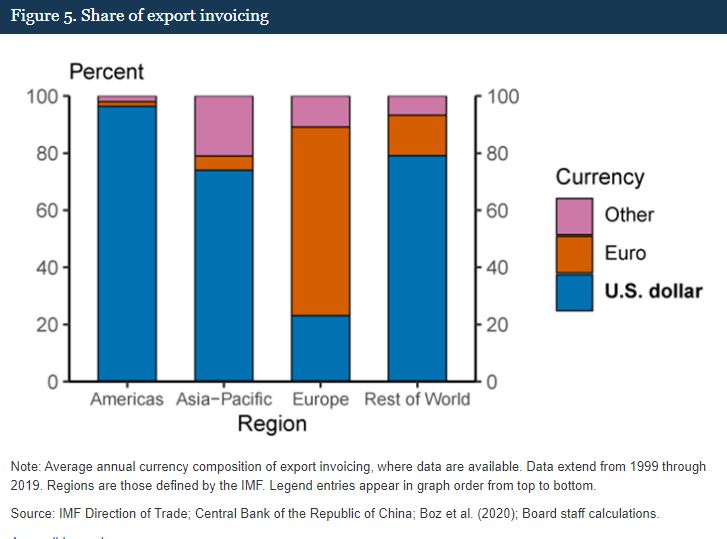

A large majority of exports are invoiced in dollars, except within Europe.

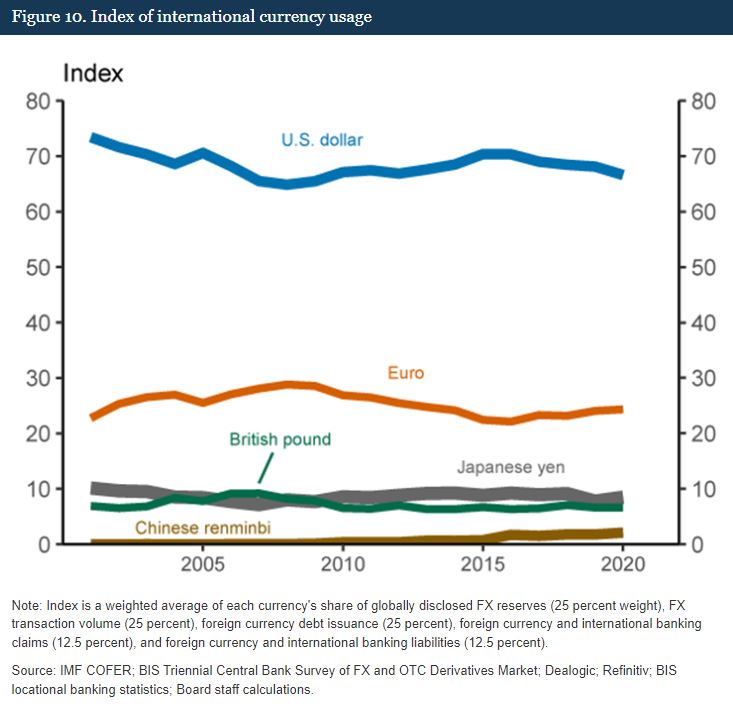

The Index of International Currency usage, which combines multiple factors, including reserves, transaction volume, debt issuance, banking claims, and others, shows just how dominant the dollar is.

The overwhelmingly dominant role that the dollar plays in global trade is often controversial and often misunderstood. It has been called an exorbitant privilege and an exorbitant burden. It has spawned a legion of conspiracy theories.

To begin exploring this dominance and its impact, we’ll start at the beginning.

How Did the Dollar Become Dominant?

International trade has always been dependent on finding an acceptable medium of exchange with a defined and agreed value. For centuries there were no standard solutions: Florins, guilders, and Mexican silver dollars were widely accepted and used in different times and regions, but there was no common standard. Some countries linked their currencies to gold and others to silver or used precious metals as trade currencies.

