May 9th, 2021

Quick Stock Overview

Ticker: VRTX

Source: www.stockrover.com

Key Data

- Sector: Healthcare

- Sales ($M): 6,415

- Industry: Biotechnology

- Net Cash per share: $22.87

- Market Capitalization ($M): 55,658

- Equity per share: $34.69

- Employees: 3,400

- Debt / Equity: 0.1

- Interest coverage: 56.0

Summary

Biotech Stocks

Biotech and pharmaceutical companies are a very special type of investment category. They are difficult to analyze for multiple reasons:

- Extremely technical products, hard to fully understand even for specialists.

- Highly dependent on the future results of R&D

- Very volatile stocks, mostly driven by clinical trials news.

- Revenues are highly dependent on regulatory authorities, drug reimbursement prices, etc…

So, they are not really the typical company value investors are interested in, as it is difficult to give them a fair value. Assets are mostly immaterial (patents, goodwill, ongoing R&D), future returns are hard to predict. In addition, their high volatility makes Biotech stocks hardly the kind of steady stable compounders value investors look for.

But I would argue that such volatility is the friend of value investors. In the words of Ben Graham, “Mr. Market has a very unstable mood”.

This means that when he is depressed, he gives away valuable assets for a dime on the dollar. And very volatile, news-driven stock prices are a perfect opportunity for value investors to get wonderful companies at a discount. At least if they get cheap enough and can be valued properly.

Before we get into Vertex in detail, let’s just see how a pharmaceutical Biotech company operates.

First it needs to spend a massive amount of capital upfront in R&D in order to explore innovative medical treatments. The initial research can take years before an interesting idea or molecule can be identified. Ideally this should be for diseases with the following characteristics:

- Large amount of patients

- No or poor existing solutions

- Serious or deadly ailments

Once the drugs are developed and tested on animals and in-vitro, the tedious clinical trials phase starts. Phase 1 trials test the drugs on healthy people, just to check that it is not dangerous for humans. Phase 2 tests it on a few patients with the diseases to see its safety and eventual efficiency. Phase 3 tests it on even more patients, to have a more accurate image and statistics of the efficiency and side effects. Each of the clinical phases involves tons of paperwork, medical studies and massive spending.

Only if the results demonstrate clear improvement and good safety, does the FDA approve the drugs to be sold. Other regulatory agencies, like the European Medicines Agency (which is the EU version of the FDA) might require their own study or complementary data, increasing R&D costs even more. On average, only 10-20% of initial discoveries turn out to be commercially viable and approved by the FDA.

And even once approved, the profits from the new drugs are highly dependent on the price authorized by the regulators, and the level of reimbursement offered by public and private health insurance.

Source: www.acsh.org

So, Biotech companies seem to have very little control over their destiny. They are very dependent on the success of R&D, that are more often than not a failure. Firms depend on the whims of the regulators to approve the drugs, and often do not even control the price at which they can sell their product.

So, that begs the question: why would anybody invest in Biotech in the first place?

Simply because when a drug is a success, it is able to generate billions of dollars in revenue for a very long time.

This is very similar to the mining business, where finding good quality ore deposits is always a gamble, but once found, it is (sometimes literally) a gold mine for the investors.

But for the disciplined value investor, it is important to have some elements to judge the company, so we should limit ourselves to older, more established Biotech companies. This way we have stable cash flow, revenue streams, and other metrics that can be useful to judge it as an investment, instead of just speculating/gambling on the next drug that may (or may not) be a success.

I think the distinction is important, as most Biotech investors are gambling on the next clinical trial result, instead of investing in a company for the long run.

Strategic Analysis

Vertex Pharmaceuticals

As a value investor, I am not looking to gamble on the future results of R&D effort more than I am gambling on exploration stage mining companies. But a cash generating company, with good visibility on its future cash flow is another story. Especially if it is sold at a discount.

Vertex is a $55 billion company with a treatment for Cystic Fibrosis. Without getting into too much detail, here’s what you really need to know about Cystic Fibrosis.

Cystic Fibrosis inheritable genetic disease which affects multiple organs, and is causing a median age of death around 30 years old. It is a nasty disease, causing chronic lung infections, but also problems with the pancreas, the liver and bones. So even before their death, the quality of life of patients is dramatically affected by the disease.

You can learn more about it at the Cystic Fibrosis Foundation. 30,000 people are affected by it in the USA, and an estimated 70,000 in the world. This is really the type of disease which needs more research efforts to be done and better treatment reaching the market as soon as possible. Until recently, most treatments were only alleviating symptoms, and even if that allowed patients to live beyond teenage years, it is still far from enough.

The good news is that Vertex’s newest treatment, TRIKAFTA, is able to help 90% of Cystic Fibrosis patients. It is changing the deadly disease into a “manageable” one, not unlike what the invention of insulin did for diabetes.

You can imagine the impact it has for each of the families of the 30,000 patients in the USA alone. Being told your child is sick with Cystic Fibrosis is not a death sentence anymore, but an ailment that can be lived with, is obviously a much better solution.

Due to its tremendous impact, the drug has also been authorized with a strong pricing power, in order to help Vertex to keep innovating and helping more patients.

A Large Enough and Profitable Niche

A 30,000-person market in the USA, 70,000 in the world might not seem like a large market. But for TRIKAFTA alone, it was enough to generate almost $4 billion of revenues in 2020. I will not enter into a discussion about drug pricing rules and strategies, and its fairness, as this is a sensitive topic where everybody seems to have an opinion.

Generally, life-saving drugs for previously incurable diseases, and drugs, which take high risks and billions of dollars to develop, are generally rewarded by the FDA with pricing allowing for billions in profit, as incentive for pharmaceutical companies to keep improving treatments.

Many drugs today are either focused on treating symptoms due to unhealthy lifestyles (statins that reduce cholesterol), have been pushed too hard on patients who did not necessarily need them (opioids) or charge excessive prices for not-so-innovative drugs (insulins).

This can turn into a liability for investors, when the public backlash against these practices pushes regulatory agencies to punish them with lower prices or lawsuits.

This is not the case of Vertex, which is literally saving lives through its innovations. So I do not see any moral dilemma in investing in Vertex, something that might have kept some investors away from pharmaceutical and Biotech companies in general.

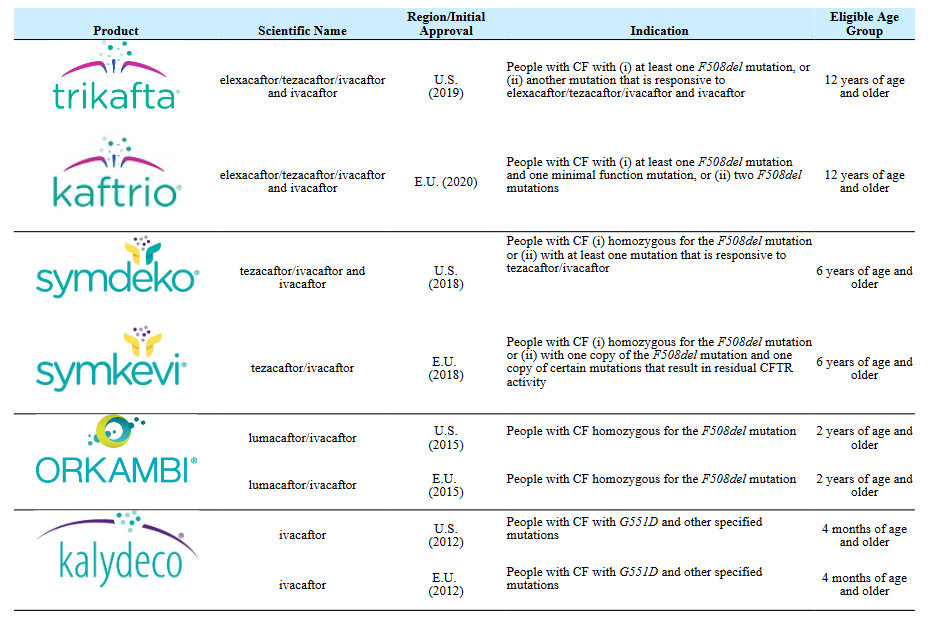

Vertex now has four different drugs for Cystic Fibrosis, with the latest being TRIKAFTA / KAFTRIO, which combines a new molecule (elexacaftor) with several of the drugs previously discovered by Vertex.

