Lazy Value Investing

When I mention that I am a value investor to my colleagues, they usually form an impression that is actually at odds with my investing style. Now, this is partially not their fault, as most financial institutions have defined value investing as such:

Value investors are those who focus on companies with lower-than-average sales and earnings growth rates. Holdings generally feature stocks with lower price-to-earnings and price-to-book ratios. Stocks generally have higher dividend yields. A fund can potentially capitalize on turnaround situations.

This narrow definition of value investing (or any definition of investing) has always irked me. This is what I have dubbed “lazy value investing”.

Putting Yourself in a Box

While I understand the reasoning behind categorizing and generalizing investment styles, it really is unfortunate that this definition curdles around the value investing community, especially since the majority of us probably don’t adhere to this strict construct.

But I digress. If you want to know my true definition of value investing, then check out my article here where I go over these misconceptions in great detail.

So why do I bring up this topic? Well, while doing some research recently, I came across a company that seemed to be offering me a great deal. I had discovered a very profitable business with solid margins, zero debt, and best of all, Its P/E (Price to Earnings) ratio was only 4.4! What a steal, right?

Well, not quite. A P/E of 4 for a business of this quality stood out to me like a fish out of water. Here are a few possibilities of why this could be:

- The market has simply mispriced this company, and it is seriously undervalued

- The market has recently reacted negatively (justified or not) to this stock, which could indicate a problem with the company

- The company financial reporting is incorrect or manipulated, indicating false earnings

- The company’s earnings have dramatically increased, and the stock price has not caught up with that increase (or vice versa)

So then, which is it? Let’s do some digging to find out.

Bio-Rad Company Overview

The company in question is Bio-Rad (BIO). Bio-Rad is a $16B healthcare company that produces medical devices for various conditions. Bio-Rad is headquartered in California, but is globally diversified, with 56% of revenues coming from international locations.

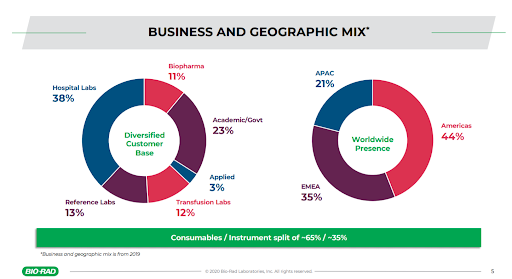

Bio-Rad also has a diverse customer base, with laboratories comprising over 60% of revenues, with other academic, governmental, and biopharma organizations earning the rest of the share.

Source: Bio-Rad Business 2021-2023 Outlook Presentation

Bio-Rad also owns a large stake (37%) in Sartorius AG, a laboratory and biopharmaceutical supplier.

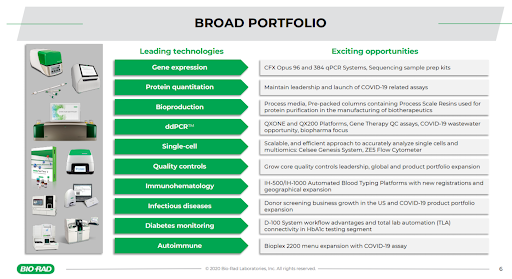

Bio-Rad divides its earnings into three different segments: Life Science, Clinical Diagnostics, and Other Operations. With over 9,000 different machines to sell, Bio-Rad has an extremely broad portfolio of equipment they sell to their customers.

Source: Bio-Rad Business 2021-2023 Outlook Presentation

In fact, Bio-Rad is operating a good business model, with various income streams. Earnings and revenue have been growing year after year, so what exactly is the problem?

Bio-Rad’s P/E Issue

To find the issue we are looking for, we will have to look at Bio-Rad’s financial data.

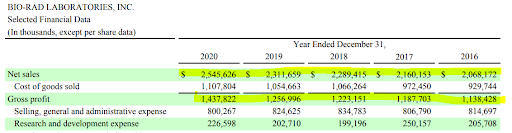

Source: Bio-Rad 2020 Annual Report

As we can see, Bio-Rad’s net sales and gross profits are showing healthy growth of around 4.5% a year. Expenses have been kept in check and have not seen any dramatic jumps. Nothing to be alarmed about here.

