Warren Buffett is not America’s richest man, but few – if any – Americans have been so rich for so long. Buffett has been a billionaire for forty years, and both the rise and longevity of his wealth are intimately tied to a key feature of his core business: the insurance float.

Let’s take a closer look at the insurance float and how Buffett used it to lay the foundation of his wealth.

Key Takeaways

- The insurance float is money that has been paid in premiums and not yet paid out in claims. This is cash that the insurance company holds but does not own.

- Insurance companies make money by investing their float. For most companies, premiums and payouts balance. The float is where they make their money.

- Buffet has become wealthy by successfully investing his float. Buffett’s investments have been consistently highly profitable over the long term.

What Is an Insurance Float?

Most people understand insurance industry terms such as premiums (the money a policyholder pays every month or every year for an insurance policy) and claims (the money an insurer must pay out).

But do you know what happens to your paid premiums once they’re sent to the insurance company?

Insurers don’t pay out all the money they collect right away. Rather, an insurance company will collect money in the form of premiums, invest that money, and then pay out claims as needed at some future date. The difference between premiums collected and claims paid out is called the insurance float.

It’s a lot like how a bank will collect deposits, invest that money (through loans to other people or companies), and then repay your money at some future date when you eventually make a withdrawal.

The insurance float has been a huge contributor to Warren Buffett’s success with Berkshire Hathaway. Because premiums received are essentially like loans from policyholders (that only need to be paid back when a claim is made sometime in the future), Buffett has been able to use insurance float as leverage when investing in stocks and private companies, which has a significant (positive) impact on the company’s return for its shareholders.

Insurance companies were among Buffett’s earliest holdings. He purchased National Indemnity and related companies in 1967 and subsequently added GEICO and National Re. He now operates multiple insurance ventures under the Berkshire Hathaway brand.

It’s part of the reason why Berkshire Hathaway’s book value and market value have grown impressively over the decades, with the company topping $1 trillion in market value in 2024!

So, let’s dive a little deeper into what insurance float exactly is and how Warren Buffett uses it to his advantage.

Warren Buffett and Berkshire Hathaway’s Insurance Float

The insurance float represents the available reserve, or the funds available for investment, once the insurer has collected premiums but is not yet obligated to pay out in claims.

In his 2002 Berkshire Hathaway Shareholder Letter, Warren Buffett explains:

To begin with, the float is money we hold but don’t own. In an insurance operation, float arises because premiums are received before losses are paid, an interval that sometimes extends over many years. During that time, the insurer invests the money. This pleasant activity typically carries with it a downside: The premiums that an insurer takes in usually do not cover the losses and expenses it eventually must pay. That leaves it running an “underwriting loss,” which is the cost of float. An insurance business has value if its cost of float over time is less than the cost the company would otherwise incur to obtain funds. But the business is a lemon if its cost of float is higher than market rates for money.

So insurance float is the difference between premiums received today over claims that must be paid many years in the future. During that time, the insurer invests the money. Insurance float is so valuable that insurance companies often operate at an underwriting loss – that is, the premiums received are not enough to cover the eventual losses (hurricanes, car accidents, etc.) that must be paid and the expenses required to resolve those claims, operate the business, etc.

Why would an insurer operate at a loss? Again, because the insurer can invest the insurance float and make even more money. In this sense, insurance float is like a loan, and the underwriting loss is like the interest rate on that loan (i.e. cost of capital).

Now, for most insurers, the cost of float is usually a few percentage points. Berkshire Hathaway’s insurance operations, however, are so well run that the company’s historical cost of float has actually been positive… meaning Berkshire Hathaway is actually being paid to take other people’s money!

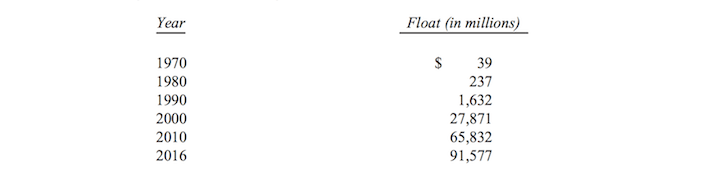

As of December 31, 2024, Berkshire Hathaway’s insurance float stood at approximately $171 billion, marking an increase of $2 billion from the end of 2023.