Source: www.vrtx.com

Source: www.vrtx.com

The company is also preparing the future by investing in R&D massively for whole arrays of diseases, while also working on actually curing Cystic Fibrosis. Most of these diseases are other rare genetic diseases without good treatment, and any success for even just one of them will mean deaths avoided and quality of life dramatically improved for tens of thousands of people.

Source: www.vrtx.com

Disease Patient number worldwide Disease Patient number worldwide Sickle Cell Disease 4,400,000 Type-1 Diabetes 1,106,000 Beta Thalassemia 70,000 Duchenne Muscular Dystrophy 500,000

We will dig deeper in their research pipeline in this report, but I think that just the existing portfolio of treatment, and especially TRIKAFTA, is already highly valuable. The company has low debt, positive earnings and cash flow and should stay that way for at least one or even two decades in the future.

This report first appeared on Stock Spotlight, our investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 rational investors!

Qualitative Analysis

Business Analysis

As the main innovator in Cystic Fibrosis treatment, Vertex has both a first mover advantage, and a monopoly on the market. Doctors tend to stick to the treatment they know best, and welcome innovation with somewhat skeptical eyes, especially for very serious conditions in children, like Cystic Fibrosis.

This means that for any new drugs to take a significant part of their profits away, it would not only need to be sage, but also to be significantly better.

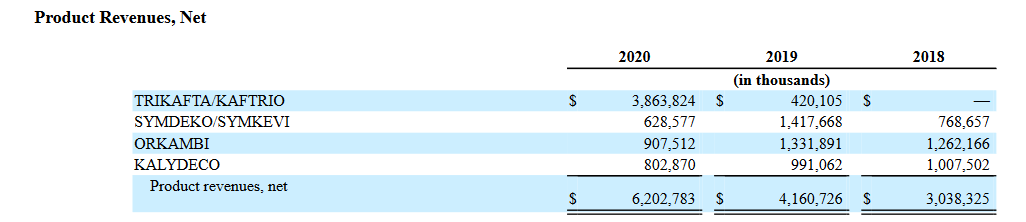

Source: www.vrtx.com

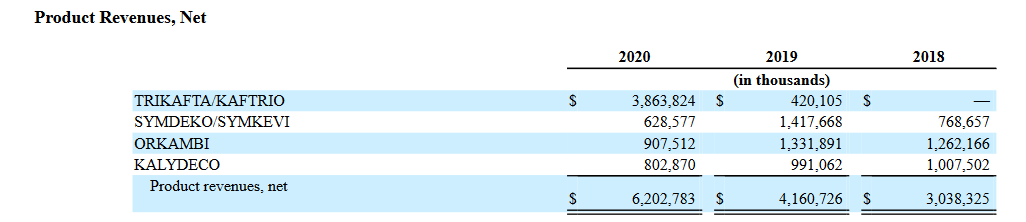

You can see in the revenue breakdown above that the arrival of TRIKAFTA to the market has partially cannibalized the other Vertex drugs revenue streams, but also doubled the overall turnover in just two years.

As TRIKAFTA needs to be taken continuously, it should produce very steady income for the years to come. So beyond a great balance sheet and good future prospects, Vertex has a solid baseline revenue that we can use for a minimum valuation.

At the moment, Vertex drugs treat around half of the patients affected by Cystic Fibrosis, so the baseline revenue is susceptible to grow at least a little more over the next years. The drugs are mostly sold in the EU and US market, and also the UK, Switzerland, Israel and Canada.

Further extension to other countries like Japan or Korea, or mid-income countries like China, India and Russia might help to grow TRIKAFTA numbers a little more.

Economic Moats

In value investing terms, Vertex has two powerful economic moats:

Intangible Assets / Intellectual property (IP)

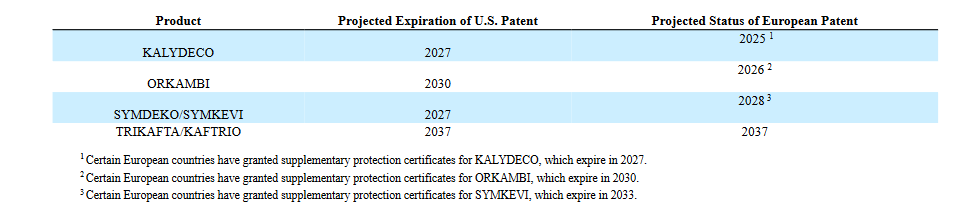

Patents and clinical trial data are the core of any Biotech company. Vertex is no exception. Here, I will need to explain a little how patents work for pharmaceutical drugs.

Patents normally expire 20 years after the first listing. But drugs are a special case, as from the discovery of a molecule to its commercialization, it often takes 5-15 years to do all the clinical trials for reaching FDA approval and commercialization.

So a very complex set of additional rules exists to help pharmaceutical companies to have patents lasting a little longer. For example, if a drug still uses the same molecule, but is released a bit slower in the body, or is tweaked to have a bit less secondary effects, it can be granted patent extensions. The usefulness of the drug for the patient is also a big criterion justifying an extension.

When the patent expires, other pharmaceutical companies can produce generic versions of it, and compete with the original one. This does not mean that all revenues dry out, but it usually means that 60-90% of the profit from the patent is lost, depending how many generics enter the market and if doctors agree to test the new options.

You can see here the duration of each of the patents for the existing drugs of Vertex, both in the US and EU. The older drugs that have been cannibalized by the approval of TRIKAFTA have 5-9 years left, and TRIKAFTA has around 16 years left.

This is a lot compared to the usual case in pharmaceuticals, and reflects that TRIKAFTA got approved as an orphan drug, meaning the approval process was sped up to reach quicker children in dire need of better treatment.

Source: www.vrtx.com

Substitution Cost

When it comes to deadly diseases in children, doctors have good reasons to be skeptical of experimenting. Trying to modify an existing treatment and getting it wrong might quickly become a matter of life or death. TRIKAFTA is now the only drug on the market able to drastically improve the condition of Cystic Fibrosis patients.

Once a patient started the treatment and is getting better (or even if his condition just stops deteriorating), doctors will be extremely reluctant to try out new options, knowing that if the patient responds poorly to the experiment, it might be a death sentence.

This means that Vertex products have a strong moat in the form of very high resistance to substitution. Only a drug proven to be radically more efficient will be able to displace TRIFKATA from the market. In addition, the commitment of Vertex to the disease means it is building a very solid relation with virtually all the doctors specialized in Cystic Fibrosis.

This gives Vertex future goodwill and good coverage in scientific analysis, medical congress presentations, etc…, all very powerful vectors of pharmaceutical marketing.

Management

The quality of management of a Biotech company is maybe even more important than for other sectors of activity. You see, the very complex regulatory system in which Vertex operates, as well as the nature of its products, mean that mistakes are simply not an option. Nor is any hint of corruption or wrongdoing. The company needs to have honest, knowledgeable and well connected managers to simply be authorized to operate. Unsurprisingly, Vertex’s management is mostly composed of doctors and PhDs.