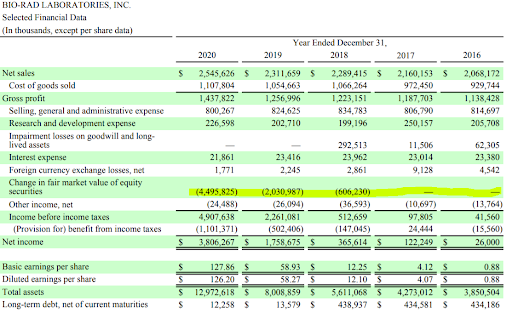

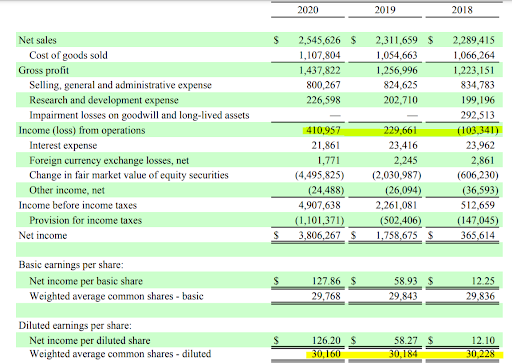

Source: Bio-Rad 2020 Annual Report

Looking further down however, for 2019 and 2020 there are significant increases in net income and earnings per share (EPS). In fact, net income and EPS grew over 220% over the past two years!

How can this be? We already determined that revenues and gross profits were growing at a 4.5% pace, so how did Bio-Rad report such a dramatic spike in earnings?

The answer lies by looking at the income statement as a whole.

Source: Bio-Rad 2020 Annual Report

Here, we can see exactly what is causing this earnings jump. It seems over the past few years, Bio-Rad has realized some gains on some securities that they owned for a hefty profit of over $7B. This realization of gains has contributed to the bottom line earnings, which is causing that 220% earnings spike.

So what gain did Bio-Rad realize? Digging further into the annual report, we can see that Bio-Rad realized their gains of their position in Sartorius AG.

Source: Bio-Rad 2020 Annual Report

So what does this mean? While this realization of gains is not necessarily a bad thing we can see that the earnings are not due to operations, but because of the selling of securities. This is an important distinction to make, since it is important to understand that the actual business of Bio-Rad is not compounding at a 220% rate.

Making Adjustments

Now that we have done our investigating let’s try and properly calculate a better ratio of Bio-Rad earnings based on its business operations. We can do this a few ways.

Operating Income P/E

Calculating Bio-Rad’s P/E ratio based on its business operations is actually pretty simple. We simply need to calculate the income from operations, which is actually already calculated for us in the comprehensive income statement.

Source: Bio-Rad 2020 Annual Report

So, if we take the total income from operations in 2020 divided by the total shares outstanding, have an adjusted EPS of $13.60. Now we simply take the current market value per share (which is $559.98 at the time of writing) and divide it by the adjusted EPS ($13.60), which gets us an adjusted P/E of 41.1.

Now I don’t have to tell you that a P/E of 41 is a far cry from the P/E of 4 that we took at face value. I guess I did just tell you though…

Accrual Ratio

Another way to calculate the validity of earnings is by using the accrual ratio. The accrual ratio is a way to calculate how much of the company’s earnings are derived from cash.

To calculate the accrual ratio, the formula is: Net Income – Free Cash Flow/Total Assets. Bio-Rad’s accrual ratio is currently sitting at a .25, which is not necessarily good (negative numbers are good here).

Simply Wall St. has an article describing the Bio-Rad’s accrual ratio situation in depth, I highly recommend you take a read.

Why Research Matters

Let me be clear here, Bio-Rad is not a bad business. They are actually maintaining quality operations by creating machines that have likely saved many lives. Shareholder value is not necessarily being eroded here either.

But viewing the company as a value investment, this example with Bio-Rad is a good reminder how “lazy value investing” can actually be detrimental to your returns. Many investors would simply look at the P/E ratio, see a low number, and buy without conducting further research thinking they are getting a great deal. After digging deep through the annual report and financial statements, we realized there was more to the story.

This is why I have always been put off by most institution’s definition of value investing. Proper value investing is intelligent investing. Intelligent investing is conducting thorough research, buying a stock for cheaper than what it is worth, and maintaining discipline by sticking to the process.