By the 18th century, the pound sterling emerged as the dominant trade currency, a condition that prevailed through 1914.

Britain and most other European countries suspended gold convertibility during the First World War, leading to a period of financial chaos when nobody was sure what any currency was really worth. Hyperinflation and economic depression in many countries played key roles in the emergence of fascism and the buildup to the Second World War.

The Bretton Woods Agreement

In 1944 730 delegates from 44 countries met in Bretton Woods, New Hampshire, with the lofty goal of setting up an orderly system for defining the value of money and enabling global trade on consistent terms.

Given the economic dynamics of the day, the choice of the US Dollar as the index currency was natural. The decision was that the US dollar would be linked to gold and that all other currencies would have a fixed value against the dollar.

Countries that were unable to maintain their exchange rate could petition the newly formed International Monetary Fund for a rate adjustment.

The Bretton Woods Agreement did not mandate that trade would be conducted in dollars, but it left the dollar as the obvious choice for trade.

The Collapse of Bretton Woods

After the Great Depression and the Second World War, the world craved order and stability, and the Bretton Woods Agreement seemed orderly and stable. The dollar was linked to gold and everything else was linked to the dollar. Gold ruled, and currency had defined value. Hyperinflation seemed impossible.

Reality is never that stable and rarely obeys the orders of humans.

The stability of Bretton Woods was its own undoing. With currency values fixed and accepted, global trade surged. Since the traders all wanted dollars, demand for dollars surged with trade.

With the demand for dollars rising, banks outside the US began making dollar loans, often for more than they had on deposit. The number of dollars in circulation exploded, each of them a claim on the US gold reserves (people of a certain age will remember the panic over “Eurodollars”). High government spending on social programs and the Vietnam war added to the burden.

By the late 1960s, it was apparent that the US simply didn’t have enough gold to meet the demand for dollars. In 1971 the US abandoned the gold standard and adopted a free-floating exchange rate set by supply and demand. The Bretton Woods system ceased to exist.

After Bretton Woods

When the Bretton Woods agreement collapsed, countries adopted different arrangements: free-floating currency, pegs to a single currency or a basket of currencies, or participation in a currency bloc. Today the free-floating system dominates: currency values are set by supply and demand.

The collapse of the Bretton Woods agreement did not break the dominance of the dollar. If anything, it enhanced it. Traders still needed a consensus currency to work with, and the dollar was the obvious choice.

Why the Dollar?

A trade currency needs certain features, and there’s no other currency that has them to anything like the extent that the dollar does.

- Liquidity. There has to be enough currency in circulation to support the demand from international trade.

- Universal acceptability. Almost everyone, anywhere in the world, accepts dollars as payment for goods and services.

- Universal convertibility at market-determined rates. Many countries deliberately manipulate exchange rates. Traders don’t want that.

- Reliable, transparent settlement systems. Traders want money to flow fast and smoothly.

- Incumbency. Inertia is a potent force, and it’s always easier to keep using what you’ve been using unless there’s a compelling reason not to.

👉 For Example

A company in South Korea sells a shipment of excavators to a construction company in Sri Lanka. If they take payment in Sri Lankan rupees, they have a problem. They can only spend those rupees on products from Sri Lanka, which they don’t need. Their bank won’t accept rupees for deposits. They will have to convert the rupees into won or dollars, and there’s limited demand for Sri Lankan rupees in South Korea.

If they ask for payment in won, the buyer will have to either sell something to a South Korean company and get paid in won or buy won on the open market, which might be difficult for them.

So they just use dollars, not because they have a prejudice toward the US, but because it’s easier and more convenient. Dollars can be bought, sold, or spent pretty much anywhere and at any time.

It’s important to remember that most world trade is conducted by private companies, not governments. They aren’t concerned with politics or policy, they want smooth, easy, convenient transactions and they want to be paid in currency with predictable value that they can spend anywhere.

Is The Use of the Dollar Mandatory?

A widely circulated conspiracy theory holds that the use of the dollar is somehow required in international trade, particularly in purchases of oil. This is, of course, not true.