Source: www.vrtx.com

For more than a few of the board members, the quality of their background is worth noticing:

Dr. Reshma Kewalramani, CEO

Former Vice President of Global Clinical Development at Amgen (one of the greatest success stories in Biotech). She was also the industry representative to the FDA’s Endocrine and Metabolic Drug Advisory Committee.

Dr. Jeffrey Leiden, Executive Chairman

Former President and CEO of Abbott Laboratories (one of the top 10 big pharmaceutical companies).

Dr. David Altshuler, Chief Science Officer

Dr. Altshuler was one of four founding members of the Broad Institute, a research collaboration of Harvard University and the Massachusetts Institute of Technology, The Whitehead Institute and the Harvard Hospitals.

Dr. Carmen Bozic, Chief Medical Officer

Former Biogen (another one of the largest Biotech success stories) Senior Vice President of Global Development and Portfolio Transformation from 2015 to May 2019 and Senior Vice President of Clinical and Safety Sciences from 2013 to 2015.

Dr. Bastiano Sanna

Former President of Semma Therapeutics, Inc., a private Biotechnology company which Vertex acquired in October 2019. He was at the Novartis Cell and Gene Therapy Unit as the Global Program Head of Stem Cell Transplant.

Vertex Management is a gathering of very successful professionals from all around the pharmaceutical industry. This speaks very well of Vertex successes to manage to get on board people that could have taken any comfy position among the top 10 big pharma giants.

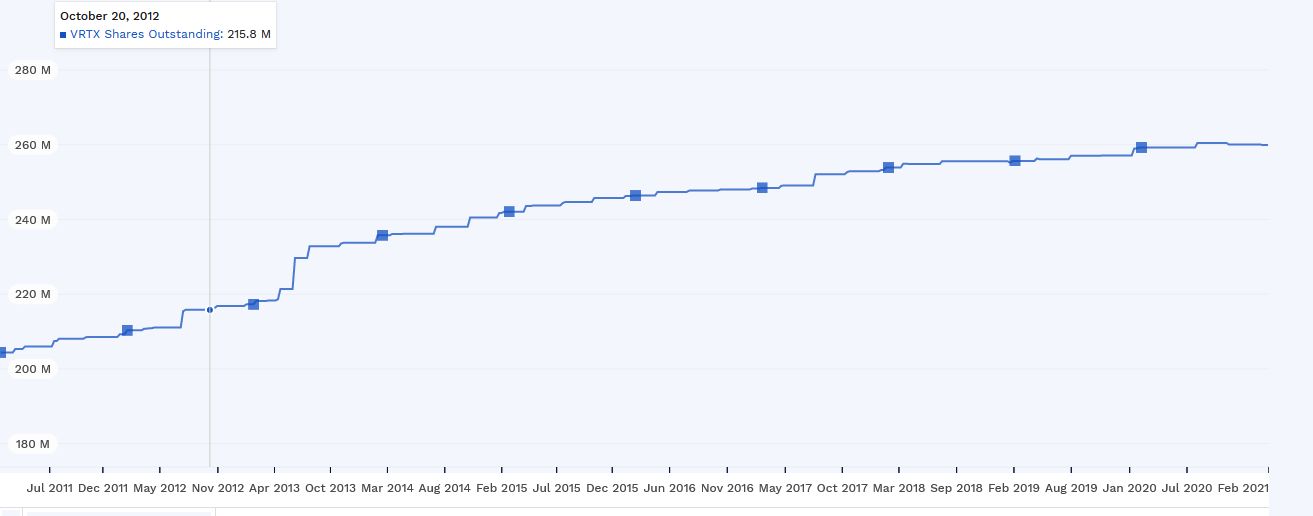

Unfortunately, this level of management quality comes at a cost, and I believe their stock compensation is rather high, even for the Biotech/pharma sector.

No less than 15% of Vertex net income is spent on stock-based compensation to management and employees. While this does ensure a better alignment of management and employees with shareholders’ interests but might be a little excessive for my taste.

This is reflected in the rather steadily increasing number of shares outstanding. Nothing alarming, but to be remembered as a potential shareholder.

Source: www.finbox.com

Competition

For competition, I will only look at the Cystic Fibrosis drugs, as all the other diseases are for now just candidate drugs in the research pipeline.

AbbVie

The main danger to TRIKAFTA revenue stream seems to come from AbbVie, a $190 billion pharmaceutical giant. They have an alternative drug in Phase 2.

It is very hard, and often a fool’s errand to try to guess the future success of clinical trials, so I do not know if this AbbVie drug will be approved or not. For me the worst-case scenario here would be for AbbVie’s drug to not only get approved, but have better results or risk profile than TRIKAFTA.

I am not seeing that as extremely likely, as their approach seems very similar to the one Vertex used to develop TRIKAFTA. But if the phase 2 of AbbVie gives much better results than TRIKAFTA, this would be a reason to re-evaluate Vertex future prospects.

mRNA therapies

The other competitive risk comes from novel approaches using mRNA therapies. Going in detail about how it works is beyond the scope of this report, but you can learn more about it here. Vertex mentions a whole list of potential competitors in its annual report:

- Translate Bio

- Arcturus Therapeutics Holdings,

- Krystal Biotech

- Spriovant Sciences

- 4D Molecular Therapeutics

- Eloxx Pharmaceuticals

So far, mRNA therapies have failed to deliver significant results, and none have been approved despite more than a decade of research in the field. But if mRNA therapies become better understood and start getting approved, this could mean a whole new batch of competitors to Vertex might appear in the next 5-10 years.

It is also worth noting that Vertex is itself very active in the field, both directly and through collaboration with Moderna, one of the leaders of mRNA therapies, as you will see below. So I am sure some competition might come in that field, but I do not see Vertex being outclassed or disrupted by it any time soon.

Research Pipeline

As you will see, my valuation method for Vertex is not going to be overly reliant on R&D future eventual successes. But the company is investing massively to enter new markets and cure or alleviate diseases resistant to treatment up to now.

So while R&D should not be the only reason to buy Vertex stock, most of the potential long-term upsides of the company will come from successful new drugs. Some of the research efforts are done conjointly with other companies, to combine their respective technical expertise and proprietary data.

Almost all of the drugs mentioned below are in phase 2 of clinical trials, so they have been proven safe for healthy humans, but their therapeutic potential is still to be proven. If you have a good understanding of medicine or biochemistry, you can learn more about the details of each R&D strategy on the Vertex Pipeline page.

Cystic Fibrosis

Vertex is at the phase 2 of testing the drug VX-561, which could potentially treat the underlying cause of Cystic Fibrosis, instead of just alleviating the symptoms.

I am not sure if this will work, but if one company has a deep understanding of the disease and is able to cure it, it is probably Vertex.

Moderna / RNA therapies

You might know Moderna as the company producing mRNA COVID-19 vaccines. Vertex is working with them to co-develop Cystic Fibrosis treatment using Moderna mRNA technology. This is very good news, as this means Vertex has been able to secure outside expertise on mRNA therapy to not let itself be distanced by other Biotech startups.

What will come out of it, is hard to tell. But at least, Moderna is for now one of only two companies in the world to have an approved mRNA treatment (together with the other mRNA COVID-19 vaccine maker, BioNTech)

Another collaboration is with Skyhawk Therapeutics, where RNA splicing research could lead to breakthroughs for various genetic diseases.

Gene Therapies

Vertex has entered into a series of collaborations to co-develop gene therapies.