The Details, in Buffett’s Words

Here’s an even more in-depth explanation of insurance float from Warren Buffett’s 2016 Berkshire Hathaway Shareholder Letter:

“One reason we were attracted to the P/C [Proprty & Casualty] business was its financial characteristics: P/C insurers receive premiums upfront and pay claims later. In extreme cases, such as claims arising from exposure to asbestos, payments can stretch over many decades. This collect-now, pay-later model leaves P/C companies holding large sums – money we call “float” – that will eventually go to others. Meanwhile, insurers get to invest this float for their own benefit. Though individual policies and claims come and go, the amount of float an insurer holds usually remains fairly stable in relation to premium volume. Consequently, as our business grows, so does our float…

We may, in time, experience a decline in float. If so, the decline will be very gradual – at the outside, no more than 3% in any year. The nature of our insurance contracts is such that we can never be subject to immediate or near-term demands for sums that are of significance to our cash resources. This structure is by design and is a key component in the unequaled financial strength of our insurance companies. It will never be compromised.

If our premiums exceed the total of our expenses and eventual losses, our insurance operation registers an underwriting profit that adds to the investment income the float produces. When such a profit is earned, we enjoy the use of free money – and, better yet, get paid for holding it.

Unfortunately, the wish of all insurers to achieve this happy result creates intense competition, so vigorous indeed that it sometimes causes the P/C industry as a whole to operate at a significant underwriting loss. This loss, in effect, is what the industry pays to hold its float. Competitive dynamics almost guarantee that the insurance industry, despite the float income all its companies enjoy, will continue its dismal record of earning subnormal returns on tangible net worth as compared to other American businesses.

Nevertheless, I very much like our own prospects… Moreover, our P/C companies have an excellent underwriting record. Berkshire has now operated at an underwriting profit for 14 consecutive years, our pre-tax gain for the period having totaled $28 billion. That record is no accident: Disciplined risk evaluation is the daily focus of all of our insurance managers, who know that while float is valuable, its benefits can be drowned by poor underwriting results. All insurers give that message lip service. At Berkshire, it is a religion, Old Testament style.”

At the end of 2024, Berkshire Hathaway’s insurance float totaled $171 billion! And because Berkshire Hathaway’s insurance operations are run at an underwriting profit, the company’s insurance float is essentially like a $171 billion interest-free loan that Berkshire is actually being paid to take (though the company experienced a brief interruption in its underwriting profit streak in 2022, it has largely maintained its strong financial performance).

Now, compare this investing model to that of private equity firms or hedge funds, who also use leverage to invest… but instead of cost-free insurance float, these PE funds and hedge funds usually use high yield loans with interest rates of 7%+ per year.

Moreover, Berkshire Hathaway’s insurance contracts are structured in such a way that it will never have to pay back more than 3% in any one year – while a high yield loan might have to be paid back in full if a private equity company or hedge fund’s performance falls below a certain level.

Viewed in this light, the Berkshire Hathaway insurance float model is clearly genius.

It’s really no wonder that Warren Buffett is one of the richest people in the world.

The Ultimate Guide to Value Investing

Do you want to know how to invest like the value investing legend Warren Buffett? All you need is money to invest, a little patience—and this book. Learn more

Hey Dillon. After consuming a bunch of Buffett/Munger commentary recently, I had a burning question: I didn’t understand the difference between “insurance float” and “underwriting profit.” And that definition seems pivotal to understanding the Berkshire business model!

Very thankful that my Google search turned up your article near the top. Thanks to your writing, I get it now!

And as a fellow money/investing writer, I certainly appreciate the time, effort, and skill it takes to write an article like this.

Thank you for your work.

-Jesse

Awesome to hear my content helped you Jesse, thanks!