If we look at the export invoicing charts cited above, we’ll see that while the dollar dominates trade, it doesn’t have a monopoly. Close to 80% of trade in Europe is invoiced in currencies other than dollars, along with nearly 25% in Asia and 20% in the rest of the world. This would not be the case if the use of the dollar was required.

But What About the Petrodollar?

A variation of the mandatory dollar theory involves “petrodollars.” The belief is that oil transactions can only be conducted in dollars, and if someone trades oil in any other currency, the dollar will collapse and its dominance will end.

This theory has no basis in reality. The price of oil, like the prices of most globally traded commodities, products, and services, is quoted in dollars for convenience, but the parties to a transaction are free to settle in any mutually agreeable currency. If the Kuwait National Petroleum Company wants to sell oil to a South Korean utility and take payment in Thai Baht or Italian Lire, nobody will stop them from doing it. In practice, though, almost everyone uses dollars.

Oil and gas are important commodities, but they do not dominate world trade or demand for dollars. Together they make up about 10% of global trade, including the substantial oil and gas trade of the US itself. A move by some countries away from dollars for oil trading would not have a dramatic impact on the global use of the dollar or the value of the dollar.

The term “petrodollar” does not describe an oil trading system. It is simply a dollar earned by trading oil. The term gained prominence in the 1970s when economists worried that oil-producing nations were accumulating dollars faster than they could spend them, and it’s still around. There is nothing about “petrodollars” that poses an imminent threat to the US or the dollar.

The Dollar’s Dominance: Privilege or Burden?

In the 1960s, Valery Giscard D’Estaing (then the Finance Minister of France) referred to the dollar’s role as the international trade and reserve currency as an “exorbitant privilege.” The term has endured and is regularly used in financial discussions.

An opposing theory, emerging more recently, holds that the dollar’s primacy imposes an exorbitant burden on the US.

Why is it a Privilege?

Most exporters want to be paid in dollars. If a country wants to import, it has to earn dollars with its own exports before it can spend dollars on imports. If the value of the exports won’t cover the cost of the imports, the country has to borrow.

Because the US pays for its imports in its own currency, it doesn’t need to earn dollars to pay for its imports. It can simply print more dollars, allowing the country to run a trade deficit without the penalties that others would suffer.

More recently, the ubiquitous use of the dollar has allowed the US to use the dollar as a weapon by threatening or imposing sanctions that would exclude countries from dollar settlement systems. These sanctions have rarely been effective (countries can trade in other currencies), but they are still perceived as a unique capability for the US.

Why is it a Burden?

Having a currency used as a trade and reserve currency also creates problems for a country.

Overvalued Currency

A trade currency is always in demand, and that keeps its value high relative to other currencies. We tend to think of a strong currency as a good thing, but it often isn’t.