- Affinia Therapeutics for Duchenne Muscular Dystrophy, Myotonic Dystrophy Type 1 and Cystic Fibrosis

- CRISPR Therapeutics AG for treatment of Beta Thalassemia, but also getting from them exclusive license treatment for Cystic Fibrosis, Duchenne Muscular Dystrophy, Myotonic Dystrophy Type 1

- Duchenne Muscular Dystrophy and Myotonic Dystrophy Type 1 research is also helped by the acquisition in 2019 of Exonics, for $245 million.

Type 1 Diabetes

One way for pharmaceutical companies to acquire new potential products is to buy smaller Biotech startups. Through the acquisition of Semma Therapeutics in 2019, for no less than $950 million in cash, Vertex is working on a medical device that would replace the part of the pancreas which fails in Type 1 diabetes patients.

It would contain the cells that are destroyed in people suffering from the disease, and the device would shield these cells from the immune system, so they stay healthy and functional. This would simply cure Type 1 Diabetes permanently.

I am not qualified to judge how likely this research effort is to succeed, but this one project alone could make Vertex revenues stream from Cystic Fibrosis like a drop in the ocean compared to getting 1 million of diabetes patients off insulin permanently.

Other diseases

Vertex is also pursuing research efforts to alleviate the following conditions:

- Pain

- Sickles Cell Disease

- Beta Thalassemia

- Alpha-1 Antitrypsin Deficiency

- APOL1-Mediated Kidney diseases

Except for chronic pain, all are niche markets of untreated or poorly treated genetic diseases.

I expect that Vertex will be able to apply the knowledge acquired in Cystic Fibrosis to some of these diseases too, creating whole new profitable markets.

Theoretical advancement

Vertex is also working on “pure” scientific progress, in collaboration with Arbor Biotechnologies and Kymera Therapeutics. This might lead to new concepts for gene therapy and genetic diseases treatment down the road. I really appreciate that Vertex is looking forward to the future that much, as this has a lot of upside potential, for a rather limited cost.

Out-licensed research

Three potential drugs (VX-970, VX-803 and VX-984) have been licensed out to Merck, all of them potential oncology (cancer) drugs.

This is in my opinion a good choice from Vertex management. Their research teams found something potentially interesting for cancer, but as this is not the focus of the company, they have licensed the data to a company that will be more able to develop and market it than Vertex could have done alone.

This allows for some potential future revenue stream without risking Vertex to lose its focus on orphan-drugs and rare genetic diseases.

Quantitative Analysis

Financials

Revenues

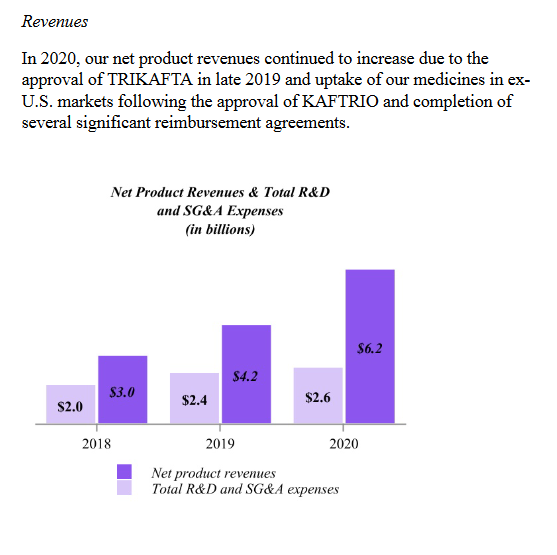

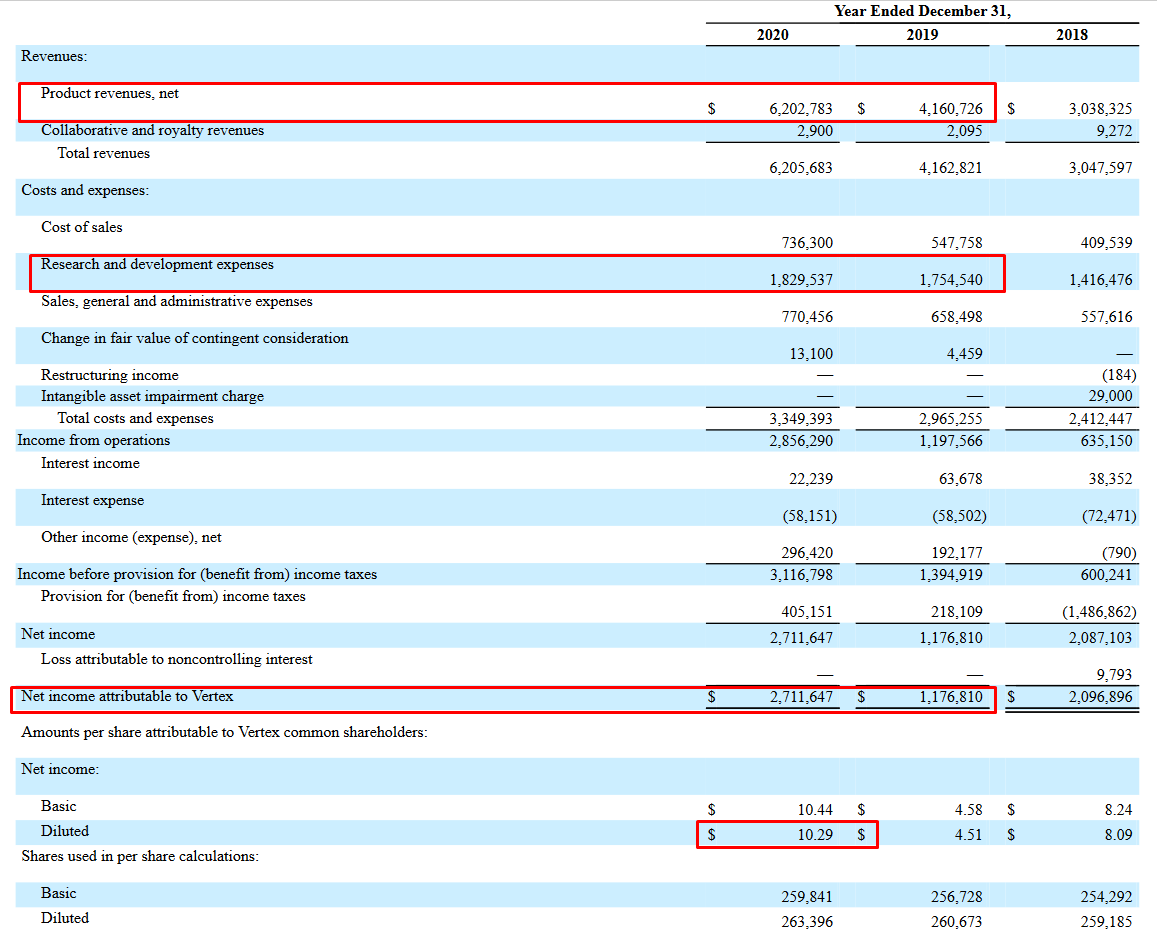

Vertex’s revenues are simple to understand. They produce and sell four different drugs which are saving the lives of Cystic Fibrosis patients. The costs are mostly covered by social security, and public and private healthcare insurance. With the approval of TRIKAFTA, revenues have exploded for almost the same costs, reflecting how production volume and sales costs are marginal in this business compared to R&D, regulatory and clinical trial costs.

Source: www.vrtx.com

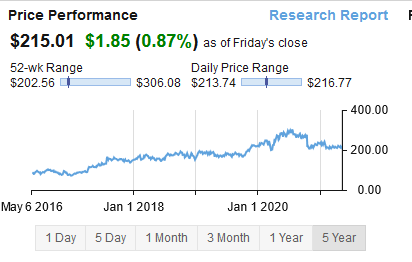

During 2019 and early 2020, the stock price was reflecting the increasing income and revenue, but the recent stock price fluctuations are giving us a window of opportunity to get Vertex at a discount.

Source: www.finbox.com

Biotech companies need to constantly invest more in R&D to simply stay competitive and renew expiring patents. So, it is not proper to do, like it sometimes happens, to register R&D spending as an investment. This artificially inflates earnings and assets and can make the balance sheet appear better than it is in reality.

Luckily, Vertex is following good accounting practices and properly considers R&D expenses as spending.

As you can see below, R&D represents actually more than half of the total of Vertex’s expenses.

Source: www.vrtx.com

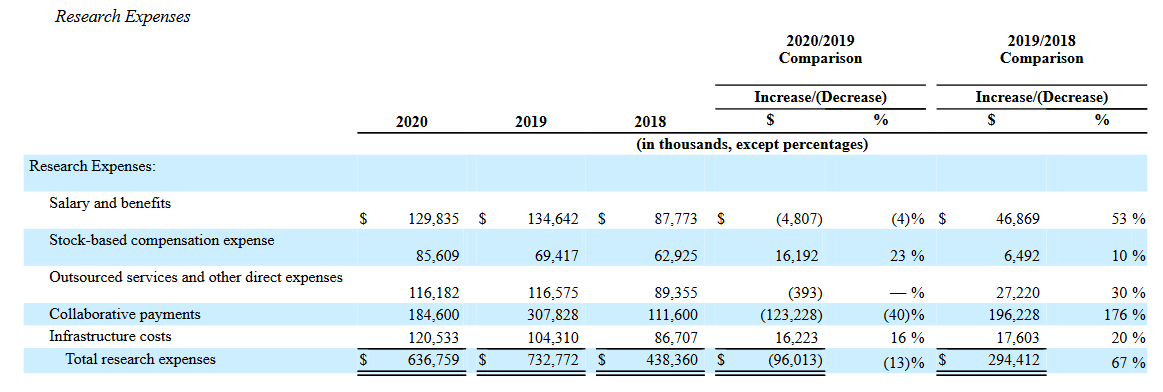

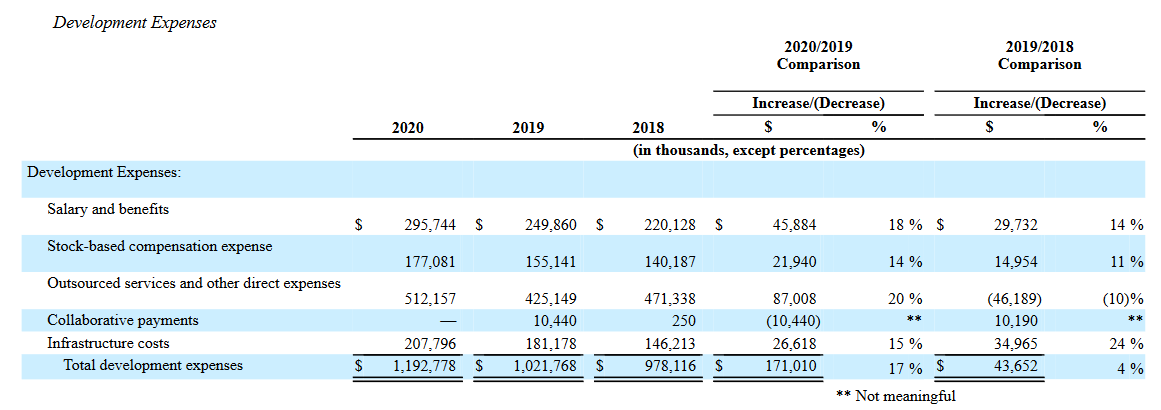

Speaking of expenses, I appreciate that the company displays a breakdown of their spending in both research and development, as you can see below. The main costs are obviously salary and compensation, closely followed by outsourced services and collaborative payment.

On one hand this means that Vertex is not fully in control of all the technologies and science behind its new drugs. On the other hand, it means it is able to gather the best ideas and data to speed up and improve its R&D process. The success this approach had in making Cystic Fibrosis a more survivable disease seems to indicate that this is the right approach.

For sure, it provides Vertex the flexibility to try new ideas and treatment methods, instead of trying to solve everything with only its own proprietary solutions. For a field as complicated as genetic diseases, it is better to have a wide array of tools instead of trying to apply one solution to every problem.

Source: www.vrtx.com

Dividends

If you are looking for dividends, Vertex is simply not for you. The company is not distributing any dividends and has no intention to do it anytime soon. This makes sense as the company is pursuing growth aggressively in many new diseases and needs to defend its position in Cystic Fibrosis.

It might also need cash to keep doing acquisitions to get its hands on more talents and new technologies. So overall I prefer this, as the company will only be a great investment if it succeeds in developing new treatments.

Debt and Balance Sheet

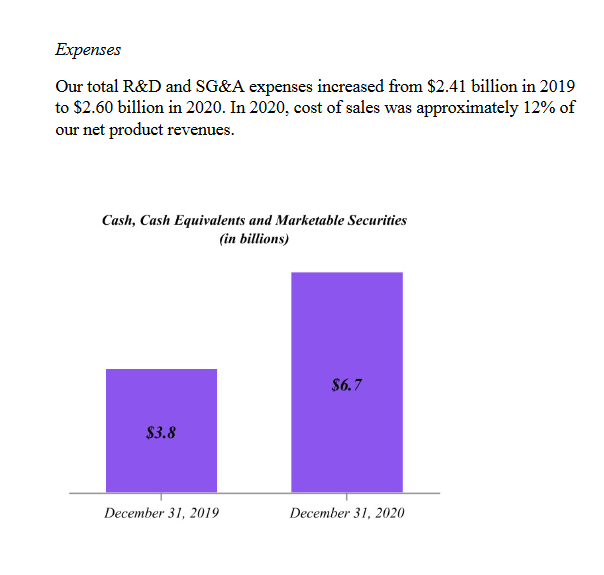

Vertex has a very solid balance sheet, with very little debt, and plenty of cash on hand, with up to $6.1 billion in cash and $5.6 billion in net debt. This is great as this covers the equivalent of four years worth of R&D or allows the company to look for acquisitions without having to worry about its debt load, debt agreement or interest rates.

Source: www.vrtx.com

Source: www.finbox.com

This cash abundance is a relatively recent thing, with almost $3 billion accumulated between 2019 and 2020. This is mostly due to the very large success of the TRIKAFTA launch.

I expect Vertex to soon redeploy this cash in either new research targets, provision it for extra spending for incoming phase 3 clinical trials (The most expensive phase), or acquire targets with valuable drugs or molecular biology technologies.