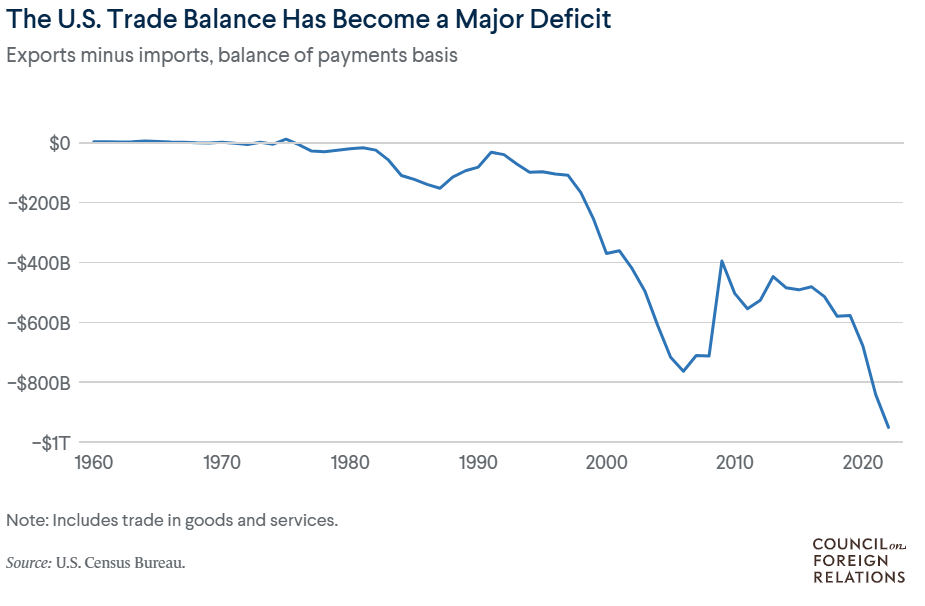

A strong currency makes a country’s imports cheaper and its exports more expensive. That created an incentive to import and a disincentive to export. It’s also a huge incentive for companies to move key functions overseas, where they can be paid for in cheaper currency.

The persistently high value of the dollar is a major reason for the US trade deficit and the move toward “offshoring” business functions. An artificially strong currency cuts exports and hurts jobs.

Loss of Control

A trade and reserve currency is no longer only a national currency. It becomes a global currency. Banks all over the world accept US dollar deposits and issue US dollar loans. Many banks issue loans far in excess of their deposits, effectively creating new dollars.

Any currency that becomes a global currency will be in the same situation. The issuing country will not only have an overwhelming incentive to print more of its own currency but will lose control of the supply of its currency generated outside its borders.

Will the Dollar Remain the World’s Currency?

We hear constant speculation that the dollar’s reign as the world’s trade and reserve currency is coming to an end. The less exciting truth is that this will probably not happen any time soon. The dollar may not be the perfect global currency, but there are very few attractive alternatives.

The dollar is far ahead of every other possible contender.

The only realistic contenders, the Euro and the Chinese Renmimbi or Yuan, each have serious drawbacks. The Euro does not have a unified Treasury or bond market behind it. The Renminbi is held back by a high degree of government intervention in exchange rates and capital flows. Neither currency has anything close to enough liquidity to underwrite international trade.

🤔 Common Question: Why does China have two currency names?

💬 The currency of the People’s Republic of China is called the Renmimbi, but a unit of that currency is called a Yuan. It’s as if there were different terms for “the dollar” and “a dollar.” In practice, the terms are interchangeable.

More important, neither China nor the EU would want their currency to become the dominant trade and reserve currency. China is the world’s leading exporter and the EU is second. A move toward the use of their currency as a global trade medium would inevitably push the value of their currency up and the competitiveness of their exports down. For export-dependent economies, this is potentially devastating. China has consistently intervened to keep the value of its currency down and support its exports.

Could There Be a New Currency?

Proposals for a world currency are not new: economist John Maynard Keynes proposed a global currency called the Bancor at the Bretton Woods conference, but the proposal was rejected.

More recently, it has been suggested that the International Monetary Fund’s Special Drawing Rights or SDR could emerge as a global currency. That would mean introducing the SDR as a medium for private transactions, not just government transactions with the IMF, and the IMF would need to have the power to control the supply of the SDR. Given the general mistrust of the IMF in much of the world, this isn’t likely to happen.

Still, others have proposed a blockchain-based cryptocurrency, but nothing even remotely appropriate for the task has emerged, and the wild fluctuations in cryptocurrency prices are not conducive to use in trade.

It is very unlikely that any currency will take over the dollar’s current dominant share of reserves and trade invoicing. What is likely is that the use of other currencies will gradually increase, slowly eroding the dominance of the dollar without a move toward a clear replacement. As global currency exchange rates and mechanisms become more transparent, this becomes more viable.

That is not necessarily a bad thing for the US. A gradual reduction in demand for dollars would allow the dollar to achieve a less inflated value, boosting exports, making imports less desirable, and creating less incentive to move business functions out of the country. That would help the US more than it would hurt.