Source: www.vrtx.com

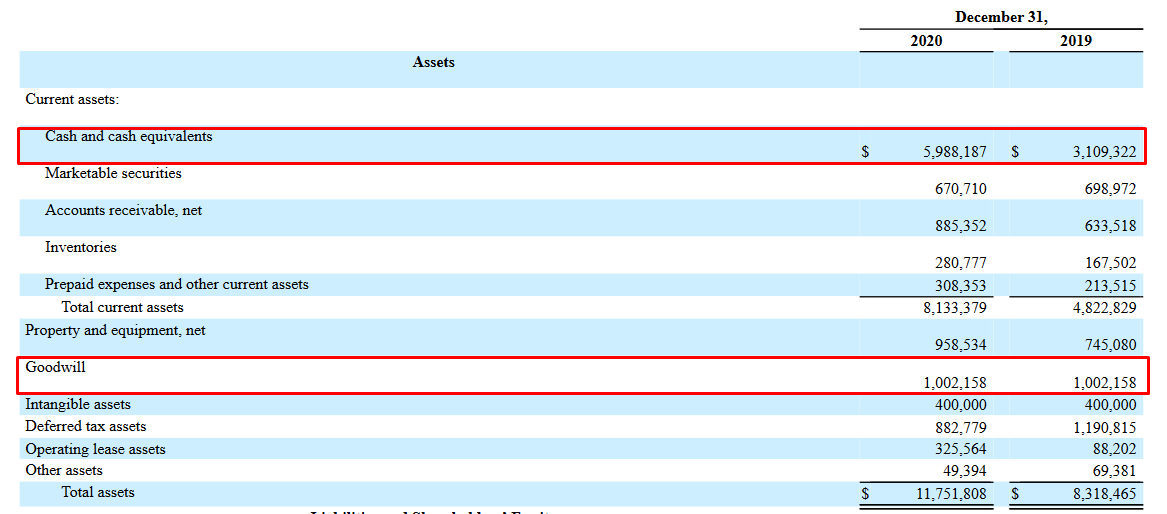

One final note regarding the balance sheet. Despite numerous acquisitions for more than $1 billion in 2019 alone, Vertex does not have a lot of goodwill in its assets, and most of it is from before 2019. This probably shows a good capital discipline regarding acquisitions, which are done more because of valuable scientific advancements and key personals than to grow the company at any cost.

From this acquisition came the potential treatment for type-1 diabetes. So as far as I can tell, acquisitions have been a good thing for Vertex for now.

Source: www.vrtx.com

Cash Flow

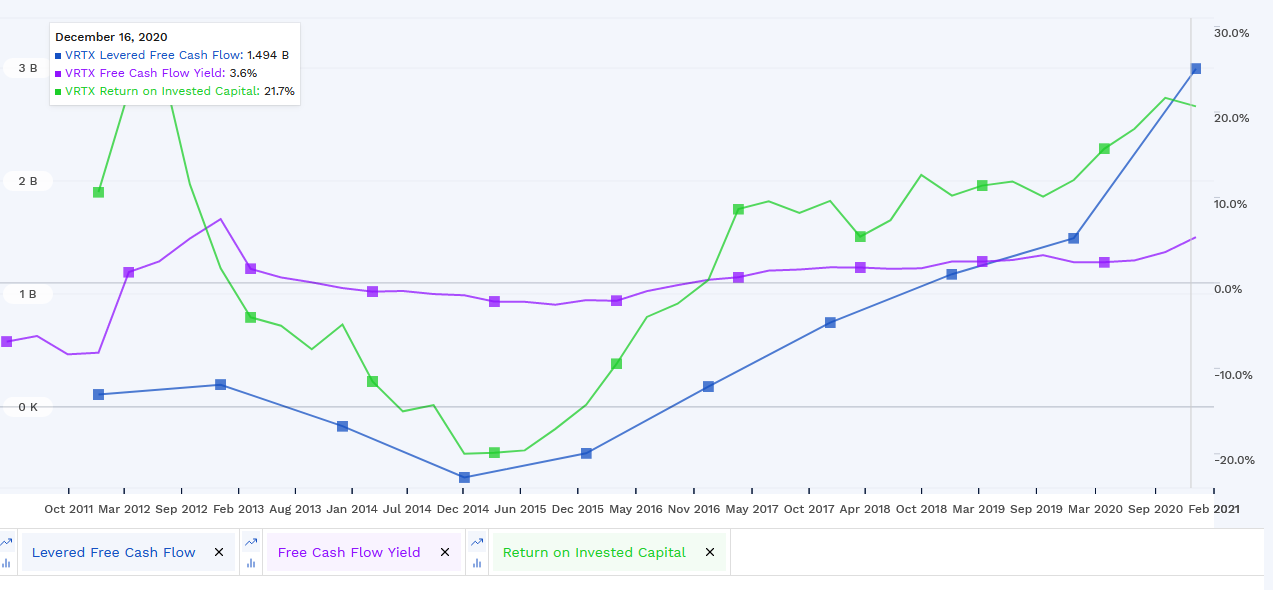

Unsurprisingly, Vertex cash flow has not always been stellar. Before the FDA approval of its flagship drugs, Vertex was cash flow negative, investing its capital in R&D, and not yet receiving much results for it. Since 2016, Vertex financial results have steadily improved.

With the drug patents expiring years in the future, we can expect these numbers to stay stable or even keep growing for the next 5-10 years or maybe even 15 years.

Source: www.finbox.com

This steady positive cash flow has allowed the company to grow its cash from $1.6 billion in 2018 to $5.9 billion by the end of 2020.

Source:www.vrtx.com

Categorization and Valuation

Investment Category

Vertex is currently one of those unique businesses that currently fits the Combo category, as it is a mix between Quality company and a Value play. Depending on the investor’s thesis, valuation, and strategy, Vertex can be used multiple ways in a portfolio.

Without the research pipeline, it would only be a Value play, as the price is somewhat low. But with the large potential upside from the various possible future treatments, I think that even a conservative priced put on the research pipeline means the company is undervalued at the moment.

The company has predictable earnings for the next 5 years, due to the absence of immediate competition in its Cystic Fibrosis market. I assume this should still be somewhat true in the 5 years after, but with possibly mounting competition before the expiration of TRIKAFTA patents.

The recent drawback on price might be related to concerns about levels of healthcare reimbursement and price re-negotiation under the Biden administration. Even if those concerns might make sense for let’s say, insulin makers, for a truly innovative drug like TRIKAFTA, this is unlikely that much pressure will be exerted on Vertex.

This is made even more true as Vertex is very publicly investing into helping to cure other orphan genetic diseases, and price renegotiation would hurt its ability to invest in more R&D.

The Mining Company Model

Every company can be valued in multiple ways. I was curious to look at what Vertex’s fair value would be in the odd case that all of their R&D efforts would not produce anything of value for the next 10 years in a row. Maybe an overly pessimistic scenario, but this gives us a baseline. So, how much would the company be worth if it would only make money from its existing patents?

In a way, this is similar to the method of evaluating a mining company. You know the minerals deposit and mining permits have a limited lifespan, after which they will be depleted. So you can similarly calculate how much can be “mined” from the existing patents. In that analogy, the mining exploration budget is equivalent to the R&D expenses. Biotech, like mining companies, are always in need to find new discoveries to keep it running.

So I took each of the drugs, and multiplied their 2020 revenues by the leftover useful patent life to get the total revenue for the lifetime of the patent. I then applied the margin between revenue and income to judge how much earnings the company should generate for the lifetime of the patents. So this assumes a constant level of spending and stable revenues from the patents.

To this the net debt amount of negative -$5.6 billion should also be added. This would bring the company value from its existing patents to around $40 billion. This is not exactly the current market cap of $55 billion, but not very far either. This implies that you get the entire research pipeline not for free, but still very cheap.

Of course, such linear projections are a rough approximation. New competitors can enter the market, TRIKAFTA is likely to keep cannibalizing the other three drugs revenues, new Cystic Fibrosis drugs by Vertex itself is likely to cannibalize TRIKAFTA at some point in the future, etc…

I also did not incorporate into these calculations any growth in the Cystic Fibrosis market, despite 50% of patients still not using Vertex drugs and the company expecting revenue to grow in 2021. So there is a good chance that the existing patents and available cash might justify entirely the current market capitalization.

On a side note, it is common for pharmaceutical companies to manage to extend the lifetime of a patent by a few years by improving its formulations slightly. If each patent gets a little bit longer life time (1-2 years), this would add another $4 billion.

I finally want to remind you that what I calculated here is income/earnings, and not revenues. This means that this is the amount of profit the company should generate from its existing properties while doing large investments in R&D and/or acquisition. It also ignores residual earnings after the patents expire.

So it is very unlikely that by the time TRIKAFTA’s patent expires, the company will be left with absolutely zero residual value. But I preferred to give you a rather conservative estimate just in case. Again, this gives us a baseline for valuing the company, ignoring all the research pipeline.

Discounted Cash Flow

One other way to calculate Vertex’s valuation is using the discounted cash flow model. You can see what it means and how it works here. But this method has a problem, which is that future cash flow of Vertex is highly dependent on the result of its R&D and clinical trials, which are essentially impossible to forecast with good accuracy.

So previous growth of free cash flow is a poor indicator to what may come. What I did was calculate 2 possible futures.

Future number 1: Vertex’s R&D if its exploration in new diseases are mostly a failure, so its free cash flow growth is mostly contained to the next 5 years, when more Cystic Fibrosis patients start TRIKAFTA therapy.

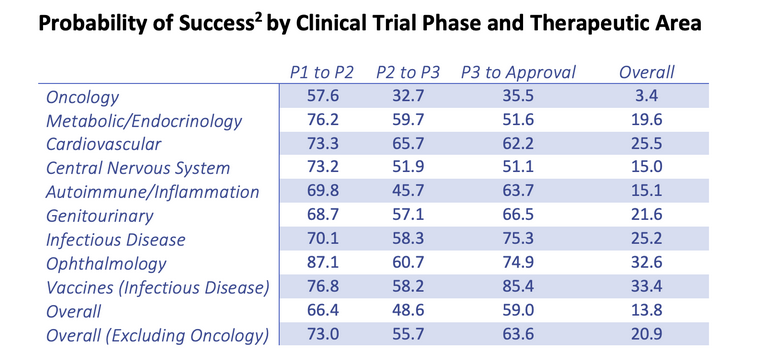

Future number 2: The R&D produces reasonably good results in at least 20% of the research project, which would be in line with the average success rate for drug development out of oncology. As a reminder, this was the success rate of clinical trials per type of drugs.

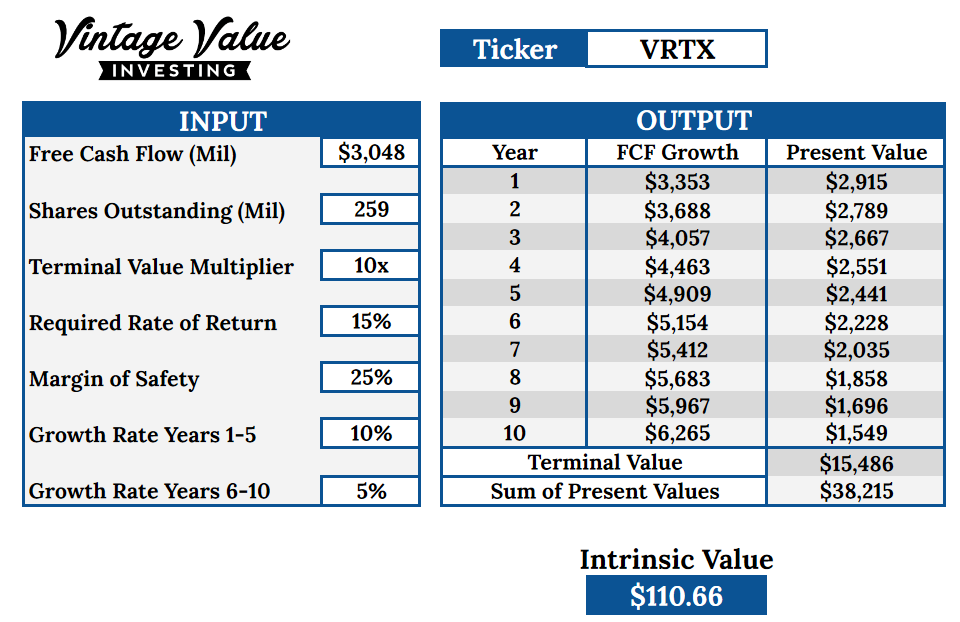

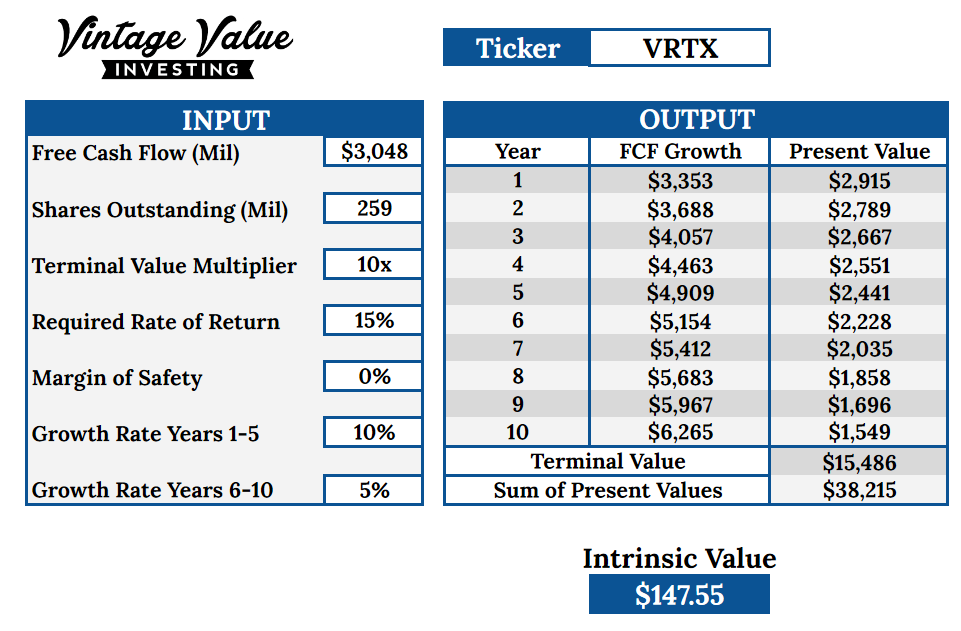

Future number 1 gives us a buying price of $110 dollars or less. I assume a low terminal value multiplier, as the market is likely to have lost all enthusiasm about Vertex if its R&D efforts failed constantly.

It assumes that the first 5 years, growth is coming from the cystic fibrosis market, and then growth strongly slows down, thanks to zero new markets getting opened by R&D. It also takes an exceptionally large margin of safety of 25% to reflect the uncertainties about the future, when it depends on clinical trials far down the road.

The intrinsic value of the company, without the margin of safety, would be $147.

So, way below the stock price of $215, but actually not that terrible considering it is an extremely pessimistic scenario. Having absolutely none of the R&D effort producing anything, even in cystic fibrosis, is not very likely, but always a low probability risk to remember. In that case, I think the results from the “mining” model are a better representation of Vertex value.

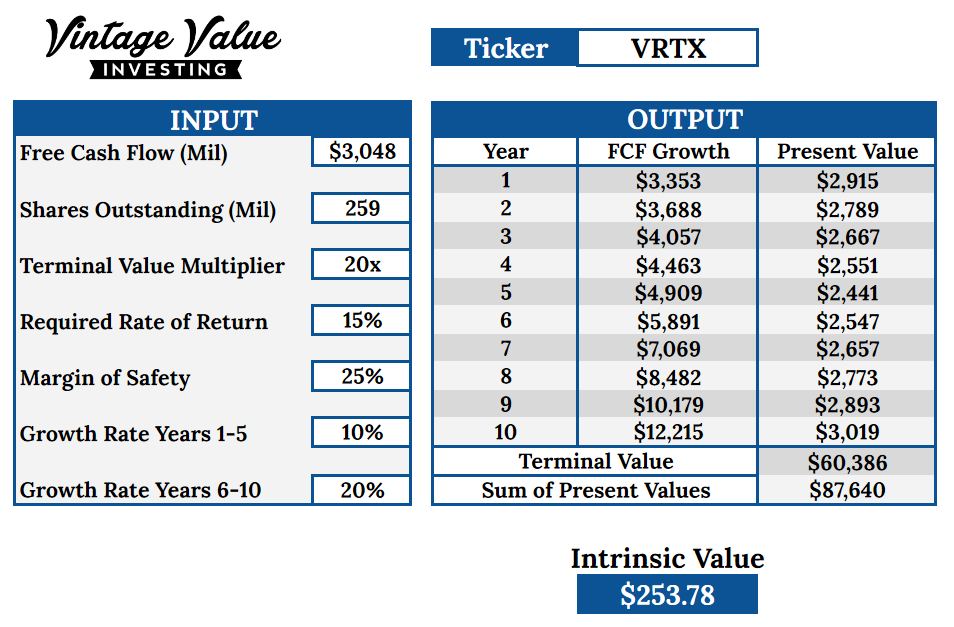

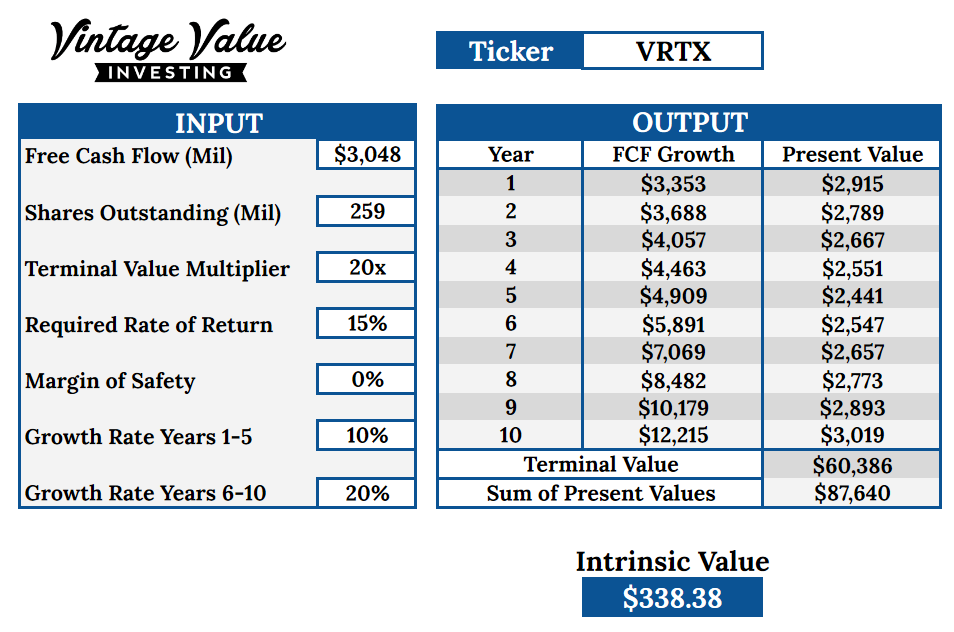

Future number 2 gives us a buying price of $253 dollars or less, far above the current stock price. It assumes that the first 5 years, growth is coming from the cystic fibrosis market, and then growth accelerates, thanks to new markets getting opened by R&D successes. It also takes an exceptionally large margin of safety of 25% to reflect the incertitude about how probable such a future is likely to be.

Without margin of safety, the real value of the company would be at $338, making the current market capitalization extremely undervalued.

I gave a rather high terminal value multiplier for this hypothesis, as markets would certainly rewarded an accelerating growth with a strong multiplier. Interestingly enough, this means that Vertex was properly priced by the market until the US election, and might have just been affected by a general pessimism regarding the healthcare and pharmaceutical sector.

Other Models

Other models are unlikely to be usable in valuing Vertex. Earnings are likely to be rather unstable and P/E even more, making the model not so useful in this case.

While the equity bond model can be used, the fact that P/E will likely be very unstable and earning growing (or not growing) quite far in the future in hard to estimate amounts, makes it not very sensitive for valuing Vertex.

Finally, the complete absence of dividends makes the yield on the cost model useless.

Final Assessment

Company Synthesis

Vertex is a solid player in the Biotech industry, with a remarkably profitable and safe niche in a sector often threatened by impending disruption. Just its existing patents alone, together with its stellar balance sheet, might justify the existing market capitalization.

But with almost $2 billion in R&D spent every year, and a management team full of biotech top leaders, I actually do not believe that Vertex will simply stagnate and die with its existing patents and approved drugs. I actually expect it to become a steady compounder and major player in the pharmaceutical industry.

Short Term Projection: 1-5 Years

As the closest competitor is only doing the phase 2 of its clinical trials, I think Vertex has a very safe and stable outlook for this period. Increased enrollment of patients is likely to allow for steady growth of revenue, income and cash flow.

Long Term Projection: 5-10 Years

The pressure on TRIFKATA might increase slightly from AbbVie’s new drug, but by then, Vertex will be established as the dominant player in the Cystic Fibrosis market, and AbbVie sales reps will likely struggle to compete with the well establish network of relations that Vertex will have solidified with doctors, patient associations and experts of the disease.

By then, the picture regarding the research pipeline should be more clear, and it will become evident if Vertex is on the verge of further breakthroughs. It could be new and better Cystic Fibrosis treatments. Or maybe replicating the success of Cystic Fibrosis for 1-3 other orphan diseases.

But what could be really a game changer is if Vertex managed to get its treatment for pain or Type 1 diabetes approved by the FDA. These are huge markets with largely unaddressed needs. The diabetes treatment could become a blockbuster treatment. Blockbusters are drugs like Statins or Viagra or Insulin, that can generate tens of billions of profits in the lifetime of their patents.

Very Long-Term Projection: 10-20 Years

During that time, all existing patents of Vertex will expire, and the future of the company will be entirely dependent on its past R&D achievement. In any case, its deep knowledge about gene therapy, mRNA therapy and orphan diseases, as well as its sales network of associated doctors and hospitals should be valuable in a form or another.

So, it would ensure some form of legacy income in the odd case that none of the research efforts have accomplished anything.

Valuation

So, Vertex is a rather safe play as pharmaceutical companies go. It is anyway a long-term play, a stock to buy and re-evaluate every 1 or 2 years and probably hold for a decade or two as long as its main market stay, Cystic Fibrosis, stays viable.

The worst-case scenario is a total failure of its R&D, with the existing patents barely justifying today’s market capitalization.

The likely scenario is some results from the next 10 years of R&D, making Vertex significantly undervalued at the moment. Depending on how successful the R&D will have been, annualized returns from 10-20% should be expected.

The best-case scenario is the launch of a blockbuster drug or treatment making Vertex one of the top 10 pharmaceutical companies. Maybe not extremely likely, but a nice potential upside to the likely scenario.

Which scenario will prevail is up to anyone to guess. There are simply too many variables to be absolutely sure of Vertex’s future. So, the list of things to follow for a Vertex investor will be:

- R&D progresses, especially clinical trials in phase 2 and 3 results for new diseases, but also for better cystic fibrosis treatment, or ideally complete cure.

- Entry of competitors in cystic fibrosis in 5-7 years, especially AbbVie.

- Growth of the cystic fibrosis market and cash flow.

- FDA approval and attitude toward Vertex products.

- Extension of existing patent durations.

- Use of the cash flow and acquisitions.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in VRTX and no plans to initiate any positions within the 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed in this article.